June 8, 2026

Understanding Continental Resource Leverage in the Global Energy Transition

Modern energy infrastructure depends heavily on specialized materials that possess unique physical and chemical properties essential for renewable technologies, electric vehicle manufacturing, and advanced electronics systems. The geographic distribution of these materials creates strategic opportunities for resource-holding regions, particularly as global economies transition away from fossil fuel dependencies toward electrified and digitized systems. Understanding Africa's critical minerals deal terms becomes crucial in this context.

The concentration of critical mineral reserves across specific geographic regions represents more than geological coincidence. It reflects billions of years of specialized geological processes that created concentrated deposits of elements like lithium, cobalt, rare earth elements, and platinum group metals in relatively few locations worldwide. This natural scarcity generates leverage for countries possessing significant reserves, but only when negotiation frameworks capture value beyond raw material extraction.

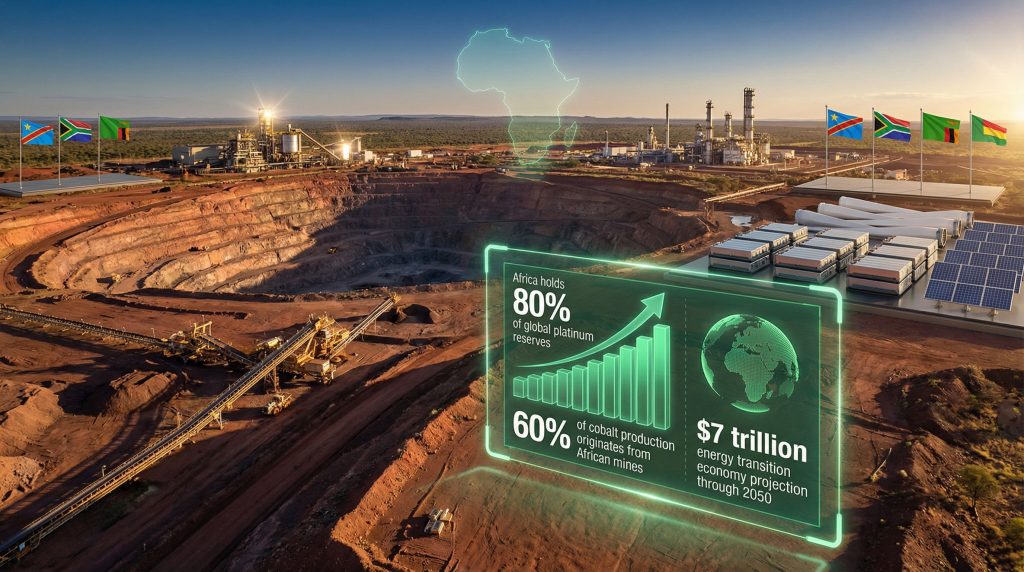

Continental Africa holds commanding positions in several minerals essential for clean energy infrastructure. South Africa and Zimbabwe control approximately 94% of global platinum reserves, with Zimbabwe alone containing roughly 27% of worldwide platinum deposits. The Democratic Republic of Congo produces approximately 70% of global cobalt, while Guinea possesses substantial bauxite reserves critical for aluminum production. These geological endowments position African nations at the center of supply chains worth hundreds of billions of dollars annually.

However, mineral wealth alone does not guarantee economic transformation. The structure of extraction agreements, processing requirements, and value chain integration determines whether resource endowments generate sustainable development or perpetuate dependency patterns established during earlier commodity cycles.

When big ASX news breaks, our subscribers know first

Strategic Bottlenecks Driving Global Competition for African Resources

The transition to renewable energy systems creates unprecedented demand for specialized materials with limited geographic availability. Unlike conventional commodities where substitution remains feasible, critical minerals & energy security often possess unique properties that cannot be replicated through alternative materials or synthetic processes.

Lithium demand trajectories exemplify this dynamic. The International Energy Agency projects lithium requirements will increase approximately 40-45 times by 2040 under current clean energy policy scenarios. This represents a 3,900-4,400% increase in annual consumption, driven primarily by battery storage systems for electric vehicles and grid-scale energy storage installations.

Battery manufacturing requires specific mineral compositions with minimal tolerance for quality variations:

- NCA (Nickel-Cobalt-Aluminum) batteries: 8kg lithium, 2kg cobalt, 2kg nickel, 3kg graphite per kWh

- NMC (Nickel-Manganese-Cobalt) batteries: 8kg lithium, 1.2kg cobalt, 2.5kg nickel, 3kg graphite per kWh

- LFP (Lithium Iron Phosphate) batteries: 7kg lithium, no cobalt requirement, 8kg graphite per kWh

These specifications demonstrate how battery chemistry choices directly influence mineral demand patterns and create specific sourcing requirements for manufacturing companies.

