August 4, 2026

The Architecture of Retail Risk: How China's Precious Metals Crackdown Reflects Deeper Market Forces

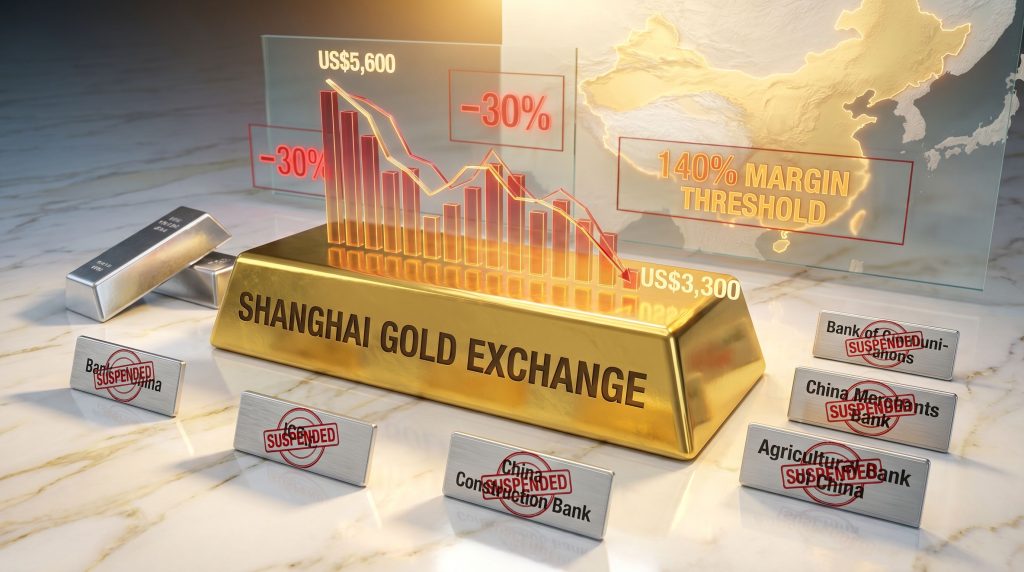

When commodity markets turn volatile, the institutions closest to retail exposure are typically the first to recalibrate. That dynamic is playing out with unusual clarity in China's precious metals sector, where Chinese banks suspend individual trading on the Shanghai Gold Exchange — a coordinated withdrawal from SGE-linked retail products by six of the country's largest banks that reveals something more structured than routine portfolio management. It reflects a deliberate, system-wide response to a rapidly deteriorating risk environment, and it carries meaningful implications for how China manages the intersection of retail finance and commodity speculation.

When big ASX news breaks, our subscribers know first

What Is Actually Happening: A New Customer Exclusion, Not a Market Collapse

The framing matters here. When Chinese banks suspend individual trading on the Shanghai Gold Exchange, the immediate instinct is to interpret this as a broader signal of market failure. The reality, however, is more nuanced. The current wave of suspensions applies specifically to the opening of new individual accounts linked to SGE precious metals trading products. Customers who already hold these accounts retain full trading access across buy, sell, and position management functions.

What has changed is the gateway. Over-the-counter banking channels, online platforms, and mobile banking applications have all been closed to new retail participants, effectively sealing the entry point without dismantling the existing architecture.

The institutions involved represent the core of China's state-linked and commercial banking system:

| Institution | Action Taken | Effective Date |

|---|---|---|

| Bank of China | Full suspension of SGE individual services | Saturday |

| ICBC | Halted new individual gold, silver and trading accounts | Saturday |

| Bank of Communications | Suspended SGE-linked new account openings | Saturday (noon) |

| China Construction Bank | Suspended new SGE product account openings | Monday |

| China Merchants Bank | Suspended new account applications | Saturday |

| Agricultural Bank of China | Suspended new applications with investor risk warning | Saturday |

The near-simultaneous timing across institutions of this scale is not coincidental. When six systemically important financial entities move in lockstep within the same weekend window, the probability of independent parallel decision-making is negligible. The coordination pattern strongly points toward centralised risk guidance flowing through China's banking regulatory infrastructure.

The Price Collapse That Triggered the Response

To understand the urgency behind this institutional response, the price context is essential. Gold reached a peak of approximately US$5,600 per ounce earlier in 2025, a level that represented the culmination of years of geopolitical accumulation narratives, de-dollarisation momentum, and central bank gold demand cycles. That peak attracted a significant wave of retail participation in China, with millions of new investors accessing leveraged SGE-linked products through their primary banking applications.

The reversal has been severe. Spot gold briefly traded below US$4,000 per ounce, marking the first time that threshold had been breached since late 2025. The drawdown from peak levels represents a loss of nearly 30% of market value within a compressed timeframe, placing this correction among the sharpest in modern gold market history.

