June 23, 2026

The Infrastructure Behind the Minerals: How State Capital Is Reshaping Canada's Resource Future

The global race to secure critical minerals supply chains is no longer driven by commodity markets alone. Increasingly, it is being shaped by the calculated deployment of state-backed financing institutions, which are stepping into the early-stage risk gap that commercial lenders have long refused to fill. Understanding how this institutional architecture works, and what it means for Canada's resource sector, is essential context for anyone tracking the future of battery metals, rare earths, and industrial minerals.

Export Development Canada (EDC), the federal Crown corporation mandated to support Canadian exporters, has positioned itself as a central actor in this evolving landscape. Its growing role in EDC support for critical minerals reflects not just a policy preference, but a structural transformation in how public capital is being weaponised to accelerate domestic production capacity.

When big ASX news breaks, our subscribers know first

EDC's Mandate Evolution: From Trade Finance to Industrial Strategy

EDC was originally conceived as a relatively straightforward trade finance institution, providing insurance and lending products to help Canadian companies export goods and services. That founding logic, while still intact, has been substantially expanded. The agency has shifted toward what can best be described as a proactive industrial policy posture, using its balance sheet to intervene at stages of the mining development cycle that conventional finance typically avoids.

This distinction matters enormously. Traditional project finance operates on the principle of bankable feasibility, meaning capital flows only once a project has demonstrated sufficient technical and economic maturity to satisfy lender risk thresholds. EDC's new model deliberately inverts this logic by absorbing pre-construction and even pre-feasibility risk, with the explicit goal of compressing development timelines and accelerating Canada's supply chain capacity.

The policy framework underpinning this evolution is Canada's Critical Minerals Strategy, which identifies specific mineral categories as strategically essential to both the clean energy transition and critical minerals energy security. EDC's expanded mandate is the operational expression of that strategy, translating federal priorities into capital flows.

The Numbers Behind the Push

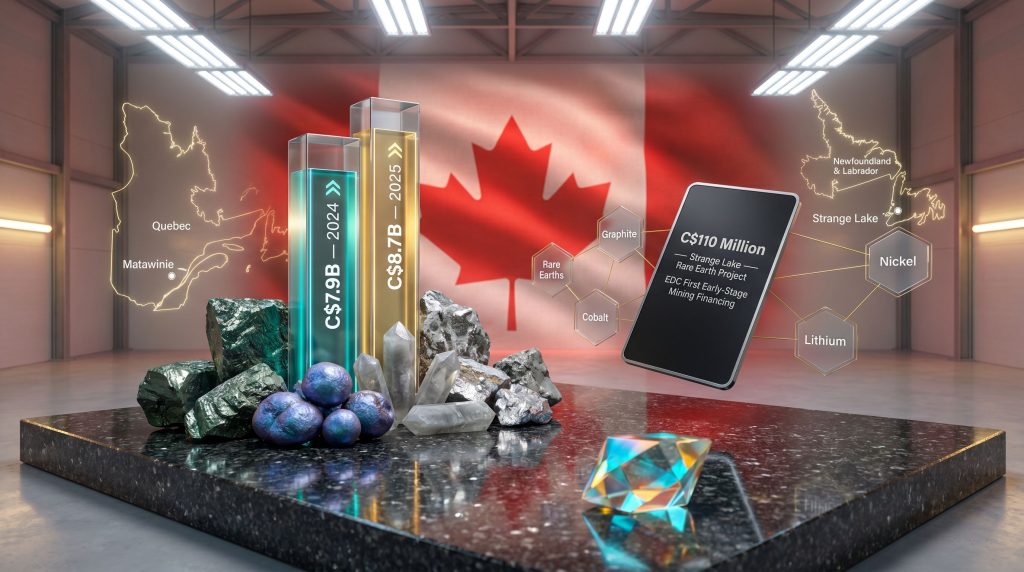

The scale of EDC's commitment to critical minerals is significant and growing. In 2025, EDC facilitated approximately C$8.7 billion in support across Canada's critical minerals sector, up from C$7.9 billion in 2024. That represents roughly a 10% year-over-year increase in institutional capital deployment within a single fiscal year, a pace that reflects genuine strategic urgency rather than incremental programme adjustment.

