June 15, 2026

The Governance Gap That Copper Markets Cannot Afford to Ignore

Commodity markets tend to fixate on price charts, inventory levels, and macroeconomic demand signals. What they consistently underweight is the human infrastructure that keeps ore flowing from pit to port. Labour relations in large-scale mining operations are rarely glamorous enough to dominate financial media, yet a single prolonged stoppage at a strategically sized mine can do more to tighten physical copper supply than months of incremental demand growth. The June 2026 CMOC Congo copper mine strike at Tenke Fungurume is a textbook illustration of this dynamic, and its resolution, while swift, leaves structural questions that the copper market will be forced to revisit.

When big ASX news breaks, our subscribers know first

Understanding TFM's Weight in Global Copper Supply

A Single Asset With Outsized Market Relevance

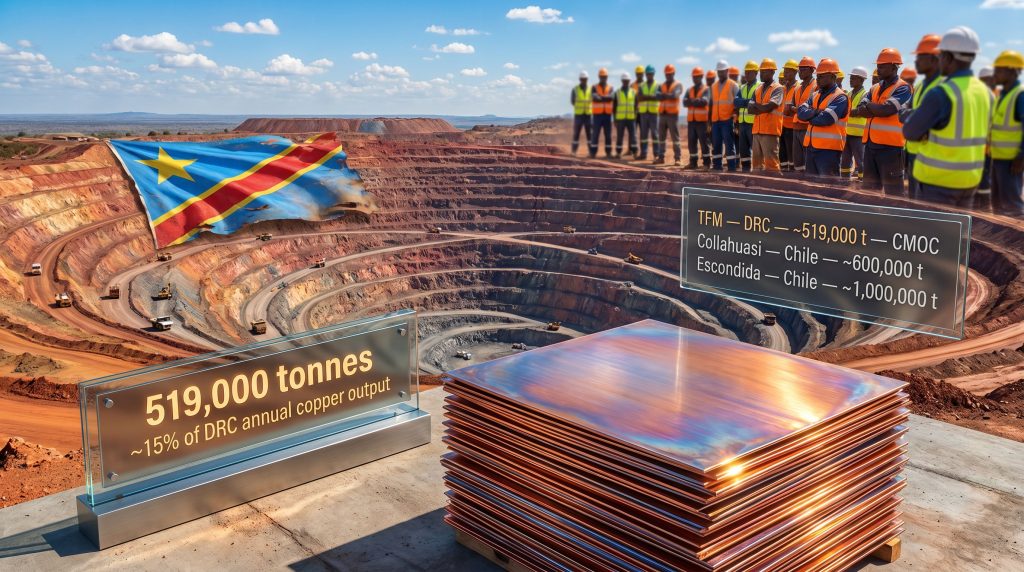

Tenke Fungurume Mining is not simply a large copper mine. It is one of the few operations globally capable of moving the needle on refined copper availability in isolation. According to reporting by Miningmx and Bloomberg, TFM produced approximately 519,000 metric tonnes of copper in 2025, a figure that equates to roughly 15% of the entire DRC's annual copper output (Miningmx, 9 June 2026; Bloomberg, 5 June 2026).

To place that in context, only a handful of operations worldwide produce more copper from a single site. Escondida in Chile, operated by BHP, sits at the top of the global rankings with output approaching 1 million tonnes annually. Collahuasi, jointly held by Glencore and Anglo American, generates roughly 600,000 tonnes. TFM sits comfortably in the tier immediately below, making it one of the most consequential single copper assets outside of South America.

| Mine | Country | Approximate Annual Output | Operator |

|---|---|---|---|

| Escondida | Chile | ~1,000,000 tonnes | BHP |

| Collahuasi | Chile | ~600,000 tonnes | Glencore / Anglo American |

| Tenke Fungurume (TFM) | DRC | ~519,000 tonnes | CMOC |

| Kamoa-Kakula | DRC | ~450,000+ tonnes | Ivanhoe Mines |

| Cerro Verde | Peru | ~450,000 tonnes | Freeport-McMoRan |

Note: Figures are approximate based on most recently available annual production data.

When CMOC's second Congolese operation, Kisanfu (KFM), is included, the company's combined in-country copper extraction reached close to 750,000 tonnes in 2024, establishing CMOC as one of the largest single-operator copper producers anywhere on the African continent (Miningmx, 9 June 2026; Bloomberg, 5 June 2026). Both mines carry an additional dimension beyond copper: they are simultaneously significant cobalt producers, giving CMOC a dual-commodity position that extends its strategic importance deep into battery metal supply chains.

