May 12, 2026

When a State-Owned Giant Becomes a Global Risk Factor

Across the global copper market, the structural tension between resource nationalism and financial sustainability has never been more visible. State-owned mining enterprises, long celebrated as instruments of national wealth retention, are increasingly exposed as instruments of fiscal fragility when governance frameworks fail to keep pace with the capital demands of ageing, complex mining operations. Few cases illustrate this tension more sharply than the current situation unfolding at the world's largest copper producer, where a new government is signalling a fundamental rethink of how a strategically critical enterprise should be run.

The Codelco governance overhaul amid debt concerns now gripping Chile's policy circles is not simply a domestic administrative story. It is a signal event for global copper markets, sovereign credit analysts, and mining investors who track supply-side risk with growing urgency as electrification demand continues to outpace new mine development.

When big ASX news breaks, our subscribers know first

Why Codelco's Structural Problems Are a Global Market Issue

Understanding why governance dysfunction at a single company generates international concern requires appreciating Codelco's unique position in the global copper supply chain. The company is not merely Chile's largest industrial employer or a source of national pride. It is a structural pillar of global copper availability, and its operational performance has measurable consequences for commodity pricing, downstream manufacturing costs, and energy transition timelines.

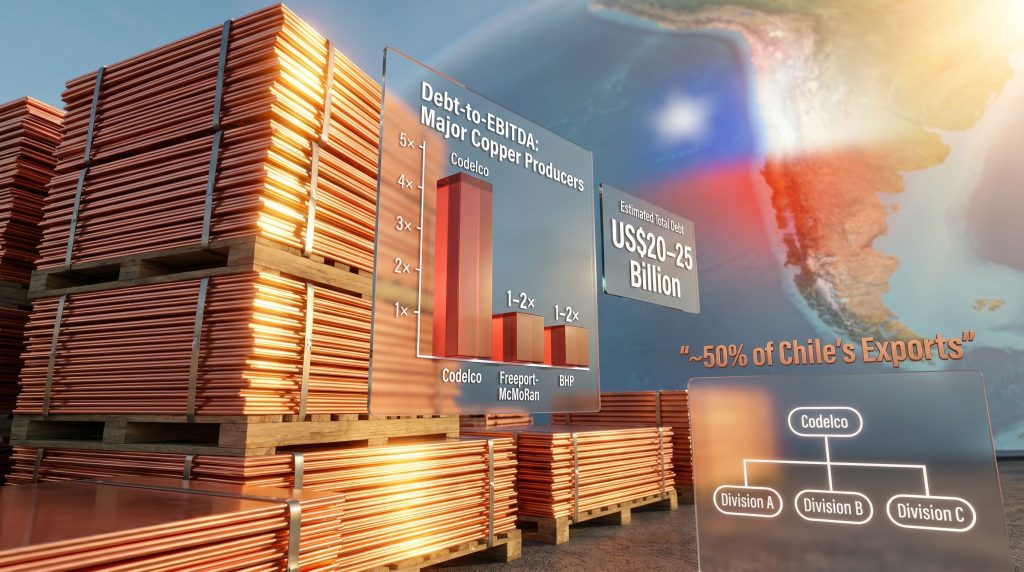

Copper accounts for roughly 50% of Chile's total export revenue, a concentration that creates a feedback loop between Codelco's financial health and Chile's sovereign fiscal position. When the company underperforms, the national budget contracts. When it borrows excessively to fund capital projects, contingent fiscal liabilities accumulate on the government's balance sheet. Furthermore, the broader Chile copper outlook is increasingly shaped by how effectively these structural problems are addressed.

The scale of this challenge becomes clearer when comparing Codelco's financial profile against major private-sector peers:

| Indicator | Codelco (Current Estimate) | Major Private Peers |

|---|---|---|

| Total Debt (Estimated) | US$20–25 billion | Substantially lower on leverage metrics |

| Debt-to-EBITDA Ratio | ~5x | Freeport-McMoRan, BHP: approximately 1–2x |

| Share of Chile's Exports | ~50% | Not applicable |

| Mandatory Fiscal Transfer | Profits + 10% of revenue | No mandatory profit transfer obligations |

| Production Trend | Declining due to project delays | Stable to growing among peers |

The contrast in leverage ratios tells the story concisely. A debt-to-EBITDA ratio of approximately 5x, against a peer range of 1–2x, reflects not mismanagement in isolation but a structural fiscal design that prevents the company from retaining sufficient earnings to self-fund investment cycles.

The Governance Failures That Made Reform Inevitable

A Reform That Did Not Reform Enough

In 2009, Chile enacted governance changes specifically designed to insulate Codelco from the volatility of political appointment cycles and to provide the stability needed for long-term capital planning. The intent was sound. The outcome was not. Analysts at Cesco, a prominent Chilean mining policy think tank, have concluded that the reform produced high management turnover and entrenched an excessively centralised reporting structure rather than resolving these issues.

