June 3, 2026

Understanding the Strategic Importance of Critical Minerals in Modern Supply Networks

The global economy operates on an intricate web of mineral dependencies that most decision-makers barely comprehend until disruption strikes. Unlike conventional commodities, critical minerals form the invisible backbone of technological civilisation, powering everything from renewable energy infrastructure to defence systems. When these supply networks face interruption, the cascading effects ripple through entire industrial sectors within weeks, not months.

Critical minerals encompass a carefully curated list of non-fuel materials deemed essential for economic and national security. The U.S. Geological Survey expanded its critical minerals designation from 35 materials in 2018 to 50 minerals by 2022, whilst the European Commission now tracks 34 critical raw materials as of 2023. This expansion reflects growing recognition of vulnerability rather than scarcity, as most critical minerals exist in adequate geological quantities but face severe processing bottlenecks.

The renewable energy transition amplifies these dependencies exponentially. Battery storage alone requires lithium, cobalt, and nickel demand to grow 40-fold by 2040 according to International Energy Agency projections for net-zero scenarios. A single smartphone contains over 60 different elements, whilst advanced semiconductors depend on gallium, germanium, and rare earth elements with no viable commercial substitutes.

Processing concentration creates the most severe vulnerabilities in global supply disruption minerals scenarios. While lithium mining spans Australia, Chile, and Argentina, 60% of global processing capacity concentrates in Chinese facilities. This processing-mining gap represents the critical chokepoint that transforms localised disruptions into global industrial crises.

When big ASX news breaks, our subscribers know first

Geographic Dependencies and Systemic Concentration Risks

China's dominance extends far beyond mining operations into the strategic control of refining infrastructure. The nation processes 90% of global rare earth elements, 80% of tungsten, 75% of gallium, 70% of graphite, and 95% of magnesium. This vertical integration creates dual leverage points: raw material access and processing capacity control.

Recent export restrictions demonstrate how processing monopolies translate into geopolitical weapons. Chinese graphite export quotas dropped 35% in 2023, whilst new restrictions target gallium, antimony, and rare earth compounds essential for defence applications. These moves extend beyond trade disputes into strategic positioning for extended supply chain control.

The distinction between raw materials and processed derivatives proves crucial during crisis scenarios. Raw ore typically contains only 0.5-2% mineral content and requires energy-intensive processing consuming 2,000-15,000 kWh per ton depending on the specific mineral. Converting concentrate (15-40% mineral content) to industry-ready refined compounds (99%+ purity) represents 70-90% of total supply chain costs and requires specialised facilities with 4-8 week commissioning periods.

Processing bottlenecks extend supply disruption timelines by 6-18 months compared to mining interruptions alone. Unlike oil refineries that can restart relatively quickly, mineral processing facilities require complex chemical rebalancing and quality control protocols that cannot be accelerated during emergencies.

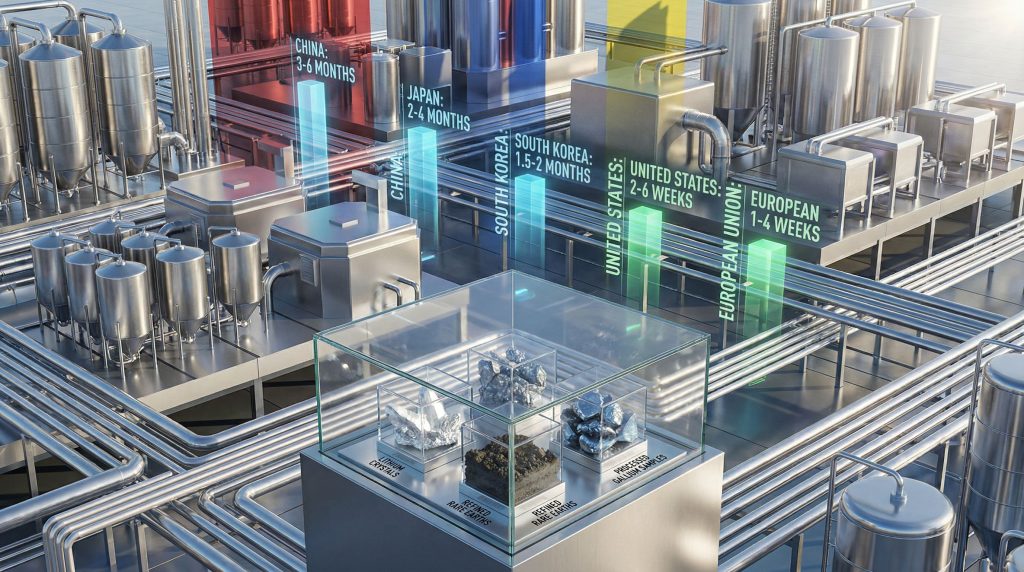

Strategic Reserve Capacity Across Major Economies

National stockpile capabilities vary dramatically in both duration and strategic focus. Analysis of publicly available data reveals striking disparities in emergency preparedness across major economies:

| Region | Coverage Duration | Strategic Focus | Release Timeline |

|---|---|---|---|

| China | 3-6 months | Domestic demand priority | Government controlled |

| Japan | 2-4 months | Post-2010 crisis response | 2-3 week deployment |

| South Korea | 1.5-2 months | Rapid industrial support | 72-hour emergency release |

| United States | 2-6 weeks | Defence applications | Variable by material |

| European Union | 1-4 weeks | Fragmented coordination | Under development |

| Australia | Variable | Producer-ally model | Bilateral agreements |

China maintains the most comprehensive strategic advantage through state-controlled reserves estimated at 5-12 months of domestic demand for rare earth elements, though precise figures remain classified. The State Reserves Bureau manages these stockpiles with political rather than economic optimisation, enabling domestic manufacturing prioritisation during supply constraints.

Japan's post-2010 rare earth crisis framework represents the most sophisticated import-dependent model. Chinese export quota restrictions in 2010 caused dysprosium prices to spike 800% and terbium 1,000% within twelve months, triggering ¥20 billion in emergency stockpile investments. Current Japanese reserves provide 2-4 months coverage for critical defence and energy minerals through hybrid government-industry coordination.

Furthermore, South Korea prioritises rapid deployment over extended duration, maintaining reserves designed for 72-hour emergency release compared to Japan's 2-3 week timeline. This approach reflects the nation's semiconductor and battery manufacturing concentration, where production delays multiply exponentially with each passing day.

Western Vulnerability Factors Beyond Reserve Size

The United States faces unique structural challenges despite possessing the world's largest military stockpile. The National Defense Stockpile contains approximately $7.2 billion in strategic materials but focuses primarily on defence-grade specifications rather than civilian industrial requirements. This defence-civilian gap means U.S. strategic reserves might sustain weeks of military demand whilst providing only days of coverage for broader manufacturing, renewable energy, and electronics sectors.

Historical depletion compounds current vulnerabilities. The NDS experienced significant drawdowns during 2001-2020 without systematic replenishment, leaving critical gaps in materials essential for clean energy infrastructure. Recent efforts to rebuild select stockpiles face congressional funding constraints and private sector coordination challenges.

European economies confront coordination difficulties that fragment response capacity. A comprehensive critical minerals strategy attempts to establish coordinated stockpiling mechanisms, but implementation timelines extend into 2026-2027 whilst current vulnerabilities persist. Individual member state reserves operate under different management frameworks, complicating emergency allocation during simultaneous demand spikes.

Regional distribution infrastructure creates additional bottlenecks during crisis scenarios. Stockpiled materials concentrated in specific geographic locations face transportation constraints when multiple industries simultaneously require emergency supplies. Unlike petroleum strategic reserves with established pipeline distribution networks, critical mineral stockpiles depend on trucking and rail networks that can saturate quickly.

Material Form and Emergency Deployment Challenges

Stockpile effectiveness depends critically on material form and industrial readiness rather than simple tonnage calculations. Emergency scenarios reveal three distinct categories of stored materials:

- Raw ore form: Requires 4-16 weeks processing before industrial use; suitable only for extended disruptions

- Concentrate form: Intermediate processing stage; 2-8 weeks to final products; requires specialised refining capacity

- Refined compounds: Industry-ready materials; immediate deployment possible; highest storage costs and degradation risks

Quality specifications further complicate emergency utilisation. Defence applications require 99.9%+ purity levels for rare earth magnets in guidance systems, whilst civilian electronics accept 99%+ specifications. Strategic reserves optimised for military requirements may prove unusable for broader economic sectors without additional processing steps.

Demand prioritisation protocols determine actual availability during multi-sector emergencies. Government rationing frameworks typically prioritise defence contractors, critical infrastructure operators, and essential manufacturing over consumer electronics, automotive, and construction sectors. This hierarchy can exhaust stockpiles faster than duration estimates suggest when calculated against total economic demand.

Critical Assessment: Most national stockpile duration estimates assume single-sector demand rather than economy-wide disruptions affecting defence, energy, manufacturing, and technology sectors simultaneously.

Export Restrictions and Weaponised Supply Chain Control

Geopolitical tensions increasingly manifest through strategic mineral export controls that extend beyond traditional trade disputes. China's 2010 rare earth export restrictions provided a blueprint for using processing monopolies as diplomatic leverage, causing ¥2-3 trillion in economic losses across Japanese manufacturing sectors.

Recent restrictions demonstrate escalating sophistication in supply chain weaponisation. An executive order on minerals may further complicate global trade dynamics. Chinese controls now target specific product grades rather than broad material categories, allowing continued civilian exports whilst restricting defence and high-technology applications.

Secondary market dynamics amplify restriction impacts through speculative price volatility. Antimony prices increased 300% within six months of Chinese export licensing requirements, whilst gallium spot markets experienced 500%+ premium spikes for immediate delivery contracts. These price shocks cascade through dependent industries regardless of actual supply availability.