Several macro forces have converged to produce this outcome:

- US Dollar Appreciation: A strengthening greenback applies consistent downward pressure on dollar-denominated commodities, compressing gold prices in both nominal and real terms.

- Persistent Rate Environment: Investor expectations that the US Federal Reserve will maintain elevated interest rates for an extended period have materially reduced the attractiveness of non-yielding assets.

- Rising Treasury Yields: Higher US bond yields draw capital away from gold, as gold and bond yields demonstrate an inverse relationship that increases the opportunity cost of holding a zero-yield asset.

- Repriced Rate Cut Timelines: The market's recalibration of when and how deeply the Fed might cut rates has been one of the more direct catalysts for gold's correction trajectory.

"Gold's inverse relationship with real yields is one of the most well-documented dynamics in commodity economics. When real yields rise, gold's relative appeal diminishes, and leveraged retail positions become disproportionately exposed to fast-moving drawdowns."

How the Risk Escalation Unfolded: A Graduated Tightening Process

Chinese financial institutions did not leap directly to account suspension. The tightening followed a deliberate escalation sequence that reflects a structured internal risk management process:

- Margin Requirement Hikes: Bank of China and China CITIC Bank were among the first to raise margin thresholds on precious metals trading products. Some requirements reached 140%, a level that effectively forces most retail participants out of leveraged positions by making them economically unviable.

- Dormant Account Closures: Before the suspension wave, major institutions began shutting inactive precious metals accounts as part of broader portfolio hygiene exercises, reducing latent exposure without triggering market headlines.

- New Account Suspension: The coordinated halt on new individual SGE-linked account openings across all retail channels — the stage now dominating public attention.

- Full Product Withdrawal: ICBC announced it will cease offering individual precious metals trading linked to the SGE entirely from July 24, with Postal Savings Bank of China, Ping An Bank, and China Guangfa Bank announcing parallel exits from the same product category.

This graduated escalation ladder reveals that the banking sector was not reacting impulsively to a single data point, but managing an evolving risk exposure through incremental policy tightening before reaching the threshold of full suspension. For further context on how these decisions were reported, Chinese banks wind down retail gold trading coverage from Caixin Global provides additional institutional detail.

Historical Precedent: China Has Done This Before

The current episode is not without precedent in Chinese financial market history. Following the 2020 crude oil futures crisis, in which retail investors suffered devastating losses on leveraged commodity products tied to negative oil prices, major Chinese banks similarly suspended new account openings for commodity trading products. The trauma of that event reshaped the regulatory appetite for retail commodity speculation across the Chinese banking system.

Perhaps more striking is the fact that several institutions had already suspended new precious metals account openings for approximately five years before this latest round of suspensions. The current wave is therefore better understood as a deepening and broadening of a structural de-risking posture that has been building across China's retail financial landscape since 2020, rather than a sudden policy reversal.

"China's regulatory history in retail commodity markets consistently prioritises systemic stability over broad market participation. Volatility thresholds tend to trigger access restrictions rather than market structure reforms, a pattern that has now repeated across oil futures in 2020 and precious metals in the current cycle."

Silver Markets: A Parallel Disruption

The precious metals disruption in China extended beyond gold. The Shanghai Futures Exchange imposed an indefinite suspension of silver futures trading, citing abnormal market conditions without specifying the precise nature of the abnormality at the time of announcement.

The dual suspension — covering gold through the SGE and silver through the SHFE — is significant because it illustrates that regulatory concern was not isolated to a single metal or a single trading venue. The breadth of the intervention signals that Chinese authorities were managing a systemic precious metals volatility event rather than a product-specific anomaly.

Silver's dual role as both a monetary and industrial metal adds additional complexity. The metal's price dynamics are more volatile than gold during macro-driven sell-offs, and the SHFE's decision to suspend silver futures during this period reflects awareness that silver's dual-use demand profile amplifies volatility in ways that create disproportionate retail risk. Furthermore, gold and silver volatility during periods of trade-related uncertainty compounds these dynamics considerably.

The next major ASX story will hit our subscribers first

Separating Short-Term Noise from Long-Term Structural Demand

One of the most important analytical distinctions to draw in the current environment is between speculative retail trading disruption and China's underlying structural role in global gold demand. These are not the same thing, and conflating them produces misleading conclusions.

| Factor | Short-Term Impact | Long-Term Outlook |

|---|---|---|

| Retail account suspensions | Reduced speculative trading volumes | Neutral to positive (removes excess speculation) |

| Margin requirement increases at 140% | Forced deleveraging of retail positions | Stabilising for market structure |

| Price correction from peak levels | Dampened near-term consumer sentiment | May stimulate physical gold buying |

| Institutional risk tightening | Lower bank exposure to commodity volatility | Supports systemic financial stability |

Physical gold purchases through retail jewellers, banks' physical gold product lines, and gold ETFs remain entirely unaffected by the SGE-linked trading suspensions. The restrictions target margin-based speculative instruments, not the physical gold market infrastructure that underpins China's longer-term demand profile.

