July 28, 2026

When Geopolitics Rewrites Energy Strategy Overnight

Supply security has historically been an afterthought in LNG contract negotiations, with price, volume, and flexibility dominating commercial discussions. That calculus changed decisively in late February 2026, when conflict involving Iran began restricting traffic through the Strait of Hormuz, a maritime chokepoint just 21 miles wide at its narrowest point, through which approximately one-fifth of global energy supply flows under normal conditions. Within days, the comfortable assumptions underpinning Asian buyers' supply portfolios evaporated, and the scramble for non-Middle Eastern LNG began in earnest.

For major integrated energy companies already tracking the global LNG supply outlook, this geopolitical rupture accelerated a strategic timeline that had been building for years. Among those companies, ExxonMobil finds itself in a particularly urgent position. Despite ranking as the world's largest publicly traded oil and gas company by market capitalisation, the U.S. supermajor has lagged considerably behind European rivals Shell and TotalEnergies in building a diversified, multi-basin LNG portfolio. That gap, long acknowledged internally, has become a pressing commercial liability in the post-Hormuz environment.

Reports surfaced in June 2026 that ExxonMobil is studying potential acquisition targets including Woodside Energy Group (ASX: WDS), Australia's largest LNG exporter, as part of early-stage internal deliberations focused on deepening its presence in global gas markets. No formal offer has been made, and both companies have declined to comment publicly. What makes this potential Exxon acquisition of Woodside Energy so strategically significant, however, extends well beyond a single transaction.

When big ASX news breaks, our subscribers know first

Woodside's Asset Base: Why It Stands Apart in the Global LNG Market

Understanding why Woodside has reportedly attracted ExxonMobil's attention requires appreciating what makes it genuinely difficult to replicate through organic growth alone. Woodside is not simply a producing LNG company. It is a multi-decade platform with producing assets, advanced development projects, established customer relationships, and a footprint spanning two hemispheres.

The following table illustrates the core strategic assets that make Woodside a compelling acquisition candidate:

| Asset | Location | Strategic Value |

|---|---|---|

| Scarborough Gas Project | Offshore Western Australia | Major LNG export growth driver into next decade |

| Browse Gas Project | Offshore Western Australia | Long-dated reserve base; equity recently increased |

| U.S. Gulf Coast LNG Project | Louisiana, United States | Atlantic Basin supply access; targeting 2029 start |

| Bass Strait (JV with ExxonMobil) | Southeast Australia | Existing relationship; Woodside assumed operatorship in 2025 |

| Asian offtake agreements | South Korea and Japan | Contracted demand from two of the world's top LNG import markets |

Each element addresses a different dimension of what a would-be acquirer needs. The Scarborough and Browse projects extend production runway well into the 2030s, providing the long-dated reserve base that justifies a premium acquisition price. The U.S. Gulf Coast facility, expected to begin operations by 2029, adds something rarer still: the ability to supply both Pacific Basin and Atlantic Basin customers from geographically separated production hubs.

For a company with existing deep operational infrastructure across the U.S. Gulf of Mexico, absorbing a U.S.-based LNG facility involves meaningfully lower integration risk than greenfield development, which typically carries a 10 to 15-year development timeline and significant capital exposure in a volatile regulatory environment.

The pre-existing contractual relationships with buyers in South Korea and Japan deserve particular attention. These are not speculative demand projections. They are established commercial agreements with two of the world's largest LNG importing nations, representing a commercial moat that would take years to develop through organic market entry.

The Pioneer Acquisition Logic and What Came Next

How $60 Billion in Permian Shale Created an LNG Blind Spot

ExxonMobil's $60 billion acquisition of Pioneer Natural Resources, completed in 2024, followed internally coherent strategic logic: consolidate low-cost, high-volume U.S. shale production to generate the sustained cash flows needed to fund longer-cycle international growth. In Permian Basin terms, the Pioneer deal was transformative.

In LNG terms, it left ExxonMobil's international gas position essentially unchanged. The Pioneer transaction delivered scale in a domestic shale play. It did not deliver geographic diversification, LNG commercialisation infrastructure, or contracted access to Asian demand. As those deficiencies became more visible against the backdrop of accelerating LNG competition from Shell and TotalEnergies, the imperative to address them grew correspondingly more urgent. Furthermore, U.S. energy policy shifts under the current administration have added an additional layer of complexity to domestic growth strategies, reinforcing the case for international diversification.

