June 23, 2026

The Invisible Architecture Behind Every Mining Investment Decision

Before a single metre of ground is broken, before equipment is ordered or workers are hired, the fate of a mining project is often determined by a document most retail investors never read. Economic feasibility studies sit at the intersection of geology, engineering, finance, and market analysis, functioning as the formal mechanism through which speculative mineral discoveries are transformed into investable assets. Understanding how these studies work, what they measure, and where they fail is arguably more valuable to anyone with exposure to the mining sector than any individual project update.

The mining industry operates within one of the longest capital commitment cycles of any sector. From initial discovery to first production, timelines routinely span ten to twenty years. Within that arc, economic feasibility studies are not a single event but a structured sequence of increasingly rigorous financial evaluations, each designed to reduce uncertainty before the next tranche of capital is deployed.

When big ASX news breaks, our subscribers know first

Why Rigorous Pre-Investment Evaluation Is Non-Negotiable

The Financial Stakes of Skipping Structured Analysis

Mining project failures rarely arrive without warning. Post-mortem analysis of high-profile project collapses consistently reveals the same pattern: optimistic assumptions were embedded early, never stress-tested adequately, and compounded through successive funding rounds until the gap between modelled and actual economics became unbridgeable.

The financial consequences are not abstract. When large-scale mining projects overrun their capital budgets, overruns frequently reach 25% to 50% above original estimates, according to historical industry data tracked across major project developments. These are not rounding errors. At a project with a projected capital cost of USD $1 billion, a 30% overrun translates to a $300 million shortfall that either dilutes equity holders significantly or collapses project financing entirely.

Feasibility Studies as the Financial Gatekeeper

The function of an economic feasibility study is often misunderstood. It is not primarily a forecasting exercise, although forecasting is embedded within it. Its deeper purpose is risk elimination before capital commitment. Every assumption that gets quantified, tested, and challenged within the study framework is an assumption that cannot blindside a project's financiers mid-construction.

An economic feasibility study is not simply a financial forecast. It is a structured risk-reduction instrument designed to prevent capital misallocation before a single dollar of construction funding is deployed.

The Strategic Gap Between Exploration Optimism and Bankable Economics

Exploration-stage companies operate in a world of possibilities. Their announcements describe drill intersections, inferred resources, and geological potential. Feasibility studies exist in a fundamentally different register: one governed by engineering costs, long-term commodity price curves, and lender requirements. Bridging these two worlds requires transforming geological data into economic certainty, and that transformation is precisely what the feasibility process is designed to achieve.

What Economic Feasibility Studies Actually Measure

Core Purpose: From Concept Validation to Capital Decision

At its foundation, an economic feasibility study answers a deceptively simple question: given everything we know about this project, does it create more value than it consumes? The analysis required to answer that question credibly is anything but simple.

A comprehensive study integrates capital cost estimation, operating cost modelling, commodity price forecasting, metallurgical recovery assumptions, infrastructure requirements, environmental compliance costs, and financing structure into a single integrated financial model. The outputs of that model, particularly Net Present Value (NPV), Internal Rate of Return (IRR), and payback period, then become the basis for investment decisions involving hundreds of millions or billions of dollars.

How Economic Analysis Differs From Technical and Environmental Assessments

It is important to distinguish economic feasibility studies from the broader suite of evaluations that mining projects undergo. A technical feasibility study determines whether a deposit can physically be mined using available methods. An environmental impact assessment identifies ecological risks and permitting obligations. A market feasibility study evaluates whether demand and pricing conditions support commercial sales. The economic feasibility study synthesises outputs from all of these into a unified investment viability verdict.

The TELOS Framework: Locating Economic Analysis Within the Broader Picture

Project evaluation methodology often references the TELOS framework, which assesses viability across five dimensions:

- Technical feasibility: can it be built and operated?

- Economic feasibility: does the financial case stack up?

- Legal feasibility: are all regulatory and permitting requirements achievable?