The centralisation problem is particularly significant from an accountability standpoint. When financial results are reported primarily at the consolidated corporate level rather than broken down by individual operating division, several dysfunctions emerge:

- Underperforming divisions are shielded from scrutiny by stronger operations elsewhere in the portfolio.

- Management teams at the divisional level face fewer measurable performance benchmarks.

- External stakeholders, including bondholders and government overseers, cannot accurately assess where capital is being deployed efficiently and where it is being consumed without adequate return.

- Identifying the precise source of cost overruns or production shortfalls becomes an exercise in approximation rather than precision.

This opacity is not merely an inconvenience. It is a structural enabler of continued underperformance, and it is one of the core reasons that Cesco has formally recommended evaluating a transition toward a holding-company model with more autonomous divisional structures. Indeed, the ongoing copper production decline has only intensified calls for this kind of architectural reform.

The Kast Administration's Reform Mandate

Chile's current government, led by President José Antonio Kast, has inherited a company that carries the cumulative weight of delayed capital projects, cost overruns, and deteriorating production volumes. Finance Minister Jorge Quiroz has publicly identified governance deficiencies as requiring urgent intervention, emphasising that the company needs greater transparency and more robust internal oversight mechanisms that go beyond simply replacing personnel at the top.

The administration is installing three new board members as part of a broader leadership transition, with the departure of outgoing chairman Máximo Pacheco marking a significant inflection point. Critically, the reform emphasis is on structural architecture rather than individual appointments. As Quiroz has made clear, the goal is to establish checks and balances capable of controlling the company's sprawling operational footprint on a sustainable basis. Bloomberg's reporting on the governance overhaul provides additional context on the political dynamics shaping this process.

The Fiscal Transfer Trap: Understanding Codelco's Debt Spiral

Why Debt Accumulates Even When Copper Prices Are Strong

The single most important and least widely understood aspect of Codelco's financial architecture is the mandatory fiscal transfer obligation. The company hands over its profits and 10% of its total revenue to the Chilean government each year. This is not a tax in the conventional sense but a constitutionally embedded wealth transfer mechanism reflecting copper's status as a sovereign natural resource rather than a commercial commodity owned by a private enterprise.

The consequence of this structure is that Codelco is perpetually capital-constrained regardless of copper price conditions. During periods of high copper prices, the government receives larger transfers. During periods of low prices, the company's ability to service existing debt is diminished. In neither scenario does the company retain sufficient earnings to fully fund the multi-billion-dollar capital expenditure programmes required to maintain and expand production capacity at ageing, deep underground operations.

Pacheco has argued that decades of underinvestment combined with this fiscal transfer structure explain the bulk of the current debt burden. The implication is striking: under a hypothetical private-sector financial framework where profit retention is the norm, the company's debt position would look fundamentally different.

Three Pathways Being Debated

Chilean policymakers are navigating three broad scenarios for restructuring this arrangement:

Scenario 1: Status Quo

- Mandatory fiscal transfers continue at existing rates.

- Capital investment is funded through additional debt issuance.

- The leverage ratio continues to deteriorate, raising long-term sustainability questions.

Scenario 2: Temporary Profit Retention

- The government authorises Codelco to retain a greater share of earnings through approximately 2030.

- Reduced debt issuance gradually improves the leverage ratio.

- Short-term treasury inflows decline, creating a fiscal trade-off that requires political management.

Scenario 3: Structural Reform With Selective Private Capital

- Private-capital partnerships are introduced at the asset or non-core business level.

- A hybrid public-private model reduces debt dependency without requiring full divestiture.

- Full privatisation remains constitutionally prohibited without a legislative supermajority.

The most credible near-term outcome is a combination of temporary profit retention, selective private partnerships on non-core assets, and a governance restructure, all of which are achievable without amending Chile's constitution.

What a Holding-Company Model Would Actually Change

Divisional Autonomy as an Accountability Tool

The holding-company model recommended by Cesco represents a fundamental departure from Codelco's current centralised architecture. Rather than consolidating all operational results into a single corporate entity, the model would establish Codelco as a parent holding company overseeing a series of more independent operating divisions, each with its own financial reporting obligations.

The practical implications of this shift are significant:

- Each division would be evaluated against its own cost structure, revenue generation, and production targets rather than being absorbed into a consolidated average.

- Management teams would face clearer performance benchmarks tied to divisional outcomes.

- Capital allocation decisions would be subject to divisional-level scrutiny, reducing the risk of cross-subsidisation where profitable operations mask chronic underperformers.