A potential Woodside transaction would deliver precisely what Pioneer could not:

- Geographic diversification across two hemispheres and two LNG supply basins

- Established Asian customer relationships providing immediate commercial relevance in the world's fastest-growing gas demand region

- Advanced development projects with defined timelines and existing regulatory approvals

- An existing joint venture relationship that reduces integration risk compared to a cold acquisition

Comparing the Available Options in Australian LNG

ExxonMobil's apparent focus on Australian LNG assets reflects a logical assessment of the available acquisition landscape. The realistic alternatives are limited:

-

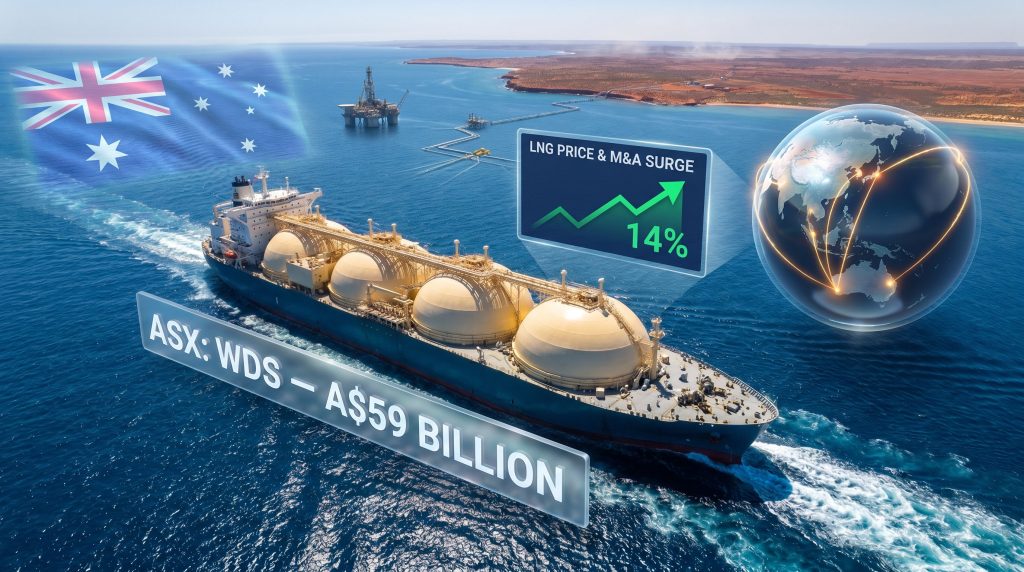

Woodside Energy (ASX: WDS): Market capitalisation of approximately A$59 billion (roughly US$42 billion) as of mid-2026; Australia's premier LNG exporter with a comprehensive multi-project development pipeline and established Asian customer base. Woodside's American depositary receipts surged as much as 14% in New York trading following initial reports of ExxonMobil's evaluation.

-

Santos Ltd.: The most frequently cited alternative for companies seeking Australian LNG exposure. Santos has attracted repeated acquisition interest, including a consortium bid linked to ADNOC that ultimately did not proceed. However, Santos is generally considered a smaller and less strategically comprehensive platform than Woodside.

-

Greenfield LNG development: Theoretically possible but practically unattractive. Development timelines of 10 to 15 years, combined with permitting complexity and capital risk, make organic LNG growth an insufficient response to the accelerated strategic timeline created by the Hormuz disruption.

The contrast between options one and three is particularly instructive. Woodside offers something no greenfield programme can: immediate access to producing assets, contracted demand, and development projects already through the most difficult early-stage regulatory and engineering phases.

The Strait of Hormuz Disruption as Strategic Catalyst

Why Australian LNG Carries a Geographic Premium

The partial closure of the Strait of Hormuz following the outbreak of conflict involving Iran in late February 2026 removed a substantial volume of LNG from accessible global supply for energy-importing nations in Northeast Asia. For Japan and South Korea, both of which historically sourced significant portions of their LNG imports from Middle Eastern producers whose shipments transited the strait, the disruption created immediate pressure to diversify toward Pacific Basin and Atlantic Basin producers.

Australian LNG exports travel via Indian Ocean and Pacific shipping routes that entirely bypass the Strait of Hormuz, making them structurally immune to supply disruptions originating in the Persian Gulf. This geographic advantage has materially elevated the strategic value placed on Australian LNG assets by both buyers and potential acquirers in the current environment. Consequently, commodity market volatility has amplified the urgency with which major energy companies are reassessing their portfolio exposures.

