June 20, 2026

The Anatomy of a Mega-Mine Deal: How Scale, Geology, and Geopolitics Converge in Ecuador

In the global mining industry, truly transformative projects share a predictable set of characteristics: low-strip-ratio open-pit geometry, proximity to export infrastructure, polymetallic by-product credits that strengthen project economics, and a resource base large enough to sustain multi-decade operations. These factors rarely align in a single deposit. When they do, the asset attracts capital at a scale that reshapes not just a company's portfolio, but an entire country's economic trajectory. The Los Cangrejos gold project in Ecuador's El Oro province is precisely this kind of convergence, and the CMOC Ecuador gold mine story that has emerged around it deserves careful, detailed analysis from investors, industry observers, and policymakers alike.

When big ASX news breaks, our subscribers know first

Ecuador's Mining Sector at an Inflection Point

From Oil Dependency to Mineral Diversification

Ecuador has historically relied on petroleum exports as its primary source of foreign exchange and fiscal revenue. For decades, oil fields in the Amazon basin provided the financial foundation for public spending, but the structural vulnerabilities of a single-commodity economy became increasingly difficult to ignore as crude prices fluctuated and production from mature fields began declining.

The country's response has been a deliberate, if gradual, pivot toward hard rock mineral extraction. Ecuador possesses geological formations that extend through the Andean and sub-Andean belts, sharing characteristics with some of the most prolific mining jurisdictions in South America. Porphyry copper-gold systems, epithermal gold-silver veins, and large-tonnage gold-bearing intrusive complexes all occur within the country's borders, yet formal large-scale mining only began gaining traction in the 2010s.

Why Foreign Capital Is Flowing Into Ecuador's Mining Corridor

Several structural factors have made Ecuador increasingly attractive to international mining capital over the past decade:

- Ecuador is dollarized, eliminating currency conversion risk for foreign investors repatriating revenues

- The country's mining code, while subject to periodic renegotiation, provides a legal framework for long-term concession agreements

- Infrastructure deficits, while real, are less severe in certain provinces than in more remote Andean or Amazon-basin jurisdictions

- Ecuador's position between Peru and Colombia places it within a well-understood Latin American resource corridor already mapped by global mining majors

The El Oro province in the country's southwest exemplifies this investment thesis. Its name literally translates to "The Gold," a reflection of alluvial gold mining traditions stretching back centuries. The modern discovery of large-scale hard rock gold systems in the province has elevated it from artisanal mining history to potential industrial mining future.

Chinese State-Linked Capital and Latin American Resources

CMOC Group, formerly known as China Molybdenum Co., Ltd., occupies a unique position in the global mining landscape. It is listed on both the Hong Kong Stock Exchange and the Shanghai Stock Exchange, operates some of the world's largest cobalt and copper mines in the Democratic Republic of Congo, and has demonstrated a consistent appetite for acquiring large, complex, long-life assets. Furthermore, the evolving mining geopolitics landscape has only accelerated this strategic appetite for tier-1 assets in emerging jurisdictions.

The company's expansion into Latin America follows a pattern observed across Chinese mining investment more broadly: identify undervalued or underdeveloped assets with exceptional resource scale, acquire through purchase of the controlling entity, and deploy capital at a pace that accelerates development timelines beyond what the original owner could finance.

"Chinese mining companies have collectively invested tens of billions of dollars across Latin America's copper, gold, iron ore, and lithium sectors over the past two decades, reshaping the ownership landscape of the region's most significant mineral assets."

What Is the Los Cangrejos Gold Project and Why Does It Matter?

Geographic Advantages That Make Los Cangrejos a Rare Tier-1 Asset

Infrastructure proximity is one of the most underappreciated value drivers in mining project assessment. The capital cost and operational complexity of a mine increases dramatically with distance from power, roads, ports, and population centres. By this measure, Los Cangrejos is exceptionally well-positioned.

