May 21, 2026

Why the Hub-and-Spoke Model Is Reshaping Junior Copper Development in Australia

The economics of developing a standalone copper mine have shifted dramatically over the past decade. Rising energy costs, tighter labour markets, and increasingly complex permitting environments have pushed the break-even capital threshold for new projects to levels that make independent development prohibitive for smaller operators. In this environment, a quieter but increasingly influential model has emerged across the ASX: centralised processing hubs that aggregate ore from multiple sources, spreading fixed infrastructure costs across a broader production base. The Hillgrove and Havilah Mutooroo Copper Project deal is one of the most instructive recent examples of this model in action.

When big ASX news breaks, our subscribers know first

Understanding the Earn-In Structure Behind the Mutooroo Partnership

What an Earn-In Agreement Actually Means for Investors

An earn-in is a contractual arrangement in which one company acquires a percentage interest in another party's mineral project by committing to a defined work program or expenditure schedule over an agreed timeframe. Unlike an outright acquisition, the earner does not pay for the asset upfront. Instead, value is transferred progressively as technical milestones are achieved and capital is deployed. This structure is particularly well-suited to the current Australian junior mining environment, where capital scarcity and development cost inflation make outright purchases difficult to justify without substantially de-risking a project first.

The agreement between Hillgrove Resources (ASX: HGO) and Havilah Resources (ASX: HAV) follows this format precisely. Hillgrove has been granted the right to earn up to an 80% interest in the Mutooroo Copper Project through a staged commitment structured across three distinct phases. Furthermore, these majors-junior partnerships are increasingly common across the ASX as capital constraints reshape deal structures.

The Three-Stage Earn-In: How the Capital Flows

The deal is constructed to protect both parties from overcommitting before key technical questions are resolved. Here is how each stage works:

-

Initial share issuance: Hillgrove issues $5 million in shares to Havilah as the opening consideration. This creates an immediate equity alignment between the two companies, giving Havilah a stake in Hillgrove's performance from day one.

-

Drilling investment phase: Hillgrove commits to spending up to $10 million in new drilling over a period of up to 24 months. The drilling program is designed to confirm resource continuity, support metallurgical test work, and generate the technical inputs needed for a prefeasibility study (PFS).

-

Final investment decision payment: Upon a positive FID, Hillgrove pays Havilah a further $35 million, structured as between 30% and 70% in cash with the remainder in shares. At this point, Hillgrove earns its full 80% project interest, while Havilah retains a 20% carried or contributing interest.

The total potential consideration flowing to Havilah across all three stages could reach approximately $50 million, a figure that represents a meaningful premium relative to Havilah's pre-announcement market capitalisation.

A critical but often overlooked feature of this structure is that the PFS expenditure is intended to be funded entirely from Hillgrove's operating cash flow. This approach limits shareholder dilution risk and signals that Hillgrove's board has sufficient confidence in the Kanmantoo operation's cash generation to self-fund the study without a capital raise.