China's role as a primary driver of global gold demand rests on foundations that include central bank accumulation strategies, a deeply embedded cultural preference for physical gold ownership, and ongoing diversification away from US dollar-denominated reserve assets. None of these structural demand pillars are materially altered by the suspension of leveraged retail trading accounts. In addition, gold safe-haven demand driven by geopolitical uncertainty continues to underpin the metal's long-term investment thesis.

Investor Risk Exposure: Understanding the Mechanics of Forced Deleveraging

For retail investors currently holding SGE-linked positions, the risk environment requires careful assessment. Those who entered leveraged positions near the price peak face potential unrealised losses in the range of 20 to 30%, depending on entry points and the degree of leverage applied.

The 140% margin requirement imposed by certain institutions creates a forced deleveraging mechanism with a specific operational logic:

- Investors whose margin ratios fall below the required threshold receive margin calls requiring immediate capital injection.

- Failure to meet margin calls within specified timeframes triggers automatic position reduction or liquidation by the bank.

- Forced liquidations at current price levels crystallise losses that might otherwise be recoverable through patience in an unlevered position.

- The liquidation cascade effect — where multiple forced sellers hit the market simultaneously — can compound price weakness and accelerate the correction.

"Retail investors in leveraged precious metals products should carefully assess their current exposure. In environments of forced deleveraging, losses can extend significantly beyond initial capital at risk, particularly when margin call timelines are compressed."

Agricultural Bank of China's decision to accompany its suspension announcement with an explicit investor risk warning reflects regulatory sensitivity to the consumer protection dimension of this event, acknowledging that the speed of the correction may have left many participants unprepared for the scale of their exposure. Reporting on how Chinese banks suspended precious metal account openings provides further context on the consumer protection messaging surrounding these announcements.

What China's Response Reveals About Commodity Market Governance

The speed, breadth, and coordination of China's banking sector response to precious metals volatility carries broader lessons for understanding how the country's financial regulatory architecture operates under stress.

Chinese regulators have consistently demonstrated a preference for access restriction over market structure reform when commodity volatility reaches thresholds that create systemic retail risk. This interventionist posture reflects a fundamentally different philosophical approach to retail commodity market participation than is typical in Western financial systems, where volatility is generally managed through disclosure requirements and margin frameworks rather than outright participation limits.

The simultaneous tightening across both gold and silver markets — spanning two separate exchanges and six major banking institutions — indicates that the response was calibrated to manage contagion risk across the entire precious metals complex rather than addressing isolated pockets of exposure.

For global gold markets, the reduction in Chinese retail speculative demand may contribute to near-term price softness. However, the removal of leveraged speculative positions from the Chinese retail market could paradoxically provide a more stable demand floor over time, as the market composition shifts back toward physical buyers and institutional participants with longer investment horizons and lower propensity for panic-driven selling.

Frequently Asked Questions

Can existing customers still trade gold through Chinese banks?

Yes. The suspensions apply exclusively to new account openings. Customers who already hold SGE-linked precious metals trading accounts retain full access to buy, sell, and manage their positions without disruption.

Why are multiple banks acting at the same time?

The near-simultaneous timing across six major institutions strongly suggests centralised regulatory guidance from Chinese banking authorities, though individual banks have characterised the decisions as internal risk management responses to current market conditions.

Does this affect physical gold purchases in China?

No. The suspension covers SGE-linked margin trading products for individuals. Physical gold purchases through retail jewellers, banks' physical gold products, and gold ETFs remain fully operational and unaffected.

What is the Shanghai Gold Exchange?

The SGE is China's primary regulated marketplace for gold trading, operating under the oversight of the People's Bank of China. It facilitates both spot gold transactions and investment products linked to gold pricing for institutional and individual participants.

Is this suspension permanent?

Banks have not indicated permanent closure of retail precious metals access. Historical precedent from the 2020 commodity trading suspensions suggests these restrictions are likely to be modified or lifted once market conditions stabilise to levels considered acceptable by regulatory authorities.

What triggered the silver futures suspension on the Shanghai Futures Exchange?

The SHFE cited abnormal market conditions as the basis for its indefinite suspension of silver futures trading. Specific details regarding the precise nature of those abnormal conditions were not publicly disclosed at the time of the announcement.

Want to Know When the Next Major Precious Metals Discovery Hits the ASX?

While Chinese banks are restricting access to leveraged gold and silver trading, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant precious metals discoveries directly to subscribers — turning complex mineral data into clear, actionable opportunities. Explore historic discoveries and their market returns, then begin your 14-day free trial to position yourself ahead of the broader market.