- External oversight, including parliamentary scrutiny and bondholder analysis, would become more granular and more effective.

This structural change would also enable a more rational approach to private-capital partnerships. If a specific division or asset is identified as a candidate for external investment, that process is far more straightforward when the division operates with transparent, independently reported financials than when it is embedded within a consolidated corporate structure.

Board Renewal and Beyond

Installing three new board members is the most visible early step in the Kast administration's governance programme. However, board composition alone is insufficient to resolve deeply embedded structural problems. The more consequential reforms are likely to involve:

- Mandatory divisional financial reporting with standardised metrics comparable to private-sector disclosure norms.

- Independent oversight mechanisms for major capital project approvals, addressing the cost overrun problem at the source.

- Defined performance benchmarks for divisional management teams with consequences for sustained underperformance.

- Enhanced transparency requirements for decision-making processes involving major procurement or partnership agreements.

Privatisation: The Option That Remains Off the Table

Constitutional Architecture and Political Reality

The question of Codelco privatisation surfaces periodically in Chilean political discourse, particularly when the company's financial performance deteriorates. The practical constraints, however, are substantial. Codelco's status as a state-owned enterprise is embedded in Chile's constitution, making full privatisation legally impossible without a legislative supermajority. The Kast administration has explicitly ruled out pursuing that path in the current political environment.

The distinction that matters in the current reform debate is not between public and private ownership but between strategic control and operational financing. The government's intent is to retain full strategic control over copper production while exploring mechanisms to reduce the company's dependence on debt financing for capital investment. Selective private partnerships on non-core assets represent the most legally viable mechanism for achieving this without triggering constitutional constraints.

Codelco's copper strategy in the context of global trade pressures adds yet another layer of complexity to this already challenging reform agenda. The real debate in Santiago is not about whether to sell Codelco but about how to give it sufficient financial oxygen to remain competitive in a global copper market that increasingly rewards producers with low leverage and strong project execution capabilities.

The next major ASX story will hit our subscribers first

Global Copper Markets and the Stakes of Reform Success

Supply Constraints and the Electrification Demand Wave

The timing of this governance crisis carries particular significance for global copper markets. Copper demand driven by electric vehicle manufacturing, grid infrastructure expansion, and industrial electrification is expected to place sustained upward pressure on supply through the coming decade. Against this backdrop, any sustained underperformance by the world's largest copper producer is not a contained bilateral issue between Codelco and the Chilean treasury. It is a supply-side variable with direct price implications for every downstream manufacturer dependent on copper as an industrial input.

Successful governance reform and balance sheet repair at Codelco could unlock the company's capacity to accelerate capital deployment into delayed projects, partially offsetting the tighter supply conditions that are already visible in current pricing. The broader copper supply crunch facing global markets means that Codelco's recovery timeline matters well beyond Chile's borders. At the time of this reporting, copper was trading near $5.64 per pound, approaching levels that reflect genuine supply-demand tightness rather than speculative positioning alone.

Chile's Broader Economic Vulnerability

Finance Minister Quiroz's acknowledgment that Chile's economic reliance on copper as a single dominant export commodity requires serious policy reconsideration reflects a sophistication that goes beyond Codelco-specific concerns. A country whose fiscal position is this closely correlated with the health of a single state enterprise faces compounded vulnerability. Governance weakness at Codelco amplifies Chile's export concentration risk, reduces national economic resilience, and creates contingent fiscal liabilities that can constrain the government's capacity to respond to other economic shocks.

A credible and well-executed Codelco governance overhaul amid debt concerns would carry benefits well beyond Codelco's own balance sheet. Improved project execution and financial transparency would reduce the risk premium that copper market participants currently assign to Chilean supply reliability. It would strengthen Chile's sovereign credit profile by reducing contingent liabilities. Furthermore, it would signal to international capital markets that the country's most important industrial asset is being managed with institutional rigour commensurate with its global significance.

The challenge is substantial. Decades of structural underinvestment, politically influenced management cycles, and a fiscal transfer framework designed for a different era have created compounding problems that no single reform can resolve quickly. Consequently, the company's ability to reclaim its top copper producer status on a financially sustainable footing will depend on whether structural reforms are implemented with sufficient depth and consistency. What the current Codelco governance overhaul amid debt concerns represents is the recognition, at the highest levels of the Chilean government, that the cost of inaction now exceeds the political difficulty of reform. As analysts at Ainvest have noted, the $20 billion debt burden makes meaningful reform not merely desirable but essential for the company's long-term viability.

This article contains forward-looking assessments and analytical interpretations of publicly available information. It does not constitute financial or investment advice. Readers should conduct independent research before making any investment decisions related to the copper sector or Chilean sovereign instruments.

Want to Track the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their exceptional market returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.