- Operational feasibility: can the organisation execute the project?

- Scheduling feasibility: can milestones be achieved within required timeframes?

Economic feasibility analysis is one node within this broader system, but it is typically the most decisive. A project can be technically achievable and legally permittable yet still be unfundable if the economic case does not meet investor thresholds.

The Three Foundational Pillars of Any Economic Feasibility Study

Pillar 1: Capital and Operating Cost Architecture

The cost architecture of a mining project divides into two distinct categories, each with different risk profiles and modelling challenges.

Capital expenditure (CAPEX) covers all upfront investment required to bring the mine into production: plant and equipment procurement, site construction, tailings facility design, access road development, power supply infrastructure, and permitting costs. In underground projects, shaft sinking and development headings represent major CAPEX line items that are notoriously difficult to estimate with precision.

Operating expenditure (OPEX) covers the ongoing costs of running the mine once production has commenced: labour, reagents, energy, maintenance, haulage, and royalties. OPEX estimates must reflect the full life of mine, including periods when ore grades decline and processing becomes more energy-intensive.

A critically underappreciated aspect of cost architecture is sustaining capital, the ongoing investment required to maintain production capacity after commissioning. Early-stage financial models frequently focus entirely on initial CAPEX while underweighting sustaining capital requirements, which can be substantial in long-life operations.

Contingency budgeting deserves particular attention. Industry convention generally applies contingency allowances of 10% to 15% on CAPEX at the definitive feasibility study stage, rising to 20% to 30% at pre-feasibility level, reflecting the greater uncertainty in earlier-stage cost estimation. Furthermore, understanding cut-off grade economics at this stage is essential, as the minimum economic grade assumptions directly influence OPEX modelling and life-of-mine projections.

Pillar 2: Revenue Projection and Profit Modelling

Revenue modelling in mining is complicated by several factors that do not affect most other industries. Commodity prices are determined by global supply and demand dynamics that no single project operator can influence. Grade variability across the ore body means that production rates and product quality will fluctuate over the mine life. Recoveries in the processing plant may differ from metallurgical testwork results, particularly during ramp-up.

Best-practice feasibility studies model revenue across multiple commodity price scenarios and explicitly disclose the price assumptions underlying each scenario. A project that only generates positive NPV under optimistic price assumptions should be treated very differently from one that remains NPV-positive at conservative long-term consensus pricing.

By-product credits represent another frequently misunderstood revenue element. Many base metal deposits contain secondary metals that generate meaningful revenue offsets against operating costs. Copper-gold projects, for example, may credit gold and silver revenues against copper OPEX, materially improving the apparent all-in cost structure. Understanding how by-product credits are applied, and how sensitive they are to price assumptions, is essential to interpreting published feasibility economics.

Pillar 3: Risk Identification and Funding Pathway Analysis

The third pillar moves beyond numbers to interrogate the structural risks that could prevent modelled economics from being realised. These risks cluster across three domains:

- Market risk: commodity price cycles, demand destruction scenarios, and customer concentration risk where offtake is concentrated among few buyers.

- Regulatory and permitting risk: jurisdictional complexity, indigenous consultation requirements, environmental approval timelines, and the risk that permitting conditions impose unanticipated capital costs.

- Financing risk: the ability to raise sufficient capital on acceptable terms, the feasibility of debt structures given project risk profile, and the availability of strategic or offtake partners willing to support project financing.

In addition, management red flags in how a project team communicates risk assumptions can signal deeper structural problems within the organisation's approach to capital discipline.

The Five Core Components of a Well-Structured Study

Component 1: Market and Demand Analysis

Understanding the market into which a project will sell its product is foundational to any revenue model. This involves analysing current and projected supply-demand balances, identifying where the project's production would sit within the global cost curve, and assessing the contractual structures available for offtake.