EDC's president and CEO has been explicit that the agency is deliberately taking on more risk and supporting projects in fundamentally new ways, including earlier-stage and pre-construction financing, to accelerate transformative developments for Canada. Furthermore, the institution has articulated a parallel goal of exporting Canadian mining expertise internationally, creating trade opportunities for domestic mining suppliers in strategic global projects.

These are not modest ambitions. They represent a redefinition of what a federal export credit agency does in a world where access to critical minerals has become a dimension of geopolitical competition. For a deeper look at the battery metals investment landscape, the structural forces at play extend well beyond any single institution.

Why the Timing Is Not Accidental

The acceleration of EDC support for critical minerals does not occur in a vacuum. Several structural forces have converged to create both the necessity and the political will for this kind of institutional intervention.

Supply chain concentration risk is perhaps the most acute driver. China currently dominates not only rare earth mining but, more critically, the processing and refining stages that transform raw ore into usable industrial inputs. For graphite specifically, China accounts for the overwhelming majority of global battery-grade supply, a dependency that has become politically untenable for Western governments designing EV and grid storage supply chains.

The mineral intensity of the clean energy transition compounds this pressure. Consider what a single electric vehicle requires compared to its internal combustion equivalent:

- An average EV battery pack contains approximately 8 kg of lithium, 35 kg of nickel, 20 kg of manganese, and 14 kg of cobalt

- Offshore wind turbines require up to 4 tonnes of copper per megawatt of generating capacity

- Grid-scale battery storage deployments demand substantial quantities of graphite for anode materials, with natural graphite remaining the dominant anode feedstock globally despite synthetic alternatives

The critical minerals demand picture is stark. The International Energy Agency has projected that demand for critical minerals could increase by three to six times current levels by 2040 under aggressive energy transition scenarios. Mine development timelines, which typically span 10 to 15 years from discovery to first production, mean that financing decisions made today determine whether supply can meet demand a decade from now.

The U.S. Inflation Reduction Act introduced a further dimension by creating powerful domestic incentives for North American mineral supply chains. While this generated competitive pressure on Canadian producers, it simultaneously opened opportunities for Canadian projects to qualify as allied-nation suppliers under content and sourcing rules, provided they can reach production within relevant timelines.

Landmark Transactions: What EDC's New Model Looks Like in Practice

The Torngat Metals Bridge Loan: A Template for Pre-Construction Financing

The most structurally significant transaction in EDC's evolving critical minerals portfolio is its financing commitment to Torngat Metals for the Strange Lake rare earth project, spanning Quebec and Newfoundland and Labrador. This deal was notable as EDC's first early-stage mining financing transaction, a deliberate signal that the institution's risk appetite has materially changed.

| Metric | Detail |

|---|---|

| Project | Strange Lake Rare Earth Project |

| Location | Quebec and Newfoundland & Labrador |

| EDC Financing | C$110 million bridge financing loan |

| Co-financing Partner | Canada Infrastructure Bank (C$55 million) |

| Transaction Significance | EDC's first early-stage mining financing deal |

| Development Stage | Pre-construction |

Strange Lake hosts one of North America's largest rare earth deposits, with mineralisation that includes heavy rare earth elements (HREEs), which are considered more strategically sensitive than light rare earths because they are used in the permanent magnets critical to EV motors and wind turbine generators. Heavy rare earth supply is dominated even more narrowly by Chinese production than the broader rare earth category, making projects like Strange Lake geopolitically significant well beyond their economic metrics.

The pairing of EDC's C$110 million commitment with the Canada Infrastructure Bank's C$55 million contribution establishes a blended public finance model that effectively creates a new category of project financing. By combining two federal institutions with complementary mandates, this structure reduces the equity dilution burden on the project developer while signalling to subsequent private lenders that the project has passed institutional due diligence.