The Hormuz disruption did not create ExxonMobil's LNG strategy gap. It made that gap impossible to defer addressing.

How Supply Shocks Drive M&A Cycles in Energy Markets

Historical patterns in energy sector consolidation consistently demonstrate that major geopolitical supply disruptions accelerate M&A activity among large integrated companies. The sequence typically unfolds across four distinct phases:

-

Immediate Phase: Spot LNG prices spike sharply as buyers scramble to secure emergency supply from alternative sources, often paying significant premiums above long-term contract rates.

-

Medium-Term Phase: Long-term contract negotiations intensify as buyers shift their priority from price optimisation to supply security, accepting less favourable commercial terms in exchange for reliability guarantees.

-

Strategic Phase: Energy majors identify acquisition targets that provide structural supply advantages independent of short-term price movements, triggering M&A evaluation cycles at the corporate strategy level.

-

Consolidation Phase: Transactions are executed, reshaping competitive dynamics across global LNG markets for the following decade.

Based on the reported timing of ExxonMobil's internal deliberations, the current environment appears to sit at the transition between phases two and three, with strategic evaluation underway but formal deal mechanics not yet initiated.

Regulatory Complexity and the Australian Approval Landscape

What FIRB Review Would Mean for a Transaction of This Scale

Any foreign acquisition of Woodside Energy at the scale being contemplated would trigger mandatory review under Australia's Foreign Investment Review Board framework. Given Woodside's status as the country's largest LNG exporter and a critical component of national energy infrastructure, regulatory scrutiny would be substantial and multi-dimensional.

The Australian government has previously demonstrated a willingness to impose national interest conditions on major energy sector transactions, including requirements relating to domestic supply obligations, employment conditions, and asset management. A transaction involving a company of Woodside's strategic importance would almost certainly receive full FIRB scrutiny, with conditions likely addressing several specific areas:

-

Western Australian domestic gas reservation policy: State-level policy requires LNG exporters to set aside a defined proportion of production for domestic consumption. Any new ownership structure would inherit this obligation without modification.

-

Scarborough Project partner agreements: A change in Woodside's corporate ownership would require careful management of existing project partnership agreements and any associated regulatory approvals that are ownership-conditional.

-

Browse Project stakeholder considerations: The Browse development carries complex stakeholder dynamics, including Indigenous land rights considerations, that would need to be actively managed through any ownership transition.

Beyond FIRB, additional regulatory considerations would include competition assessments across relevant LNG markets, shareholder approval processes in both Australia and the United States, and potential conditions arising from the existing Bass Strait joint venture structure. In addition, geopolitical trade tensions between major economies may further complicate cross-border deal approvals at a regulatory level.

Leadership Timing and Governance Complexity

The potential acquisition approach arrives at a particularly sensitive moment in Woodside's corporate governance cycle. Liz Westcott assumed the role of Chief Executive Officer in 2026, following the departure of Meg O'Neill to lead bp. Incoming chief executives typically seek operational stability during their initial months in the role before engaging with transformative corporate events, and a major acquisition approach during this transition period introduces additional governance complexity for both the target and potential acquirer.

For ExxonMobil, the timing also carries implications for deal execution. A CEO transition at the target company can complicate due diligence processes, slow decision-making timelines, and introduce uncertainty around management retention that affects post-acquisition integration planning.

The Pre-Existing Woodside-ExxonMobil Relationship

Why Bass Strait Changes the Integration Calculus

One dimension of this potential transaction that receives less analytical attention than it deserves is the pre-existing operational relationship between ExxonMobil and Woodside. The two companies are already joint venture partners in the Bass Strait project, located off southeastern Australia. As Woodside's official announcement confirms, Woodside transitioned into the operator role at Bass Strait in 2025, while the equity interests of both parties remained unchanged.

This operational familiarity is commercially significant for several reasons. M&A practitioners consistently identify integration complexity as one of the most decisive determinants of post-acquisition value creation in the energy sector. Companies that acquire businesses with which they have no prior operational relationship face substantially higher integration costs, longer transition timelines, and greater risk of personnel and knowledge loss during the consolidation period.

For ExxonMobil, acquiring Woodside would not mean integrating an entirely unfamiliar organisation. The companies share established working relationships at the project level, mutual understanding of operational standards, and a history of constructive commercial interaction. That prior relationship does not eliminate integration risk, but it meaningfully reduces the uncertainty premium that markets typically apply to large-scale cross-border energy sector transactions.

