July 28, 2026

What Drives China's Record-Breaking Smelter Capacity Utilisation?

The global copper smelting industry operates within complex technological frameworks where capacity optimisation strategies determine market positioning and competitive advantages. Modern pyrometallurgical processes require sophisticated coordination between concentrate sourcing, operational efficiency metrics, and by-product revenue streams to maintain sustainable margins during volatile market conditions.

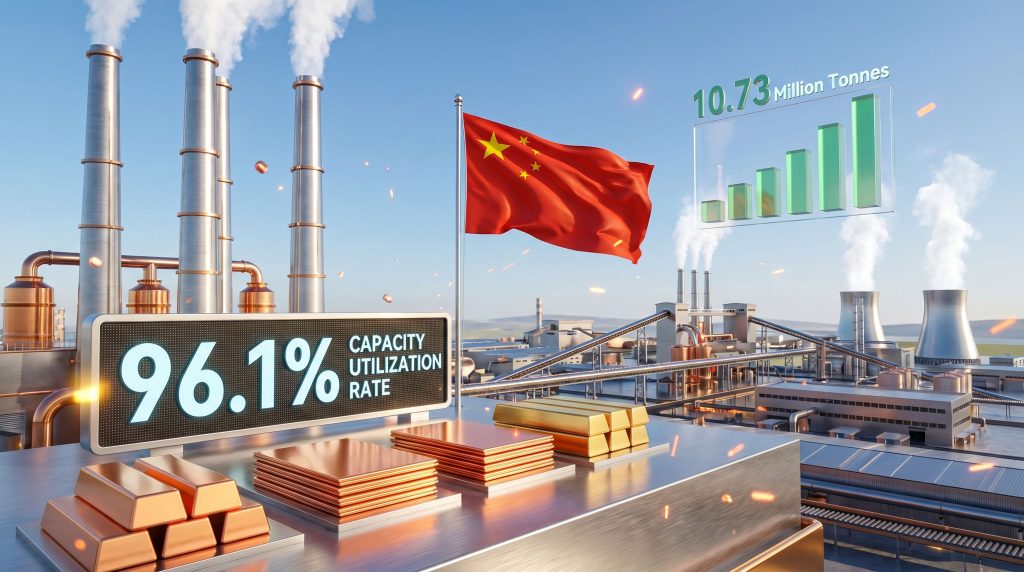

China's smelting infrastructure achieved unprecedented operational levels in March 2026, with active capacity reaching 10.73 million tonnes according to Earth-i's SAVANT satellite monitoring index. This milestone represents a 775,000-tonne increase from March 2025 levels and stands 1.49 million tonnes above the three-year average, demonstrating sustained expansion beyond typical seasonal variations.

The capacity active record of Chinese smelters reflects sophisticated operational management during challenging market conditions. With inactive capacity dropping to just 3.9% in March 2026, Chinese facilities operate at 96.1% utilisation rates, significantly outperforming the global average of 88.3% derived from worldwide inactive capacity of 11.7%.

Understanding the 10.73 Million Tonne Milestone

Earth-i analysts attribute this performance improvement to downstream demand recovery following what they characterised as a buyer resistance period that had suppressed international refined copper imports during January's record pricing environment. This structural shift from demand suppression to normalisation indicates sophisticated inventory management strategies across the Chinese industrial base.

The achievement extends beyond utilisation rate optimisation to encompass continuous infrastructure development. Chinese smelting capacity expansion has proceeded alongside efficiency improvements, creating dual pathways for output growth through both new facility commissioning and enhanced productivity from existing assets.

These remarkable performance levels align with broader copper prices insights showing sustained market strength. Furthermore, the expansion supports the global copper supply forecast projections for increased processing capacity.

Key Performance Metrics:

- Active capacity utilisation: 96.1% (March 2026)

- Monthly improvement: 1.1 percentage point increase from February

- Annual capacity growth: 775,000 tonnes above March 2025

- Three-year differential: +1.49 million tonnes versus historical average

Economic Factors Behind Peak Performance

Chinese smelters demonstrate resilience through integrated by-product revenue optimisation, particularly sulfuric acid monetisation during supply-constrained periods. Current sulfuric acid pricing reached US$210 per tonne in April 2026, representing a 74% increase from January levels, providing crucial margin support as treatment charges deteriorated into negative territory.

This dual-revenue model enables Chinese operators to maintain profitability despite challenging primary revenue conditions. Facilities equipped with advanced sulfuric acid recovery systems convert traditional waste streams into revenue-positive output, creating structural competitive advantages unavailable to non-integrated smelters globally.

The operational flexibility extends to concentrate sourcing strategies, where Chinese smelters leverage vertical integration partnerships and geographic proximity to key supply regions. This positioning enables continued operations during concentrate scarcity periods that force capacity reductions elsewhere.

