June 12, 2026

Understanding Global Critical Mineral Supply Chain Vulnerabilities

Global supply chain dependencies in critical minerals create profound vulnerabilities that extend far beyond individual commodity markets. When examining rare earth elements specifically, the concentration of processing capabilities in single geographic regions represents both an opportunity for emerging producers and a strategic risk for consuming nations. The Egypt China rare earth partnership exemplifies this dynamic, where developing economies leverage untapped mineral resources to establish new geopolitical partnerships and economic development pathways.

The intersection of resource geology, processing technology, and international finance creates complex scenarios where traditional Western development models compete against integrated state-led approaches. Furthermore, understanding these patterns requires examining specific cases where resource-rich nations navigate between technological sovereignty and partnership dependencies while considering the broader implications of the critical minerals strategy 2025.

When big ASX news breaks, our subscribers know first

What Drives Egypt's Strategic Pivot to Chinese Rare Earth Partnerships?

Economic Diversification Beyond Traditional Revenue Streams

Egypt's economic transformation strategy extends significantly beyond its historical reliance on Suez Canal revenues and tourism income. Current economic data reveals the limitations of these traditional pillars: Suez Canal revenues generate approximately $7 billion annually as of 2023, representing roughly 2% of total government revenue according to Suez Canal Authority reporting. In addition, tourism sector contribution peaked at 12% of GDP pre-pandemic, with ongoing recovery efforts still underway.

The nation's Vision 2030 development framework explicitly identifies critical minerals as a strategic diversification pillar, targeting an increase in manufacturing sector contribution from 16% to 20% of GDP by 2030. This represents a deliberate pivot toward value-added industrial development rather than continued dependence on service sector revenues and commodity transit fees.

Egypt's real GDP growth averaged 3.6% annually from 2020-2023, with IMF projections of 4.2% for 2024-2025. However, achieving sustainable growth above 5% requires industrial base expansion that current economic structures cannot support without significant capital investment and technology transfer aligned with the global energy transition in critical minerals.

Regional comparative analysis demonstrates the potential scale of mineral-based economic transformation. Morocco's phosphate industry generates substantial foreign exchange through its 43 million metric tons annual production, making it the world's largest phosphate reserves holder and exporter. Consequently, Egypt's strategy appears designed to replicate this success model using rare earth elements rather than phosphates as the primary value driver.

Geopolitical Positioning in Global Supply Chain Restructuring

The timing of Egypt's rare earth partnership initiatives reflects sophisticated geopolitical positioning during a period of US-China trade tensions and global supply chain restructuring. Egypt's geographic location provides strategic advantages as a mineral logistics hub connecting African extraction sites, Asian processing centers, and European consumer markets through existing Red Sea and Mediterranean shipping infrastructure.

Current analysis suggests Egypt is pursuing a geopolitical hedging strategy, positioning itself as an alternative rare earth supplier outside traditional Western-aligned frameworks. This approach leverages the reality that Western development financing mechanisms often require governance and environmental conditions that extend project timelines significantly compared to integrated state-led partnerships, particularly as nations implement policies like the US critical minerals policy.

The Red Sea corridor via the Suez Canal creates natural infrastructure alignment for rare earth ore movement to Chinese refineries or alternative international processing facilities. This geographic advantage reduces transportation costs and enables flexible market access compared to landlocked African mineral regions that require complex logistics chains to reach international markets.

Regional competition dynamics add urgency to Egypt's initiative. Algeria possesses documented rare earth potential but lacks commercial-scale operations, while Morocco's established phosphate infrastructure provides competitive advantages in related mineral processing. Therefore, Egypt's window of opportunity depends partly on establishing first-mover advantages in North African rare earth development before neighbouring countries develop competing capabilities.

How Significant Are Egypt's Untapped Rare Earth Resources?

Golden Triangle Region: Geological Assessment and Potential

The Golden Triangle region spans approximately 9,000 square kilometers across southeastern Egypt's Eastern Desert, bounded by the Red Sea, Nile Valley, and Suez Canal according to USGS geological surveys. This area contains documented mineral endowments including REE-bearing phosphates, heavy mineral sands containing monazite and xenotime, and iron oxide-apatite deposits.

