July 21, 2026

The Industrial Fault Line Beneath European Sanctions Policy

Every time the European Union attempts to tighten its economic grip on Russia, it runs headlong into the same structural problem: Europe's industrial base is deeply entangled with the very supply chains it seeks to restrict. This tension rarely surfaces as cleanly as it has in the ongoing debate over EU sanctions on Aughinish Alumina, a refinery on Ireland's Shannon Estuary that sits at the intersection of geopolitical ambition and raw material dependency.

The story of why Brussels stepped back from sanctioning this facility is not simply a tale of political hesitation. It is a revealing case study in how commodity-level sanctions collide with industrial self-preservation, and why the EU's own architecture makes rapid policy change structurally difficult even when the moral argument for action appears compelling.

When big ASX news breaks, our subscribers know first

Understanding Aughinish Alumina's Role in the European Supply Chain

A Facility Whose Scale Makes It Hard to Ignore

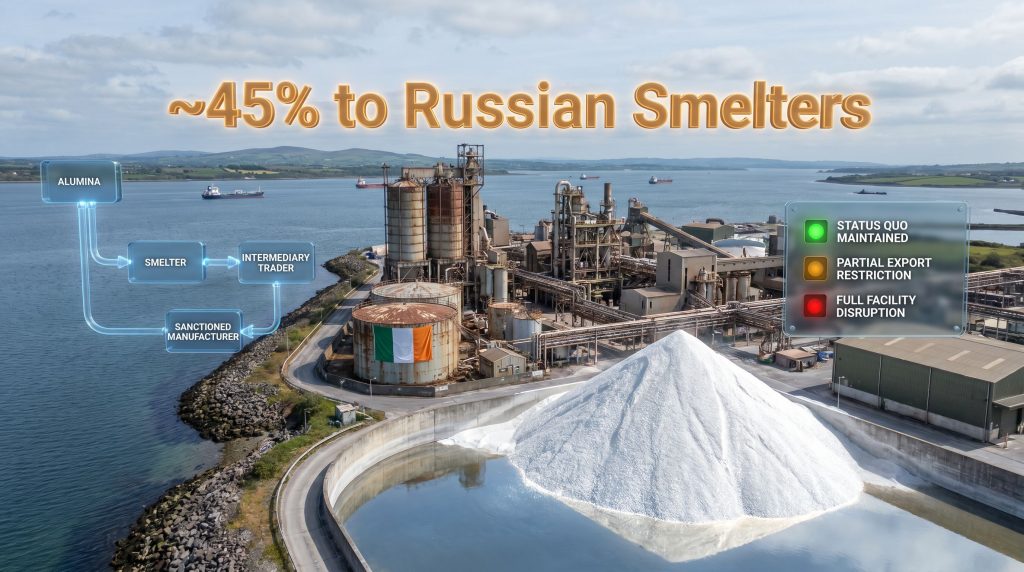

Positioned on the Shannon Estuary in County Limerick, Ireland, Aughinish Alumina operates as one of the largest alumina refineries within the European Union. The plant is owned by Rusal, the Russian aluminium producer that ranks among the world's largest primary aluminium companies by output volume.

To understand why this refinery generates such intense policy debate, it helps to understand what alumina actually is and where it sits in the aluminium production hierarchy:

- Bauxite ore is mined and then refined through the Bayer process to produce aluminium oxide, commonly called alumina

- Alumina is the essential feedstock fed into electrolytic smelters to produce primary aluminium

- Without a consistent alumina supply, smelter operations contract, and downstream manufacturing across automotive, aerospace, packaging, and construction sectors feels the impact

- Europe's smelting capacity is already operating under structural pressure from elevated energy costs, meaning any feedstock disruption carries amplified consequences

The plant's export profile adds further complexity to the policy picture. According to the company's own figures, approximately 55% of Aughinish's 2025 exports were directed toward European and international customers, while the remaining 45% went to Russian smelters operating under Rusal's ownership. That 45% figure has become the focal point of the entire sanctions debate, and its implications extend well beyond the aluminum and alumina markets of a single member state.

The Aluminium Value Chain: Why Intermediate Materials Matter

One dimension of this debate that tends to receive insufficient attention is the chemical and industrial specificity of alumina itself. Unlike finished aluminium products, alumina is an intermediate oxide compound. Its production involves precise refining conditions, and its quality specifications, particularly in terms of particle size distribution, sodium content, and loss-on-ignition characteristics, affect smelter efficiency and metal quality at every downstream stage.

This means that alumina supply is not instantly interchangeable. Smelters that have optimised their operational parameters around a particular alumina specification cannot simply substitute alternative supply without productivity consequences. This physical characteristic of the material, independent of any financial or geopolitical consideration, is part of why European smelters are cautious about disruptions to established supply relationships.