How Do Global Supply Chain Dynamics Affect Chinese Smelter Operations?

Treatment and refining charge economics reveal the structural tensions underlying global copper concentrate markets. Spot market conditions reached approximately -US$78.50 per tonne in April 2026, representing a dramatic reversal from the positive US$50 per tonne recorded in January 2024. This US$128.50 swing demonstrates unprecedented concentrate scarcity pressures.

Satellite data shows record copper smelter activity in China, confirming operational optimisation across the sector. Additionally, analysis indicates that Chinese smelter capacity utilisation has driven copper prices near record highs through sustained demand.

Concentrate Availability and Sourcing Strategies

The benchmark annual TC/RC agreement between Antofagasta and major Chinese smelters established US$0 per tonne for 2026 contracts, marking the lowest annual rate ever negotiated in industry history. This baseline reflects structural tightness where concentrate producers command premium pricing power relative to downstream processing facilities.

Indonesian export restrictions compound supply chain pressures, with the Batu Hijau concentrate export permit scheduled for expiration at month-end April 2026. This regulatory change removes material tonnages from international markets, forcing greater competition among global smelters for remaining available concentrate supplies.

Simultaneously, the Kamoa-Kakula facility in the Democratic Republic of Congo initiated anode production in late 2025, absorbing its 500,000-tonne annual capacity through internal vertical integration rather than export markets. This removes high-grade concentrate from international trading channels while demonstrating the strategic value of mine-to-metal integration.

Regional Supply Disruptions:

- Iran: Two smelters with 400,000 tonnes combined capacity offline

- Australia: Mount Isa facility (300,000 tonnes) under extended maintenance

- Indonesia: Batu Hijau export permit expiration imminent

- DRC: Kamoa-Kakula concentrate now internally consumed

Treatment Charge Economics in Negative Territory

The compression of TC/RC rates into negative territory creates acute margin pressure for non-integrated smelting operations. Chinese facilities benefit from superior positioning through multiple revenue streams, geographic proximity to key markets, and vertical integration structures that provide greater operational flexibility during concentrate shortage periods.

European smelters demonstrate relative resilience with 6.2% regional inactive capacity, compared to 32.3% in North America and 27.4% in South America. This performance differential suggests varying degrees of operational efficiency, cost structure optimisation, and access to concentrate supplies across global regions.

The sulfuric acid pricing surge amplifies competitive advantages for Chinese operators equipped with advanced by-product recovery systems. Traditional waste stream monetisation becomes increasingly valuable during periods when primary revenue margins compress, highlighting the strategic importance of integrated process technologies.

What Are the Structural Implications of China's Smelting Dominance?

China's smelting sector demonstrates systematic capacity expansion aligned with long-term demand projections for electrification and clean energy infrastructure. The 10.73 million tonnes of active capacity positions Chinese facilities to capture disproportionate value from global copper demand growth estimated to reach 33 million tonnes by 2035 and 37 million tonnes by 2050 according to International Energy Agency forecasts.

This expansion forms part of broader copper-uranium investment trends across Asian markets. In contrast, the US copper production overview shows challenges in maintaining competitive smelting operations.

Capacity Expansion Timeline and Market Share Evolution

| Regional Performance | Inactive Capacity (%) | Monthly Change | Three-Year Average |

|---|---|---|---|

| China | 3.9% | -1.1 percentage points | Not specified |

| Europe | 6.2% | Not specified | Not specified |

| Asia-Pacific | 18.7% | Not specified | 5.7% |

| North America | 32.3% | +10.3 percentage points | Not specified |

| South America | 27.4% | Not specified | Not specified |

The data reveals systematic underperformance in Western Hemisphere facilities, with North American smelters experiencing 10.3 percentage point deterioration in a single month. This suggests structural challenges beyond temporary maintenance issues, likely reflecting unfavourable economics under current TC/RC conditions and elevated compliance costs.

Regional Competition and Market Positioning

Australian smelting faces particular challenges, exemplified by Mount Isa's extended maintenance outage contributing to elevated Asia-Pacific regional inactivity rates. The 300,000-tonne facility remains offline beyond typical maintenance windows, highlighting operational challenges facing non-Chinese facilities during concentrate-scarce periods.

Iranian facilities compound global capacity constraints, with two smelters representing 400,000 tonnes combined capacity maintaining extended downtime periods. These disruptions remove material processing capacity from global markets while simultaneously affecting sulfuric acid supply chains, creating dual pressures on operational economics.

The concentration of operational capacity within China creates strategic leverage over global copper supply chains. Chinese dominance extends beyond volume to encompass technological capabilities, integrated operations, and preferential access to emerging African concentrate sources through vertical partnerships and strategic investments.

Which Operational Metrics Define Smelting Industry Performance?