Egypt's Documented Mineral Resources by Type:

| Resource Type | Location | Estimated Scale | Current Status |

|---|---|---|---|

| REE-bearing phosphates | Golden Triangle | Commercial quantities documented | No extraction operations |

| Heavy mineral sands | Red Sea coastal zones | Monazite and xenotime present | Exploration phase |

| Iron oxide-apatite | Eastern Desert | Multiple identified locations | Assessment ongoing |

| Phosphate production | Multiple sites | 6.8 million MT annually (2023) | Active commercial operations |

However, a critical data gap exists regarding reserve quantification. Unlike established rare earth provinces globally, Egypt lacks independently verified, peer-reviewed reserve estimates published by authoritative geological institutions such as USGS or British Geological Survey. This represents a significant limitation for investment analysis and project feasibility assessment.

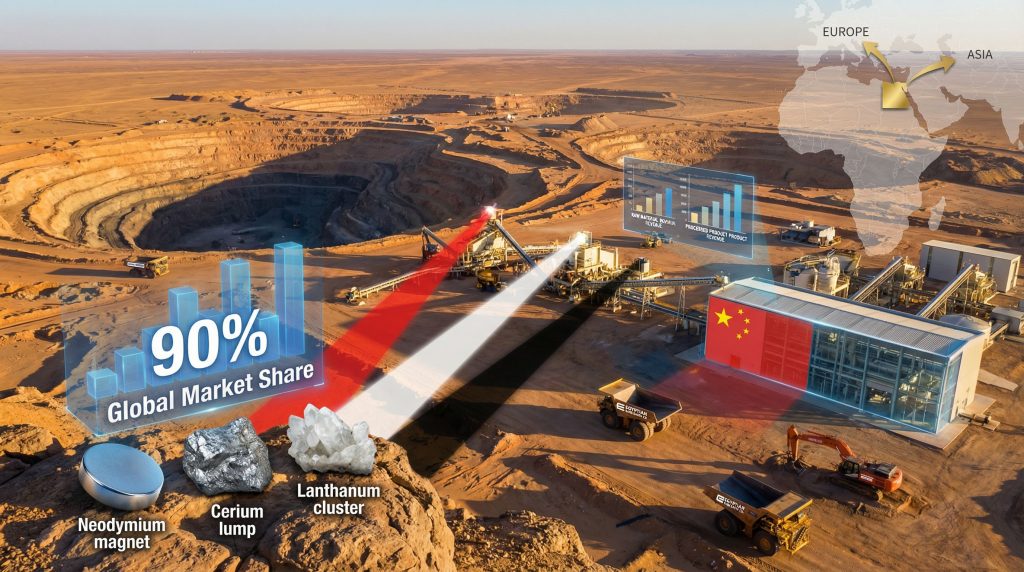

Global context provides important scale comparisons. China maintains 37 million metric tons of rare earth oxide equivalent reserves (37% of global identified reserves), while Vietnam holds 22 million metric tons and Myanmar possesses 24 million metric tons. Without confirmed reserve estimates, Egypt's resource significance remains speculative despite documented mineralisation.

Resource Quality vs. Quantity: The Critical Data Gap

The distinction between resource potential and economic viability represents the most significant uncertainty in assessing Egypt's rare earth prospects. Current information indicates scale, grade, and extraction economics remain undefined despite political announcements regarding development readiness.

Rare earth content in phosphatic byproducts typically ranges 500-1,500 ppm (parts per million) for light rare earths, with highly variable heavy rare earth distribution depending on deposit location and mineralogy. Egypt's current phosphate production of 6.8 million metric tons annually theoretically provides substantial rare earth byproduct potential, but actual recovery would require significant processing infrastructure investments not currently planned or budgeted.

Industry Analysis Note: Light rare earth elements typically constitute 70-85% of total rare earth concentrations in phosphate-associated deposits globally, while heavy rare earth elements represent 15-30% of total content but provide significantly higher economic value per unit.

Processing complexity analysis reveals substantial technical challenges. Monazite processing from heavy mineral sands requires radioactive thorium management protocols, adding regulatory and operational complexity requiring specialised infrastructure absent from current Egyptian mining operations. Recovery rates for rare earth elements from phosphate processing via hydrometallurgical methods typically range 60-85%, depending on acid digestion efficiency and separation technology sophistication.

The absence of feasibility studies, development timelines, and named projects represents a critical information gap for investment credibility. Without this technical foundation, announcements of readiness for processing appear premature and politically motivated rather than grounded in geological and economic analysis.

Why Are Chinese State Entities Egypt's Primary Technology Partners?