The Mutooroo Resource: What the JORC Numbers Actually Tell Us

Breaking Down the Mineral Resource Estimate

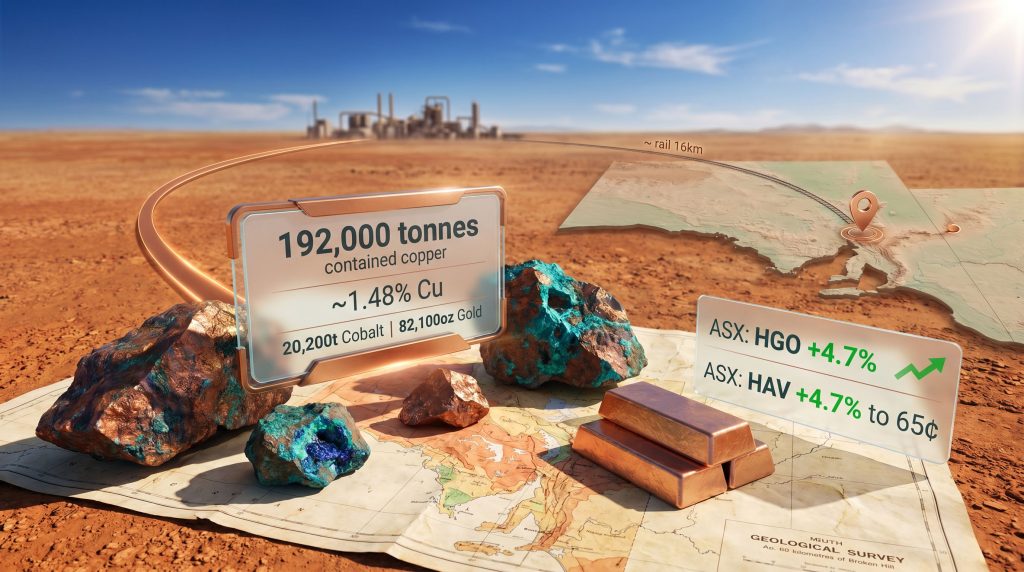

The Mutooroo Copper Project holds a JORC Sulphide Mineral Resource Estimate that positions it as a credible development-stage asset. The key metrics are summarised below:

| Metric | Mutooroo (Havilah) |

|---|---|

| Contained Copper (JORC) | ~192,000 tonnes |

| Cobalt Content | ~20,200 tonnes |

| Gold Content | ~82,100 ounces |

| Resource Grade | ~1.48% Cu (13.1Mt) |

| Development Stage | Pre-Feasibility Study (PFS) |

The grade of approximately 1.48% copper is notably higher than many of the large-tonnage porphyry copper projects that dominate global supply. Most large-scale copper mines globally operate at grades between 0.4% and 0.8% Cu, meaning Mutooroo's sulphide resource sits at roughly double to triple the average feed grade of many operating mines. For a centralised processing hub model, higher feed grades reduce the volume of material that needs to be trucked or railed, which directly improves the logistics economics of the hub-and-spoke arrangement.

The polymetallic credits are also significant. The cobalt content of approximately 20,200 tonnes adds a layer of potential revenue diversification, given cobalt's role in battery cathode chemistry and its own supply constraints. The 82,100 ounces of gold provides further by-product credit that could meaningfully improve the project's all-in sustaining cost profile at the feasibility stage.

The Sulphide Mineralisation Distinction

It is worth understanding why the JORC resource specifically references sulphide mineralisation. Sulphide copper ores require flotation-based processing to produce a copper concentrate, which is then smelted into refined metal. This processing pathway is standard at facilities like Kanmantoo, which already operates a flotation circuit. The various copper processing methods available to operators differ significantly in their infrastructure requirements and cost profiles. The fact that Mutooroo's resource is sulphide-dominant is precisely what makes routing its ore through Kanmantoo's existing plant a technically credible proposition, subject to metallurgical test work confirming compatibility.

Location and Logistics: Why Geography Matters for Project Economics

Mutooroo sits approximately 60km southwest of Broken Hill in South Australia. Critically, it is located only around 16km from the Transcontinental Railway Line and Barrier Highway, two of South Australia's most significant freight corridors. For a hub-and-spoke mining model, proximity to established logistics infrastructure is not a minor footnote. It is a primary determinant of whether trucking or rail haulage of ore to a processing facility is economically viable.

The distance between Mutooroo and the Kanmantoo processing facility in the Adelaide Hills is substantial, which means that ore transport costs will be a central variable in the PFS economics. However, the proximity to the Transcontinental Railway Line means that rail haulage is a realistic option, potentially offering a lower per-tonne cost than long-distance road transport. The PFS will need to model both scenarios carefully, and the outcome of this analysis will be a key determinant of whether the FID proceeds.

The Kanmantoo Processing Hub: Hillgrove's Core Strategic Asset

From Single Mine to Multi-Source Processor

Kanmantoo is Hillgrove's underground copper operation in the Adelaide Hills. Hillgrove made a final investment decision to restart the operation in 2023, with first concentrate shipment achieved in June 2024. The restart demonstrates that the facility is operational and capable of producing market-grade copper concentrate. However, as a single-source operation, Kanmantoo faces a natural production ceiling determined by the underground mine's own ore reserve.