The Matawinie Graphite Mine: Canada's Clean Energy Flagship

The Matawinie mine, developed by Nouveau Monde Graphite (NMG) in Quebec, represents the most visible expression of Canada's ambition to become a major non-Chinese source of battery-grade graphite. Recognised as Canada's largest graphite project and described in federal communications as a G7-scale development, Matawinie's construction commencement in 2026 has been widely framed as a landmark moment.

What makes Matawinie strategically distinctive is not simply its scale but its intended position in the value chain. NMG's stated development trajectory aims to produce not just mining-grade flake graphite but purified spherical graphite suitable for direct use as battery anode material. This distinction is critical: the value differential between raw graphite concentrate and battery-ready anode material is substantial, and the processing knowledge required to close that gap is currently concentrated in China.

A fully integrated Canadian graphite operation, from mine through to anode-grade product, would represent a genuine supply chain capability that Western battery manufacturers currently cannot source outside China. EDC's involvement in supporting Matawinie's development is consequently not simply a mining investment; it is an investment in value chain diversification at a stage where the processing premium is highest.

Canada's Comparative Advantage and the Financing Gap

Canada's geological endowment across critical mineral categories is well-established. The country hosts significant reserves of lithium, graphite, cobalt, nickel, copper, uranium, and rare earth elements. Quebec's lithium belt, the Ring of Fire in Ontario, the rare earth deposits of Labrador and Quebec, and the graphite occurrences across multiple provinces collectively constitute a resource base that few other allied nations can match in breadth.

However, geological endowment is a necessary but insufficient condition for supply chain leadership. The critical constraint is financing, specifically the willingness of capital to flow into the pre-production stages where risk is highest and potential returns are most distant.

This is precisely the gap EDC is attempting to bridge. The agency's willingness to absorb pre-construction risk functions as a de-risking catalyst: once federal capital is committed at an early stage, the project's risk profile shifts sufficiently to attract subsequent private and institutional capital that would not have moved without that initial signal.

The next major ASX story will hit our subscribers first

How EDC Compares to Allied-Nation Export Credit Agencies

Canada is not alone in deploying state-backed capital for critical minerals, but the specific model EDC is adopting has distinctive features worth examining in comparative context.

| Country / Agency | Financing Instrument | Focus Area | Notable Feature |

|---|---|---|---|

| Canada (EDC) | Bridge loans, pre-construction financing | Full value chain, graphite, rare earths | Early-stage risk capital; ECA partnerships with Japan and Korea |

| United States (DOE / DFC) | Loan guarantees, direct loans | Domestic processing, rare earth independence | IRA-aligned domestic supply chain incentives |

| Japan (JBIC / NEXI) | Equity participation, concessional loans | Battery metals, rare earths in allied nations | Long-term offtake-linked financing structures |

| Australia (EFA) | Export finance, guarantees | Critical minerals processing, downstream value-add | Focus on processing capacity to reduce raw ore exports |

| European Union (EIB) | Strategic project designation, blended finance | Battery metals, lithium, cobalt | Critical Raw Materials Act alignment |

Japan's model is particularly instructive. Japanese export credit institutions have historically taken equity positions in strategic mining projects, linking financing to long-term offtake agreements that guarantee mineral supply to Japanese industrial consumers. In addition, EDC's memoranda of understanding with Japanese and Korean export credit agencies suggest Canada is seeking to build complementary relationships with institutions that operate downstream.

This ensures Canadian minerals reach end-use markets in allied nations rather than being redirected through Chinese processing intermediaries. Meanwhile, the approach to European critical raw materials offers another instructive parallel, as the value-add differential between mined concentrate and refined intermediate products is where the most durable economic benefit accumulates.

The Risks That Cannot Be Ignored

Any serious analysis of EDC's expanded critical minerals mandate must engage with the risks that this strategic pivot introduces.

Pre-construction financing risk is the most structurally significant. The historical attrition rate of mining projects from exploration to production is severe: industry data consistently shows that fewer than 1 in 1,000 mineral exploration projects ever reach commercial production. Even projects that advance to pre-feasibility stages face substantial probability of failure from geological disappointment, permitting delays, commodity price collapse, or capital market withdrawal.

