July 9, 2026

Global resource competition has fundamentally shifted from traditional commodities to specialised materials that power modern technological systems. Critical minerals energy security now determines national economic capabilities and industrial competitiveness more than conventional energy sources or agricultural products. This transformation reflects the intersection of technological advancement, manufacturing complexity, and geopolitical strategy in ways that reshape international economic relationships.

The mineral dependency patterns emerging across advanced economies reveal vulnerabilities that extend far beyond simple supply shortages. Industries requiring precise material specifications for high-performance applications face constraints that cannot be addressed through conventional market mechanisms or strategic reserves alone. These dependencies create cascading effects throughout manufacturing networks and innovation ecosystems.

Strategic Resource Architecture and Economic Control

Modern industrial supremacy increasingly depends on controlling the complete supply chain from raw material extraction through sophisticated processing and refinement. China rare earth dominance demonstrates how nations can leverage geological advantages through systematic investment in processing infrastructure and technological capabilities.

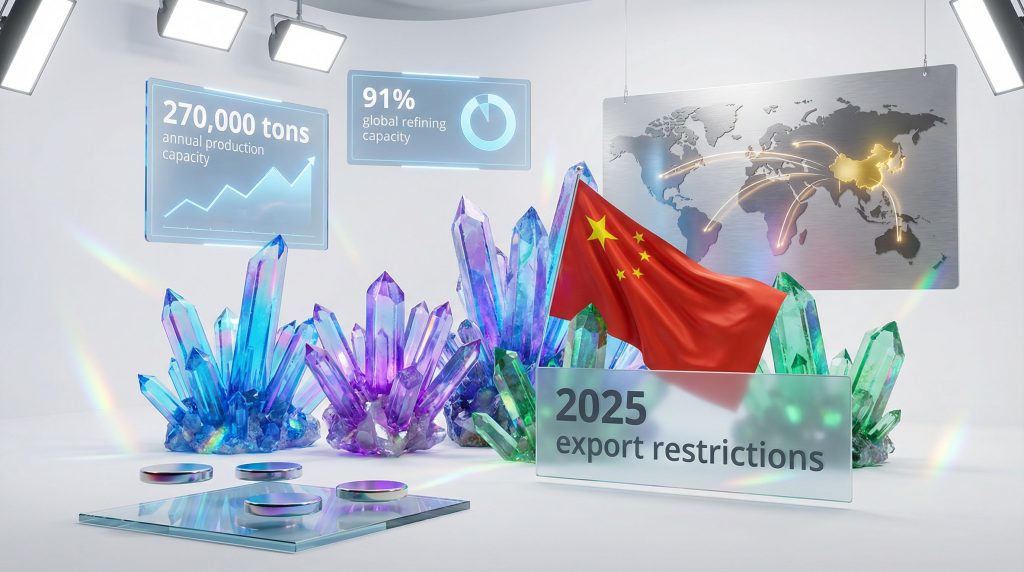

Rare earth elements encompass seventeen chemically similar metals divided into light rare earth elements (LREEs) including cerium, lanthanum, and neodymium, and heavy rare earth elements (HREEs) such as dysprosium, terbium, and yttrium. These materials enable critical functions in permanent magnets, catalysts, phosphors, and advanced alloys essential for contemporary technology.

China currently maintains approximately 70% of global rare earth mining capacity and nearly 90% of processing infrastructure, according to recent industry analysis. This dual dominance in extraction and refinement creates multiple control points throughout the supply chain, enabling both market influence and strategic leverage.

The processing concentration represents a particularly sophisticated form of economic control. While other nations possess rare earth deposits, the complex separation and purification processes require substantial capital investment, environmental management capabilities, and accumulated technical expertise. China's processing facilities in regions like Ganzhou, Jiangxi Province, which serves as a major heavy rare earth production base, demonstrate the scale and specialisation required for commercial viability.

Production Infrastructure and Scale Economics

The rare earth industry exhibits significant economies of scale in both mining and processing operations. Large-scale facilities achieve lower per-unit costs through optimised chemical processes, waste management systems, and integrated supply chains that smaller operations cannot replicate economically.