Rare earth elements present similar constraints. Wind turbine permanent magnets typically contain 30-32% neodymium and 6-8% dysprosium by weight, with no viable substitutes for high-performance applications. Approximately 80-85% of rare earth refining capacity remains concentrated in China, creating supply chain vulnerabilities that drive diversification strategies among importing nations.

Processing concentration amplifies supply risks. Roughly 65-70% of lithium conversion capacity operates in China, while 80% of cobalt refining occurs in China and Belgium combined. This geographic concentration creates leverage opportunities for raw material suppliers but also demonstrates how processing location determines value capture distribution along supply chains.

The designation of certain minerals as "strategic critical materials" by the U.S. Department of Energy and EU Commission elevates them beyond traditional commodity classification. This strategic framing justifies government involvement in supply agreements and long-term procurement strategies that prioritise security over cost optimisation.

How Current Agreement Structures Limit African Value Capture

Analysis of recent mining agreements reveals consistent patterns where African governments provide binding commitments while international partners offer conditional support mechanisms with limited enforceability. These patterns highlight the need for better Africa's critical minerals deal terms.

Typical African Government Obligations Include:

- Reserved access rights to specified mineral assets for 15-25 year periods

- Tax stabilisation commitments preventing rate increases during project lifecycles

- Regulatory framework modifications to accommodate investor requirements

- Infrastructure development cost-sharing arrangements

- Flexibility in local content requirements during initial project phases

International Partner Commitments Typically Feature:

- Technical assistance programmes with advisory-level obligations

- Security cooperation arrangements subject to government approval

- Market access facilitation through existing commercial networks

- Processing investment intentions without binding timelines

- Skills development initiatives with undefined performance metrics

Financial terms demonstrate this asymmetry clearly:

| Agreement Component | African Obligation Level | International Commitment Level |

|---|---|---|

| Royalty Rates | 2-5% (legally binding) | Market-based pricing (flexible) |

| Tax Incentives | Statutory changes required | Conditional on investment targets |

| Processing Requirements | Flexible timelines permitted | Advisory support only |

| Infrastructure Investment | Co-financing commitments | Financing under consideration |

| Local Content | 30-60% (stated targets) | Best-effort compliance |

Case Study: DRC Cobalt Agreement Evolution

The Democratic Republic of Congo's 2021 Mining Code amendments increased cobalt royalty rates from 2% to 3.5% while introducing processing investment requirements. However, subsequent negotiations with major operators resulted in rates settling at 2.5-3% in exchange for binding processing facility construction commitments. The evolving DRC cobalt developments demonstrate these negotiation dynamics.

These agreements now include financial penalties of $500 million to $1 billion if processing milestones are not achieved within specified timeframes. This represents a significant evolution from earlier agreements that lacked enforceable processing obligations.

Namibian Uranium Processing Model

Namibia's recent uranium mining agreements with international operators include binding local processing requirements with graduated implementation schedules. Agreements specify that 60% of uranium concentrate processing must occur domestically by project year 5, escalating to 80% by year 10.

Non-compliance triggers penalty provisions and potential licence revocation, demonstrating how newer agreements incorporate stronger enforcement mechanisms compared to traditional mining contracts.

The Economics of Fragmented Versus Coordinated Negotiation

When individual African countries negotiate mining agreements independently, they often create competitive dynamics that systematically favour international partners through induced bidding wars for investment capital. This fragmentation contrasts with the integrated approach seen in the global mining landscape.

Documented competitive effects include:

- Tax incentive escalation between neighbouring jurisdictions

- Weakened environmental and social performance standards

- Reduced local content requirements to attract investment

- Accelerated permitting processes that limit community consultation

- Infrastructure development obligations shifted toward government budgets

Research on competitive tax bidding between 2010-2015 shows copper royalty rates declined from 5-6% to 2-3% across southern African countries as governments competed for mining investment during commodity price volatility periods.

Processing Investment Scale Requirements

Individual country agreements rarely generate sufficient throughput volumes for economically viable processing facilities. Most beneficiation projects require minimum annual throughput capacities that exceed single-country production levels:

- Lithium conversion facilities: Minimum 20,000-30,000 tons annual capacity

- Cobalt refining operations: Minimum 15,000-25,000 tons annual throughput

- Rare earth processing plants: Minimum 5,000-10,000 tons rare earth oxides annually

- Platinum group metal refining: Minimum 200,000-400,000 ounces annual capacity

These scale requirements necessitate regional coordination to aggregate sufficient feedstock volumes for economically justified processing investments.