Key Infrastructure Snapshot:

| Infrastructure Factor | Detail |

|---|---|

| Distance to Machala (provincial capital) | ~30 km |

| Distance to Bolívar Port | ~40 km |

| Distance to major substation | ~20 km |

| Distance to national highway | ~8 km |

| Elevation profile | Low elevation, reducing operational complexity |

The low-elevation footprint of the deposit is a detail that merits emphasis. High-altitude mines, common throughout the Andes, face challenges ranging from reduced equipment performance and worker acclimatisation requirements to higher reagent consumption in processing circuits. Los Cangrejos avoids these constraints almost entirely, a factor that has direct positive implications for both capital expenditure estimates and ongoing operational costs.

Understanding the Deposit: Scale, Grade, and Reserve Quality

The deposit's resource base, defined under the 2023 Pre-Feasibility Study, positions Los Cangrejos among the largest undeveloped gold projects in the Western Hemisphere.

Resource and Reserve Summary (2023 Pre-Feasibility Study):

| Category | Tonnage | Gold Grade | Contained Gold |

|---|---|---|---|

| Measured and Indicated Resources | 1.376 billion tonnes | 0.46 g/t | 638 tonnes |

| Proven and Probable Reserves | 659 million tonnes | 0.55 g/t | 359 tonnes |

A few technical observations are worth noting for readers unfamiliar with resource classification conventions. The fact that the Proven and Probable reserve grade (0.55 g/t) exceeds the broader Measured and Indicated resource grade (0.46 g/t) is not unusual. Reserve conversion typically focuses on the higher-grade portions of a deposit that are economically mineable under the specific pit design and economic assumptions used, while lower-grade peripheral material remains classified as a resource but falls outside the reserve pit shell.

The contained gold figure of 638 tonnes in the Measured and Indicated category is equivalent to approximately 20.5 million troy ounces, placing this project in genuinely rare company globally. For context, most new gold mines being developed globally contain fewer than 5 million ounces of reserves.

A lesser-known technical consideration at deposits of this type is the relationship between strip ratio and reserve grade. The reported life-of-mine strip ratio of 1.26 waste-to-ore is remarkably low for an open-pit gold operation, and combined with the deposit's scale and infrastructure proximity, it suggests a capital efficiency profile that is difficult to replicate elsewhere. In addition, a major copper system context helps illustrate just how rare this combination of attributes is in a single project.

How Los Cangrejos Compares to Ecuador's Existing Large-Scale Mines

Ecuador's large-scale mining sector, while young, already hosts two internationally significant operations:

- Fruta del Norte (operated by Lundin Gold): A high-grade underground gold-silver mine in the Zamora Chinchipe province, notable for producing gold at grades exceeding 8 g/t, but with a resource base and production scale substantially smaller than Los Cangrejos

- Mirador (operated by Ecuacorriente, a subsidiary of Chinese interests): A copper-gold porphyry open-pit mine in southeastern Ecuador, which established the operational template for large-scale open-pit mining in the country

Los Cangrejos differs from both in its combination of tonnage scale, polymetallic character, and low-cost infrastructure access. It is best understood not as a high-grade boutique mine but as a bulk-tonnage, long-life industrial operation designed to generate sustained cash flows over a multi-decade horizon.

How CMOC Secured Control of Ecuador's Largest Primary Gold Deposit

The Lumina Gold Acquisition: A US$420 Million Strategic Entry Point

CMOC's path to Los Cangrejos ran through Vancouver-headquartered Lumina Gold Corp, the junior mining company that had advanced the project through exploration and Pre-Feasibility Study stages. In June 2025, CMOC completed the acquisition of 100% of Lumina Gold Corp for US$420 million, giving the Chinese mining group full control of the deposit.

For investors familiar with gold M&A activity, the transaction price warrants analytical context. Paying US$420 million for a pre-construction asset containing 359 tonnes of Proven and Probable gold reserves implies a discovery and acquisition cost of approximately US$1.17 per reserve ounce before any development capital. While this appears modest relative to the eventual project economics, it reflects the execution and jurisdiction risk premium that markets apply to pre-FID (Final Investment Decision) assets in emerging mining jurisdictions.

