June 23, 2026

The Infrastructure Imperative: Understanding Europe's Battery Storage Transformation

When electricity grids were originally designed, the core assumption was simple: generation follows demand. Operators would spin up power plants as consumption rose and dial them back when it fell. That model worked reasonably well for decades, but it was always fragile. The accelerating deployment of solar and wind energy has fundamentally broken that assumption. Generation no longer follows demand; it follows weather. And the only technology capable of reconciling that mismatch at scale is battery storage.

This is the structural reality underpinning what the SolarPower Europe European battery market outlook for 2026 to 2030 describes with striking clarity: a market that has recorded twelve consecutive years of record annual installations is not experiencing a cyclical surge. It is experiencing a permanent architectural shift in how Europe manages its electricity system.

When big ASX news breaks, our subscribers know first

What 2025's Deployment Numbers Actually Tell Us

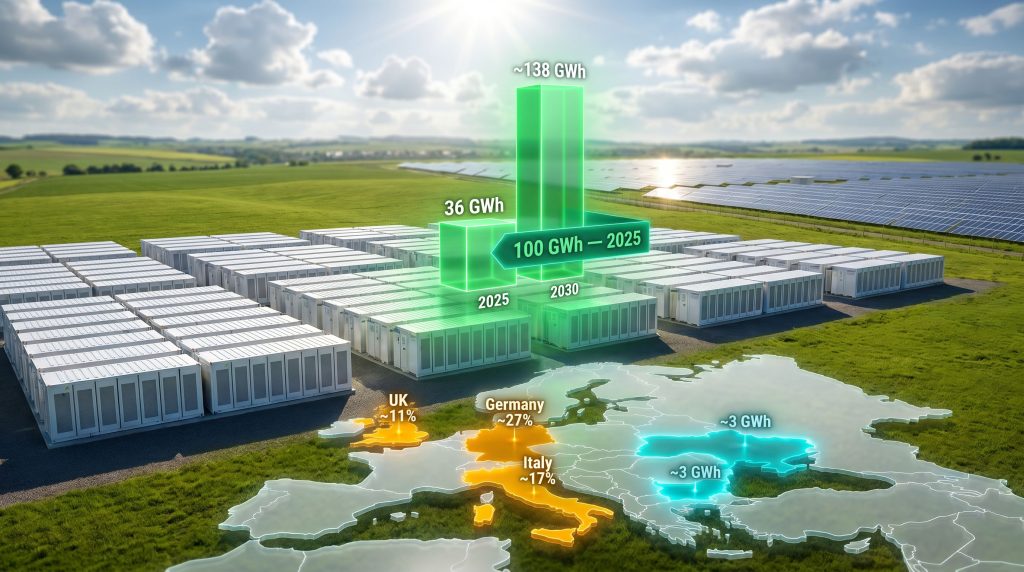

The headline figures from Europe's 2025 battery storage performance are compelling on their face. Annual new installations reached 36 GWh, representing 48% year-on-year growth, and cumulative installed capacity crossed the 100 GWh threshold for the first time in the continent's history. However, the more revealing story lies beneath those aggregates.

The Utility-Scale Tipping Point

For the first time, large-scale battery deployments accounted for more than half of all new European capacity added in a single year. Utility-scale installations reached 19 GWh in 2025, nearly doubling the 9.7 GWh recorded in 2024. This is not simply a quantitative jump; it represents a qualitative shift in who is building storage, why, and at what scale.

The segment breakdown underscores this realignment:

| Segment | 2024 Share | 2025 Share | Growth Rate |

|---|---|---|---|

| Utility-Scale (Large-Scale) | Below 50% | Above 50% (19 GWh) | ~96% year-on-year |

| Residential and C&I Combined | Above 50% | Below 50% | +16% combined |

Residential and commercial and industrial (C&I) storage continued to grow in absolute terms, rising 16% combined, but the centre of gravity has decisively shifted. This transition carries significant implications for how the market is financed, how projects are structured, and what technologies dominate procurement pipelines going forward.

