June 22, 2026

When Mexico's Most Trusted Offshore Contractors Walk Away

The relationship between a state-owned oil company and its preferred domestic contractors is rarely transactional in isolation. It is the product of decades of institutional alignment, regulatory familiarity, and shared risk tolerance. When that relationship begins to fracture, the signal is rarely confined to a single procurement event. It points toward something more fundamental: a recalibration of how private capital assesses sovereign commercial risk.

The collapse of PEMEX's tender for the Mistle-1EXP drilling platform in June 2026 is precisely that kind of signal. The sequential departure of multiple domestic contractors, culminating in CICSA exits PEMEX drilling platform tender without submitting a single technical or economic bid, exposes tensions within Mexico's offshore contracting ecosystem that no amount of administrative relaunching can resolve without structural reform.

When big ASX news breaks, our subscribers know first

What the Mistle-1EXP Tender Collapse Actually Reveals

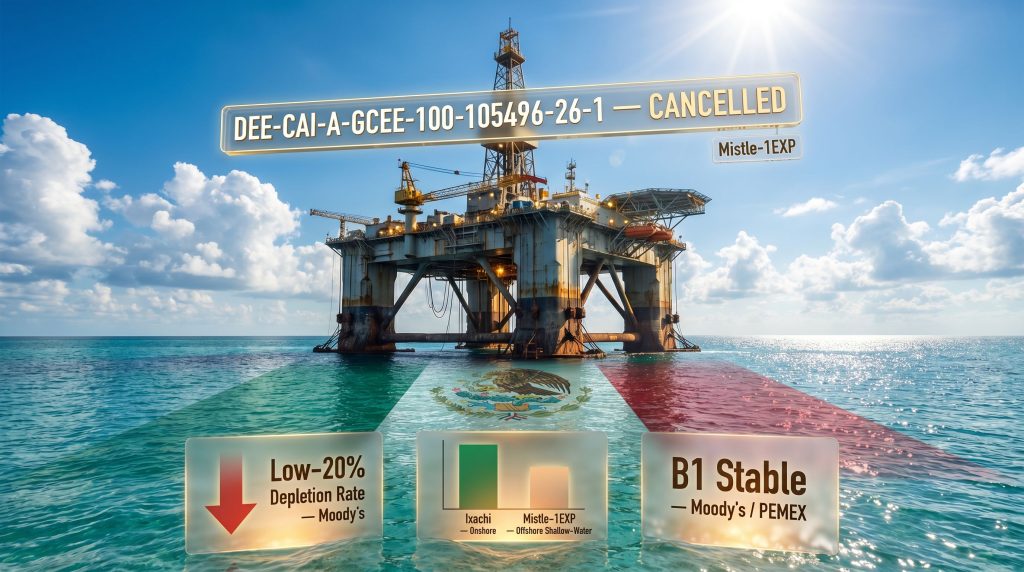

The Anatomy of Procedure DEE-CAI-A-GCEE-100-105496-26-1

Issued on April 28, 2026, tender procedure DEE-CAI-A-GCEE-100-105496-26-1 was designed to secure the lease of a semisubmersible offshore drilling platform for the Mistle-1EXP exploratory well. The well sits in shallow Gulf of Mexico waters off the Tabasco coast, near the town of Sánchez Magallanes. By June 17, 2026, PEMEX had cancelled the entire process through official notice PM-DEE-SPTMP-GPRPM-445-2026, less than seven weeks after issuance.

That timeline alone is diagnostically important. Competitive offshore procurement processes typically require months of technical evaluation, financial modelling, and bid preparation. A collapse within weeks indicates that the fundamental parameters of the tender failed to clear the viability threshold for contractors before they even reached the bid preparation stage.

| Specification | Detail |

|---|---|

| Tender Procedure Number | DEE-CAI-A-GCEE-100-105496-26-1 |

| Contract Type | Lease only, no purchase option |

| Minimum Water Depth Capability | 328 feet (shallow-water classification) |

| Maximum Drilling Depth | 24,600 feet |

| Scope | Platform lease plus comprehensive maintenance |

| Target Well | Mistle-1EXP exploratory well |

| Location | Gulf of Mexico, Tabasco coast, near Sánchez Magallanes |

| Tender Issued | April 28, 2026 |

| Cancellation Date | June 17, 2026 |

| Cancellation Notice | PM-DEE-SPTMP-GPRPM-445-2026 |

The lease-only structure, combined with comprehensive maintenance obligations attached to a platform PEMEX would never own under the contract terms, created a risk profile that distributed operational burden heavily onto the contractor without providing the offsetting benefit of asset ownership. That combination proved systematically unattractive. Furthermore, PEMEX's challenges awarding offshore platform contracts have been well documented, suggesting this outcome was far from unprecedented.

