July 15, 2026

The Invisible Bottleneck Reshaping Global Copper Markets

Copper has long been treated as the world's most reliable economic barometer, a metal whose price movements telegraph manufacturing cycles, construction booms, and infrastructure investment with remarkable precision. That relationship, built over decades of synchronised global industrial activity, is breaking down in 2026. The forces now driving copper pricing are not factory output rates in Guangdong or housing starts in the United States. They are sulphuric acid shipment logs from Chinese customs databases, warehouse receipt counts in COMEX-approved facilities, and the logistics constraints of a single shipping chokepoint in the Middle East.

Understanding how US tariff fragmentation and copper supply chain repricing have reshaped the market requires moving beyond traditional demand-side analysis entirely. The question facing institutional capital, procurement strategists, and project developers is no longer how much copper the world contains. It is which producers can deliver LME-grade refined cathode into increasingly fragmented Western supply chains before mid-2027, and at what cost.

Analytical framing: The copper market's dominant pricing variable in 2026 is not reserve depletion or demand growth. It is the deliverability of finished cathode under a bifurcated tariff regime combined with a chemical input supply crisis that is measurably reducing output from leaching operations across two continents.

When big ASX news breaks, our subscribers know first

What the Section 232 Tariff Architecture Actually Does to Copper Markets

When the United States announced its Section 232 copper tariff framework effective August 1, 2025, initial market reaction was swift and misdirected. COMEX copper futures surged approximately 13% on the assumption that broad import duties would cover all copper product categories. The subsequent price correction of roughly 19% from that spike revealed how poorly the bifurcated structure was initially understood. The tariff-driven copper rally exposed significant gaps in market comprehension of the policy's selective architecture.

The critical design feature of the Section 232 framework is its selectivity. Rather than applying a uniform duty across the copper value chain, the structure imposes differentiated rates that protect domestic fabricators while creating complex cost pass-through dynamics for downstream industries.

| Copper Product Category | Tariff Rate | Effective Date |

|---|---|---|

| Semi-finished products (pipes, tubes, wires, rods, sheets) | 50% | August 1, 2025 |

| Raw copper concentrates | 0% | August 1, 2025 |

| Refined copper cathode (key supplier nations) | Exempt | Transitional period |

| Projected refined copper tariff | 15% rising to 30% | 2027 to 2028 |

The 50% duty on semi-finished copper products does not get absorbed at the border. It cascades through downstream manufacturing in ways that compress margins across several capital-intensive sectors simultaneously:

- Construction: Copper pipe and tube pricing for plumbing, HVAC, and building services

- Automotive: Wiring harness components and electrical system fabrication inputs

- Electronics manufacturing: Copper rod and sheet used in circuit board and connector production

- Renewable energy infrastructure: Wiring for solar installations, wind turbines, and EV charging networks

Furthermore, the broader effects of US tariffs on copper supply chains have introduced structural uncertainty across procurement pipelines globally. Chile, which has historically accounted for a substantial share of US refined copper imports, and Canada, as a key Free Trade Agreement partner, received exemptions on raw concentrates and refined cathode. This exemption structure shields US semi-finished manufacturers from foreign competition while exposing midstream industries to significantly higher input costs, creating an uneven competitive landscape across the value chain.

Goldman Sachs and Citigroup analysts continued through early 2026 to forecast that the US could impose Section 232 copper import tariffs of up to 25% on refined copper cathode in a subsequent phase, with an anticipated July 2026 decision point. That expectation, rather than the current exemption structure, has driven the most significant inventory repositioning in the copper market in years.

How Policy Selectivity Drives Capital Repositioning

According to analysis from Fast Markets, the selectivity of US copper tariff policy has prompted trading desks and smelters to fundamentally reassess their logistics and warehousing strategies. Consequently, capital has begun migrating toward near-term producers capable of delivering into compliant Western supply chains ahead of anticipated tariff phase expansion.