China's production network spans multiple geological regions, from the Bayan Obo mine in Inner Mongolia to distributed processing facilities across several provinces. This geographic distribution provides operational resilience whilst maintaining centralised technical and logistical coordination.

Processing capabilities require substantial ongoing investment in environmental management, waste treatment, and technological upgrading. The complexity of rare earth separation involves sophisticated chemical processes using organic solvents, ion exchange systems, and precipitation techniques that demand continuous technical refinement and regulatory compliance.

Key production considerations include:

- Ore grade variations affecting processing requirements and cost structures

- Environmental remediation obligations for mining and processing operations

- Technical expertise requirements for complex separation processes

- Infrastructure integration between mining sites and processing facilities

- Quality control standards for end-user applications in electronics and manufacturing

When big ASX news breaks, our subscribers know first

Market Control Mechanisms and Export Strategy

China's rare earth strategy extends beyond production dominance to include sophisticated market control mechanisms that influence global pricing, availability, and industrial planning cycles. Export licensing systems, quota allocations, and processing restrictions create multiple intervention points for economic and diplomatic objectives.

Recent export control measures demonstrate how resource control translates into negotiating leverage in broader economic relationships. Beijing's tightened export restrictions have led to supply disruptions across the United States, European Union, India, and other major economies, forcing dependent industries to adjust production schedules and seek alternative suppliers.

The value-added processing concentration provides additional strategic advantages. Rather than simply exporting raw materials, China focuses on manufacturing finished products like permanent magnets, catalysts, and specialised alloys that command higher profit margins and create deeper dependencies among importing nations.

Price Discovery and Market Manipulation

Trading centres like Baotou in Inner Mongolia serve as global price discovery mechanisms for rare earth markets. The concentration of trading activity, processing capacity, and inventory management in specific geographic locations enables significant influence over international pricing patterns.

Historical precedents demonstrate the effectiveness of export controls as economic tools. During 2010-2012, China implemented export quotas that dramatically increased rare earth prices globally, forcing dependent industries to absorb substantial cost increases whilst alternative suppliers struggled to develop adequate capacity.

Price volatility in rare earth markets reflects both genuine supply-demand imbalances and strategic manipulation possibilities. Neodymium oxide pricing has experienced extreme fluctuations, reaching peaks that reflect market tightness and uncertain availability rather than fundamental production costs.

Market control factors include:

- Licensing delays that create uncertainty in supply planning

- Quota allocations that limit available quantities regardless of demand

- Processing restrictions that force raw material exports to China for refinement

- Strategic stockpiling that removes material from immediate market availability

- Quality standards that favour established suppliers with proven capabilities

Industrial Dependency Patterns and Vulnerability Assessment

Modern manufacturing sectors exhibit varying degrees of rare earth dependency based on technological requirements and substitution possibilities. Electric vehicle production, renewable energy infrastructure, electronics manufacturing, and defence applications each present distinct vulnerability profiles and strategic implications.

The automotive industry's transition toward electrification creates substantial rare earth demand growth, particularly for permanent magnet motors in electric vehicles. This dependency intersects with national climate policies and industrial competitiveness goals, making supply security a strategic priority beyond commercial considerations.

Wind energy installations require significant quantities of rare earth permanent magnets for high-efficiency generators. The intersection of renewable energy targets and critical material dependencies creates policy tensions between environmental objectives and supply chain security concerns.

Electronics and Defence Applications

Consumer electronics rely on rare earth elements for display technologies, battery systems, and miniaturised components that enable portable device functionality. The ubiquity of these applications across telecommunications, computing, and consumer products creates broad economic exposure to supply disruptions.

Defence applications present particular substitution challenges due to performance requirements, reliability standards, and qualification processes that restrict material alternatives. Military systems often require specific rare earth compositions that cannot be easily replaced without extensive redesign and testing procedures.