Why Utility-Scale Has Become the Market's Engine

Five interconnected forces are accelerating large-scale battery energy storage system (BESS) deployment across Europe:

-

Grid flexibility requirements rising sharply as solar and wind penetration increases intraday volatility and creates acute balancing needs that thermal generation cannot address at the required response speeds.

-

Revenue stacking capabilities that allow utility-scale assets to participate simultaneously in frequency regulation markets, capacity remuneration mechanisms, wholesale energy arbitrage, and ancillary services, creating multi-layered revenue profiles that improve project bankability.

-

Lithium-ion cost compression continuing to reduce per-kilowatt-hour economics for all duration categories, with long-duration storage economics improving particularly rapidly as cell prices fall. Furthermore, developments in the battery raw materials market are adding further downward pressure on input costs.

-

Hybrid solar-plus-storage configurations becoming the default project structure for new utility-scale solar developments across Southern and Central Europe, embedding BESS into renewable project pipelines from the design stage.

-

Institutional capital deployment accelerating as improved revenue visibility and more bankable contract structures draw long-term infrastructure investors into the sector, reducing the cost of capital for project developers.

Industry Insight: Revenue stacking is one of the least understood but most financially important concepts in battery storage project development. A single utility-scale BESS asset can generate income from multiple sources simultaneously: selling frequency response services to grid operators, participating in day-ahead energy markets, providing capacity to system operators, and offering balancing services. This multi-stream revenue architecture is what separates modern BESS project economics from the single-revenue-stream models that made early storage projects difficult to finance.

Geographic Diversification: Reading the Market Maturity Signal

The Established Leaders and Their Declining Dominance

Germany, the United Kingdom, and Italy retained their positions as Europe's three largest battery storage markets in 2025. However, their combined share of new annual installations fell to approximately 47%, down sharply from nearly 80% in 2023 and 2024. That contraction in concentration is one of the most strategically significant data points in the entire report.

Germany continues to lead with roughly 27% of new capacity, followed by Italy at 17% and the United Kingdom at 11%. All three markets benefit from well-developed wholesale electricity markets, established grid services frameworks, and relatively mature project finance ecosystems.

The Surprise Entrants: Ukraine and Bulgaria

Ukraine and Bulgaria each entered the top five European battery storage markets for the first time in 2025, with both countries adding close to 3 GWh of new capacity. Their simultaneous emergence is analytically important for entirely different reasons.

Bulgaria's arrival reflects the broader maturation of Central and Eastern European electricity markets, where grid modernisation programmes and rising renewable penetration are creating genuine storage demand. Its presence signals that the geographic expansion of European storage deployment is systematic, not opportunistic.

Ukraine's case is categorically different. Battery storage in Ukraine has transitioned from a commercially attractive investment opportunity into a national energy security imperative. Extensive damage to the country's conventional power infrastructure has created an acute operational need for distributed and grid-scale storage capacity. This dynamic, where critical minerals and energy security considerations increasingly drive deployment decisions, is becoming more relevant across Eastern European markets with ageing or vulnerable grid infrastructure.

Structural Signal: When storage deployment spreads across a larger number of national markets, the overall market becomes more resilient to single-country policy cycles. The declining share of the top three markets is therefore a positive structural indicator, not a sign of weakening in the core markets.

SolarPower Europe's 2026 to 2030 Forecast: Scenarios and Implications

Projected Annual Installation Trajectory

| Year | Annual Installations (Medium Scenario) | Key Context |

|---|---|---|

| 2025 (Actual) | 36 GWh | 48% year-on-year growth; 12th consecutive record year |

| 2026 (Projected) | Above 50 GWh | First year expected to breach the 50 GWh threshold |

| 2029 (Medium Scenario) | ~118 GWh | Utility-scale comprising approximately 69% of new additions |

| 2029 (Best Case) | ~183 GWh | High-scenario trajectory implying a CAGR of up to 55% |

| 2030 (Medium Scenario) | ~138 GWh | Aligned with the EU's 200 GW storage target pathway |