How the COMEX-LME Premium Has Physically Rerouted Global Copper Flows

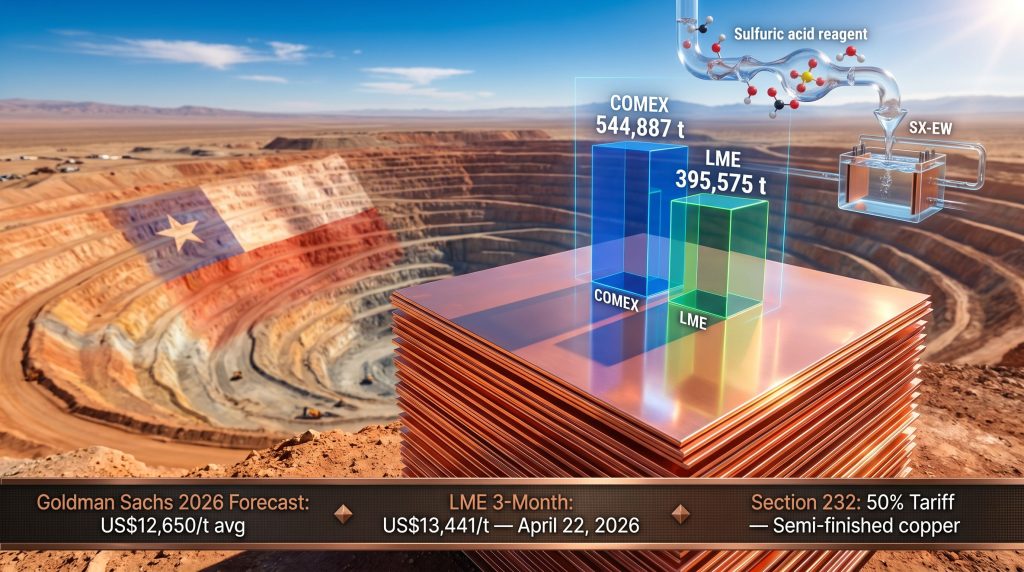

The mechanics of the COMEX-LME arbitrage are straightforward in theory and consequential in practice. When COMEX copper futures trade at a sustained premium to LME equivalent pricing, the economics of physically moving refined cathode into US warehouse locations improve. Trading desks, merchants, and smelters respond by redirecting supply toward the premium market, draining inventory from Asian LME warehouses while accumulating stocks in COMEX-approved US locations.

By April 22, 2026, COMEX copper inventories had reached 544,887 tonnes, within 980 tonnes of the February 2026 record of 545,867 tonnes. LME copper inventories stood at 395,575 tonnes over the same period, following sustained outflows from Asian warehouse locations. The COMEX-LME arbitrage premium peaked at approximately US$2,520 per tonne during 2025, a level that comfortably exceeded the transport and financing costs required to justify physical copper redirection.

| Inventory Metric | Value | Date |

|---|---|---|

| COMEX copper inventory | 544,887 tonnes | April 22, 2026 |

| LME copper inventory | 395,575 tonnes | April 22, 2026 |

| COMEX February 2026 record | 545,867 tonnes | February 2026 |

| COMEX-LME arbitrage peak | ~US$2,520/tonne | 2025 |

| Potential arbitrage ceiling projection | ~US$5,000/tonne | Estimated as US stocks draw down |

| US refined copper import increase | 500,000+ metric tonnes YoY | Early 2025 |

This inventory dynamic exposes a critical structural weakness in domestic US copper processing capacity. Annual US mine production runs at approximately 1.2 million tonnes, while domestic smelting capacity handles roughly 585,000 tonnes per year, leaving a processing gap of approximately 615,000 tonnes that must be exported to Mexico, Canada, Japan, and China for conversion into usable refined metal. New domestic sales requirements mandating that 25% of domestically mined copper be sold within the US, rising to 40% by 2029, add tension to this structural imbalance without addressing the underlying economics of domestic smelting.

Structural gap: The US tariff framework creates strong incentives to localise copper processing, but existing smelting economics remain unfavourable relative to established operations in Asia and Latin America. Tariff-driven policy cannot substitute for the capital investment required to close the midstream processing deficit.

As US stocks approach capacity ceilings, the arbitrage ceiling projection of approximately US$5,000 per tonne reflects the potential spread expansion as inventory draw-down forces buyers to pay escalating premiums for domestically warehoused cathode. This scenario remains speculative but is increasingly reflected in forward curve pricing. Investors should treat forward price projections as analytical scenarios rather than guaranteed outcomes.

The Sulphuric Acid Crisis: When a Chemical Input Becomes a Strategic Constraint

Solvent extraction-electrowinning, commonly known as SX-EW, accounts for approximately 17% of global copper supply and operates through a fundamentally different production pathway than conventional mining. Rather than producing copper concentrate for smelting, SX-EW circuits apply sulphuric acid as a lixiviant in heap-leach operations, dissolving copper from oxide and supergene ores and then recovering it through solvent extraction and electrowinning to produce finished LME-grade copper cathode without any smelter involvement.

This production bypass creates a distinct structural advantage in the current market environment. However, it also creates a distinct vulnerability: SX-EW output is directly proportional to acid availability. The ongoing copper supply crunch has made this chemical dependency increasingly visible to institutional investors and procurement teams alike.