The DRC's Transformation Into a Copper Superpower

The scale of TFM's output only makes sense when viewed against the broader DRC mineral wealth trajectory. The country produced less than 1 million tonnes of copper annually in the early 2010s. By 2023, the US Geological Survey was recording DRC copper output in the range of 2.5 to 2.6 million metric tonnes per year, an acceleration driven almost entirely by large-scale foreign capital, predominantly from Chinese state-affiliated and private mining groups acquiring concessions across Lualaba and Haut-Katanga provinces (USGS, Mineral Commodity Summaries, various years 2014–2024).

This transformation has repositioned the DRC as the world's second-largest copper-producing nation, a status that carries significant geopolitical and supply chain implications at a moment when copper prices are trading near multi-year record highs and structural demand growth is accelerating across multiple end-use sectors.

What Ignited the June 2026 Strike at Tenke Fungurume

The Collective Bargaining Agreement and the Exclusion Complaint

Workers at TFM began their industrial action on 1 June 2026, with the immediate trigger being a newly negotiated collective bargaining agreement (CBA) between TFM management and a designated union delegation. The central grievance was procedural rather than purely financial: rank-and-file employees alleged that the negotiations had been conducted without meaningful consultation with the broader workforce, effectively excluding them from a process that would directly govern their terms of employment.

Beyond the procedural complaint, workers raised three substantive demands:

- Inclusion of a formal housing allowance within their compensation structure

- Expanded and more accessible healthcare benefits

- Greater transparency and genuine worker representation in future CBA negotiations

What makes this dispute analytically interesting is that its primary driver was not a wage floor disagreement. It was a question of institutional legitimacy: whether the union delegation that signed the CBA had the genuine mandate of the workers it purported to represent.

Why This Type of Dispute Is Particularly Hard to Resolve

Labour relations specialists and researchers studying African mining sectors have long noted that disputes rooted in procedural exclusion rather than direct pay demands tend to resist quick resolution. A wage dispute can be settled with a pay adjustment. A legitimacy dispute requires structural reform of how workers are consulted and represented, which takes considerably longer and carries reputational costs for management regardless of outcome.

In the DRC mining sector specifically, union representation is frequently contested terrain. Multiple competing unions may claim simultaneous legitimacy over the same workforce, creating conditions where no single delegation can credibly claim to speak for all workers. When management selects one union over others as a negotiating counterpart, the risk of perceived co-optation rises sharply, particularly when the resulting agreement is seen as falling short of worker expectations.

Labour disputes in DRC mining that originate from perceived procedural exclusion, rather than pure wage demands, signal a deeper institutional deficit that pay adjustments alone cannot address. The resolution requires governance reform, not just a budget line item.

How CMOC Managed the Escalation and Achieved Resolution

A Structured Escalation Model With Financial Incentives and Legal Pressure

TFM's response to the June 2026 strike combined legal classification, ultimatum setting, financial incentives, and accountability measures in a sequenced escalation strategy. The company declared the strike illegal under applicable Congolese labour law frameworks and immediately used that designation as the foundation for its response.

| Response Phase | Action Taken | Timing |

|---|---|---|

| Legal Classification | Strike declared illegal by TFM management | Immediate |

| Return-to-Work Ultimatum | Workers ordered to resume duties | Night of 3 June 2026 |

| Dismissal Threat | Non-compliant workers warned of immediate termination | 3 June deadline |

| Loyalty Bonus | $500 offered to workers who did not participate | Post-resolution |

| Courage Bonus | $1,000 offered to workers who faced aggression for refusing to strike | Post-resolution |

| Internal Investigation | Probe into alleged intimidation and equipment damage launched | Findings to be referred to Congolese authorities |

Workers returned to their posts following the company's escalation, with operations resuming before 5 June 2026. CMOC confirmed the strike had concluded and characterised the overall impact on copper production as minimal. TFM also publicly acknowledged that the underlying concerns raised by workers would be reviewed through legitimate internal channels, a commitment that will require follow-through to prevent a recurrence (Miningmx, 9 June 2026; Bloomberg, 5 June 2026).