From Vancouver to Quito: How a Canadian Junior Miner Became a Chinese Mega-Project

The transition from Canadian junior developer to Chinese mining major is a well-worn path in the global resources industry. Junior miners perform the high-risk, capital-intensive work of exploration and early-stage resource definition, often funded through equity markets that accept speculative risk in exchange for optionality on discovery. When projects reach a scale that exceeds the financing capacity of their junior developer parents, they become natural acquisition targets for majors with access to low-cost capital and project execution infrastructure.

Lumina Gold followed this template precisely. The company had invested years and tens of millions of dollars advancing Los Cangrejos from initial discovery through to a bankable Pre-Feasibility Study, at which point the asset's value was largely derisked from a geological standpoint. CMOC's acquisition effectively monetised that derisking at a premium to Lumina's market capitalisation, while positioning CMOC to capture the substantially larger value created during construction and operation.

Timeline of Ownership Transition and On-Site Mobilisation

The pace of activity following the acquisition signals CMOC's intent to move rapidly through the development pipeline.

Key Milestone Timeline:

- June 2025: CMOC completes 100% acquisition of Lumina Gold Corp for US$420 million

- June 2025: CMOC deploys a dedicated project team to establish on-site presence in El Oro province

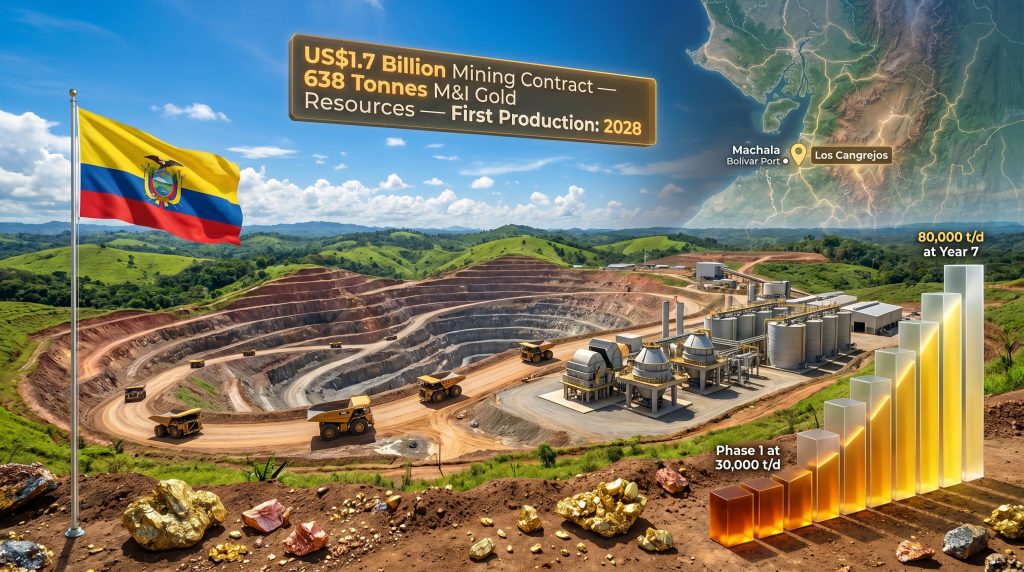

- Late April 2026: Ecuador's government executes a landmark US$1.7 billion mining contract with CMOC's local subsidiary, ODIN Mining del Ecuador

- 2028 (Target): First gold production scheduled from the Los Cangrejos operation

The roughly ten-month interval between acquisition close and signed mining contract reflects an unusually efficient regulatory and commercial negotiation timeline for a project of this complexity and scale.

Breaking Down the US$1.7 Billion Mining Contract

Financial Architecture of the Deal: Royalties, Taxes, and State Revenue Projections

Ecuador's contract with CMOC for the Los Cangrejos project is structured to deliver an estimated US$4.39 billion in cumulative state revenue across the mine's 26-year life, comprising taxes, royalties, and associated fees. According to Reuters reporting on the deal, an advance royalty payment of US$54 million is embedded in the agreement, with US$34 million payable upfront and US$20 million linked to development milestones including plant commissioning.