China's Export Restriction and the Quantified Chilean Risk

Chinese sulphuric acid shipments to Chile followed a trajectory in early 2026 that has material implications for global copper supply balances:

| Period | Chinese Acid Shipments to Chile |

|---|---|

| March 2025 | 151,268 tonnes |

| February 2026 | 31,870 tonnes |

| March 2026 | Zero tonnes |

| Prior zero-shipment month | July 2023 |

China supplied approximately one-third of Chile's total sulphuric acid imports in 2025 and represented an estimated 20% of the acid used specifically in Chilean copper leaching operations. The shift from 151,268 tonnes to zero shipments over twelve months is not a gradual adjustment. It is a structural removal of a critical reagent input from the world's largest copper-producing nation. The Chile copper market outlook has consequently deteriorated sharply among forecasters tracking cathode deliverability into Western supply chains.

Goldman Sachs estimates that a sustained twelve-month Chinese export ban could place approximately 200,000 tonnes of Chilean cathode production at risk, equivalent to roughly 1% of annual global copper supply. Chilean producers face a constrained set of responses: sourcing replacement acid from Middle Eastern or European suppliers at longer lead times and higher freight costs, drawing down strategic acid reserves, or accepting proportional production curtailments tied to reduced acid availability.

The Strait of Hormuz Dimension

The second vector of acid supply risk operates through a different mechanism but converges on the same output constraint. Sulphur, the precursor chemical used to manufacture sulphuric acid, transits the Strait of Hormuz as part of Middle Eastern petrochemical export flows. Extended disruption to Hormuz shipping beyond late May 2026 could reduce Democratic Republic of the Congo copper production by an estimated 125,000 tonnes in 2026 alone, according to Goldman Sachs analysis.

The DRC's SX-EW copper sector relies on sulphur-derived acid sourced through supply chains that pass through or near this chokepoint. Unlike Chile, where the acid restriction is a direct policy action, the DRC faces a logistics pathway vulnerability that is harder to hedge through alternative sourcing contracts.

Combined supply risk scenario: Goldman Sachs analysis places up to 325,000 tonnes of combined cathode production at risk across Chile and the DRC under concurrent disruption scenarios, equivalent to approximately 1.5% of annual global copper supply despite the bank's simultaneous forecast of a 490,000-tonne 2026 market surplus. These projections carry uncertainty and should be treated as scenario analysis rather than base-case expectations.

The Chinese Smelter Paradox: Capacity Expansion Against Concentrate Constraints

China refined 14.72 million tonnes of copper in 2025, a scale that creates systemic global dependency for concentrate-producing miners. Yet the economics of Chinese smelting have deteriorated materially. The China Smelter Purchase Team (CSPT), the coordinating body for major Chinese copper smelters, issued no treatment charge or refining charge guidance for the fifth consecutive quarter as of April 2026, confirming that smelter economics have eroded to the point where standard benchmark negotiations have been suspended entirely.

Treatment charges (TC) and refining charges (RC) represent the fees smelters collect from miners for converting copper concentrate into refined metal. When these charges turn negative, as has occurred in the current cycle, it means smelters are effectively paying miners for the privilege of processing their ore, a structural inversion that reflects severe concentrate scarcity relative to installed smelting capacity.

Against this backdrop, the guidance issued by major CSPT members for 2026 production revealed a striking divergence from stated production discipline:

| Smelter | 2025 Actual Production | 2026 Guidance | Direction |

|---|---|---|---|

| Jiangxi Copper | 2.38 million tonnes | 2.39 million tonnes | Increase |

| Yunnan Copper | 1.64 million tonnes | 1.71 million tonnes | Increase |

| Daye Nonferrous | 716,000 tonnes | 713,000 tonnes | Marginal reduction |

The continued expansion of smelter output guidance against constrained concentrate supply has two structural consequences. First, it shifts bargaining power toward miners with concentrate to sell, as smelters compete for diminishing feedstock. Second, it reinforces the strategic premium attached to SX-EW projects that produce finished cathode without any smelter interaction, bypassing the TC/RC negotiation entirely and capturing the full copper price.

Capital Intensity as the New Development Screening Criterion

The shift in institutional capital allocation toward copper development assets in 2026 is not driven by resource scale or exploration upside. It is governed by a tightly defined set of pre-production economics that reflect the current financing environment. In addition, the range of viable copper investment strategies has narrowed considerably as capital intensity thresholds tighten.

Pre-production capital intensity for new copper projects typically ranges from US$15,000 to US$25,000 per tonne of annual production capacity, according to S&P Global's 2024 Mining Capital Intensity Database. Several large-scale greenfield developments have faced delays or scope reductions at these levels given elevated interest rates and extended permitting timelines. The market's preferred development threshold has moved below US$12,000 per tonne, representing a discount of 25% to 40% against the broader peer range.