For battery metals such as lithium, cobalt, and nickel, long-dated demand projections have become particularly contested terrain. Analysts applying different electric vehicle adoption curves and battery chemistry assumptions can reach materially divergent conclusions about future demand, which feeds directly into project NPV calculations through the revenue modelling framework.

Component 2: Technical and Engineering Assessment

The engineering component of a feasibility study translates the geological model into a mining and processing plan. Key decisions include mining method selection (open pit versus underground, bulk versus selective mining), processing route design, and infrastructure configuration.

One dimension that receives insufficient attention in investor-facing materials is metallurgical complexity. A deposit with excellent grade but difficult metallurgy may require more complex processing, higher reagent consumption, or lower overall recovery rates than a lower-grade but more amenable ore body. Metallurgical testwork results are among the most critical inputs to feasibility economics and among the most frequently glossed over in project communications.

Component 3: Financial Modelling and Metrics Framework

The financial model is the analytical core of the study. It integrates cost inputs, production schedules, price assumptions, and financing costs into a time-series cash flow model, then applies discounting techniques to arrive at the headline NPV and IRR metrics.

| Metric | Definition | Why It Matters |

|---|---|---|

| Net Present Value (NPV) | Present value of future cash flows minus initial investment | Primary viability indicator; positive NPV confirms value creation |

| Internal Rate of Return (IRR) | Discount rate at which NPV equals zero | Benchmarked against cost of capital; higher IRR signals stronger returns |

| Break-Even Point | Production level or price at which revenues equal total costs | Defines the floor for economic operation |

| Payback Period | Time required to recover initial capital investment | Critical for investor risk appetite and financing terms |

| CAPEX Intensity | Capital cost per unit of annual production capacity | Comparative efficiency metric across project types |

The discount rate applied to the cash flow model is one of the most consequential and least debated assumptions in published feasibility studies. Most mining feasibility studies apply discount rates of 5% to 8% in real terms, but this choice dramatically influences the resulting NPV. A project with a life-of-mine NPV of $500 million at a 5% discount rate may show an NPV below $200 million at 10%, which could determine whether institutional lenders are willing to participate in project financing.

Component 4: Sensitivity and Scenario Analysis

No financial model produces a single correct answer. Sensitivity analysis quantifies how much the key output metrics change when individual input assumptions are varied, identifying which variables pose the greatest risk to project economics.

Standard sensitivity variables include:

- Commodity price movement (typically modelled at plus or minus 10% to 20%)

- Ore grade variance relative to resource model assumptions

- Processing recovery rates versus metallurgical testwork

- Capital cost overruns at various percentage levels

- Operating cost inflation above base-case assumptions

More sophisticated feasibility work applies Monte Carlo simulation, which runs thousands of iterations across probability distributions for each key variable simultaneously. This produces a probability distribution of possible NPV outcomes rather than a single-point estimate, giving decision-makers a clearer picture of the range of outcomes and the likelihood of achieving the base-case economics. Indeed, interpreting drill results correctly at the exploration stage feeds directly into the quality of grade assumptions underpinning these sensitivity models.

Component 5: Cost-Benefit Analysis and Investment Justification

The final component synthesises the financial analysis into a decision framework that addresses the needs of multiple stakeholders simultaneously. For boards and institutional investors, the focus is on return metrics and risk-adjusted returns. For lenders, the emphasis falls on cash flow coverage ratios and downside protection. For regulators and community groups, the relevant outputs are employment, tax revenue, and economic development contributions.

Furthermore, cost-benefit analysis frameworks applied across the full project lifecycle allow decision-makers to weigh total economic impact rather than focusing exclusively on headline NPV figures.