The Alleged Indirect Supply Chain: What Investigators Found

A joint investigation conducted by The Irish Times and the Organized Crime and Corruption Reporting Project examined how aluminium produced using Aughinish-sourced alumina flows through the Russian industrial system. The findings outlined a multi-step indirect pathway:

- Aughinish refines bauxite into alumina at its Limerick facility

- Alumina is exported to Rusal-operated smelters located in Russia

- Those smelters convert alumina into primary aluminium metal

- The primary aluminium is then sold through a Moscow-based trading intermediary

- That trading entity reportedly supplies materials to Russian manufacturers formally listed under EU sanctions as defence-sector entities

The critical legal and political complexity here is that Aughinish itself does not transact directly with any sanctioned entity at any point in this chain. The alleged harm is entirely indirect, a feature that makes regulatory intervention both legally contested and politically fraught.

This indirect model is not a novel evasion technique. It reflects the structural reality of globally integrated commodity supply chains, where raw materials pass through multiple ownership changes and processing stages before reaching their final application. The difficulty for sanctions architects is that existing EU frameworks are primarily designed to target direct transactions with designated parties, not downstream industrial flows that are several ownership transfers removed from the original export.

Why the EU Declined to Act: Three Structural Barriers

1. Supply Chain Disruption Risk

European aluminium smelters already face a compounding set of pressures. Energy cost inflation has eroded the competitiveness of EU-based primary aluminium production over recent years, with several smelters reducing output or entering temporary curtailment. Against that backdrop, restricting access to one of the bloc's largest alumina suppliers would remove a critical feedstock source from an already strained system.

Industry observers have noted that raw material availability, rather than energy alone, is increasingly becoming a binding constraint for European smelters. Any alumina price spike flowing from Aughinish disruption would translate directly into higher primary aluminium production costs, with downstream consequences for manufacturers across multiple end-use sectors. Furthermore, the broader aluminium tariff impacts already circulating in global markets have added additional pressure to an already fragile supply picture.

2. Economic Consequences for Ireland

Aughinish communicated directly to the Irish government that restrictions on alumina exports to Russia could jeopardise the economic viability of the Limerick facility. The company's position, as reported, was that such measures would produce no meaningful impact on Russia's industrial capacity while potentially creating commodity market inflation across Europe.

The Irish government's response has been to publicly resist supporting sanctions measures that would disproportionately harm domestic industry. This is a nationally rational position, but it illustrates precisely the kind of member state resistance that makes EU-wide commodity sanctions so difficult to advance.

3. The Unanimity Requirement

Perhaps the most consequential structural barrier is procedural. Adding any new commodity to the EU sanctions list requires unanimous agreement across all member states. This is an exceptionally high threshold when the commodity in question directly affects the industrial base of multiple EU economies.

Member states with significant downstream aluminium manufacturing, those whose smelters and fabricators depend on reliable alumina feedstock, have no incentive to vote for restrictions that damage their own production sectors. The unanimity rule means a single economically exposed member state can effectively veto the entire measure. Consequently, the broader debate around tariffs and supply chains at the EU level has made achieving that consensus even more difficult.

The Legal Gap at the Centre of the Debate

The phrase circulating in policy discussions is instructive: alumina is not currently classified as a restricted or sanctioned commodity under EU trade law. This means that Irish-based alumina exports to Russia remain entirely lawful, regardless of what downstream applications that alumina may ultimately support. Several factors make closing this gap structurally difficult:

- Legal classification issues: Alumina is an industrial oxide, not a dual-use technology or a finished military product, which are the categories that typically trigger sanctions designations under EU frameworks

- Proportionality constraints: EU sanctions law requires demonstrated proportionality between the measure and its stated objective; broad commodity bans risk being challenged on those grounds by affected industrial parties

- Indirect harm doctrine: EU sanctions architecture is designed around direct transactional links to designated entities, not attenuated downstream flows through multiple intermediary stages

- Precedent concerns: Sanctioning an intermediate industrial material without a direct military classification could open regulatory challenges affecting other commodity-level trade restrictions across the broader sanctions framework

Who Is Pushing for Change, and What Arguments Are They Making?

Despite the European Commission's cautious stance, political pressure for expanding the sanctions perimeter has been building. Multiple Members of the European Parliament have formally urged the Commission to include alumina in future sanctions packages. Belgium has publicly committed to advocating for the closure of what critics describe as an alumina export loophole within EU institutional channels.

The EU's sanctions envoy has also acknowledged that the framework may need reassessment in light of how aluminium-related materials interact with Russia's defence-industrial base. In addition, the recently adopted EU metals action plan has intensified scrutiny of how strategic materials flow through the bloc's industrial base, adding further momentum to the calls for reform.

