June 5, 2026

The Quiet Erosion of Dollar Dominance and What It Means for Gold

Monetary systems rarely collapse overnight. They erode. The transition from one reserve currency architecture to another typically unfolds across decades, punctuated by geopolitical shocks, policy failures, and the slow accumulation of structural imbalances that eventually become impossible to ignore. Today, the global monetary order built at Bretton Woods in 1944 is showing precisely these fracture lines, and the relationship between de-dollarization and gold prices is emerging as one of the most consequential investment themes of the coming decade.

Understanding this dynamic requires moving beyond the daily fluctuations in the gold spot price and examining the deeper forces reshaping how sovereign nations store and protect national wealth. Furthermore, gold in the global monetary system has taken on renewed strategic importance as governments reassess the risks embedded in dollar dependency.

When big ASX news breaks, our subscribers know first

Why Central Banks Are Rethinking Reserve Composition

The dollar's position as the world's dominant reserve currency was not simply a product of American economic strength. It was engineered through a series of interlocking mechanisms: the petrodollar recycling system that tied energy trade to dollar denomination, the global dependence on SWIFT for cross-border transactions, and the unrivalled depth and liquidity of U.S. Treasury markets. For decades, these mechanisms reinforced each other, making the dollar the path of least resistance for governments managing national reserves.

That architecture is now under measurable strain. According to analysis cited by Deutsche Bank researchers, the dollar's share of global central bank foreign exchange reserves has declined from approximately 60% to roughly 40% in recent years. Simultaneously, gold's share of global reserves has approximately doubled over the past four years, reaching an estimated 30%. These are not trivial shifts. They represent a multi-trillion-dollar reallocation of sovereign capital away from dollar-denominated instruments.

The assets nations are moving toward carry no counterparty risk and cannot be frozen, sanctioned, or devalued by any single government's policy decision. The world losing trust in the US dollar is no longer a fringe thesis — it is increasingly reflected in measurable reserve allocation data.

The 2022 freezing of Russian sovereign dollar reserves following the invasion of Ukraine is widely regarded as a watershed moment in this process. It demonstrated, in real time, that dollar-denominated assets held by foreign governments are subject to the geopolitical priorities of Washington. For reserve managers in countries that consider themselves potentially vulnerable to future sanctions, this created an entirely new category of risk, one that had previously been treated as theoretical.

Gold, by contrast, exists outside any nation's legal jurisdiction. It cannot be frozen, cancelled, or restructured. This characteristic, long appreciated in theory, suddenly became operationally urgent.

The Scale of Sovereign Gold Accumulation Since 2008

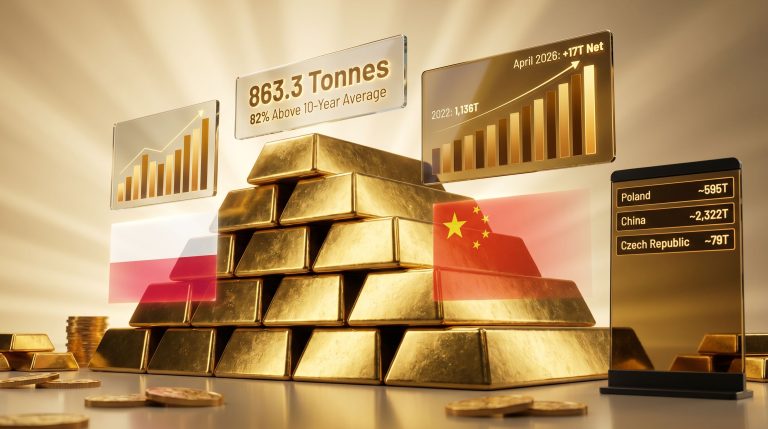

The shift toward gold in official reserves did not begin with the Ukraine conflict. According to Deutsche Bank research, emerging market central banks have collectively purchased approximately 225 million ounces of gold since the 2008 financial crisis. The pace of accumulation accelerated meaningfully after 2022, but the underlying trend of sovereign gold buying predates the geopolitical trigger by well over a decade.

