July 15, 2026

The Geological Clock Ticking Beneath the World's Copper Supply

Every major commodity cycle eventually confronts a structural limit that no amount of capital or engineering ingenuity can fully override. For copper, that limit is increasingly being defined not by demand uncertainty but by the geology beneath Chile's Atacama Desert, where ore grades have been quietly deteriorating for decades inside the mines that built the modern copper market.

Understanding why Codelco flat copper output in coming years has become the defining supply-side narrative of this decade requires looking past quarterly production reports and into the deeper mechanics of porphyry copper deposits, underground transition projects, and the financial architecture of a state-owned enterprise carrying approximately $25 billion in debt. The numbers matter, but the forces shaping those numbers run far deeper.

When big ASX news breaks, our subscribers know first

The Strategic Weight of Codelco in Global Copper Markets

Codelco is not simply a large copper miner. It is the single largest state-owned copper producer on Earth, and its output decisions ripple through commodity pricing, energy transition planning, and downstream manufacturing supply chains in ways that no privately listed miner can replicate. Indeed, understanding Codelco top producer status helps contextualise why its output trajectory carries such outsized market significance.

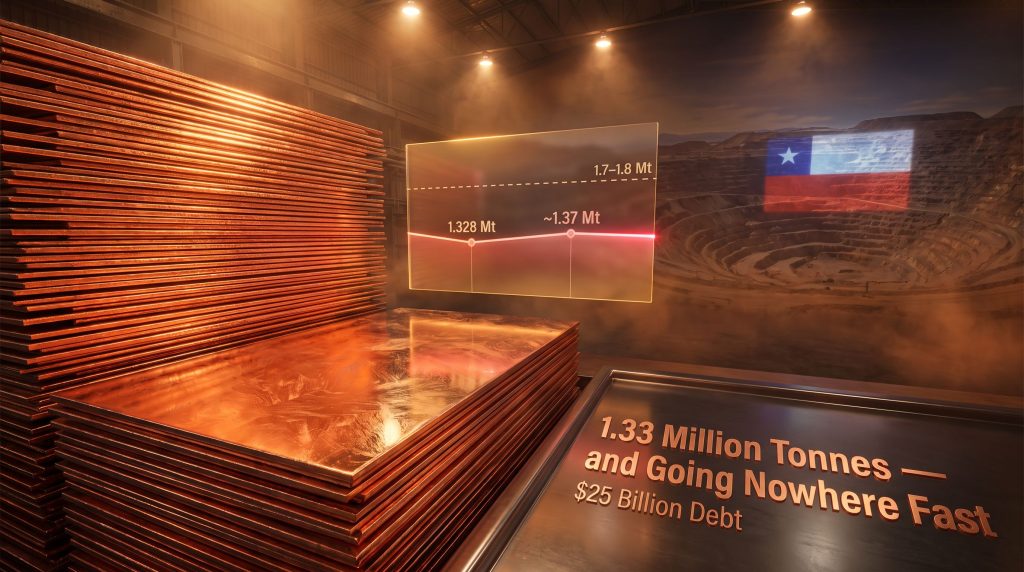

In 2024, Codelco's own-mine production reached approximately 1.328 million metric tonnes, representing a partial recovery from the multi-year lows recorded in 2022 and 2023. To contextualise that figure: global copper mine production is estimated at roughly 22 million tonnes annually, meaning Codelco alone accounts for around 6% of total mined supply. That share may sound modest until one considers that copper markets operate on marginal supply dynamics, where shortfalls of even 200,000 to 300,000 tonnes can generate meaningful price volatility.

The structural difference between Codelco and a publicly listed miner is critical to understanding its production trajectory. A listed producer answers to shareholders and can access equity markets with relative speed. Codelco answers to the Chilean government, which historically extracts significant dividend flows to fund national programmes, creating a persistent tension between reinvestment needs and political obligations. This governance dynamic directly constrains the capital available for the structural projects Codelco depends on to offset geological decline.

What Flat Output Actually Means: The Numbers Behind the Plateau

When Codelco's chairman Bernardo Fontaine told a Chilean congressional committee in July 2026 that production in coming years was likely to remain at levels broadly similar to today, the market interpreted this as an informal downgrade of the company's official 2030 ambitions. According to Reuters reporting on Codelco's output expectations, the numbers firmly support that reading.

| Year | Output / Projected Output (Mt) | Year-on-Year Trend | Key Driver |

|---|---|---|---|

| 2022-2023 | Multi-decade lows | Sharp decline | Operational disruptions, grade decline |

| 2024 | 1.328 million | Partial recovery | Structural project ramp-up |

| 2025 | 1.34-1.37 million | Flat to modest gain | Revised internal targets |

| 2026 | ~1.344 million | +0.8% vs. 2025 | Incremental structural progress |

| 2027 | ~1.37 million | Slight increase | Project contributions |

| 2030 (target) | 1.7-1.8 million | Long-term ambition | Full structural project delivery (contested) |

The gap between where Codelco sits today and where its official targets suggest it should be by 2030 is approximately 370,000 metric tonnes. At a recovery rate of roughly 5,000 tonnes per year since the 2023 trough, the mathematics of closing that gap within the stated timeframe become increasingly difficult to defend without a step-change in project execution. No such step-change is currently visible in the production pipeline.