NORINCO, CNNC, and Norin Mining: Capability Matrix Analysis

Chinese state entities offer comprehensive capabilities that differentiate them from Western alternatives in rare earth development partnerships. This integrated approach combines technical expertise, financing capacity, and downstream market access through single organisational structures rather than requiring coordination across multiple private sector entities, especially as initiatives like the European CRM facility develop alternative approaches.

Chinese Partner Companies – Core Capabilities:

| Company | Ownership Structure | Relevant Technology | Global Experience | Processing Capacity |

|---|---|---|---|---|

| NORINCO | 100% state-owned (SASAC) | Integrated mining + SX separation | DRC copper, Zimbabwe projects | ~80,000 MT processing |

| CNNC | 100% state-owned (SASAC) | Hydrometallurgical + thorium mgmt | Uranium mining globally | ~60,000 MT processing |

| Norin Mining | Hong Kong registered, Chinese backing | Feasibility + project development | REE project assessment | Advisory capacity |

China's rare earth processing dominance provides the strategic context for these partnerships. Current data shows China controls approximately 60-65% of global rare earth processing capacity as of 2024, reduced from historical levels of 85-90% during 2010-2015 due to recent Western capacity development initiatives. However, China maintains 85% of global refined rare earth metal production, representing 170,000 metric tons of rare earth compounds annually.

NORINCO brings integrated supply chain management experience through mining and processing operations across Africa, particularly copper operations in Democratic Republic of Congo and development projects in Zimbabwe since the 1990s. The company's state ownership structure enables long-term capital commitments and risk tolerance that private sector alternatives typically cannot match in frontier mineral development contexts.

CNNC's competitive advantage centres on hydrometallurgical separation technology and thorium management protocols critical for monazite processing. The company's nuclear industry expertise provides specialised capabilities for handling radioactive byproducts that complicate rare earth extraction from heavy mineral sands, a potentially significant advantage for Egyptian deposits containing thorium-bearing minerals.

Technology Transfer vs. Dependency: Strategic Trade-offs

The fundamental strategic question involves whether Chinese partnerships enable Egyptian processing sovereignty or create upstream dependency relationships. Analysis of comparable partnerships reveals patterns that suggest technology transfer occurs primarily at extraction stages while downstream processing capabilities remain concentrated in Chinese facilities.

China's established rare earth strategy involves securing upstream access whilst maintaining downstream control through processing technology and market access. State-linked entities like NORINCO and CNNC operate within China's strategic materials system rather than functioning as neutral technology vendors, creating inherent conflicts between partner country sovereignty objectives and Chinese supply chain control preferences, particularly relevant given ongoing minerals recycling transition initiatives.

Comparative Partnership Analysis – Vietnam Model:

Vietnam's rare earth engagement with Chinese entities provides relevant precedents for potential Egyptian outcomes. Vietnamese operations at Dong Pao and bauxite residue recovery projects resulted in limited domestic processing capability development. Most ore and intermediate products require export to China for final separation, enabling Vietnam to capture 15-25% of value chain revenue whilst China retains 75-85% through processing and sales activities.

Myanmar Partnership Lessons:

Myanmar's experience demonstrates the limitations of technology partnerships without stable political frameworks. Despite possessing 24 million metric tons in rare earth reserves (world's third largest), actual extraction remains minimal at approximately 400 metric tons annually due to processing infrastructure gaps and geopolitical instability affecting Chinese joint venture implementation.

The integrated model that Chinese firms offer creates both advantages and dependencies. Capital requirements for rare earth separation facilities typically range $100-300 million USD for integrated mining-to-separation operations, representing substantial commitments that require long-term off-take agreements and technology licensing arrangements to justify investments.

What Are the Economic Development Scenarios for Egypt?

Scenario 1: Successful Domestic Processing Integration

The optimistic development pathway involves Egypt establishing sovereign rare earth processing capabilities through technology transfer and joint venture arrangements with Chinese partners. This scenario requires systematic capability development across multiple technical and institutional domains.

Steps to Establish Processing Sovereignty:

- Technology Acquisition Phase (Years 1-3): Secure solvent extraction systems, hydrometallurgical processing equipment, and separation technology through joint venture agreements with NORINCO or CNNC subsidiaries

- Workforce Development Requirements (Years 2-5): Establish technical training programmes for rare earth separation processes, environmental management protocols, and quality control systems requiring 500-1,000 specialised technicians

- Infrastructure Development Timeline (Years 3-7): Construct integrated processing facilities with $200-400 million capital investment including power generation, water treatment, and waste management systems

- Market Access Development (Years 5-10): Establish customer relationships with downstream rare earth consumers in automotive, renewable energy, and electronics sectors outside Chinese market control

Revenue projections under successful integration scenarios suggest Egypt could capture 60-75% of rare earth value chain revenue through domestic processing rather than raw material export. Assuming moderate-scale operations producing 10,000-20,000 metric tons of separated rare earth products annually, gross revenues could reach $200-500 million depending on market prices and product mix between light and heavy rare earths.