When a federal Crown corporation deploys public capital at the pre-construction stage, it is absorbing risks that commercial lenders have explicitly priced out of their portfolios. The governance frameworks, staged disbursement structures, and co-financing arrangements that surround these transactions are not administrative formalities but essential safeguards against material public capital loss.

Commodity price volatility presents a second category of risk with particular relevance to the current moment. Lithium prices experienced a dramatic collapse between 2022 and 2024, falling by more than 80% from peak levels as Chinese production capacity expanded faster than EV demand materialised. Graphite prices have similarly been under pressure from Chinese supply dominance.

Indigenous rights and social licence constitute a third dimension of risk that is particularly acute in the Canadian context. Many of the most significant critical mineral deposits in Canada are located within or adjacent to Indigenous territories, and the legal framework governing free, prior, and informed consent has evolved substantially. EDC's own environmental and social risk frameworks, which reference the Equator Principles and IFC Performance Standards, are designed to manage this exposure, but implementation requires genuine engagement rather than procedural compliance.

Trade Diversification as a Strategic Objective

EDC's critical minerals financing strategy cannot be fully understood without situating it within Canada's broader trade diversification ambition. Federal support for critical mineral projects has articulated an explicit goal of doubling non-U.S. exports, a target that reflects the structural vulnerability exposed by periods of trade tension with Canada's largest trading partner.

Critical minerals represent one of the highest-value pathways to building new bilateral trade relationships, because the minerals Canada holds are precisely what allied industrial economies in Asia and Europe need to execute their own energy transitions. Japanese battery manufacturers, Korean EV producers, and European automotive suppliers are all seeking secure, non-Chinese sources of graphite, lithium, and rare earth materials.

Canada's minister of international trade has stated that delivering world-class critical minerals to the global stage is essential to diversifying trading relationships and achieving the country's non-U.S. export growth targets. The framing explicitly connects mineral supply to economic sovereignty, positioning Canada's resource endowment as a geopolitical asset to be actively managed rather than passively exported.

The Processing Gap: Canada's Most Significant Strategic Vulnerability

Perhaps the least discussed but most consequential challenge facing Canada's critical minerals ambitions is not in the ground but in the processing facilities that do not yet exist at scale. Mining a critical mineral and transforming it into a form usable by battery manufacturers or magnet producers are fundamentally different industrial operations requiring different capital, expertise, and chemical process knowledge.

Canada currently exports the overwhelming majority of its mined mineral production as concentrate or intermediate product, with final processing occurring elsewhere, frequently in China. The economic implications are stark: the value of battery-grade lithium carbonate is multiples higher than spodumene concentrate; the value of separated rare earth oxides vastly exceeds mixed mineral concentrate; purified spherical graphite commands a premium over run-of-mine flake.

Building processing and refining capacity is therefore the next frontier for EDC support for critical minerals policy, and it is an area where EDC's expanded mandate will face its most complex financing challenges. Processing facilities require different risk assessment frameworks than mining operations, involving chemical engineering complexity, offtake agreement structures, and environmental permitting dimensions that are materially distinct from conventional project finance.

Key Takeaways for Investors and Industry Observers

- EDC's critical minerals financing grew from C$7.9 billion in 2024 to C$8.7 billion in 2025, a ~10% increase that signals sustained institutional commitment

- The Torngat Metals C$110 million bridge loan establishes a replicable template for blended pre-construction public finance

- Matawinie represents Canada's most advanced attempt to capture the processing premium on graphite, targeting battery-ready anode material rather than raw concentrate

- EDC's bilateral ECA partnerships with Japan and Korea are designed to connect Canadian supply with Asian demand in a structure that bypasses Chinese processing intermediaries

- The processing and refining capacity gap remains Canada's most significant structural vulnerability, and future EDC financing programmes will need to engage this challenge directly

- Commodity price cycles and Indigenous consent frameworks represent the two highest-probability risk factors for pre-construction financing programmes

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. References to forecasts, financing scenarios, and commodity demand projections involve inherent uncertainty and should not be relied upon as predictive of actual outcomes. Readers should conduct their own due diligence before making any investment decisions.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex mineral data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.