Ore Grade Deterioration: The Geological Ceiling That Capital Cannot Simply Buy Through

One of the least widely understood dynamics in copper mining is the relationship between ore grade decline and the capital intensity required to maintain, let alone grow, output. Copper ore grade refers to the concentration of copper within a given tonne of rock, typically expressed as a percentage. At Codelco's flagship operations, including Chuquicamata and Ministro Hales, average ore grades have been declining progressively since at least 2021.

This is not a temporary operational problem. Porphyry copper deposits, which dominate Chilean geology, are characterised by large, low-grade mineralisation that becomes progressively lower-grade as mines age and higher-grade zones are depleted. The critical point that separates informed investors from casual market observers is this: declining ore grades at scale require proportionally more rock to be moved, processed, and refined for every tonne of finished copper produced, driving up unit costs even when commodity prices are supportive.

Furthermore, the broader Chile copper price outlook is directly shaped by these geological realities, as sustained grade deterioration feeds into tighter supply expectations across the market.

Several compounding factors make Codelco's grade challenge particularly acute:

- Open-pit mines transitioning to underground operations face a period of reduced throughput during the transition phase

- Geomechanical instability, which refers to the structural behaviour of rock under stress at depth, adds engineering complexity and safety risk to underground expansions

- Underground mines typically have lower throughput rates than open-pit operations, meaning ore grade becomes even more critical to economic viability at depth

- The capital cost of underground transition projects at the scale Codelco is executing is measured in billions of dollars per project, with long lead times before production contributions materialise

The El Teniente Factor: A Single Mine's Collapse Reshapes the National Output Curve

El Teniente, located in the Andes south of Santiago, holds the distinction of being the world's largest underground copper mine by ore reserves. It is also Codelco's single largest producing asset, which makes the tunnel collapse that occurred there in early 2025 one of the most consequential individual mining incidents in recent commodity market history.

The incident resulted in a projected production decline at El Teniente of approximately 13%, reducing estimated output at that mine to around 310,100 tonnes for 2025. Recovery is expected to take a minimum of three years, meaning the drag on Codelco's national output will persist well into the late 2020s regardless of progress elsewhere in the portfolio.

Beyond the production mathematics, the incident carries governance weight. A major safety event at a flagship state-owned asset attracts congressional scrutiny, affects operational morale, and can delay regulatory approvals for adjacent expansion works. These second-order effects are difficult to quantify but are not immaterial to the recovery timeline.

Project Delays and the Structural Portfolio Under Pressure

Codelco's structural projects, most notably the Chuquicamata Underground transition and the Rajo Inca development, were designed with a clear strategic logic: as open-pit ore grades declined, underground operations would access higher-grade zones at depth to sustain overall output. The execution has been considerably more complex than the design.

Fontaine's congressional testimony acknowledged directly that these projects have encountered unexpected delays and cost overruns. This is significant for two reasons. First, it represents a public admission from the company's chairman rather than a disclosure buried in technical reporting. Second, it comes against the backdrop of a $25 billion debt burden that limits Codelco's flexibility to simply inject additional capital to accelerate timelines.

"The tension between Codelco's debt obligations, the Chilean government's dividend expectations, and the investment requirements of its structural project portfolio represents one of the most complex capital allocation challenges in the global mining industry today."

Is the 2030 Target of 1.7 Million Tonnes Still Credible?

Framing Codelco's output trajectory through scenario analysis rather than accepting the official target at face value reveals the genuine range of outcomes facing global copper markets. However, analysts tracking the wider copper supply crunch increasingly regard even the base case as optimistic given current execution rates.

| Scenario | 2030 Output Estimate | Probability | Key Dependency |

|---|---|---|---|

| Base Case | 1.4-1.5 million Mt | Most likely | Incremental project delivery |

| Optimistic | 1.6-1.7 million Mt | Low to moderate | Full structural project execution |

| Downside | Below 1.3 million Mt | Tail risk | Further operational disruption |

The base case reflects a world where structural projects contribute incrementally, El Teniente recovers broadly on schedule, and the debt burden constrains but does not prevent capital deployment. The optimistic case requires near-perfect execution across a portfolio that has already demonstrated it cannot deliver near-perfect execution. The downside case, while a tail risk, is not negligible given the geomechanical complexity of Codelco's underground environments.

Historical precedent from large state-owned mining enterprises globally suggests that decade-long production targets set during periods of operational stress are rarely achieved on the original timeline. The political incentive to maintain ambitious official targets is real, but so is the geological and financial friction that prevents their delivery.

El Abra: Could a $7.5 Billion Expansion Become Codelco's Most Viable Growth Option?