It is also worth noting that ExxonMobil previously divested its 50% interest in the WA-1-R block, which encompasses the Scarborough gas field, to Woodside in a transaction valued at US$444 million plus a contingent payment of up to US$300 million tied to a final investment decision. This prior asset-level transaction creates additional commercial familiarity around one of Woodside's most strategically significant development assets. Furthermore, the North West Shelf extension represents yet another layer of strategic context underpinning Woodside's long-term production outlook.

The next major ASX story will hit our subscribers first

Strategic Scenario Analysis: Three Possible Outcomes

With deliberations reported to be at a preliminary, internal stage, the range of possible outcomes remains wide. Three distinct scenarios warrant serious consideration:

Scenario 1: Full Corporate Acquisition

ExxonMobil tables a formal offer at a premium to Woodside's market capitalisation of approximately A$59 billion, successfully navigates FIRB review and shareholder approval processes in both countries, and completes a transaction that creates one of the world's largest integrated LNG operators. The combined entity would possess production assets spanning Australia, the U.S. Gulf Coast, and ExxonMobil's existing international positions, with contracted access to two of the world's largest LNG import markets. Estimated timeline from formal offer to completion: 12 to 24 months.

Scenario 2: Targeted Asset Transaction

Rather than pursuing a full corporate takeover, ExxonMobil negotiates to acquire a stake in specific Woodside assets, most likely an interest in the U.S. Gulf Coast LNG project or an increased position in one of the Australian development projects. This approach substantially reduces regulatory complexity and total capital commitment while still advancing ExxonMobil's LNG diversification strategy. It would also avoid the governance complications associated with a full corporate transaction during Woodside's CEO transition period.

Scenario 3: Deliberations Conclude Without a Transaction

Preliminary evaluations determine that deal economics, regulatory friction, integration complexity, or capital allocation priorities do not justify proceeding. ExxonMobil pursues alternative LNG growth pathways through partnership arrangements, greenfield participation, or acquisition of a non-Australian LNG asset in a different jurisdiction.

Disclaimer: The preliminary nature of current deliberations means Scenario 3 carries meaningful probability. Energy sector M&A evaluations at this stage historically convert to completed transactions at a rate well below 50%, based on patterns of deal activity among supermajors over the past two decades. Nothing in the current reporting constitutes confirmation of a transaction, and investors should not treat speculative M&A coverage as a reliable indicator of deal completion.

What This Situation Reveals About the Broader LNG Investment Landscape

The reported interest in a potential Exxon acquisition of Woodside Energy is not simply a story about two companies. It reflects deeper structural forces reshaping global energy markets in ways that will influence capital allocation, supply security strategy, and LNG pricing dynamics for years to come.

Several broader themes emerge from this situation:

-

LNG is becoming the primary strategic battleground for energy majors seeking long-term relevance in a world where Asian gas demand continues to grow while domestic policy environments in many markets tighten around fossil fuel development.

-

Geopolitical supply shocks are compressing strategic timelines in ways that make multi-year deliberation cycles commercially unaffordable. The Hormuz disruption did not create ExxonMobil's LNG gap; it simply made that gap impossible to address on a gradual organic timeline.

-

The scarcity of large, integrated LNG platforms available for acquisition is itself a strategic dynamic. With Woodside and Santos representing essentially the full menu of Australian LNG acquisition candidates, competition among potential acquirers could ultimately support transaction valuations above what fundamental asset values alone would suggest.

-

Established Asian customer relationships carry increasing strategic premium as buyer nations shift from price-focused procurement to security-focused procurement, making contracted demand relationships more durable and commercially valuable than historical pricing models reflect.

-

Integration risk reduction through prior relationships will become an increasingly important factor in M&A evaluation as deals grow larger and more complex, favouring acquirers who have existing operational knowledge of their targets.

As industry analysis from the AFR highlights, Woodside's strengthened operational position across Australian gas infrastructure further underscores why it has emerged as a focal point for international strategic interest. The coming months will determine whether ExxonMobil's internal deliberations advance to a formal approach. What is already clear is that the strategic logic driving those deliberations reflects some of the most consequential forces reshaping the global energy landscape, and the outcome will matter well beyond the balance sheets of the two companies involved.

Want to Stay Ahead of Major Resource Discoveries Before the Broader Market?

While ExxonMobil's reported interest in Woodside Energy reflects the growing premium placed on strategic resource assets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they are announced — explore historic examples of exceptional returns to understand what early positioning can mean, and begin your 14-day free trial at Discovery Alert to secure your market-leading edge.