The US$4.39 billion projected state revenue figure requires contextual interpretation. This represents cumulative undiscounted revenue across 26 years, meaning its net present value at any reasonable discount rate would be substantially lower. The figure is nonetheless significant: it implies average annual state receipts of approximately US$169 million per year at steady-state production, providing Ecuador with a recurring, long-duration revenue stream that partially compensates for declining oil output.

The 50/50 Value-Sharing Framework

The contract incorporates a value-sharing structure whereby approximately half of the project's economic value flows to the Ecuadorian state through various fiscal mechanisms. This model blends multiple revenue collection instruments rather than relying on a single royalty or tax rate, which provides Ecuador with revenue diversification across the mine's operating phases.

For CMOC, the framework's acceptability depends on the assumptions embedded in their financial model. At current gold prices, the economics of a deposit with 359 tonnes of Proven and Probable reserves, a low strip ratio, and robust infrastructure access can absorb a significant fiscal burden while still generating attractive returns on the US$1.7 billion construction investment.

Advance Royalty Mechanics: How Milestone-Based Payments Protect State Interests

The US$54 million advance royalty structure serves an important function from a sovereign risk management perspective. By requiring US$34 million upfront and tying the remaining US$20 million to a verifiable technical milestone (plant commissioning), Ecuador secures a meaningful financial commitment from CMOC before construction capital has been fully deployed. This structure:

- Reduces Ecuador's exposure to project abandonment risk in the pre-construction phase

- Aligns CMOC's financial incentive structure with project advancement

- Establishes a contractual precedent that can be referenced in future mining contract negotiations

Comparing Ecuador's Contract Terms to Regional Mining Fiscal Regimes

Comparative Table: Mining Fiscal Frameworks in Latin America

| Country | State Revenue Share Model | Advance Royalty Mechanism | Notable Example |

|---|---|---|---|

| Ecuador (Los Cangrejos) | ~50% of project value | US$54M advance royalty | CMOC / Los Cangrejos |

| Chile | Variable royalty + corporate tax | Not standard | Escondida (BHP) |

| Peru | Royalty tiers + windfall tax | Limited application | Cerro Verde |

| DRC (CMOC reference) | Production-sharing | Renegotiated 2022 | Tenke Fungurume |

Ecuador's framework sits toward the higher end of the regional state-take spectrum, though this is partly offset by the country's dollarised monetary environment and the project's exceptional infrastructure positioning. Investors comparing jurisdictional risk-adjusted returns should weigh the elevated fiscal take against the reduced currency and logistics risk relative to more remote Andean or Central African alternatives.

What the Los Cangrejos Mine Will Actually Produce

Open-Pit Mining Design: The Cangrejos and Gran Bestia Pit Configuration

The Los Cangrejos operation is designed around two open-pit zones, the Cangrejos pit and the Gran Bestia pit, which together define the initial mine plan. Open-pit mining at this scale involves sequential benching of rock in expanding concentric cuts, with ore and waste separated at the point of blast and loading. The project's exceptionally low strip ratio of 1.26:1 means that for every tonne of ore extracted, only 1.26 tonnes of waste rock require movement and disposal, a ratio that places Los Cangrejos in the most capital-efficient tier of open-pit gold operations globally.

Processing Circuit Explained: From Crushing to CIL Gold Recovery

Processing Technology Stack:

- Conventional open-pit mining and drilling and blasting

- Primary crushing followed by High-Pressure Grinding Rolls (HPGR) for energy-efficient comminution

- Ball mill grinding circuit for further particle size reduction

- Copper flotation circuit for by-product concentrate production

- Carbon-in-Leach (CIL) gold recovery circuit for final gold extraction

The inclusion of HPGR technology is notable from an operational efficiency standpoint. High-Pressure Grinding Rolls consume significantly less energy per tonne of material processed than traditional semi-autogenous grinding (SAG) mills, and they tend to produce a product with more micro-fractures, which improves downstream leach kinetics in CIL circuits. At an 80,000 tonne-per-day throughput rate, even marginal improvements in energy efficiency translate to material reductions in operating cost per ounce.