Employment generation potential includes 2,000-5,000 direct jobs in mining and processing operations, plus 8,000-15,000 indirect jobs in supporting industries, transportation, and services. This scale of employment creation would provide meaningful economic impact in targeted regions whilst developing technical capabilities transferable to other mineral processing industries.

Export diversification benefits extend beyond rare earth sales to potential development of downstream manufacturing capabilities in permanent magnets, catalysts, and specialty alloys that utilise rare earth inputs. This secondary industrial development could generate additional $100-300 million in annual export revenues once established.

Scenario 2: Resource Extraction Without Value Addition

The alternative scenario involves Egypt functioning primarily as a raw material supplier with limited domestic processing capability development. Historical analysis of African mineral partnerships with Chinese entities suggests this outcome occurs frequently despite initial intentions for technology transfer and value addition.

Raw material export economics provide significantly lower revenue capture compared to processed products. Rare earth ores and concentrates typically trade at 20-40% of the value of separated rare earth products, meaning Egypt would capture only a fraction of potential revenues whilst Chinese partners retain higher-margin processing and sales activities.

Raw Material vs. Processed Product Revenue Comparison:

| Product Level | Typical Price Range (per MT) | Egyptian Revenue Capture | Processing Location |

|---|---|---|---|

| Rare earth ore/concentrate | $500-1,500 | 100% of extraction value | Egypt |

| Mixed rare earth carbonate | $1,200-3,000 | Limited (if processed domestically) | China or Egypt |

| Separated rare earth oxides | $2,500-15,000+ | Minimal (if exported) | China |

| High-purity metals/alloys | $5,000-50,000+ | None (if not developed) | China |

This scenario creates economic dependency relationships where Egypt becomes reliant on Chinese partners for market access whilst providing limited domestic industrial development. Employment generation remains concentrated in extraction activities, typically creating 500-1,500 direct jobs compared to integrated processing alternatives.

Long-term implications include reduced leverage in price negotiations, limited technology transfer beyond basic mining operations, and vulnerability to changes in Chinese rare earth import policies or global supply chain restructuring that could reduce demand for Egyptian raw materials.

The risk of this outcome increases if initial joint venture agreements prioritise rapid revenue generation over capability building, or if Egyptian government priorities shift toward short-term foreign exchange earnings rather than long-term industrial development objectives.

How Does This Partnership Reshape Regional Critical Mineral Dynamics?

North African Rare Earth Competition Landscape

Regional competition dynamics in North Africa create both opportunities and constraints for Egyptian rare earth development initiatives. Morocco's established position in phosphate production provides competitive advantages in related mineral processing, whilst Algeria's untapped rare earth potential represents a future competitive threat if developed systematically.

Morocco's phosphate infrastructure produces 43 million metric tons annually, generating substantial export revenues and creating economies of scale in mineral processing technologies. Morocco's state-owned OCP Group has developed integrated supply chains from mining through processing to international distribution, providing a successful model for state-led mineral development that Egypt appears to be replicating for rare earths.

Algeria possesses documented rare earth deposits but lacks commercial-scale extraction operations. However, Algeria's energy infrastructure and existing industrial base could support rapid rare earth development if Chinese or other international partners provide similar technology and financing packages to those offered to Egypt. This creates competitive pressure for Egypt to establish first-mover advantages before regional alternatives emerge.

Regional supply chain integration opportunities exist through coordination rather than competition. North African rare earth development could create specialised processing hubs where Egypt focuses on specific rare earth elements or processing stages whilst Morocco and Algeria develop complementary capabilities. This approach would maximise regional leverage in global supply chain negotiations.

Cross-border infrastructure development could reduce individual country costs for rare earth processing. Shared power generation, transportation corridors, and technical expertise would enable smaller-scale operations to achieve economies of scale through regional cooperation rather than requiring each country to develop complete supply chains independently.