This is where the Hillgrove and Havilah Mutooroo Copper Project deal changes Hillgrove's strategic calculus entirely. If Mutooroo ore can be processed through Kanmantoo, Hillgrove gains access to a second feed source without needing to build a second processing plant. The company has flagged that adding Mutooroo to its ore feed pipeline could potentially lift copper output beyond 20,000 tonnes per annum (20kt pa), a threshold that would represent a meaningful step-change in Hillgrove's production profile and revenue base.

Capital Efficiency Through Infrastructure Leverage

The capital efficiency argument for the hub-and-spoke model is compelling when compared to standalone development alternatives:

-

A greenfield standalone copper processing facility capable of handling Mutooroo's resource would require construction of a new concentrator, tailings storage facility, water and power infrastructure, site access roads, and all associated approvals.

-

Routing Mutooroo ore through Kanmantoo avoids the capital cost of constructing all of this infrastructure from scratch, leveraging assets that Hillgrove has already built, permitted, and operationalised.

-

The existing workforce, site approvals, and operational capability at Kanmantoo represent genuine de-risking factors that a standalone development would need to replicate entirely.

-

Metallurgical test work remains the critical outstanding variable. If Mutooroo ore responds well in Kanmantoo's flotation circuit, the capital efficiency case strengthens substantially.

Hillgrove's CEO Bob Fulker has articulated that the staged PFS approach, funded from operating cash flow, ensures capital is only deployed as technical assumptions are validated. This reflects a disciplined capital deployment philosophy that is increasingly rare among ASX junior miners, where growth ambitions often outrun available funding.

What the Deal Means for Havilah Shareholders

Unlocking a High-Quality but Capital-Intensive Asset

Mutooroo has been one of Havilah's most significant assets for years, but the project faced a fundamental challenge: the capital cost of a standalone processing facility was difficult to justify for a company of Havilah's market capitalisation. The resource is high-grade and well-located relative to logistics infrastructure, but without a cost-effective processing pathway, it remained largely stranded on Havilah's books.

The Hillgrove partnership resolves this problem by providing a credible, lower-capital development pathway. Havilah's technical leadership has noted that the arrangement has the potential to substantially reduce execution risk for Havilah shareholders, an assessment that the market appeared to endorse. Havilah shares rose 7.4% to 65 cents in early trade following the announcement.

Havilah's retained 20% project interest also carries meaningful optionality value. If Mutooroo advances to production, Havilah holds a free-carried or contributing interest in what could become a producing copper asset, without bearing the full development burden.

It is also worth noting Havilah's prior engagement with JX Advanced Metals Corporation regarding Mutooroo. International strategic interest in the project from a major metals company signals that Mutooroo's resource quality and strategic location have attracted attention beyond the domestic ASX investor base, adding a layer of credibility to the project's long-term value proposition.

The next major ASX story will hit our subscribers first

Risk Factors Every Investor Should Understand

The deal is structured sensibly, but several material risks remain:

-

Metallurgical compatibility: The most critical near-term risk is whether Mutooroo's sulphide ore will process efficiently through Kanmantoo's existing flotation circuit. This is not guaranteed, and test work results could alter the economics substantially.

-

Ore transport economics: The logistics cost of moving ore from Mutooroo to Kanmantoo is a central PFS variable. If rail haulage proves uneconomic or unavailable, truck haulage costs could compress project margins significantly.

-

PFS outcomes: A PFS is not a bankable feasibility study. Its conclusions are indicative, not definitive. Hillgrove's FID commitment hinges on PFS outcomes being sufficiently positive to justify the $35 million payment to Havilah. In addition, a definitive feasibility study would represent a further, more rigorous evaluation hurdle before full project sanctioning.

-

Copper price sensitivity: Project economics at FID will be directly influenced by prevailing copper prices. A sustained decline from current levels could push the project's internal rate of return below Hillgrove's investment threshold.