Phased Production Ramp-Up: From 30,000 t/d to 80,000 t/d

Production Scaling Schedule:

| Phase | Throughput Capacity | Timeline |

|---|---|---|

| Phase 1 | 30,000 tonnes per day | Year 1 (from 2028) |

| Full Ramp-Up | 80,000 tonnes per day | Year 7 (~2034) |

| Annual Gold Output (Steady State) | ~11.5 tonnes gold per year | Post-ramp |

| Life-of-Mine Strip Ratio | 1.26 | 26-year mine life |

The phased approach to throughput expansion is standard practice for large-tonnage mining projects, as it allows initial cash flows to partially fund subsequent capital expenditures while the operational team optimises the processing circuit before scaling. The jump from 30,000 to 80,000 tonnes per day represents a more than doubling of plant capacity and will require substantial additional capital investment between Years 1 and 7.

By-Product Revenue Streams: Copper Cathodes, Molybdenum, and Their Economic Contribution

One of the less-discussed aspects of Los Cangrejos' economics is its polymetallic character. The deposit contains recoverable copper and molybdenum alongside gold, with the copper flotation circuit designed to produce copper concentrate or cathode-equivalent product as a commercial by-product. These additional revenue streams serve as a natural hedge against gold price volatility, strengthening the project's all-in sustaining cost (AISC) per ounce of gold through by-product credits.

CMOC's existing expertise in processing complex polymetallic ores, developed through decades of operating molybdenum mines in China and copper-cobalt operations in the DRC, provides a genuine technical advantage in optimising recovery of these secondary metals.

The next major ASX story will hit our subscribers first

How CMOC's Ecuador Strategy Fits Its Global Portfolio

CMOC's Operational Footprint: From the DRC to South America

CMOC has transformed from a domestic Chinese molybdenum producer into one of the world's largest diversified base and precious metals miners. Its Tenke Fungurume copper-cobalt mine in the DRC is among the largest of its type globally, and the company's operational experience across geologically complex, politically sensitive jurisdictions informs its approach to Ecuador. Consequently, Zijin's global expansion offers a useful parallel for understanding how Chinese mining majors systematically build out their international resource portfolios.

The Los Cangrejos acquisition represents CMOC's most significant entry into South American gold production, diversifying the company away from its heavy concentration in African base metals and providing exposure to the gold price cycle.

Why Ecuador? CMOC's Strategic Rationale

Several factors likely converged to make Ecuador the chosen destination for CMOC's South American gold strategy:

- The sheer scale of Los Cangrejos' resource base, which is large enough to justify the fixed costs of a dedicated in-country operational team and management structure

- Ecuador's dollarised economy reducing foreign exchange complexity

- The relative underdevelopment of Ecuador's mining sector compared to Peru or Chile, presenting first-mover advantages in terms of regulatory relationships and community engagement frameworks

- Lumina Gold's pre-existing permitting work and community relations infrastructure in El Oro province

Risks and Challenges Facing the Los Cangrejos Development

Political and Regulatory Risk: Ecuador's History of Mining Policy Volatility

Ecuador's mining investment environment has historically been characterised by policy discontinuity. The country has experienced multiple cycles of resource nationalism, constitutional changes affecting mining rights, and shifts in royalty and tax frameworks between administrations. Investors with long memories will recall periods when mining contracts were unilaterally modified or exploration concessions suspended.

The 26-year mine life embedded in Los Cangrejos' financial model spans multiple presidential terms and potential policy cycles, making the durability of the signed contract a material risk factor that deserves serious consideration.

Environmental and Social Licence Considerations in El Oro Province

Large-scale open-pit gold mining in Ecuador has faced opposition from environmental groups and affected communities, particularly where water resources intersect with mine footprints. El Oro province has both agricultural and aquaculture economic activities that could be perceived as incompatible with open-pit mining operations. Maintaining a robust social licence to operate will require sustained community engagement investment throughout construction and operations.