This matters because it suggests the demand driver is structural rather than reactive. Central bank gold reserves are being expanded as part of long-term reserve diversification strategies that reflect concerns about currency debasement, dollar weaponisation risk, and the desire for monetary sovereignty that cannot be undermined by another nation's fiscal or foreign policy decisions.

Reserve Share Rotation: A Structural Shift in Numbers

| Reserve Asset | Approximate Share ~2015 | Approximate Share ~2026 (Est.) |

|---|---|---|

| U.S. Dollar | ~65% | ~40% |

| Gold | ~10-12% | ~30% |

| Other Currencies (EUR, CNY, etc.) | ~25% | ~30% |

Source: Deutsche Bank research; institutional reserve data estimates. Past composition and projections involve estimation and should not be treated as definitive figures.

What makes this rotation particularly significant from a price perspective is that central bank gold demand does not behave like speculative investor demand. Sovereign buyers are not momentum traders. They do not sell when prices rise or panic when prices fall. Their accumulation is driven by strategic allocation decisions made over years, which means the demand base underpinning gold prices is more durable and less price-sensitive than conventional financial flows.

Deutsche Bank analysts have modelled the price sensitivity of this demand, estimating that for every additional 1 million ounces of gold purchased by central banks, the gold price rises approximately 1%. At current accumulation rates, this creates a persistent and self-reinforcing upward pressure on prices that operates independently of the retail and institutional investor flows that drive shorter-term market movements.

Gold Price Scenarios Under Different De-Dollarization Pathways

The relationship between de-dollarization and gold prices plays out differently depending on how quickly and deeply reserve reallocation unfolds. Institutional analysts have framed this through a scenario-based approach that helps investors assess the range of plausible outcomes. For a broader perspective, Investopedia's analysis of de-dollarisation and gold prices offers useful additional context on how these dynamics are interpreted across financial markets.

Scenario 1: Gradual Diversification (Base Case)

- Dollar share stabilises around 38-42% of global reserves

- Central bank gold buying remains elevated but does not accelerate dramatically

- Gold price supported in the $2,800-$3,500 range through structural demand

- This scenario assumes no major new geopolitical shocks and continued but measured reserve reallocation

Scenario 2: Accelerated Rebalancing (Bull Case)

- Geopolitical fragmentation deepens; major economies reduce dollar exposure more aggressively

- Emerging market central banks push gold holdings toward 40% of reserves

- Deutsche Bank analysis projects gold could reach $5,000-$8,000 per ounce over a five-year horizon under this scenario

- Total emerging market foreign exchange reserves are assumed to decline to approximately $5 trillion in this modelling

Scenario 3: Dollar Stabilisation (Bear Case)

- U.S. fiscal consolidation restores dollar credibility

- Federal Reserve tightening pushes real interest rates sharply positive

- Geopolitical tensions ease, reducing the premium on politically neutral assets

- Gold corrects toward $2,000-$2,400 as the structural case for reserve diversification weakens

"The $8,000 per ounce scenario does not require a dollar collapse or an end to the reserve currency system. Deutsche Bank analysts have stressed that this outcome would require only the continuation of the current directional trend in reserve reallocation over a multi-year period. Projections of this kind are inherently speculative and dependent on multiple macroeconomic assumptions holding simultaneously. They should not be treated as forecasts."

Monetary Expansion: The Inflation Signal Markets Are Underweighting

The de-dollarization narrative for gold is reinforced by a parallel development in domestic monetary conditions. According to Federal Reserve data, the U.S. M2 money supply grew from approximately $21.61 trillion in February 2025 to $22.67 trillion in February 2026, a year-on-year expansion of 4.9%. An additional $57 billion was added to M2 in March 2026 alone.