The core argument advanced by sanctions proponents rests on three pillars:

- Aluminium is a strategically important input for Russia's defence production, appearing in weapons systems, military vehicles, and aerospace platforms

- Allowing EU-based production to feed Russian smelters, even indirectly, undermines the economic isolation objectives that the broader sanctions programme is designed to achieve

- The indirect supply chain model, if left unaddressed, creates a replicable blueprint for routing other restricted materials through legitimate EU industrial operations

The next major ASX story will hit our subscribers first

Scenario Analysis: What Happens If Policy Changes?

| Scenario | Trigger Condition | Likely Market Impact |

|---|---|---|

| Status Quo Maintained | No unanimous EU agreement on alumina sanctions | Aughinish continues operating; political pressure persists but supply chain remains stable |

| Partial Export Restriction | EU restricts alumina exports to Russia-affiliated entities only | Aughinish redirects volumes; Russian smelters face feedstock constraints; European spot prices may tighten modestly |

| Full Facility Disruption | Sanctions render the Limerick plant economically unviable | Significant EU supply shortfall; alumina spot price spike; downstream aluminium cost inflation across automotive, aerospace, and packaging sectors |

The third scenario carries the most severe downstream consequences. Several EU-based smelters source alumina from Aughinish as part of their primary feedstock mix. A sudden removal of that supply, without sufficient alternative sourcing arranged in advance, would force smelters to either curtail output or absorb higher spot market costs. Both outcomes translate into higher aluminium prices for the downstream manufacturers and end users who ultimately consume the metal.

A Broader Precedent With Implications Beyond Alumina

The debate over EU sanctions on Aughinish Alumina reflects a wider structural challenge confronting EU sanctions architecture: how to apply commodity-level restrictions to globally integrated industrial supply chains without generating disproportionate self-harm. This tension has previously emerged in EU debates over Russian gas dependency, fertiliser precursor materials, and other industrial inputs where European economic interests are directly entangled with Russian supply.

What makes the alumina case particularly instructive is the specificity of the indirect harm allegation. The investigative findings did not allege that Aughinish knowingly supplied a sanctioned entity. They alleged that alumina, processed through multiple stages of lawful commercial activity, eventually contributed to a supply chain that reached sanctioned defence manufacturers. Whether existing sanctions frameworks are equipped to address that level of indirect causal connection remains an open legal question.

Policymakers in Brussels must weigh several competing considerations simultaneously:

- Whether restricting alumina materially degrades Russia's defence-industrial output, given that Russia has alternative bauxite and alumina supply routes through Guinea, Australia-linked trade flows, and domestic refining capacity

- Whether the economic costs imposed on European industry are proportionate to the strategic benefit the restriction would deliver

- Whether sanctioning an intermediate industrial oxide sets a workable regulatory precedent for future commodity-level decisions, particularly as the EU looks to expand sanctions coverage in coming packages

Furthermore, the broader competitive dynamics among global aluminium producers mean that any European supply disruption could rapidly translate into market share shifts that are difficult to reverse once established. As investigative reporting from outlets including iStories Media has detailed, the pathway from Irish alumina to Russian industrial output may be more direct than the legal framework currently acknowledges.

The European Commission's decision to defer action on Aughinish is less an expression of political indifference and more a reflection of the structural constraints that govern sanctions policy when member state industrial interests and geopolitical objectives are in direct conflict. Resolving that conflict, if it can be resolved, will require either a new legal framework for addressing indirect supply chain harm or a level of member state consensus that has not yet materialised.

Key Takeaways on EU Sanctions and Aughinish Alumina

- Alumina remains outside the EU sanctions perimeter as of mid-2026, creating a legally permissible but politically contested trade channel between Ireland and Russia

- Approximately 45% of Aughinish's 2025 exports reportedly went to Russian Rusal-operated smelters, with the remaining 55% serving European and other international customers

- The indirect supply chain pathway from Irish refinery to Russian smelter to defence-linked manufacturer is the core allegation driving political pressure for EU sanctions on Aughinish Alumina expansion

- The EU's unanimity requirement for sanctions additions creates a high structural barrier to rapid policy change when member states face direct economic exposure to the outcome

- The physical specificity of alumina as an industrial feedstock means disruption cannot be easily absorbed through spot market substitution, amplifying the market consequences of any policy change

- The outcome of this debate will shape how the EU approaches commodity-level sanctions for other intermediate industrial materials with potential dual-use downstream applications

Disclaimer: This article contains forward-looking analysis, scenario projections, and market assessments that involve inherent uncertainty. Readers should not interpret any content here as financial, investment, or legal advice. Policy outcomes described are speculative and subject to change based on geopolitical developments and EU institutional decisions.

Want to Stay Ahead of Commodity Market Shifts Driven by Geopolitical Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity and exploration data into actionable investment insights — explore historic discoveries and their market returns to understand the scale of opportunity at stake, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major market move.