Amid the challenges across its own-mine portfolio, Codelco's 49% stake in the El Abra copper mine in northern Chile has attracted renewed strategic attention. El Abra's majority owner, Freeport-McMoRan, has outlined a $7.5 billion expansion project that could substantially increase the mine's output capacity.

Fontaine described El Abra as potentially the most attractive destination for whatever investment resources Codelco can access, a framing that signals a possible pivot in strategic priority away from the struggling structural project portfolio toward a joint-venture growth pathway. In this respect, El Abra sits alongside a broader wave of new copper supply projects globally that are being assessed as alternatives to capacity constrained by geological or operational challenges.

However, several structural complexities attach to this opportunity:

- Joint venture governance: As a 49% minority partner, Codelco cannot unilaterally approve or accelerate the expansion; Freeport-McMoRan's strategic priorities and capital allocation decisions are decisive

- Capital commitment scale: A 49% share of a $7.5 billion project implies a Codelco contribution potentially approaching $3.5 billion, a significant draw on an already constrained balance sheet

- Timeline uncertainty: Large greenfield and brownfield copper expansions in Chile face permitting, community consultation, and water access challenges that routinely extend project timelines beyond initial estimates

- Strategic alignment risk: Freeport-McMoRan's global portfolio priorities may not always align with Codelco's urgency to restore domestic output metrics

If El Abra proceeds on an accelerated timeline and Codelco secures its proportional financing, it could represent one of the most significant new copper supply additions in Latin America this decade. The conditional nature of that outcome, however, warrants careful attention from anyone modelling Codelco's medium-term production trajectory.

The next major ASX story will hit our subscribers first

The Cochilco Audit: When Production Transparency Becomes a Market Issue

Chile's national copper commission, Cochilco, is conducting a preliminary audit of Codelco's 2025 production reporting, with a focus on approximately 20,000 metric tonnes of copper whose inclusion in the official production figure has attracted scrutiny. The audit results are expected in September 2026.

To contextualise the scale: 20,000 tonnes represents roughly 1.5% of Codelco's annual output at current levels. While that percentage may appear modest, the implications extend well beyond the tonnage itself.

Production reporting discrepancies at a state-owned enterprise of Codelco's scale affect:

- Bond market credibility: International debt investors require confidence in the financial and operational data underlying their credit assessments

- Government accountability: The Chilean Congress, which oversees Codelco as a state asset, relies on accurate production data to evaluate management performance

- Commodity market signals: Any upward adjustment to reported production that is subsequently revised downward creates a distorted picture of supply availability, potentially affecting copper price discovery

The audit outcome will matter not only for the number itself but for what it signals about internal reporting governance at one of the world's most systemically important mining operations.

How Codelco's Production Plateau Affects the Global Copper Supply-Demand Balance

Copper's role in the energy transition is well established. Each electric vehicle contains approximately 80 to 100 kilograms of copper, roughly four times the amount in a conventional internal combustion vehicle. Grid-scale battery storage, offshore wind infrastructure, and data centre construction all represent structurally growing demand vectors that analysts project will add millions of tonnes of annual consumption by the early 2030s.

Against this backdrop, Codelco flat copper output in coming years is not a localised operational story. It is a structural supply signal with global pricing implications, and consequently it is reshaping investment strategies across the entire copper value chain.

Several compounding dynamics amplify Codelco's output plateau into a broader market concern:

- Major copper-producing nations including Peru have faced their own operational disruptions from community conflicts and political instability

- The Democratic Republic of Congo, a growing copper supplier, faces infrastructure and governance constraints that limit the pace of production growth

- New copper project development timelines from discovery to production typically span 15 to 20 years, meaning projects needed to close the 2030s supply gap should ideally already be in advanced development

- The copper exploration pipeline is widely regarded as insufficient to replace depleting reserves at existing operations

Geographic Concentration Risk and the Case for Supply Diversification

Chile accounts for approximately 27% of global copper mine production, a concentration that exposes commodity markets to systemic risk when Chilean operations underperform. Codelco's challenges reinforce the strategic rationale for copper supply diversification that major mining groups and commodity traders have been actively pursuing.

In response, copper growth partnerships between major producers and junior explorers are gaining momentum as one practical mechanism for accelerating pipeline development outside Chile's increasingly constrained geology. Furthermore, according to Mining Technology's analysis of Codelco's recent output trends, these concerns are well founded across multiple recent reporting periods.

Emerging copper jurisdictions across Zambia, Ecuador, and parts of Central Asia are attracting increasing exploration capital, precisely because investors recognise that Chile-concentration risk is not theoretical. It is currently materialising in real production numbers, and the case for diversification has never been more compelling.

Disclaimer: This article contains forward-looking statements, scenario projections, and analyst interpretations that involve inherent uncertainty. Production forecasts, price implications, and project timelines discussed herein are subject to material change based on operational, financial, geological, and political factors. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research before making investment decisions.

Want to Position Ahead of the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across copper and 30+ other commodities — turning complex geological data into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have delivered extraordinary returns on the Discovery Alert discoveries page, and begin your 14-day free trial today to secure your market-leading edge.