Why Did CMOC's Shares Fall After the Announcement?

Investor Caution: Despite the strategic significance of the Los Cangrejos deal, CMOC's Hong Kong-listed shares declined approximately 3.8% following the contract announcement. Market participants appear to have focused on the scale of capital commitment, the extended construction timeline, and the jurisdictional risk profile of Ecuador rather than the long-term reserve value being secured.

This reaction illustrates a well-documented tension in mining investment psychology: the market frequently penalises large capital commitments in the near term, even when the long-term value creation case is compelling. For contrarian investors, such reactions can represent mispricing opportunities, though the complexity and duration of the Los Cangrejos development cycle demands patience that is inconsistent with most institutional investment mandates.

Currency, Commodity Price, and Financing Risks Over a 26-Year Mine Life

A 26-year mine life creates multi-cycle exposure across gold price, energy cost, and reagent cost variables. The project's economics will be tested across multiple gold bear markets, and the financing structure underpinning the US$1.7 billion construction budget will need to accommodate potential periods of reduced cash generation during ramp-up. However, the definitive feasibility study process will be critical in locking down the project's bankable cost structure and formalising lender commitments. The milestone-based advance royalty structure provides some buffer, but investors should model downside scenarios incorporating gold prices materially below current levels.

Ecuador's Emerging Gold Mining Landscape

Ecuador's Three Pillars of Large-Scale Mining

Los Cangrejos joins Fruta del Norte and Mirador as the third anchor asset in Ecuador's emerging large-scale mining sector. Each project represents a distinct mineral system and operational model:

- Fruta del Norte: High-grade underground gold-silver, operated by a Canadian major

- Mirador: Porphyry copper-gold open-pit, operated under Chinese capital

- Los Cangrejos: Bulk-tonnage intrusive-hosted gold with polymetallic credits, under CMOC via ODIN Mining del Ecuador

The diversification across deposit types, operational models, and ownership structures gives Ecuador's mining sector a degree of resilience that single-commodity or single-operator jurisdictions lack.

Chinese Capital as the Dominant Force in Ecuador's Mining Buildout

The combination of Mirador and Los Cangrejos means that Chinese-controlled entities now have significant positions in two of Ecuador's three large-scale mining pillars. This concentration of ownership creates both economic opportunity (access to Chinese capital markets and supply chains) and sovereign risk considerations around negotiating leverage in future contract renewals or modifications.

What This Deal Signals for China-Latin American Mining Relations

Belt and Road Adjacency: Chinese Mining Investment as Strategic Infrastructure

While Los Cangrejos is a commercially motivated investment, it exists within a broader pattern of Chinese resource acquisition across Latin America that has geopolitical dimensions. Chinese state-linked companies now hold significant mining positions in Peru, Chile, Brazil, and Ecuador, creating a network of resource relationships that extends well beyond simple commercial logic. For further detail on CMOC's Ecuadorian operations, CMOC's Ecuador gold business page provides the company's own operational perspective on its strategic positioning in the country.

Ecuador's Balancing Act: Attracting Capital While Managing Sovereignty

Ecuador's challenge in the CMOC negotiation was structuring a deal attractive enough to secure a US$1.7 billion construction commitment while preserving sufficient fiscal and regulatory sovereignty to satisfy domestic political constituencies. The advance royalty mechanism and the headline US$4.39 billion state revenue projection appear designed partly as political communications tools, translating complex mining economics into figures accessible to non-specialist policymakers and the public.

Frequently Asked Questions: CMOC Ecuador Gold Mine

What is the Los Cangrejos gold mine in Ecuador?

Los Cangrejos is a large-scale, low-elevation open-pit gold project located in Ecuador's El Oro province, approximately 30 km from the provincial capital of Machala. It hosts Measured and Indicated gold resources of 638 tonnes across 1.376 billion tonnes of mineralised material, making it one of the largest undeveloped gold deposits in the Western Hemisphere.

Who owns the Los Cangrejos project and how did CMOC acquire it?