How a Competitive Field Collapsed to a Single Bidder

The disintegration of the Mistle-1EXP tender unfolded across several distinct stages, each involving a different category of participant:

Formally documented withdrawals:

- CICSA (Grupo Carso subsidiary): Filed a letter of apology in lieu of a technical or economic proposal, a procedurally unusual move that signals deliberate strategic disengagement rather than operational incapacity

- SCJ Constructora: Declined participation without advancing to bid submission

Informally reported withdrawals (per Reforma's Capitanes column):

- COSL México: Exited without formal notification

- Energy & Oil Green Solutions: Also abandoned the process without formal documentation

Sole remaining participant:

- An international consortium comprising OGD Services Holdings Limited, Essar Shipping DMCC, Energy II Limited, and Corporación Gargnano S.A. de C.V., a group with Indian corporate participation, submitted the only valid proposal

A procurement process that contracts to a single bidder, particularly one with no established operational relationship with PEMEX, is functionally non-competitive under standard public procurement governance principles. PEMEX's decision to cancel the process outright rather than proceed with a sole-source award reflects an institutional awareness that awarding under those conditions would carry both reputational and operational consequences.

PEMEX's official cancellation rationale cited two factors: changes to its leasing strategy, and required adjustments to technical specifications. Neither factor was elaborated upon in public communications. No timeline for relaunching the tender has been provided.

CICSA Exits PEMEX Drilling Platform Tender: A Strategic Pattern, Not an Isolated Decision

Reading the Withdrawal Through the Lakach Precedent

The Mistle-1EXP platform tender was not the first occasion in 2026 in which a Grupo Carso-affiliated entity evaluated an offshore hydrocarbon commitment with PEMEX and then chose not to deploy capital. It was the second, occurring within approximately two months of Carlos Slim's public articulation of reservations about the Lakach deepwater gas field development.

In May 2026, Slim described the Lakach project, valued at approximately US$1.88 billion, as economically irrational in its current form, arguing that its technical complexity and cost structures were disproportionate relative to the gas volumes it could deliver. He specifically identified the Ixachi onshore field as capable of supplying comparable volumes at substantially lower operational complexity.

The Mistle-1EXP withdrawal follows an identical decision architecture: evaluation of the opportunity, assessment of the risk-return structure, and disengagement before capital commitment. The key distinction is scale. Lakach was a multi-year development commitment valued in billions. The Mistle-1EXP platform lease was a narrower infrastructure contract. Yet the same logic produced the same outcome.

This convergence matters analytically because it suggests Grupo Carso is not responding to project-specific deficiencies but applying a consistent capital allocation filter across offshore hydrocarbon opportunities in Mexico, regardless of contract scale.

Comparing Onshore and Offshore Risk Profiles in Mexico's Upstream Sector

The preference for onshore projects like Ixachi over offshore commitments like Lakach and Mistle-1EXP reflects measurable differences in risk structure:

| Risk Dimension | Onshore (e.g., Ixachi) | Offshore Shallow-Water (e.g., Mistle-1EXP) |

|---|---|---|

| Capital Intensity | Moderate | High |

| Technical Complexity | Lower | Higher |

| Contractor Liability Exposure | Contained | Broader (maintenance obligations) |

| PEMEX Specification Stability | Generally stable | Subject to revision (as demonstrated) |

| Competitive Tender Participation | Broader field | Narrowing |

| Depletion Rate Pressure | Moderate | Severe (low-20% range per Moody's) |

| Asset Ownership Pathway | Possible | Absent under lease-only terms |

The absence of a purchase option in the Mistle-1EXP lease structure is particularly significant from a contractor perspective. In offshore drilling markets, platform ownership provides long-term asset value that can offset the elevated operational costs and technical risks of marine environments. A lease-only structure removes that offset entirely, leaving contractors exposed to operational complexity without compensating upside.

The Upstream Stakes: Why This Well Cannot Wait

Depletion Rates and the Structural Urgency of Exploration

Moody's has flagged that PEMEX's primary producing fields are declining at underlying rates in the low-20% range on a production-weighted basis. That figure represents the rate at which existing reserves are being drawn down each year without adequate replacement through new discovery or development. At that pace, the operational urgency of exploratory wells like Mistle-1EXP extends well beyond individual project economics.