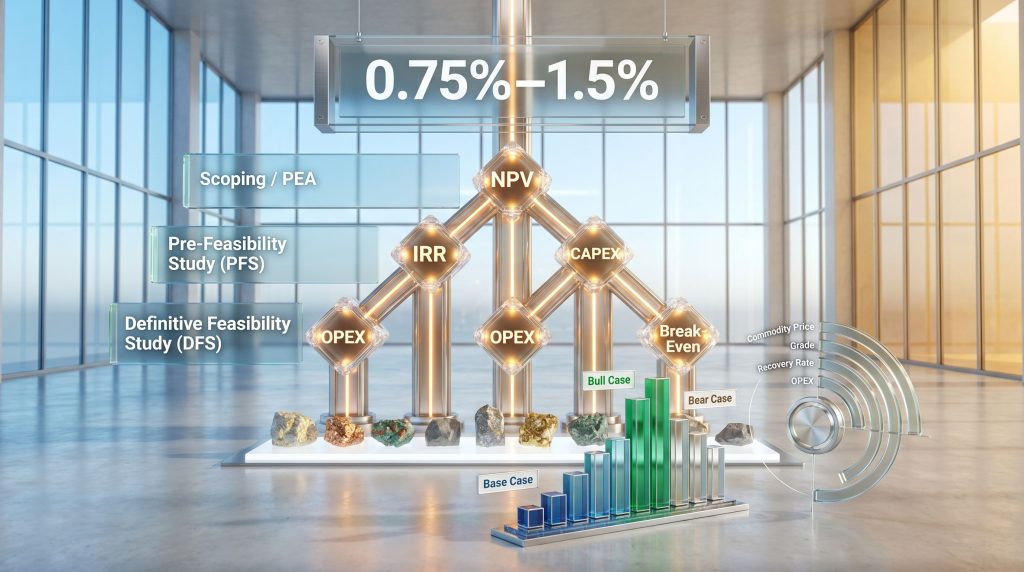

Understanding Study Costs and the 0.75% to 1.5% Rule

One of the most practically useful conventions in mining project finance is the relationship between feasibility study cost and total projected project capital. Industry practice positions study expenditure at between 0.75% and 1.5% of total project CAPEX for a definitive feasibility study. On a $500 million project, that implies study costs of $3.75 million to $7.5 million.

| Study Type | Accuracy Range | Typical Cost as % of Project CAPEX | Primary Use Case |

|---|---|---|---|

| Scoping / PEA | ±35-50% | 0.1-0.3% | Early-stage concept screening |

| Pre-Feasibility Study (PFS) | ±20-25% | 0.3-0.75% | Project advancement and resource conversion |

| Definitive Feasibility Study (DFS) | ±10-15% | 0.75-1.5% | Financing, board approval, and construction decision |

The progression across study types reflects a deliberate capital efficiency logic. Early-stage studies consume minimal capital while screening out uneconomic projects before significant funds are committed. Later-stage studies require substantially more investment in engineering, metallurgical testwork, and infrastructure assessment, but they also underwrite the financing decisions that involve orders of magnitude more capital. Spending 1% of a project's capital cost to confirm the viability of the other 99% represents one of the highest-return investments available in the project development process.

The next major ASX story will hit our subscribers first

The Five Most Common Analytical Failures in Mining Feasibility Studies

Understanding where feasibility studies go wrong is as important as understanding what they are designed to achieve.

Mistake 1: Optimism Bias in Performance Assumptions

The most pervasive analytical failure in mining feasibility studies is the systematic application of best-case assumptions across multiple input variables simultaneously. When laboratory-scale metallurgical recoveries are applied to commercial-scale operations without ramp-up discounting, when production schedules assume continuous equipment availability that real operations never achieve, and when grade assumptions reflect resource model averages rather than mining dilution realities, the compounding effect on financial outputs can be substantial.

Mistake 2: Treating Cost Inputs as Fixed Rather Than Probabilistic

Single-point cost estimates are inherently misleading in long-duration capital projects. Input costs for labour, energy, and consumables evolve over multi-year construction and operational periods. Feasibility studies that fail to model inflationary pressures on CAPEX during extended construction timelines have consistently underestimated project costs, particularly in high-inflation periods.