Industry-specific dependencies:

- Electric vehicles: Permanent magnet motors requiring neodymium and dysprosium

- Wind turbines: High-performance generators using rare earth magnets

- Consumer electronics: Display phosphors and battery materials

- Defence systems: Specialised alloys and precision components

- Telecommunications: Fiber optic amplifiers and signal processing equipment

Processing Bottlenecks and Infrastructure Requirements

The rare earth supply chain demonstrates how mining capacity alone cannot address dependency concerns without corresponding processing infrastructure. Many countries with rare earth deposits lack the technical capabilities and capital investment required for commercial-scale processing operations.

Australia and the United States possess significant rare earth deposits but continue exporting raw materials to China for processing before importing finished products. This circular dependency illustrates the complexity of achieving supply chain independence through mining alone.

Processing infrastructure requires substantial capital investment, estimated in billions of dollars for commercial-scale facilities capable of competing with established Chinese operations. Environmental compliance costs in Western jurisdictions add additional complexity and expense compared to less regulated processing environments.

Technology Transfer and Intellectual Property Barriers

Rare earth processing involves proprietary technologies and accumulated expertise that create barriers to new market entrants. Separation processes, quality control systems, and waste management techniques represent intellectual property that established producers protect strategically.

The transfer of processing technology faces restrictions related to commercial competitiveness and national security considerations. Chinese entities may be reluctant to licence critical processes that would enable competitor facilities in other countries.

Processing challenges include:

- Capital intensity requirements for commercial-scale facilities

- Environmental compliance and waste management costs

- Technical expertise and intellectual property acquisition

- Quality control standards for end-user applications

- Market development for processed products versus raw materials

Competitive Response Strategies and Alternative Supply Development

The United States has unveiled a $12 billion stockpile initiative called Project Vault designed to finance domestic and allied mining and processing capabilities. This response demonstrates recognition that addressing rare earth dependencies requires coordinated investment across multiple countries and supply chain stages.

More than 50 nations, including India, participate in a metallic alliance aimed at securing critical mineral supply chains and reducing reliance on Chinese production. This multilateral approach reflects the scale of investment and cooperation required to develop alternative supply sources.

However, new heavy rare earth suppliers face significant timeline challenges, with most projects not expected to achieve commercial viability until 2027 or later. This extended development timeline creates ongoing vulnerability during the transition period.

Investment Requirements and Economic Viability

Alternative supply chain development requires substantial capital commitment across mining, processing, and manufacturing stages. The economic viability of these investments depends on sustained political support, market demand, and competitive positioning relative to established Chinese suppliers.

Processing facilities in Western countries face higher operating costs due to environmental regulations, labour expenses, and infrastructure requirements. These cost differentials must be offset through premium pricing, government support, or strategic value considerations beyond pure economic returns.

Development considerations:

- Geological exploration and deposit characterisation

- Environmental impact assessment and permitting processes

- Capital raising for mining and processing infrastructure

- Technology acquisition and workforce development

- Market development and customer qualification processes

Future Market Dynamics and Demand Projections

Global rare earth demand continues expanding driven by electrification trends, renewable energy deployment, and advanced manufacturing growth. Electric vehicle production targets, wind energy installations, and electronics proliferation create sustained demand growth that outpaces supply development timelines.

Furthermore, china rare earth dominance may evolve toward maintaining smaller production percentages whilst retaining processing dominance and technological leadership. Projected scenarios suggest China could hold approximately 51% of production capacity by 2030 whilst maintaining 76% of refining capability.

The green energy transition accelerates rare earth consumption across multiple sectors simultaneously. Electric vehicle targets, renewable energy mandates, and energy efficiency requirements create compounding demand pressures that challenge supply development efforts.

Technological Innovation and Substitution Potential

Research initiatives focus on reducing rare earth intensity through improved efficiency, recycling technologies, and alternative materials development. Magnet recycling capabilities could address portion of demand growth whilst reducing primary mining requirements.

However, substitution possibilities remain limited for many critical applications due to performance requirements and technical constraints. Alternative materials often involve trade-offs in efficiency, reliability, or cost that limit practical adoption.