Moody's rates PEMEX at B1 Stable, with the Mexican sovereign government's ongoing financial support identified as a key stabilising factor. The agency has also noted that mixed development contracts deployed to date have generated only modest incremental production relative to the scale of PEMEX's depletion challenge, underscoring that contractual activity and meaningful production outcomes are not automatically correlated.

Exploratory wells in strategically identified zones are the mechanism through which PEMEX identifies reserves before committing to development-stage capital. When platform procurement for an exploratory well fails, the consequence is not simply a delayed drilling schedule. It is a gap in the reserve assessment pipeline at precisely the moment when PEMEX's production base most urgently requires replenishment data.

The Shallow-Water Tabasco Zone: Strategic Context

The Mistle-1EXP well is positioned within a broader PEMEX initiative to assess hydrocarbon potential in the shallow-water Gulf of Mexico zone off Tabasco. This region has been identified by PEMEX as material to future production capacity. The failure to secure a contracted drilling platform therefore disrupts not just a single well programme, but the sequenced exploration activity that well was designed to initiate.

Downstream consequences of the Mistle-1EXP procurement failure include:

- Indefinite delay to drilling operations at the Mistle-1EXP well

- Disruption to PEMEX's shallow-water exploration sequencing along the Tabasco coast

- Reduced visibility on reserve additions in a zone identified as strategically significant

- Erosion of production guidance credibility if exploratory timelines slip

- Compounding pressure from existing field depletion rates in the low-20% range

Structural Weaknesses in PEMEX's Offshore Procurement Design

Four Governance Failures That the Tender Exposed

The Mistle-1EXP collapse is not an isolated procurement misstep. It surfaces a set of recurring structural vulnerabilities in how PEMEX designs, issues, and manages offshore tenders:

1. Specification Instability

PEMEX's own cancellation notice acknowledged that technical specifications required adjustment, raising the question of whether the tender was issued before the well programme's operational requirements were fully defined. Releasing a tender with incomplete or evolving specifications forces contractors to price uncertainty into their risk models, which systematically increases the likelihood of withdrawal.

2. Imbalanced Risk Allocation

A lease-without-purchase-option structure combined with comprehensive maintenance obligations concentrates operational risk on the contractor without offering the asset ownership upside that could offset that exposure. This structural imbalance appears to be deterring qualified domestic bidders on a repeating basis.

3. Inadequate Pre-Tender Market Sounding

The rapid collapse of what appeared to be a competitive field, from multiple interested parties to a single international consortium, suggests that PEMEX's pre-tender engagement with the contractor market may not be accurately gauging actual appetite for specific risk configurations before a public process is launched.

4. Preferred Contractor Alignment Erosion

Historically PEMEX-aligned domestic contractors like CICSA are now applying explicit selectivity filters to offshore commitments. This represents a material shift in the informal contractor ecosystem that PEMEX has historically relied upon to maintain competitive tender fields. When that ecosystem becomes selectively disengaged, international consortia without established PEMEX relationships become the default fallback, introducing new operational integration risks.

What a Redesigned Tender Would Need to Address

Based on the structural factors that drove participant withdrawals, a revised procurement process for Mistle-1EXP platform services would benefit from addressing the following dimensions:

- Finalise specifications before issuance to eliminate mid-process revision as a contractor risk factor

- Reassess maintenance obligation allocation to determine whether partial retention by PEMEX or separation into a distinct contract lot would restore contractor interest

- Conduct formal pre-tender industry dialogue to test realistic contractor appetite before committing to a public procurement timeline

- Evaluate whether a purchase option at a defined premium would broaden the competitive field by restoring a pathway to asset ownership

- Publish a clear relaunch schedule to prevent prolonged uncertainty from further eroding domestic contractor confidence in the process

The Broader Investment Climate Signal

Private Capital Selectivity and Mexico's Upstream Future

The Mistle-1EXP tender outcome functions as a data point within a larger pattern of private capital selectivity in Mexico's upstream oil and gas sector. This pattern does not exist in isolation. Indeed, broader oil price movements and trade dynamics are also shaping the risk calculus of domestic and international contractors operating across global energy markets.