The bonus structure itself is worth examining. The $500 loyalty payment offered to non-striking workers and the $1,000 payment offered to those who resisted intimidation were designed simultaneously as financial rewards and as signals of management's authority over the narrative. By framing these payments around loyalty and courage, TFM sought to reframe the strike's moral geography internally. Furthermore, according to reporting from Metal.com, the bonus package was seen as an attempt to restore workforce cohesion as much as to resolve the immediate industrial dispute.

Labour Risk in Chinese-Operated African Mines: A Systemic Pattern

The Governance Mismatch Between Capital Deployment and Workforce Engagement

Chinese mining capital has moved into the DRC at extraordinary speed over the past decade. The pace of asset acquisition, infrastructure development, and production ramp-up at operations like TFM and KFM has been genuinely remarkable by any historical standard. However, what has not kept pace is the development of participatory labour governance frameworks that align with local workforce expectations.

This mismatch is not unique to CMOC or to the DRC, but it is particularly visible in the Congolese copper belt because the scale of operations is large enough to generate internationally newsworthy disruptions. Researchers studying Chinese outbound mining investment in sub-Saharan Africa have documented recurring patterns including limited worker consultation processes, restrictive union environments, and compensation structures that sometimes diverge significantly from local expectations and from practices established by Western operators in the same jurisdictions.

Comparing Approaches Across Major DRC Copper Operators

| Operator | Nationality | Labour Engagement Approach | Recent Dispute Indicators |

|---|---|---|---|

| CMOC (TFM and KFM) | Chinese | Centralised CBA negotiation model | June 2026 strike |

| Glencore (KCC) | Swiss-British | Established multi-union frameworks | Periodic wage disputes |

| Ivanhoe Mines (Kamoa-Kakula) | Canadian | Community and workforce engagement programs | Limited major strikes reported |

| Jinchuan Group | Chinese | Under governance scrutiny | $145 million fraud probe flagged (Miningmx, 2026) |

The contrast between the Canadian operator model at Kamoa-Kakula and the approach observed at some Chinese-operated concessions reflects deeper differences in corporate governance philosophy, stakeholder management culture, and the degree to which community and worker relations are treated as strategic assets rather than operational costs. In addition, the broader DRC cobalt disruption context compounds the stakes for operators across the entire basin, given how closely cobalt and copper production are intertwined at major concessions.

What Copper Demand Trajectories Mean for DRC Supply Security

Four Structural Demand Vectors Creating Market Tightness

The strategic significance of any disruption at TFM must be read against the backdrop of where copper demand is heading. The International Energy Agency and broader commodity research communities have consistently identified four copper demand drivers that will structurally elevate copper consumption through the late 2020s and into the 2030s:

- Electric vehicle manufacturing: Each battery electric vehicle requires approximately 2.5 to 4 times the copper of a conventional internal combustion engine vehicle, with the exact volume depending on vehicle class and battery chemistry.

- Renewable energy infrastructure: Both wind and solar installations are copper-intensive per megawatt of installed capacity, with offshore wind particularly demanding given cable and subsea infrastructure requirements.

- Power grid modernisation: Ageing transmission and distribution infrastructure in North America, Europe, and parts of Asia requires substantial copper investment simply to maintain existing capacity, let alone to support electrification growth.

- AI data centre buildout: Server infrastructure, power distribution systems, and the cooling systems that keep high-performance computing operational are all copper-dependent, creating a demand vector that was negligible a decade ago and is now material.

Against this demand trajectory, copper prices near record highs mean that even a short-duration disruption at a mine producing over half a million tonnes annually carries measurable market signalling risk. The physical tightness implied by supply disruption at TFM-scale operations translates directly into spot price pressure and forward curve steepening. Consequently, understanding the copper supply crunch dynamics that underpin these pressures is increasingly essential for commodity market participants seeking to assess forward risk.

The DRC's Systemic Vulnerability and the Supply Security Paradox

The DRC combines the world's most concentrated deposits of copper and cobalt with some of its most persistent institutional fragilities. Key systemic risk factors embedded in the operating environment include:

- Ambiguous labour law enforcement: The threshold between a legally protected strike and an illegal industrial action is frequently contested, and enforcement is inconsistent across provinces and political cycles.

- Fragmented union structures: Multiple unions claiming legitimacy over the same workforce undermine coherent collective bargaining and create conditions where management can face competing demands simultaneously.

- Geographic remoteness: Major mining concessions in Lualaba and Haut-Katanga are geographically isolated, limiting access to independent mediation services and creating information asymmetries that complicate dispute resolution.