Marimaca Copper's Marimaca Oxide Deposit in Chile's Antofagasta Region illustrates this dynamic directly. The company's 2025 Definitive Feasibility Study outlined:

- Pre-production capital costs: just under US$600 million

- Annual copper cathode production: 50,000 tonnes

- Capital intensity: approximately US$11,700 per tonne

- Strip ratio: 0.8:1 (versus the industry-typical 2:1 to 4:1 range)

- Internal rate of return: 39% at a US$4.30 per pound copper price assumption

- Construction target: end of 2026

The project's below-peer capital intensity is supported by the low strip ratio, which reduces ore movement costs materially, and by proximity to established port infrastructure in the Antofagasta Region. Marimaca's management has publicly anchored the engineering process to capital discipline within a broader risk management framework, indicating that cost reduction decisions are evaluated against overall project risk rather than pursued as standalone targets.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, has indicated that capital reduction decisions at the project level must always be assessed within the overall risk context of the development, rather than pursued as isolated engineering targets. (Source: Crux Investor, April 28, 2026)

Marimaca raised C$80 million in early 2026 per company disclosures, with the Pampa Medina sulphide footprint covering approximately 3 kilometres by 1.5 kilometres targeted for resource definition through 200,000 to 300,000 metres of drilling to be funded from operating cash flow rather than equity issuance.

The next major ASX story will hit our subscribers first

Infrastructure Access as a Quantifiable Capital Advantage

In established copper districts, the most significant capex line item for an SX-EW developer is often the electrowinning plant itself. Where that infrastructure already exists and carries underutilised nameplate capacity, the pre-production economics of an adjacent development asset change structurally.

Fitzroy Minerals signed a non-binding letter of intent with Sociedad Punta del Cobre S.A. (Pucobre) regarding the Buen Retiro Copper Project near Copiapó, Chile. Under the arrangement, Pucobre would make available at least 80% of the nameplate capacity at its Planta Biocobre electrowinning facility, which is capable of producing 800 tonnes of copper cathode per month, equating to approximately 9,600 tonnes annually.

The processing facility is located approximately 70 kilometres by road from the Buen Retiro project, which sits adjacent to the Pan-American Highway and Pacific coastal infrastructure. Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, has noted that access to an operational electrowinning tank-house reduces both capital expenditure requirements and the complexity of the permitting process for the project. (Source: Crux Investor, April 2026)

The Buen Retiro project carries additional district-level validation: Pucobre operated the Manto Negro copper oxide mine on the same property from 2005 to 2009, producing 34.4 million pounds of copper and establishing site-specific operational and environmental baselines that reduce geological and metallurgical risk relative to greenfield discoveries. The project also sits within the Punta del Cobre copper belt, where Lundin Mining's Candelaria copper-gold mine produced 145,000 tonnes of copper in 2025 per Lundin disclosures.

Under the existing option agreement signed in January 2023, Pucobre retains a 30% claw-back right exercisable following completion of the project's Final Technical Report, requiring reimbursement of 90% of eligible expenditures, or at least US$10.2 million, to Fitzroy. Commercial tolling terms for the Planta Biocobre facility are expected to be finalised within approximately 90 days to support the pre-feasibility study economic model, with Fitzroy targeting completion of all four option stages by Q2 2027.

Strategic Operator Participation and the Institutional Validation Signal

Abitibi Metals announced a C$30.75 million non-brokered private placement on April 23, 2026, with Discovery Silver Corp. expected to acquire an approximately 9.9% ownership stake upon closing. The financing includes:

- 11.76 million charity flow-through shares priced at C$0.85

- 35.78 million hard-dollar shares priced at C$0.58

- Participation rights allowing Discovery Silver to maintain proportional ownership in subsequent financing rounds

The announcement followed Abitibi's confirmation of 80% ownership of the B26 polymetallic copper-gold deposit in Québec in March 2026. Recent drill results returned 2.71% copper-equivalent over 7 metres within a broader interval grading 1.81% copper-equivalent over 15 metres in the project's western down-plunge zone.

Jonathon Deluce, President and Chief Executive Officer of Abitibi Metals, has noted that since optioning the project, total tonnage has grown by more than 125% through systematic drilling, underscoring the deposit growth trajectory that attracted strategic capital participation. (Source: Crux Investor, 2026)

The distinction between institutional and retail capital underwriting matters considerably for risk assessment. When a producing mining company acquires a ~10% strategic stake through a non-brokered placement, the transaction reflects technical due diligence that retail-facing brokered deals cannot replicate. This validation signal has become a screening criterion for sophisticated investors evaluating development-stage copper assets in the current environment.