Cumulative Capacity Milestones

| Milestone | Projected Timeframe | Scenario |

|---|---|---|

| 100 GWh cumulative | End of 2025 | Achieved |

| ~200 GWh cumulative | 2027 to 2028 | Medium |

| ~400 GWh cumulative | 2029 | Medium (EU-27 at ~334 GWh) |

| ~580 GWh cumulative | End of 2030 | Medium scenario |

| ~600 GWh cumulative | 2030 | High scenario |

The Gap Between Ambition and Trajectory

The SolarPower Europe European battery market outlook has been direct in acknowledging that even its medium-scenario projections may fall short of what Europe's electricity system actually requires. The EU has formally recognised the need for 200 GW of storage capacity by 2030 to maintain system adequacy as renewable penetration increases. Translating that political target into physical deployment will require annual installation rates to nearly double from current levels, sustained consistently through the end of the decade.

That is not a technology problem. It is a permitting problem, a market design problem, and a financing problem. According to Solar Power Europe's European market outlook for battery storage, the pace of regulatory reform will ultimately determine whether Europe can meet its stated ambitions.

The Policy Architecture Problem: Where the Deployment Gap Actually Lives

Four Critical Levers Identified by SolarPower Europe

The report identifies four specific policy interventions as essential to closing the gap between current trajectories and 2030 targets:

-

Streamlined permitting and grid connection processes — Regulatory approval timelines remain among the most consistently cited barriers to project execution across European markets. Projects that are technically ready and financially structured can spend years in permitting queues, destroying return profiles and delaying grid integration.

-

Market access and revenue stacking frameworks — Ensuring BESS assets can participate across multiple revenue streams without regulatory fragmentation is critical to project bankability. Markets where storage assets are restricted to single revenue streams produce weaker economics and attract less capital.

-

Stable and bankable investment conditions — Long-term revenue certainty structures, including capacity remuneration mechanisms, are essential for satisfying infrastructure lender requirements. Without bankable offtake or equivalent revenue security, project finance remains structurally challenging for many developers.

-

Scaled EU deployment instruments — Direct deployment support through mechanisms including the Innovation Fund, Horizon Europe, and European Investment Bank clean energy financing windows can bridge the gap between commercial project pipelines and the volume of deployment required to meet system adequacy targets.

Policy Tension: Europe's storage ambition is well-documented at the political level, but the regulatory infrastructure needed to translate that ambition into bankable projects has not kept pace with deployment targets. The primary obstacle is not technology readiness or capital availability; it is the coherence and speed of the regulatory environment in which projects must be developed.

Battery Storage Europe: Industry Coordination as a Deployment Accelerant

SolarPower Europe operates the Battery Storage Europe platform, a dedicated industry initiative that brings together major energy developers, grid operators, and technology providers to coordinate market development and policy engagement. Founding participants include large-scale European energy companies such as EDP and Statkraft.

The platform's ambition — a tenfold expansion in installed capacity by 2030 relative to its founding baseline — underscores the scale of acceleration the industry considers both necessary and achievable under the right conditions. In addition, current medium-scenario forecasts suggest that hitting the upper end of that ambition will require consistent outperformance against baseline projections throughout the remainder of the decade.

The next major ASX story will hit our subscribers first

Supply Chain Geopolitics: The Chinese Manufacturing Dependency Question

A Shifting Global Procurement Landscape

Europe's strong domestic deployment growth is occurring against a backdrop of intensifying global scrutiny over Chinese battery supply chains. The US Department of Defense has placed prominent Chinese energy storage and solar manufacturers — including CATL, BYD, JA Solar, Trina Solar, Three Gorges, and Huawei — on a trade restriction list effective from 2027. While this is a US policy measure, its ripple effects on global procurement strategies are already being felt across European project pipelines.