Impact on Global Supply Chain Diversification Efforts

Western nations' critical mineral security strategies increasingly emphasise supply chain diversification away from Chinese-controlled sources. The Egypt China rare earth partnership creates complex implications for these diversification efforts, potentially reducing Chinese geographical concentration whilst maintaining Chinese processing control.

The European Union's Critical Raw Materials Act and United States' Defense Production Act prioritise developing alternative rare earth sources outside Chinese influence. Egyptian production could theoretically support these objectives by providing non-Chinese raw materials, but Chinese partnership structures may limit the effectiveness of this geographic diversification if processing remains Chinese-controlled.

Supply Chain Analysis: Geographic diversification without processing sovereignty may provide limited strategic benefits for consuming nations seeking to reduce rare earth supply vulnerabilities, as bottleneck control simply shifts from Chinese mines to Chinese processing facilities using internationally sourced raw materials.

Alternative partnership opportunities exist with Western allies through different development models. US Development Finance Corporation, European Bank for Reconstruction and Development, and allied government agencies offer project financing for critical mineral development, though typically with longer approval timelines and additional governance requirements compared to Chinese state entity partnerships.

Market psychology factors influence investment flows and policy decisions regarding rare earth supply security. Egyptian production announcements may reduce perceived supply risk premiums in rare earth pricing even before commercial production begins, affecting global market dynamics and investment decisions in competing projects.

The success or failure of the Egypt China rare earth partnership model will influence similar decisions by other African nations with rare earth potential, potentially accelerating the spread of Chinese-partnered development or encouraging alternative partnership models depending on outcomes achieved.

The next major ASX story will hit our subscribers first

What Investment and Development Risks Should Stakeholders Consider?

Technical and Operational Risk Assessment

Rare earth project development involves substantial technical risks that extend beyond traditional mining operations due to complex metallurgical processing requirements and environmental management challenges. Egyptian projects face additional risks due to limited domestic experience in rare earth extraction and processing technologies.

Project Development Risk Factors:

| Risk Category | Specific Concerns | Mitigation Requirements | Timeline Impact |

|---|---|---|---|

| Environmental compliance | Thorium management, acid waste treatment | Specialised facility design, regulatory approval | 12-24 months additional |

| Technical feasibility | Processing technology adaptation | Pilot plant operations, metallurgical testing | 18-36 months validation |

| Infrastructure development | Power, water, transportation access | Major capital investment, government coordination | 2-5 years construction |

| Workforce availability | Specialised technical skills gap | Training programmes, international recruitment | 2-3 years development |

Processing technology adaptation represents a critical technical risk. Rare earth separation requires precise chemical process control and specialised equipment that may not perform identically across different ore compositions. Egyptian deposits may require customised processing approaches that increase development costs and extend commissioning timelines beyond initial projections.

Environmental regulations create compliance risks particularly for thorium-bearing mineral processing. International atomic energy agency protocols for radioactive material handling require specialised infrastructure and operational procedures that add $20-50 million to facility development costs and extend regulatory approval timelines significantly.

Water availability and quality represent operational constraints in Egypt's arid climate. Rare earth processing typically requires 3-8 cubic metres of water per metric ton of processed ore, creating sustainability challenges and potential conflicts with agricultural and municipal water demands in resource-constrained regions.

Geopolitical and Economic Risk Evaluation

International sanctions and trade policy developments create significant risks for projects involving Chinese state entities. US and European sanctions regimes increasingly target Chinese companies involved in critical mineral supply chains, potentially affecting financing, technology transfer, and market access for Egyptian rare earth operations.

Currency stability and investment protection frameworks influence project viability through their impact on long-term investment returns. Egyptian pound devaluation risks affect project economics when capital investments are denominated in US dollars or Chinese yuan whilst revenues may be received in local currency or subject to government pricing controls.

Regional security considerations could affect long-term operations through disruption of transportation infrastructure, workforce availability, or international partnership stability. Red Sea shipping lane security issues demonstrated in 2023-2024 highlight vulnerability of export-dependent industries to regional conflict spillover effects.

Contract enforcement and dispute resolution mechanisms between Egyptian entities and Chinese partners may involve complex jurisdictional issues. International arbitration processes for state-to-state commercial disputes can extend for years and create uncertainty regarding investment protection and operational control during conflict periods.

Market access dependency risks emerge if Egyptian rare earth production becomes primarily dependent on Chinese downstream customers. Alternative market development requires substantial marketing investments and customer relationship building that may not be prioritised if Chinese partners provide guaranteed off-take agreements.