Financing structure note: Charity flow-through shares allow Canadian mining companies to pass exploration expenditure tax deductions to investors while raising capital at a premium to market, effectively reducing the issuer's cost of capital. Hard-dollar shares represent direct equity participation without tax structure. Understanding this blended financing architecture is essential for evaluating dilution impact accurately.

Goldman Sachs' 2026 Copper Outlook and the Surplus-Premium Paradox

Goldman Sachs maintained its 2026 average copper price forecast at US$12,650 per tonne alongside a projected 490,000-tonne global market surplus, a combination that initially appears contradictory. The reconciliation lies in the supply chain fragmentation premium, which drives a wedge between headline market balance data and the pricing of deliverable cathode in Western-accessible locations. As the Atlantic Council has noted, the divergence between tariff policy and rare earth investment strategy reveals how fragmented trade architecture creates uneven pricing across commodity supply chains.

Three-month LME copper traded at US$13,441 per tonne on April 22, 2026, above the Goldman full-year average forecast, reflecting both the COMEX-LME premium effect and the acid-driven Chilean curtailment risk priced into the forward curve.

| Scenario | Copper Supply Impact | Key Driver |

|---|---|---|

| Base case (no additional disruption) | 490,000-tonne surplus | LME average ~US$12,650/t |

| Chinese acid ban sustained 12 months | ~200,000 tonnes Chilean cathode at risk | Export policy |

| Hormuz disruption beyond May 2026 | ~125,000 tonnes DRC reduction | Logistics pathway |

| Combined disruption scenario | Up to 325,000 tonnes combined | Concurrent geopolitical stress |

| LME spot (April 22, 2026) | US$13,441/t | COMEX premium and acid risk |

All Goldman Sachs projections carry inherent uncertainty. Price forecasts, supply risk estimates, and surplus calculations represent analytical scenarios subject to revision as market conditions evolve. This article does not constitute financial advice.

The Seven-Criterion Framework for Copper Development Assessment in 2026

Institutional capital allocation toward copper developers has converged around a multi-criterion framework that extends well beyond resource scale or grade. Projects that satisfy the majority of the following criteria are attracting disproportionate financing interest:

- Pre-production capital intensity below US$12,000 per tonne placing the project 25% to 40% below the S&P Global peer range

- SX-EW or direct cathode production pathway eliminating TC/RC exposure in a negative treatment charge environment

- Access to existing third-party processing infrastructure reducing standalone plant capex and permitting complexity

- Construction timeline targeting completion before mid-2027 to capture COMEX-LME premium and acid-driven Chilean curtailment pricing

- Sequential financing model funded from operating cash flow deferring exploration dilution to the post-construction phase

- Jurisdictional alignment with Western critical mineral procurement frameworks supporting offtake premiums under the European Critical Raw Materials Act and US Inflation Reduction Act sourcing requirements

- Strategic operator participation in financing validating technical quality through institutional rather than retail capital underwriting

The interaction between US tariff fragmentation and copper supply chain repricing has compressed the decision window for developers targeting this opportunity set. The forward curve pricing in both the COMEX premium and the acid supply risk creates a time-bounded window of elevated returns for projects capable of delivering cathode into Western supply chains before mid-2027. Projects that miss this window face a different market environment, one where the acid disruption may have been partially resolved and tariff policy may have crystallised into a new equilibrium.

For investors evaluating copper development assets, the core question has shifted from geological discovery risk toward supply chain execution risk: not whether the copper exists, but whether the developer can convert it into deliverable LME-grade cathode, at a defensible capital cost, within the window that current market fragmentation has opened. Furthermore, as Nasdaq analysis of copper policy risk has highlighted, the emerging copper premium reflects precisely this convergence of policy-driven fragmentation and physical scarcity, reinforcing the case that US tariff fragmentation and copper supply chain repricing remain the defining structural forces shaping investment decisions across the sector in 2026.

This article is intended for informational purposes only and does not constitute investment advice. All forward-looking statements, price forecasts, and production estimates carry material uncertainty. Readers should conduct independent due diligence and consult qualified financial advisors before making investment decisions. References to specific companies are for illustrative purposes and do not constitute a recommendation to buy or sell any security.

Want to Track the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, instantly translating complex geological and commodity data into actionable investment intelligence — ideal for investors navigating the supply chain fragmentation and tariff-driven repricing reshaping copper markets in 2026. Explore how historic mineral discoveries have generated exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next significant find.