A critical distinction that investors often overlook is the difference between CPI as a symptom and monetary expansion as the underlying cause. Classical monetary theory, rooted in the quantity theory of money, holds that sustained increases in the money supply eventually translate into higher prices across the economy. The CPI reading is the visible consequence of a process that begins with credit creation and balance sheet expansion.

CPI and Inflation Indicators: April 2026 Snapshot

| Inflation Indicator | Latest Reading |

|---|---|

| Headline CPI (Month-over-Month) | +0.6% |

| Headline CPI (Annual) | 3.8% (highest since May 2023) |

| Core CPI (Annual) | 2.8% |

| Core CPI Annualized (Monthly Pace) | ~4.8% |

| Energy Index (Monthly) | +3.8% |

| Gasoline (Monthly / Annual) | +5.4% / +28.4% |

| Food Prices (Monthly) | +0.5% |

| Shelter Costs (Monthly) | +0.6% |

| Producer Price Index (Monthly) | +1.0%+ |

| Core PPI (Monthly) | +0.6% |

Source: U.S. Bureau of Labor Statistics, April 2026 CPI release.

The annualised pace of monthly core CPI is running at approximately 4.8%, nearly two and a half times the Federal Reserve's stated 2% target. Producer prices, which function as a leading indicator for future consumer inflation, rose more than 1% in a single month, suggesting that pipeline pressures are not abating. Electricity costs have reportedly climbed roughly 50% over the past five years, implying an annual average increase of approximately 10%, a figure that diverges substantially from headline CPI methodology.

There is also a legitimate debate about whether CPI methodology accurately captures the inflation that households actually experience. Formula changes implemented during the 1990s altered the way the index is calculated, and some analysts argue that using the older methodology would produce headline inflation readings closer to 6-7% rather than the official 3.8%. This is a contested claim that warrants scrutiny, but it reflects a genuine tension between statistical measurement and lived economic experience — a tension visible in data showing that 65% of Americans identified rising costs and affordability as their primary financial concern in a recent Gallup survey.

The Fiscal-Monetary Trap and Its Implications for Gold

One of the most structurally important and least widely understood dynamics in the current environment is the bind facing the Federal Reserve. With U.S. federal debt-to-GDP exceeding 100%, the interest rate required to genuinely suppress inflation creates a fiscal problem of its own. Higher rates increase the government's debt servicing burden on an already stretched balance sheet, creating political pressure to keep rates lower than inflation dynamics would otherwise justify.

This tension creates what some analysts describe as fiscal dominance — a condition in which monetary policy becomes constrained by the government's financing needs rather than operating independently to achieve price stability. In this environment, real interest rates, which are the most historically reliable short-to-medium-term driver of gold prices, are likely to remain structurally lower than a purely inflation-fighting policy would produce.

Allegations have also circulated that the Federal Reserve quietly resumed Treasury purchases in December 2025, effectively expanding its balance sheet again regardless of the official framing applied to these operations. If accurate, this would represent a return to the kind of monetary accommodation that historically correlates with periods of gold price appreciation.

The next major ASX story will hit our subscribers first

Why De-Dollarization Is Not the Whole Story for Gold

It is important for investors to understand that de-dollarization and gold prices are linked through a multi-factor system, not a single causal chain. Gold's price at any given moment reflects the net balance of several competing forces:

- Real Interest Rates — The most historically reliable short-to-medium-term driver; negative or falling real rates create a strong tailwind for gold

- U.S. Dollar Strength (DXY) — An inverse relationship that operates across most market cycles; dollar weakness typically amplifies gold's upside

- Inflation Expectations — Both realised inflation readings and forward breakeven rates influence gold's safe-haven premium

- Central Bank Demand — Structural, strategic, and increasingly dominant; less price-sensitive than speculative flows and therefore more durable

- Investor Risk Appetite — Flight-to-safety dynamics during equity market stress or geopolitical escalation create episodic demand spikes

- De-Dollarization Momentum — A long-duration, slow-moving structural force that primarily transmits into gold prices through sovereign reserve allocation decisions

It is also worth noting that Federal Reserve research has cautioned against a simplistic interpretation of central bank gold purchases. Sovereign buying does not always correspond to a direct reduction in dollar holdings. In many cases, it reflects broader diversification across multiple currencies simultaneously, with gold added as a complement rather than a pure dollar substitute. The distinction matters for modelling the precise transmission mechanism between de-dollarization and gold prices.