Frequently Asked Questions About Egypt's Rare Earth Strategy

Timeline and Implementation Questions

Commercial production timelines depend heavily on the completion of feasibility studies and detailed geological assessments that have not yet been publicly disclosed. Based on international rare earth project development experiences, integrated mining and processing operations typically require 5-8 years from initial development decisions to commercial production.

Investment level requirements for commercial-scale operations are substantial. International rare earth processing facilities typically require $100-300 million USD in capital investment for basic separation capabilities, with additional $50-150 million required for integrated mining infrastructure depending on deposit characteristics and processing complexity.

Environmental regulation impacts will significantly influence development timelines. Rare earth operations require environmental impact assessments, waste management plans, and specialised permits for radioactive material handling where applicable. Regulatory approval processes typically add 12-24 months to project development schedules in emerging market jurisdictions.

Strategic Partnership Structure

Ownership models under consideration have not been publicly disclosed, but international precedents suggest joint venture structures where Chinese partners provide technology and financing in exchange for equity stakes and long-term off-take agreements. Egyptian government participation typically involves mineral rights provision and infrastructure development support.

Technology transfer agreements structure will determine whether Egypt develops independent processing capabilities or remains dependent on Chinese technical support for operations. Successful technology transfer requires not just equipment provision but also training programmes, technical documentation, and ongoing support agreements that enable autonomous operations.

Egyptian company roles in operations will likely evolve from junior partners in initial development phases toward increased operational responsibility over time. However, the pace and extent of this transition depends on contract negotiations and Egyptian institutional capacity building that has not yet been detailed publicly.

Long-term Strategic Implications for Global Rare Earth Markets

Supply Security and Market Competition Effects

Egyptian rare earth production could contribute to global supply diversification efforts whilst potentially maintaining Chinese processing control depending on partnership structures implemented. Geographic diversification without processing sovereignty may provide limited strategic benefits for consuming nations seeking to reduce supply vulnerabilities.

Price stability implications for downstream industries depend on production scale and market access arrangements. Additional supply sources generally contribute to price stability by reducing single-source dependencies, but the magnitude of impact depends on actual production volumes achieved and their integration into existing supply chains.

Market Impact Projections:

- Potential production scale: 10,000-30,000 metric tons annually (based on comparable development projects)

- Global market share: 5-15% of current global production if successful

- Price impact potential: Limited unless production reaches 20,000+ MT annually

- Timeline to market impact: 7-10 years from current development stage

Market competition effects will likely be concentrated in light rare earth elements rather than high-value heavy rare earths, based on typical composition of phosphate-associated and heavy mineral sand deposits. This limits potential impact on supply security for the most strategically critical rare earth elements used in advanced technology applications.

Technology Innovation and Processing Evolution

Opportunities for next-generation extraction technologies may emerge through Egyptian rare earth development, particularly in areas of environmental impact reduction and processing efficiency improvement. Chinese partners' technical capabilities could contribute to technological advancement if partnership agreements incentivise innovation rather than replication of existing processes.

Environmental sustainability improvements in rare earth processing represent a key opportunity area. Advanced acid recovery, tailings management, and water recycling technologies could be implemented in Egyptian operations to address environmental concerns that have historically affected rare earth industry development globally.

Regional expertise development potential extends beyond rare earth processing to broader critical mineral capabilities. Successful technology transfer could establish Egypt as a regional hub for mineral processing expertise, supporting development of other critical mineral resources across North Africa and creating additional economic diversification opportunities.

The success of the Egypt China rare earth partnership model will influence global patterns of critical mineral development cooperation, potentially encouraging similar state-to-state partnerships in other resource-rich developing nations or highlighting the limitations of technology transfer approaches that maintain processing dependencies. Furthermore, this partnership demonstrates how nations are seeking to secure strategic mineral partnerships whilst considering broader critical mineral supply chain resilience.

Investment Disclaimer: This analysis is based on publicly available information and industry precedents. Actual project development outcomes may differ significantly from projections discussed. Potential investors should conduct independent due diligence and risk assessment before making investment decisions related to rare earth development projects or companies involved in these partnerships.

Ready to Capitalise on Critical Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers instant alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities in critical minerals and rare earth sectors before broader market recognition. Explore historic examples of exceptional returns from major mineral discoveries by visiting Discovery Alert's discoveries page, then begin your 30-day free trial to position yourself ahead of evolving global supply chain developments.