Earth-i's SAVANT monitoring system provides unprecedented transparency into global smelting operations, tracking approximately 95% of worldwide capacity through satellite-based detection methods. This technological advancement enables real-time assessment of operational changes within 4-6 week reporting cycles, superior to traditional industry reporting mechanisms.

The capacity active record of Chinese smelters demonstrates how operational excellence translates to market leadership. This achievement reflects the broader global copper production trends showing Asia's increasing dominance.

Capacity Utilisation Benchmarking

The 96.1% utilisation rate achieved by Chinese smelters represents optimal operational efficiency under current market conditions. This performance level indicates sophisticated maintenance scheduling, supply chain coordination, and demand forecasting capabilities that maximise productive capacity whilst maintaining equipment reliability.

Global benchmarking reveals significant regional disparities in operational performance. Chinese facilities operate 7.8 percentage points above the global average, demonstrating systematic advantages in operational management, technology deployment, and market positioning relative to international competitors.

Operational Performance Hierarchy:

- China: 96.1% utilisation (3.9% inactive)

- Europe: 93.8% utilisation (6.2% inactive)

- Global Average: 88.3% utilisation (11.7% inactive)

- Asia-Pacific (ex-China): 81.3% utilisation (18.7% inactive)

- South America: 72.6% utilisation (27.4% inactive)

- North America: 67.7% utilisation (32.3% inactive)

Technology Integration and Process Efficiency

Chinese smelters leverage advanced pyrometallurgical processes optimised for by-product recovery, particularly sulfuric acid capture systems that convert environmental compliance requirements into revenue opportunities. This technological integration provides margin protection during periods of compressed primary product economics.

The ability to monetise sulfuric acid production becomes increasingly valuable during supply disruption periods. Current pricing at US$210 per tonne reflects supply constraints originating from Iranian conflict impacts, creating windfall revenues for facilities equipped with appropriate recovery infrastructure.

Maintenance scheduling optimisation enables Chinese facilities to minimise downtime during peak demand periods whilst maintaining equipment reliability. Extended maintenance windows observed at facilities like Mount Isa suggest operational challenges that Chinese operators have systematically addressed through advanced planning and equipment management protocols.

How Do Commodity Price Dynamics Impact Smelting Economics?

Copper futures reached US$6.11 per pound (US$13,480 per tonne) in late April 2026, approaching historical highs established during January's supply disruption period. This price recovery of over 5% weekly gains reflects sustained demand strength combined with structural supply constraints affecting global concentrate availability.

Copper Price Correlation with Smelting Activity

The January 2026 pricing peak briefly exceeded US$14,500 per tonne during intraday trading, driven by supply disruptions across multiple mining operations and inventory accumulation in response to tariff uncertainties. Current pricing levels position copper within 2% of historical closing records, indicating sustained fundamental strength.

Price elasticity in smelting demand demonstrates greater resilience in integrated operations compared to standalone processing facilities. Chinese smelters maintain operational continuity through diversified revenue streams, whilst Western Hemisphere facilities experience capacity reductions when primary product margins compress below operational thresholds.

Forward market structures indicate continued supply tightness, with term structure patterns reflecting expectations for sustained elevated pricing through 2026. This environment favours smelters with operational flexibility and integrated supply chain positioning over facilities dependent on spot concentrate procurement.

By-Product Revenue Optimisation

Sulfuric acid market dynamics create significant revenue opportunities for properly equipped facilities. The 74% price increase from January to April 2026 demonstrates how geopolitical supply disruptions can transform secondary revenue streams into primary profit drivers for integrated operations.

Chinese smelters benefit from geographic proximity to major sulfuric acid consumption markets, reducing transportation costs and enabling rapid response to price signals. This positioning advantage becomes increasingly valuable during periods of supply constraint when logistics optimisation determines market access and pricing realisation.

Precious metal recovery from concentrate processing provides additional revenue diversification, though specific production volumes and pricing realisations remain proprietary to individual operators. The cumulative impact of optimised by-product recovery enables Chinese facilities to maintain operations during periods when treatment charges alone would not support economic processing.

Investment Considerations:

This analysis contains forward-looking statements and projections that involve inherent risks and uncertainties. Commodity markets remain subject to volatile pricing, regulatory changes, and operational disruptions that can materially affect financial performance. Readers should conduct independent research and consider consulting qualified investment professionals before making investment decisions based on this information.

The capacity active record of Chinese smelters represents a fundamental shift in global copper processing economics, with implications extending beyond traditional supply-demand modelling to encompass technological capabilities, operational excellence, and strategic market positioning that may persist through multiple commodity cycles.

Could the Next Mining Discovery Transform Your Investment Portfolio?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of the broader market. Explore Discovery Alert's historic discoveries page to understand how major mineral finds can generate exceptional returns, then begin your 14-day free trial to position yourself ahead of the market.