-

Execution timeline: A 24-month drilling window is relatively tight for a project of this complexity. Delays in permitting, wet season access, or rig availability could push key milestones back.

This article contains general information only and does not constitute financial advice. Investors should conduct their own due diligence and consider their personal circumstances before making any investment decision. Past performance is not indicative of future results.

The Broader Copper Supply Context: Why Timing Matters

The Hillgrove and Havilah Mutooroo Copper Project deal does not exist in a vacuum. It is unfolding against a backdrop of structural copper supply constraints that have been building for years. Global copper demand is being driven by a convergence of electrification trends: electric vehicle adoption, renewable energy grid buildout, data centre infrastructure, and industrial electrification are all copper-intensive at a scale that existing mine supply is struggling to match. The copper supply crunch is, furthermore, intensifying pressure on developers to bring credible mid-tier projects like Mutooroo to the market efficiently.

On the supply side, the major copper mining nations are contending with declining ore grades at existing operations, longer lead times for new project approvals, rising development costs, and geopolitical risk in key producing regions. Australia's relatively stable regulatory environment and established mining jurisdiction credentials make South Australian copper projects particularly attractive to both domestic and international capital.

Industry analysis has flagged the possibility of an acute copper supply shortfall over the medium term, with demand from electrification and AI-driven data centre buildout potentially outpacing new mine supply. Consequently, considered copper investment strategies are becoming increasingly important for investors seeking exposure to this structural demand story. In this context, projects like Mutooroo, sitting at the pre-feasibility stage with a defined high-grade resource, established logistics access, and a credible processing pathway, occupy a strategically valuable position in the global copper development pipeline.

Frequently Asked Questions: Hillgrove and Havilah Mutooroo Copper Deal

What is the Mutooroo Copper Project?

A high-grade copper-cobalt-gold project located in South Australia, approximately 60km southwest of Broken Hill, with a JORC Sulphide Mineral Resource of approximately 192,000 tonnes of contained copper at a grade of around 1.48% Cu.

How much is Hillgrove paying to earn into Mutooroo?

Hillgrove will issue $5 million in shares to Havilah upfront, invest up to $10 million in drilling over 24 months, and pay a further $35 million (30 to 70% cash, remainder in shares) upon a final investment decision to earn an 80% interest.

What is a prefeasibility study in mining?

A PFS is an intermediate technical and economic evaluation that assesses project viability in sufficient detail to support a decision on whether to proceed to a full feasibility study. It examines processing options, capital and operating cost estimates, infrastructure requirements, and preliminary project economics.

What is an earn-in agreement?

An earn-in is a contractual arrangement where one company acquires a percentage interest in another company's project by spending a defined amount or completing specified work programs. Ownership transfers progressively as milestones are met, rather than through an upfront purchase.

How did markets respond to the announcement?

Havilah shares rose approximately 7.4% to 65 cents, while Hillgrove shares gained approximately 4.7% to 4.4 cents on the announcement day, suggesting both shareholder bases viewed the deal favourably at first assessment.

Summary Scorecard: Assessing the Deal Across Both Parties

| Dimension | Hillgrove (HGO) | Havilah (HAV) |

|---|---|---|

| Primary Benefit | Capital-efficient production growth | Monetisation of a stranded asset |

| Capital Commitment | Up to ~$50M total (phased) | Receives $5M shares + $35M at FID |

| Risk Profile | PFS and metallurgical compatibility risk | Execution risk transferred to Hillgrove |

| Retained Interest | 80% upon FID | 20% project interest retained |

| Strategic Fit | Extends Kanmantoo processing hub model | Unlocks value without standalone capex burden |

What to Watch in the Months Ahead

-

Release of the formal PFS scope and indicative timeline

-

Results from the new drilling program across the 24-month window

-

Metallurgical test work outcomes confirming or complicating Kanmantoo plant compatibility

-

Copper price trajectory and its influence on project economics at FID

-

Any further international strategic interest in Mutooroo that could signal broader recognition of the project's value

Want to Capitalise on the Next Major ASX Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including high-grade copper projects like Mutooroo — instantly translating complex resource data into actionable insights for investors at every level. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.