Innovation pathways include:

- Magnet recycling and urban mining technologies

- Alternative material research for specific applications

- Efficiency improvements reducing per-unit rare earth requirements

- Circular economy models for critical material recovery

- Advanced processing techniques improving yield and reducing waste

The next major ASX story will hit our subscribers first

Risk Assessment and Economic Resilience Planning

Supply disruption scenarios reveal cascading vulnerabilities across manufacturing sectors and national economies. The concentration of processing capabilities creates single points of failure that could affect multiple industries simultaneously during geopolitical tensions or trade disputes.

Manufacturing sector vulnerabilities vary by country based on industrial composition and import dependencies. Countries with substantial automotive, electronics, or renewable energy industries face greater exposure to rare earth supply disruptions than those with different economic structures.

Defence industry dependencies present national security implications beyond commercial considerations. Military systems requiring specific rare earth materials may face operational constraints during extended supply disruptions.

What Are the Main Scenario Planning and Contingency Strategies?

Economic resilience planning requires multiple scenario assessment including gradual supply tightening, sudden export restrictions, and complete supply cutoffs. Each scenario demands different response strategies and resource allocation priorities.

In addition, critical minerals strategic reserve optimisation involves balancing inventory costs against supply security benefits. Stockpiling decisions must consider material degradation, technological obsolescence, and opportunity costs of capital allocation.

Risk mitigation approaches:

- Strategic reserve sizing and composition optimisation

- Bilateral supply agreements with multiple suppliers

- Industrial policy coordination among allied economies

- Demand reduction through efficiency and substitution initiatives

- Emergency allocation protocols for critical applications

Investment Opportunities and Market Evolution

Rare earth supply chain development creates investment opportunities across mining, processing, technology development, and recycling sectors. However, these investments involve substantial capital requirements, long development timelines, and regulatory uncertainties that affect risk-return profiles.

Emerging rare earth projects outside China face market development challenges including customer qualification, competitive positioning, and financing constraints. Success requires coordination between government support, private investment, and end-user commitment to alternative suppliers.

Processing technology development represents a particular investment opportunity due to the bottleneck nature of refining capabilities. Companies developing efficient, environmentally compliant processing technologies could capture significant value across multiple geographic markets.

Regulatory Framework Evolution and Trade Policy

Critical mineral designation policies affect investment flows, tax treatment, and strategic priority allocation across developed economies. These regulatory frameworks continue evolving as governments recognise the economic and security implications of mineral dependencies.

Export control reciprocity creates potential for escalating trade tensions as countries implement restrictions on strategic materials and technologies. This dynamic affects investment planning and market development strategies for all participants.

Investment considerations include:

- Project development timelines and capital intensity

- Regulatory environment and government support levels

- Market development and customer base establishment

- Competitive positioning relative to established suppliers

- Technology acquisition and intellectual property development

How Will Trade Wars Impact Supply Chain Development?

The us-china trade war impact on rare earth supply chains continues creating uncertainty for manufacturers and investors. Tariff policies and export restrictions force companies to reassess sourcing strategies whilst governments develop strategic responses to mineral dependencies.

Consequently, mining industry innovation accelerates as companies seek technological solutions to reduce rare earth consumption or develop alternative materials. This innovation drive represents both necessity and opportunity for businesses operating in mineral-dependent sectors.

According to expert analysis, china rare earth dominance will likely persist through the current decade despite international diversification efforts. The combination of processing expertise, infrastructure investment, and market control mechanisms provides substantial advantages that alternative suppliers will require years to replicate effectively.

Understanding these dynamics helps investors, policymakers, and industry participants navigate the complex intersection of resource security, economic competition, and technological development in critical material markets.

Investment in alternative supply chains requires sustained commitment across political cycles and market conditions to achieve meaningful supply diversification.

This analysis is based on publicly available information and industry reports. Investors should conduct independent research and consider professional advice before making investment decisions related to critical materials or rare earth supply chains.

What Opportunities Await in the Next Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications about significant ASX mineral discoveries, including critical minerals breakthroughs that could reshape supply chains. Explore how historic discoveries generate substantial market returns and begin your 14-day free trial today to position yourself ahead of emerging opportunities in this rapidly evolving sector.