Simultaneously, the European Investment Bank has extended a funding restriction on high-risk inverters and BESS power conversion system (PCS) suppliers, explicitly including certain Chinese manufacturers, to cover renewable energy projects receiving EIB financing. This policy applies to billions of euros in project funding and is already redirecting European procurement toward alternative supply sources. Consequently, Europe's critical minerals supply chain is attracting renewed strategic attention from policymakers and investors alike.

| Region | Key 2025 Characteristic | 2030 Outlook |

|---|---|---|

| Europe | 36 GWh annual; 100 GWh cumulative milestone crossed | ~580 GWh cumulative (medium scenario) |

| United States | Rapid utility-scale BESS expansion; IRA-driven investment | Sixfold demand growth projected by 2030 (SEIA) |

| China | Dominant global manufacturer and deployer | Continued market leadership in production and deployment |

This dual pressure — from US trade restrictions reshaping global sourcing patterns and EU financing rules narrowing the pool of bankable suppliers for European projects — creates both near-term friction and longer-term opportunity. Near-term friction arises from cost and supply chain adjustment requirements. The longer-term opportunity lies in the potential for European and allied-nation battery manufacturing investment to fill the procurement gap, a process supported by the establishment of a critical raw materials facility within the EU's broader industrial strategy.

The Residential Segment Contraction: A Structural Correction, Not a Crisis

The near-term outlook for residential battery storage is notably more challenging than the utility-scale picture. Residential storage is projected to contract by approximately 17% in coming years, primarily reflecting the expiry of household subsidy programmes in Germany and other core European markets. Germany, which has historically driven a significant share of residential storage installations, has seen the withdrawal of key incentive schemes that previously made behind-the-meter storage economically attractive for homeowners.

The C&I segment is partially absorbing this decline, growing its market share by approximately 2 percentage points, but the overall trajectory for distributed storage is one of consolidation rather than expansion in the near term. This does not represent a structural failure of the residential storage concept; it reflects the natural maturation of a market segment that has become progressively less dependent on subsidy support as hardware costs have fallen.

What Europe's Battery Trajectory Signals for the Decade Ahead

Three Structural Shifts Defining the Next Phase

The SolarPower Europe European battery market outlook crystallises three structural shifts that will define how European storage markets evolve through 2030 and beyond:

-

Geographic diversification will progressively reduce concentration risk and open new national-level investment opportunities across Central and Eastern Europe, where grid modernisation needs and renewable expansion are creating fresh demand pools.

-

Utility-scale dominance will reshape project finance frameworks, grid planning methodologies, and technology procurement strategies across the continent, driving further standardisation and cost reduction in large-format BESS deployments.

-

Energy security imperatives will increasingly function as a deployment accelerant in markets with vulnerable or ageing grid infrastructure, operating independently of commercial return considerations and creating a class of storage deployment driven by resilience requirements rather than energy market economics. Furthermore, battery supply chain alliances are forming across allied nations to reduce dependence on any single supplier geography.

The Verdict on Europe's Storage Ambition

Europe's battery storage market is not simply expanding; it is fundamentally restructuring. The progression from a residential-led, subsidy-dependent sector to a utility-scale, commercially-driven, and energy-security-motivated market represents a maturation that few sectors achieve so visibly. The 100 GWh cumulative milestone crossed in 2025 is a landmark, but it also illustrates how far the journey still runs.

Whether the continent can convert this structural momentum into the deployment velocity required to meet its 2030 targets depends far less on technology capabilities or capital availability than on the speed and coherence with which European policymakers can reform the regulatory frameworks that currently constrain project execution. For broader context on Europe's solar and storage trajectory, SolarPower Europe's EU solar market outlook provides useful parallel analysis covering generation-side developments. The market is ready. The question is whether the policy environment can keep pace.

Readers seeking additional data and analysis on European battery storage market developments may find value in exploring ESS News (ess-news.com), a specialist publication covering energy storage markets, policy, technology, and industry developments across Europe and globally.

This article contains forward-looking projections and scenario-based forecasts sourced from third-party industry analysis. Such projections are inherently uncertain and should not be construed as financial advice. Actual market outcomes may differ materially from those described.

Want to Capitalise on the Minerals Driving Europe's Battery Storage Boom?

The battery storage revolution transforming Europe's electricity grids demands vast quantities of lithium, nickel, cobalt, and other critical minerals — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, turning complex data into actionable investment insights. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.