Value Addition Multiplier Effects Across Processing Levels

The economic impact of mineral processing extends far beyond direct employment creation, generating multiplier effects that transform regional economic structures. The mining industry evolution demonstrates these transformative effects.

| Processing Level | Value Addition Multiple | Employment Impact | Skills Development |

|---|---|---|---|

| Raw Ore Export | 1.0x baseline | 5,000-8,000 jobs | Basic mining operations |

| Concentrate Production | 2.5x baseline | 12,000-18,000 jobs | Technical operations |

| Refined Materials | 4.2x baseline | 25,000-35,000 jobs | Advanced chemistry |

| Component Manufacturing | 7.8x baseline | 45,000-65,000 jobs | Engineering expertise |

| Finished Products | 12.5x baseline | 80,000-120,000 jobs | Advanced manufacturing |

Employment data reflects direct and indirect job creation per billion dollars of mineral production value, based on International Labour Organisation analysis of mining sector employment patterns and World Bank studies on manufacturing sector linkages.

South Africa's platinum sector demonstrates these dynamics. Raw platinum exports generate approximately $5-6 billion annually, but refined platinum products and specialty applications generate 2.5-3x higher margins. However, South Africa processes only 40% of its platinum domestically, with higher-margin refining concentrated in Europe and North America.

Environmental and Social Governance Integration in Modern Agreements

Contemporary critical mineral agreements increasingly incorporate environmental performance requirements that extend beyond traditional mining regulations. The integration of renewable energy solutions becomes essential in these frameworks.

Environmental Standards Now Include:

- Carbon footprint reduction targets aligned with Paris Climate Agreement commitments

- Water usage optimisation requirements with recycling rate minimums

- Biodiversity impact mitigation through offset and conservation programmes

- Waste management standards incorporating circular economy principles

- Renewable energy utilisation mandates for mining operations

Social Impact Performance Indicators:

- Local employment percentage targets with skills development programmes

- Community development fund contributions tied to production volumes

- Indigenous rights protection measures with consultation requirements

- Gender equality promotion programmes in workforce development

- Education and healthcare infrastructure support commitments

These requirements reflect global investor emphasis on Environmental, Social, and Governance (ESG) compliance, but also create opportunities for African governments to negotiate broader development commitments beyond traditional fiscal arrangements.

The next major ASX story will hit our subscribers first

Technological Innovation and Mineral Demand Evolution

Battery chemistry evolution significantly impacts critical mineral demand patterns, creating both opportunities and risks for resource-holding countries.

Lithium Iron Phosphate (LFP) battery adoption eliminates cobalt requirements entirely while increasing graphite demand. Chinese manufacturers have achieved LFP cost reductions of 30-40% compared to nickel-cobalt chemistries, driving rapid market share growth in electric vehicle applications.

Solid-state battery development could revolutionise mineral demand profiles by 2030-2035. These technologies potentially reduce lithium requirements by 20-30% while eliminating liquid electrolyte components. However, solid-state batteries may increase demand for specialised materials like lithium metal and ceramic separators.

Recycling technology advancement will create secondary supply sources for critical minerals. Battery recycling facilities can recover 95% of lithium, 95% of cobalt, and 95% of nickel from end-of-life batteries. As recycling capacity expands through 2030-2040, primary extraction demand may moderate despite overall market growth.

Regional Integration Opportunities Through Coordinated Resource Development

Coordinated African approaches to critical minerals development can accelerate continental integration through shared infrastructure projects and harmonised regulatory frameworks. Furthermore, these initiatives build on African mineral potential that requires strategic coordination.

Cross-Border Infrastructure Development:

- Multi-country rail networks connecting mining regions to processing hubs and export terminals

- Shared electricity generation and transmission systems serving industrial corridors

- Integrated water management systems supporting multiple jurisdictions

- Common logistics and warehousing facilities reducing transportation costs

Technical Expertise Sharing:

- Regional centres of excellence for mining engineering and metallurgy

- Shared research and development facilities for beneficiation technology

- Joint training programmes for specialised technical skills

- Integrated quality control and certification systems

The African Continental Free Trade Area (AfCFTA) creates institutional frameworks for coordinated resource development, but implementation requires specific protocols for mining sector integration and dispute resolution mechanisms.