- Political volatility cycles: Regional conflict dynamics and periodic shifts in Congolese government mining policy create unpredictable operating environments that compound labour relations risk.

The deeper paradox is that the DRC's rise to copper superpower status has been built on the foundation of foreign, predominantly Chinese, investment capital. However, the institutional labour governance infrastructure that would stabilise and protect that position over the long term has not been developed at equivalent speed. This leaves the DRC's supply position structurally more fragile than headline production volumes suggest.

The DRC's copper output growth story is genuinely impressive by historical standards. But a supply position built on concentrated foreign capital without parallel institutional development carries embedded fragility that physical markets will eventually price more accurately.

Furthermore, the ongoing US-China cobalt rivalry over Congolese resources adds a geopolitical dimension that amplifies the consequences of any operational disruption at major Chinese-operated assets such as TFM. If labour unrest were to broaden from isolated single-mine events into coordinated sector-wide industrial action, the simultaneous impact on copper and cobalt supply could generate meaningful disruption across both base metal markets and battery supply chains.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: CMOC Congo Copper Mine Strike

What caused the CMOC Tenke Fungurume strike in June 2026?

Workers initiated industrial action on 1 June 2026, primarily protesting a collective bargaining agreement they alleged was finalised without genuine rank-and-file participation. Secondary demands included the introduction of a housing allowance and improvements to healthcare coverage.

Was the CMOC Congo strike considered legal or illegal?

TFM management classified the strike as illegal under applicable Congolese labour law and used this designation as the legal basis for issuing dismissal warnings to workers who had not returned to work by the company's stated deadline.

How much copper does Tenke Fungurume produce?

TFM produced approximately 519,000 tonnes of copper in 2025, representing roughly 15% of the DRC's total annual copper output, making it one of the most productive copper operations outside of Chile (Miningmx, 9 June 2026; Bloomberg, 5 June 2026).

How did the Tenke Fungurume strike end?

TFM issued a return-to-work deadline of 3 June 2026, backed by immediate dismissal threats for non-compliance. Workers who had not participated in the strike received a $500 loyalty bonus, and those who faced intimidation for refusing to join were offered a $1,000 payment. Operations resumed by 5 June 2026.

What is CMOC's total Congo copper production?

Across both TFM and Kisanfu (KFM), CMOC extracted close to 750,000 tonnes of copper from the DRC in 2024, positioning the company as one of the largest single-operator copper producers globally (Miningmx, 9 June 2026; Bloomberg, 5 June 2026).

Why does DRC copper supply matter to global markets?

The DRC has become the world's second-largest copper producer through sustained large-scale foreign investment over the past decade. Its mines also produce the majority of the world's cobalt, giving the country an outsized role in both copper supply chains and battery material supply chains simultaneously.

Key Investor and Market Takeaways

The June 2026 CMOC Congo copper mine strike was resolved quickly in operational terms, but its underlying causes remain structurally unaddressed. A workforce that feels excluded from the negotiation of its own employment conditions is a workforce that will find another moment to express that dissatisfaction, potentially under less favourable market or operational circumstances.

For commodity markets and institutional investors, the TFM incident surfaces several considerations worth monitoring:

- The speed of CMOC's escalation response effectively contained immediate production losses, but the absence of substantive governance reform leaves the root cause intact.

- CMOC's dual-mine Congo footprint produces enough copper to materially influence global physical supply balances. Future disruptions at this scale will not be immaterial to spot markets or futures pricing, particularly given already elevated copper price levels.

- The widening gap between the pace of Chinese mining capital deployment in Africa and the pace of institutional labour governance development at those operations represents an underappreciated ESG and operational risk factor for investors with exposure to Chinese-operated African mining assets.

- As copper demand accelerates through the energy transition and the digital infrastructure buildout, the DRC's embedded systemic risks — including labour fragmentation, governance ambiguity, and institutional fragility — will attract increasing scrutiny from commodity markets, supply chain risk analysts, and institutional capital allocators.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities. Commodity production figures and price references are based on sources available at the time of writing and may be subject to revision. Readers should conduct their own due diligence before making investment decisions.

Want to Stay Ahead of the Next Major Copper Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across copper and more than 30 other commodities — transforming complex data into actionable investment insights before the broader market reacts. Explore how historic discoveries have generated substantial returns on the Discovery Alert discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.