When domestic contractors with multi-decade state relationships begin applying explicit risk filters to offshore commitments and those filters produce formal tender withdrawals rather than competitive bids, the message to policymakers is structural in nature, not episodic. Three converging dynamics define the current environment:

- Fiscal constraints on PEMEX limit its ability to offer contract terms that adequately compensate contractors for the elevated risks of offshore operations

- Accelerating field depletion increases the operational urgency of new exploration while simultaneously reducing PEMEX's financial flexibility to fund exploration attractively

- Shifting private capital preferences among major domestic conglomerates are redirecting investment toward lower-complexity, higher-certainty onshore opportunities, a trend reinforced by Grupo Carso's behaviour across both the Lakach and Mistle-1EXP situations

Mexico's shallow-water exploration programme cannot be sustained on the assumption that historically aligned domestic contractors will continue absorbing offshore risk under current contract structures. A fundamental reassessment of how PEMEX designs, prices, and allocates risk in offshore procurement is a prerequisite for restoring competitive tender participation and, by extension, for advancing the reserve replacement agenda that PEMEX's depletion trajectory demands.

The Mistle-1EXP situation also introduces a less-discussed dynamic within Mexico's upstream contracting market: the growing divergence between what PEMEX's fiscal position allows it to offer and what the offshore drilling market requires to justify contractor participation. OPEC's influence on global oil markets further complicates this calculus, as shifting supply dynamics affect the commercial viability of marginal exploration projects worldwide. As global offshore rig demand has recovered following the commodity cycle downturn of the mid-2010s, contractors now have alternative deployment opportunities for specialised equipment.

A Mexican tender with suboptimal risk allocation is no longer the only option on the table for experienced offshore operators. In a softer rig market, contractors might accept less favourable terms to secure utilisation. In a tighter market, they can afford to be selective, and the Mistle-1EXP experience suggests they are exercising precisely that selectivity. Furthermore, the trade war's impact on oil prices has introduced additional volatility that makes long-term offshore commitments even harder to justify under current contract structures.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: CICSA, PEMEX, and the Mistle-1EXP Tender

What is the Mistle-1EXP well and why does it matter?

Mistle-1EXP is an exploratory well operated by PEMEX in shallow Gulf of Mexico waters off the Tabasco coast near Sánchez Magallanes. It forms part of PEMEX's reserve identification programme in a region considered strategically significant for future hydrocarbon production. The well requires a semisubmersible drilling platform, which PEMEX attempted to procure through a competitive tender that ultimately collapsed.

Why did CICSA exit the PEMEX drilling platform tender without submitting a bid?

CICSA submitted a formal letter of apology rather than a technical or economic proposal. While no public explanation was provided, the withdrawal aligns with a broader pattern of Grupo Carso-affiliated entities disengaging from complex offshore hydrocarbon commitments with PEMEX, consistent with Carlos Slim's publicly stated preference for lower-complexity onshore projects over capital-intensive offshore operations.

How many companies withdrew from the Mistle-1EXP tender?

Four companies exited before cancellation. CICSA and SCJ Constructora withdrew formally, while COSL México and Energy & Oil Green Solutions reportedly departed without formal notification according to Reforma's Capitanes column. Only one participant, an international consortium, submitted a valid proposal.

What was PEMEX's stated reason for cancelling the tender?

PEMEX cited changes to its leasing strategy and the need to revise technical specifications to meet the operational requirements of the well programme. No relaunch timeline has been announced.

What is the connection between the Mistle-1EXP tender and the Lakach gas field situation?

Both situations involve Grupo Carso-affiliated entities evaluating and then withdrawing from offshore hydrocarbon commitments with PEMEX. In the Lakach case, Carlos Slim publicly described the deepwater project as economically irrational relative to onshore alternatives. The Mistle-1EXP withdrawal followed a structurally identical logic within approximately two months.

What depletion rates are PEMEX's fields currently experiencing?

Moody's has indicated that PEMEX's primary producing fields are declining at underlying rates in the low-20% range on a production-weighted basis, establishing the strategic urgency of the exploratory activity the Mistle-1EXP well was designed to support. However, US policy changes affecting Venezuela and PDVSA demonstrate that sovereign energy companies across the region face comparable structural pressures, reinforcing that PEMEX's challenges are not entirely unique to Mexico.

Disclaimer: This article draws on publicly available information from Mexico Business News, Moody's ratings communications, and Reforma reporting. It contains forward-looking analysis and structural assessments that reflect the author's interpretation of available evidence. Nothing in this article constitutes financial or investment advice. Readers should consult qualified advisers before making decisions based on any information contained herein.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

While PEMEX's procurement struggles highlight the risks of sovereign energy exposure, savvy investors are turning their attention to ASX-listed mineral explorers — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment a significant discovery hits the exchange, transforming complex geological data into actionable opportunities. Explore historic discoveries and their extraordinary returns to understand what early positioning can mean, then begin a 14-day free trial to secure your market-leading edge.