Consequently, retaliatory restriction cycles create compound vulnerabilities as importing nations implement their own export controls on downstream products. Technology transfer restrictions accompanying mineral export limits prevent recipient nations from developing independent processing capabilities, perpetuating long-term dependencies.

How Long Would Critical Minerals Last in a Supply Shock?

According to recent analysis of supply shock scenarios, most Western economies would face severe shortages within 2-8 weeks of complete supply disruption. The International Energy Agency warns that export controls on critical minerals have transformed supply concentration risks from theoretical concerns into immediate realities.

The next major ASX story will hit our subscribers first

Investment Implications and Sector Transformation

Mining sector valuations increasingly reflect supply security premiums rather than purely cost-based metrics. Operations with geographically diversified processing partnerships command 15-25% valuation premiums over single-country exposure projects, whilst companies with government partnership agreements in strategic mineral development access preferential financing terms.

Technology sector adaptation strategies focus on supply chain resilience investments that reduce single-source dependencies. Mineral substitution research programmes target $50-100 billion annual investment globally by 2030, whilst recycling technology advancement receives comparable funding from both government and private sources.

Infrastructure investment requirements for supply security extend far beyond traditional mining development. Processing facility construction in consumer markets requires $200-500 million per facility depending on mineral complexity, whilst transportation network resilience improvements demand coordinated public-private investment frameworks.

In addition, circular economy models gain strategic rather than purely environmental importance as recycling technologies reduce primary supply dependencies. Advanced battery recycling can recover 95%+ of lithium, nickel, and cobalt from end-of-life electric vehicle batteries, though current facilities process less than 5% of available material volumes.

Building Long-Term Mineral Security Through Diversification

Effective supply security requires multi-dimensional approaches extending beyond strategic stockpiling into comprehensive risk management frameworks. Diversification strategies must address geographic, technological, and temporal vulnerabilities simultaneously whilst maintaining economic competitiveness.

Regional processing hub development offers the most sustainable path toward reduced single-country dependencies. Allied nation partnerships in mineral processing capacity create distributed resilience whilst sharing infrastructure development costs. Australian rare earth processing facilities serving Japanese and South Korean markets exemplify this collaborative approach.

Moreover, the broader implications of US-China trade impacts on global mineral markets necessitate careful strategic planning. European raw materials supply initiatives demonstrate how regional blocs can develop independent processing capabilities.

Substitution technology development provides long-term independence from specific mineral dependencies. Research into alternative battery chemistries, magnetic materials, and electronic components progresses rapidly under government funding programmes, though commercial deployment typically requires 7-15 years from laboratory demonstration to industrial scale.

International cooperation mechanisms need standardisation to enable effective resource sharing during emergencies. Joint strategic reserve development projects and coordinated response protocols require treaty-level agreements rather than informal arrangements to ensure reliability during geopolitical tensions.

Policy Framework Requirements for Enhanced Resilience

Regulatory incentives must balance supply security objectives with economic efficiency to avoid creating uncompetitive domestic industries. Strategic mineral classification systems require regular updating to reflect evolving technological dependencies and emerging vulnerabilities rather than static historical assessments.

Emergency powers for resource allocation need clear legal frameworks established during peacetime to enable rapid deployment without constitutional challenges. Private sector coordination protocols require advance agreement on government authority during crisis scenarios whilst protecting proprietary information and competitive positions.

Long-term industrial policy coordination across government agencies prevents contradictory objectives between trade, defence, energy, and environmental regulators. Whole-of-government approaches to mineral security enable consistent policy signals that support private sector investment in resilience infrastructure.

Strategic Resilience in an Interconnected Global Economy

Most advanced economies face uncomfortable realities regarding their ability to withstand complete global supply disruption minerals scenarios. Coverage periods measured in weeks rather than months expose fundamental vulnerabilities in industrial systems designed for just-in-time efficiency rather than crisis resilience.

The strategic advantage of comprehensive mineral security extends beyond immediate crisis response into long-term competitive positioning. Nations with reliable access to critical materials can maintain industrial production, support allied partners, and leverage supply stability for diplomatic influence during global uncertainties.

Investment priorities must shift from pure cost optimisation toward balanced consideration of supply security, environmental sustainability, and geopolitical independence. This transformation requires patient capital deployment in processing infrastructure, technology development, and international cooperation mechanisms that may not generate immediate financial returns but provide essential strategic insurance.

Building effective mineral security demands coordinated responses across government, industry, and international partners rather than purely national approaches to inherently global supply chains. The interconnected nature of modern industrial systems requires collaborative solutions that strengthen collective resilience whilst maintaining competitive market dynamics.

Disclaimer: This analysis incorporates publicly available government data, industry estimates, and published research. Strategic reserve information remains classified in many jurisdictions, limiting precision in coverage calculations. Investment implications discussed are for informational purposes and do not constitute financial advice.

Ready to Position Yourself for the Next Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities in critical minerals and emerging commodities ahead of broader market recognition. Explore how major mineral discoveries can generate substantial returns and begin your 14-day free trial today to secure your competitive advantage in this strategically vital sector.