CMOC Group acquired Los Cangrejos by purchasing 100% of Lumina Gold Corp, the Canadian junior mining company that had developed the project, for US$420 million in June 2025. Operations are now conducted through CMOC's Ecuadorian subsidiary, ODIN Mining del Ecuador.

When will the Los Cangrejos mine begin production?

The current target for first gold production is 2028, assuming construction progresses on schedule following the April 2026 signing of the US$1.7 billion mining contract.

How much gold will Los Cangrejos produce annually?

At steady-state production following the full ramp-up to 80,000 tonnes per day throughput (targeted around 2034), the operation is projected to produce approximately 11.5 tonnes of gold per year, equivalent to roughly 370,000 troy ounces annually.

How much revenue will Ecuador receive from the CMOC mining contract?

Ecuador is projected to receive cumulative state revenue of approximately US$4.39 billion across the mine's 26-year operating life through a combination of taxes, royalties, and associated fiscal mechanisms, plus US$54 million in advance royalty payments structured around project milestones.

What is ODIN Mining del Ecuador?

ODIN Mining del Ecuador is the CMOC Group subsidiary established to hold and operate the Los Cangrejos concession in Ecuador. It is the legal counterparty to the Ecuadorian government in the US$1.7 billion mining contract signed in late April 2026.

Is Los Cangrejos a gold-only project or does it produce other metals?

Los Cangrejos is a polymetallic project. While gold is the primary economic driver, the deposit also contains recoverable copper and molybdenum. The processing circuit includes a dedicated copper flotation stage, and by-product revenues from copper cathodes and molybdenum products are expected to contribute meaningfully to the project's all-in sustaining cost economics.

What are the main environmental concerns surrounding the project?

Key environmental considerations include potential impacts on regional water resources, land use changes in an agriculturally active province, and the long-term management of tailings storage facilities associated with processing 80,000 tonnes of ore per day at full capacity. Community consultation processes and environmental impact assessments form part of the permitting framework, though the specifics of conditions attached to the current mining contract have not been fully disclosed publicly.

Key Takeaways: The Strategic Significance of CMOC's Ecuador Gold Mine

Summary Table: Los Cangrejos Project at a Glance

| Metric | Value |

|---|---|

| Total Contract Value | US$1.7 billion |

| CMOC Acquisition Cost (Lumina Gold) | US$420 million |

| Projected State Revenue (26-year LOM) | US$4.39 billion |

| Advance Royalties | US$54 million |

| Measured and Indicated Gold Resources | 638 tonnes |

| Proven and Probable Reserves | 359 tonnes |

| Annual Gold Production (Target, Steady State) | ~11.5 tonnes |

| Mine Life | 26 years |

| First Production Target | 2028 |

| Peak Processing Rate | 80,000 t/d |

| Life-of-Mine Strip Ratio | 1.26 |

The CMOC Ecuador gold mine story is ultimately one of scale, patience, and strategic positioning. For CMOC, Los Cangrejos provides a decades-long gold production platform with polymetallic upside and infrastructure advantages that are genuinely difficult to replicate. For Ecuador, the project represents the most ambitious mining investment in the country's history, with fiscal returns that could materially reshape the national revenue base if realised as projected.

The near-term market scepticism reflected in CMOC's post-announcement share price decline may prove to be the kind of short-term noise that long-duration asset investors learn to look through. Whether the 2028 first production target is met, and whether Ecuador's policy environment remains stable enough to deliver the projected US$4.39 billion in state revenue, are the two questions that will define this project's ultimate significance in Latin American mining history.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements including production targets, revenue projections, and timelines are inherently uncertain and subject to risks including gold price movements, regulatory changes, construction delays, and geopolitical factors. Readers should conduct their own due diligence before making any investment decisions.

Want to Catch the Next Major Mineral Discovery Before the Broader Market Does?

The CMOC–Los Cangrejos deal illustrates precisely how transformative large-scale mineral discoveries can become — and how early positioning matters enormously. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, turning complex geological and market data into actionable investment insights for both short-term traders and long-horizon investors. Explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.