Practical Considerations for Investors

For investors evaluating gold exposure in the context of de-dollarisation, several practical considerations are worth examining. In addition, understanding gold as a safe haven helps frame why these allocation decisions carry such long-term strategic weight.

- Portfolio diversification value: Gold has historically demonstrated low correlation to equities and investment-grade bonds, providing genuine risk reduction in a multi-asset portfolio rather than simply speculative upside

- Physical vs. paper gold: Physical gold eliminates counterparty risk entirely, which is particularly relevant given that the core thesis for gold in a de-dollarising world is precisely the value of assets that sit outside any institutional dependency. ETFs and futures offer liquidity but reintroduce the counterparty dimension

- Time horizon alignment: The de-dollarisation thesis operates on a multi-year to multi-decade timeframe. Investors focused on this structural narrative typically take a long-duration view and treat short-term price volatility as noise rather than signal

- Silver as a complementary consideration: Silver shares gold's monetary metal characteristics but also carries significant industrial demand exposure, particularly in renewable energy infrastructure. This creates a different risk-return profile that some investors use to complement core gold positions

- Purchasing power context: Even at official inflation rates, fiat currency purchasing power erodes meaningfully over multi-decade periods. Gold's finite supply — it cannot be created by monetary policy — positions it as a structural hedge against this erosion regardless of the de-dollarisation scenario

Consequently, a research overview on de-dollarisation's macroeconomic implications further supports the case that these structural forces are gaining momentum across the global economy.

"Investors should be aware that all projections discussed in this article, including gold price scenarios, are speculative and forward-looking in nature. They involve assumptions about geopolitical developments, central bank behaviour, inflation dynamics, and monetary policy that may not materialise as anticipated. Nothing in this article constitutes financial advice. Past performance of any asset class is not indicative of future results."

Key Takeaways: The Structural Investment Case in a Multipolar World

The structural case connecting de-dollarization and gold prices rests on a convergence of factors that individually would be meaningful and collectively represent a potentially historic shift in global capital allocation. The following points summarise the core framework:

- The dollar's share of global central bank reserves has declined materially from approximately 60% to 40%, while gold's share has roughly doubled to an estimated 30%

- Emerging market central banks have purchased approximately 225 million ounces of gold since 2008, with the pace of accumulation accelerating after 2022

- Deutsche Bank research estimates that every additional 1 million ounces of central bank gold purchases drives approximately a 1% increase in the gold price

- Under an accelerated de-dollarisation scenario where emerging market central banks increase gold to 40% of reserves, institutional projections place gold at $5,000-$8,000 per ounce over five years, though these are speculative scenarios rather than forecasts

- The annualised pace of core CPI is running at approximately 4.8%, nearly two and a half times the Fed's 2% target, while M2 expanded by 4.9% year-on-year to February 2026

- The geopolitical weaponisation of dollar reserves has permanently altered the risk calculus for sovereign reserve managers in ways that are unlikely to reverse regardless of short-term diplomatic developments

- De-dollarisation is a structural tailwind for gold, not a binary trigger. It operates across years and decades, reinforcing central bank demand that is strategically driven and inherently less price-sensitive than speculative investor flows

The convergence of monetary expansion, fiscal constraints, geopolitical multipolarity, and sovereign reserve reallocation creates a macro environment in which gold's role as a politically neutral, counterparty-free monetary asset becomes more strategically relevant with each passing year — not less.

Want to Stay Ahead of the Next Major ASX Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into actionable insights — including gold, which sits at the centre of one of the most consequential monetary shifts in decades. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.