Mistake 3: Relying on Outdated or Peer-Substituted Data

Using stale commodity price benchmarks or engineering cost data from superseded databases creates systematic bias in cost estimation. Equally problematic is the practice of substituting cost data from peer projects in different jurisdictions without adjusting for labour market conditions, regulatory requirements, infrastructure availability, and geological differences. A processing cost derived from a Chilean open-pit copper operation is not a reliable benchmark for an underground Canadian gold project.

Mistake 4: CAPEX-Only Focus That Neglects Lifecycle Operating Costs

Projects with attractively low upfront capital requirements can appear deceptively economic if sustaining capital and long-term OPEX are inadequately modelled. This is particularly relevant in underground operations where ore body access deteriorates over time and development costs escalate, and in processing-intensive operations where reagent consumption increases as ore grades decline.

Mistake 5: Excluding Policy, Regulatory, and Carbon Cost Variables

Long-dated project economics are increasingly exposed to regulatory cost variables that were not historically incorporated into feasibility models. Carbon pricing mechanisms, royalty regime changes, and environmental compliance cost escalation can materially affect project economics across twenty-year mine lives. Feasibility studies that omit these variables produce optimistic financial projections that may not survive contact with the regulatory environment in which projects actually operate.

Projects that advance to construction without addressing these five analytical gaps face significantly elevated risk of cost overruns, financing failure, and operational underperformance.

From Mineral Resource to Bankable Economics: The Development Pathway

Understanding how economic feasibility studies fit within the broader project development sequence helps investors interpret corporate announcements and milestone achievements more accurately.

- Mineral Resource Estimate (MRE): establishes the geological foundation and quantifies the in-situ resource across inferred, indicated, and measured confidence categories.

- Preliminary Economic Assessment (PEA/Scoping Study): screens project economics at a high level with accuracy of ±35% to ±50%, using conceptual engineering assumptions and long-term consensus price forecasts.

- Pre-Feasibility Study (PFS): refines assumptions, advances resource classification from inferred to indicated and measured, and delivers accuracy of approximately ±20% to ±25%.

- Definitive Feasibility Study (DFS): delivers bankable project economics with accuracy of ±10% to ±15%, sufficient to support financing applications and formal board approval for construction.

Each stage gate involves a go/no-go decision. Projects with marginal economics at the PFS stage frequently enter optimisation loops, revisiting pit design, processing route selection, production scheduling, and infrastructure configuration to identify whether design modifications can improve the financial case before committing to DFS expenditure. For context, definitive feasibility studies represent the most capital-intensive and rigorous phase of project evaluation, requiring fully engineered designs and validated cost data before lenders will commit to project financing.

It is also worth noting that drilling programs conducted between PFS and DFS stages are commonly used to upgrade inferred resources to higher confidence categories, directly strengthening the geological assumptions upon which bankable economics are built.

How Feasibility Study Quality Determines the Cost of Project Capital

The relationship between feasibility study quality and financing cost is direct and quantifiable. Lenders and institutional equity investors price perceived risk into their required returns. A project supported by a rigorous, independently verified definitive feasibility study with robust sensitivity analysis commands a lower risk premium than a project advancing on the basis of a preliminary economic assessment with wide accuracy bands.

This risk premium differential manifests as a lower Weighted Average Cost of Capital (WACC), which in turn increases the project's NPV at any given set of operating assumptions. The implication is that investment in study quality and independent review is not merely a regulatory or governance requirement: it is a direct lever on project value.

A high-quality definitive feasibility study does not merely confirm project economics. It materially reduces the perceived risk premium demanded by lenders and equity investors, directly lowering a project's weighted average cost of capital.