Investment Risk Mitigation Through Multilateral Frameworks

Development finance institutions can support coordinated African approaches through risk-sharing mechanisms that reduce country-specific investment concerns.

Available Financing Mechanisms Include:

- Regional infrastructure development funds with sovereign guarantees

- Processing facility co-investment programmes reducing equity requirements

- Technical assistance coordination reducing implementation costs

- Political risk insurance covering regulatory and currency risks

The World Bank's Infrastructure Investment Programme has allocated $2.3 billion for African mining-related infrastructure development through 2028, while the African Development Bank's industrialisation strategy prioritises mineral processing capacity development.

China's Belt and Road Initiative has committed over $60 billion to African infrastructure projects, with significant focus on mining sector transportation and processing facilities. However, these arrangements often include long-term commodity supply commitments that limit African negotiation flexibility.

Future Scenarios for African Critical Minerals Development

Three primary development pathways emerge from current negotiation patterns and global demand projections.

Status Quo Fragmentation Scenario:

Individual African countries continue competing for investment through reduced fiscal terms and weakened processing requirements. This scenario maintains Africa as a raw material supplier with limited value addition, generating $180-220 billion in annual mineral exports by 2040 but minimal industrialisation impact.

Selective Coordination Scenario:

Regional blocs coordinate negotiation standards while maintaining country-specific agreements. Southern African countries align platinum and chrome agreements, while West African countries coordinate bauxite and iron ore terms. This approach could capture $280-340 billion annually by 2040 with moderate processing development.

Full Continental Integration Scenario:

African Union establishes binding minimum standards for critical minerals agreements across all member countries. Coordinated approach enables large-scale processing investments and integrated supply chains, potentially generating $420-580 billion annually by 2040 with substantial industrialisation effects.

Implementing Coordinated Negotiation Frameworks

Successful coordination requires institutional mechanisms that balance national sovereignty with collective bargaining advantages.

Technical Capacity Development Requirements:

- Specialised expertise in mineral economics and international valuation methodologies

- International trade law knowledge covering investment treaties and dispute resolution

- Environmental impact assessment capabilities for complex industrial projects

- Social development planning skills for community engagement and benefit-sharing

- Financial modelling and risk analysis competencies for long-term project evaluation

Institutional Framework Components:

- Regional coordination secretariat with technical advisory committees

- Standardised monitoring and evaluation systems across participating countries

- Binding dispute resolution mechanisms for inter-country coordination issues

- Information sharing platforms for market intelligence and negotiation best practices

- Regular review processes for updating minimum standards based on market conditions

The Economic Community of West African States (ECOWAS) has established preliminary frameworks for mining sector coordination, while the Southern African Development Community (SADC) maintains mineral resource development protocols that could be expanded for critical minerals.

Long-Term Strategic Implications for African Economic Transformation

Well-structured critical mineral agreements can catalyse broader economic development through manufacturing sector growth, financial sector expansion, and technology ecosystem creation.

Economic Multiplier Effects Include:

- Local manufacturing development serving mining sector supply chains

- Financial services expansion supporting project financing and trade finance

- Technology sector growth through digitisation of mining and processing operations

- Service industry development in logistics, consulting, and technical services

- Export diversification reducing dependence on single commodity cycles

African countries that successfully implement coordinated approaches could capture 15-25% of global critical minerals value chains by 2040, compared to the current 8-12% share concentrated primarily in raw material extraction.

The transformation potential extends beyond mining sector impacts. Coordinated mineral development creates precedents for regional integration in other sectors, demonstrates African negotiation capacity to international partners, and generates financial resources for broader development programming.

However, success depends on sustained political commitment across participating countries, technical capacity development within government institutions, and careful balance between coordination benefits and individual country interests.

Africa's critical minerals deal terms will ultimately determine whether the continent's geological advantages translate into sustainable economic transformation or perpetuate extractive dependency patterns. The opportunity exists, but realisation requires sophisticated negotiation approaches that capture long-term development value while maintaining attractive investment conditions for international partners.

Disclaimer: This analysis involves forecasts and projections based on current market conditions and policy trends. Actual outcomes may differ significantly due to technological developments, policy changes, market volatility, and other factors beyond the scope of this assessment. Readers should consult additional sources and professional advisors before making investment or policy decisions related to critical minerals development.

Ready to Capitalise on Africa's Critical Minerals Boom?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market as the critical minerals sector accelerates. Understand why major mineral discoveries can lead to substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 30-day free trial today to position yourself ahead of the market.