How Economic Feasibility Studies Compare to Other Project Evaluations

| Study Type | Primary Focus | Key Output | Decision Supported |

|---|---|---|---|

| Economic Feasibility Study | Financial viability and investment returns | NPV, IRR, payback period | Go/no-go capital decision |

| Technical Feasibility Study | Engineering and operational practicality | Process design, throughput capacity | Construction methodology |

| Market Feasibility Study | Demand, pricing, and competitive positioning | Revenue assumptions, market share | Commercial strategy |

| Environmental Impact Assessment | Ecological and social risk | Permitting conditions, mitigation plans | Regulatory approval |

| Operational Feasibility Study | Workforce, logistics, and execution capability | Staffing models, supply chain design | Operational readiness |

Frequently Asked Questions About Economic Feasibility Studies

What is the difference between a pre-feasibility study and a definitive feasibility study?

A pre-feasibility study operates at a higher level of engineering abstraction, with cost accuracy of approximately ±20% to ±25% and a greater reliance on conceptual design assumptions. A definitive feasibility study requires detailed engineering, committed vendor quotes for major equipment, and validated metallurgical testwork to achieve the ±10% to ±15% accuracy range required for financing decisions.

How long does it typically take to complete an economic feasibility study?

Pre-feasibility studies for mid-sized projects typically require twelve to eighteen months. Definitive feasibility studies for projects of similar scale commonly take eighteen to thirty-six months, depending on the complexity of the deposit, infrastructure requirements, and the volume of metallurgical testwork needed.

What commodity price assumptions should feasibility studies use?

Industry practice varies, but most credible feasibility studies apply long-term consensus commodity price forecasts derived from investment bank surveys, typically representing a conservative mid-cycle price rather than spot prices. Studies that use near-term spot prices during commodity bull markets systematically overstate project economics.

Can a project with a negative NPV still proceed to development?

In limited circumstances, yes. Strategic rationale, such as maintaining supply chain security, utilising existing infrastructure, or processing ore that extends the life of an adjacent operation, can justify development decisions that standard NPV analysis would not support. However, these decisions require explicit acknowledgement that economic value creation under standard criteria has not been demonstrated.

What role does sensitivity analysis play in a feasibility study?

Sensitivity analysis identifies which input variables most significantly affect project economics, allowing decision-makers to focus risk management attention on the highest-impact assumptions. It also provides a framework for evaluating how much commodity price decline or cost escalation a project can absorb before becoming uneconomic.

How do environmental and social factors affect economic feasibility outcomes?

Environmental and social factors increasingly affect feasibility economics through multiple pathways: permitting costs and timelines, rehabilitation and closure obligations, community benefit agreements, and the growing exposure to carbon pricing mechanisms. Feasibility studies that treat these factors as qualitative considerations rather than quantified cost inputs produce less reliable economic projections.

Key Takeaways for Investors and Project Teams

- A rigorous economic feasibility study integrates financial modelling, technical validation, market analysis, and risk quantification into a single decision-support framework, and should never be treated as a marketing document.

- The three non-negotiable outputs are a defensible NPV calculated at a disclosed and justifiable discount rate, a benchmarked IRR that demonstrates adequate returns above the cost of capital, and a clearly defined break-even threshold that reveals downside resilience.

- Study credibility depends on the quality of underlying data, the independence of the study team, and the robustness of sensitivity testing across all major input variables.

- Feasibility study expenditure of 0.75% to 1.5% of total project cost represents one of the highest-return investments in the project development cycle given the capital it protects.

- The five most common analytical failures, optimism bias, fixed-cost assumptions, poor data sourcing, CAPEX-only focus, and policy cost blindness, are all preventable with disciplined methodology and independent review.

Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to invest in any mining project or company. All forward-looking statements, financial projections, and scenario analyses discussed herein involve inherent uncertainty. Readers should conduct their own due diligence and consult qualified financial and technical advisors before making investment decisions.

Want to Know Which ASX Mining Projects Have the Economics to Back Them Up?

Discovery Alert's proprietary Discovery IQ model cuts through the complexity of mineral project announcements, delivering real-time alerts the moment significant ASX discoveries are made — turning dense technical data into actionable investment intelligence. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market when the next significant discovery is announced.