May 12, 2026

When the World's Second-Largest Copper Mine Goes Quiet, Markets Pay Attention

Underground block cave mining is one of the most productive and operationally demanding extraction methods ever developed. It relies on precise geological control, carefully calibrated ore draw sequencing, and infrastructure networks that stretch kilometres beneath the earth's surface. When a system of this complexity encounters a catastrophic wet material event, the resulting disruption does not resolve in weeks.

It resolves in years, and the consequences radiate well beyond a single company's balance sheet into the global supply chains that modern industrial economies depend upon.

The Freeport Grasberg mine recovery 2027 forecast has become one of the most closely watched operational commitments in the global copper market, carrying implications not just for Freeport-McMoRan shareholders but for every downstream industry that depends on reliable copper supply at scale.

When big ASX news breaks, our subscribers know first

Understanding What Happened at Grasberg: The September 2025 Mud Flow Explained

On September 8, 2025, approximately 800,000 tonnes of saturated wet material collapsed into the Grasberg Block Cave (GBC) underground section, killing seven workers and triggering an immediate operational halt across the entire complex. The scale of the event was sufficient to warrant a formal force majeure declaration, pausing contractual obligations and initiating insurance claim processes expected to offset approximately $1 billion in operational losses.

The term "mud flow" or "wet material collapse" understates the engineering complexity of what occurred. In underground block cave operations, ore zones are accessed through networks of draw points, ore passes, and production drives carved into rock at multiple levels below the surface. When highly saturated material enters these confined spaces, the damage extends across tunnels, support structures, ore handling equipment, and ventilation systems simultaneously.

Production across the full Grasberg complex stopped for nearly a month. The two unaffected zones within the broader complex, the Deep Mill Level Zone (MLZ) and the Big Gossan mine, were restarted in late 2025 and have been driving the baseline operational output since. GBC itself underwent partial reopening focused exclusively on production zones that sustained no direct impact from the wet material event.

Why Grasberg's Operational Architecture Made This Disruption Unusually Complex

The Grasberg complex is not a single mine. It is an integrated cluster of underground operations drawing from the same extraordinary orebody in Papua, Indonesia. The orebody contains copper, gold, and silver in concentrations that make it globally significant for all three metals simultaneously. The GBC represents the primary production engine within this complex, and Production Block 1 within GBC was the specific zone that sustained the direct structural impact in September 2025.

Block caving, the extraction method used at GBC, works by undercutting an ore column and allowing controlled cave propagation under gravity. Draw points at the cave base extract fragmented ore in carefully sequenced ratios to prevent uneven caving behaviour, dilution events, or the kind of wet material infiltration that occurred in September 2025. Restoring this system after a major structural incident is not a linear repair process.

It requires mud removal, rock mass characterisation, draw point reconstruction, and staged restart with continuous stability monitoring before normal extraction can resume. This technical reality explains the extended timeline that markets have been grappling with throughout 2025 and 2026. Furthermore, the global copper supply gap created by this disruption adds considerable urgency to every milestone update Freeport releases.

Current Operational Status as of Mid-2026: What 40-50% Capacity Actually Means

Freeport-McMoRan confirmed that Grasberg was operating at approximately 40-50% of its total pre-incident capacity as of May 2026. That figure requires context to interpret accurately.

The 40-50% baseline does not represent a damaged version of the full mine running at half efficiency. It represents the MLZ and Big Gossan mines operating at full utilisation, supplemented by whatever output GBC's undamaged zones can contribute. These are structurally separate production streams within the same complex, meaning the baseline output is genuine rather than degraded throughput. The ceiling, however, is capped by the ongoing GBC Block 1 unavailability.

Logistics infrastructure and ore handling systems have also undergone significant upgrades during this period. Conveyor systems, dewatering capacity, processing plant configurations, and ore transport networks have all been modified to support the phased production ramp-up, meaning the infrastructure entering the recovery phase is in some respects better positioned than the pre-incident baseline.

Freeport's deliberate choice to maintain a phased recovery rather than attempting a full immediate restart reflects both safety obligations following a fatal incident and the engineering reality that block cave restart sequencing must follow geological validation, not commercial timelines.

How the 2026 Production Guidance Was Rebuilt From the Ground Up

The financial impact of the September 2025 incident on Freeport's annual production guidance was substantial and multi-dimensional. The following table illustrates the scope of the revision:

| Metric | Pre-Incident Forecast | Revised 2026 Guidance | Change |

|---|---|---|---|

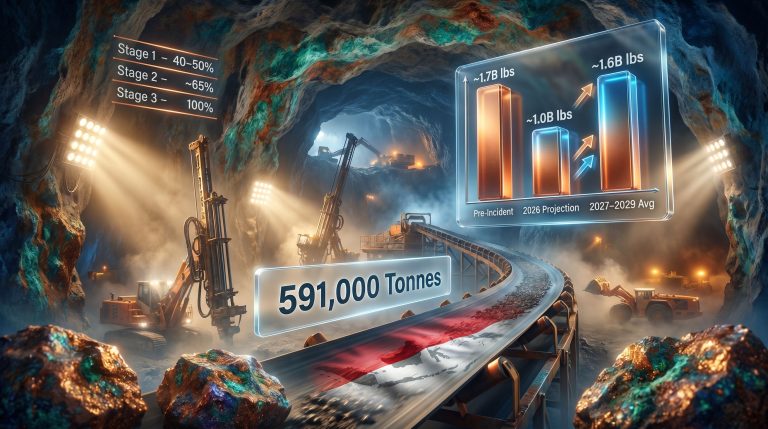

| Copper Output | ~1.7 billion lbs | ~1.1 billion lbs | Down approximately 35% |

| Gold Output | ~1.6 million oz | Materially reduced | Significant decline |

| Q4 2025 Sales | 445M lbs Cu / 345K oz Au | Described as "insignificant" | Near-total production loss |

| Cumulative Cu Supply Loss (through 2026) | Not applicable | ~591,000 tonnes | Critical structural gap |

The Q4 2025 production characterisation as "insignificant" reflects the timing of the September incident against Freeport's strongest sequential quarter, compounding the annual guidance impact.

More significant from a market signalling perspective was the late April 2026 revision of Freeport's second-half 2026 recovery target. On April 23, 2026, in connection with its quarterly earnings release, Freeport downgraded the H2 2026 production recovery target from 85% of full capacity to 65%. The revision reflected the complexity of GBC Block 1 structural repairs, specifically the extended timelines required to safely restore draw point infrastructure and rock mass stability in the affected production zones.

Freeport subsequently filed a regulatory update with U.S. securities authorities confirming that the end-2027 full recovery timeline remained intact, establishing a formal compliance baseline for market guidance. In addition, understanding the broader copper price drivers at play helps contextualise why this guidance update generated significant market attention.

The 591,000-Tonne Supply Gap: A Number That Matters Beyond Freeport's Balance Sheet

Grasberg contributes approximately 5% of total global copper production on an annualised basis. At that scale, the cumulative copper supply loss estimated at approximately 591,000 tonnes through the end of 2026 represents a structural market deficit that cannot be rapidly offset by alternative producers. New copper mine development requires 10 to 20 years from discovery to production.

Existing operations cannot simply scale up output to absorb a 591,000-tonne shortfall without significant capital investment and timeline commitments of their own. The copper supply crunch building across global markets is consequently sharpened by every month of delayed Grasberg recovery.

This supply arithmetic sits alongside an accelerating demand backdrop driven by:

- Electric vehicle battery systems and charging network infrastructure requiring extensive copper wiring

- Grid-scale renewable energy deployment, where wind and solar installations use between two and five times more copper per megawatt than conventional power generation

- Data centre and AI infrastructure buildout, with high-density computing facilities requiring substantial copper for power distribution and thermal management

- Urbanisation in emerging markets continuing to drive baseline infrastructure copper consumption

The convergence of structural supply disruption with rising secular demand is the central dynamic amplifying market sensitivity to every Grasberg recovery timeline announcement.

The May 2026 Communication Divergence: When Two Spokespeople Created a Market Event

In May 2026, the Indonesian head of PT Freeport Indonesia publicly indicated that full production restart could extend into 2028, a statement that departed from Freeport-McMoRan's April 23 guidance of end-2027 full recovery. The market reaction was immediate and instructive.

Copper prices climbed to a three-month high, and Freeport-McMoRan shares rose 5% to $64.75 in a single trading session. Markets interpreted the PT Freeport Indonesia commentary as a new development rather than recognising it as a more conservative version of information already disclosed in Freeport's formal quarterly earnings. According to Reuters reporting, the production adjustment announcement prompted immediate scrutiny of Freeport's official timeline commitments.

Freeport's Phoenix headquarters responded by clarifying that the April 23 earnings release already contained the revised mine plan and that media coverage was presenting already-disclosed information as new developments. A company spokesperson indicated that any material delay beyond the disclosed timeline would trigger immediate market notification under securities disclosure obligations, effectively drawing a compliance boundary around the 2027 guidance.

Freeport filed a quarterly update with U.S. regulators on the Friday prior reiterating the 2027 recovery timeline, and CEO Kathleen Quirk was scheduled to address Grasberg operations at the Bank of America Global Metals, Mining and Steel Conference the following Tuesday.

The May 2026 market reaction revealed something important about investor behaviour in complex mining situations: when dual governance structures produce conflicting public statements, markets default to pricing the more pessimistic scenario first and verifying accuracy second. The copper price move and Freeport share price gain both reversed partially once the April disclosure context was re-established.

Why the Phoenix-Jakarta Communication Gap Is a Structural Feature, Not a Failure

Understanding why conflicting statements emerged from the same mine requires understanding the ownership structure of PT Freeport Indonesia.

Indonesian government entities hold a 51.24% controlling stake in PT Freeport Indonesia, while Freeport-McMoRan retains a 48.76% minority stake but manages all mine operations through a contractual arrangement from its Phoenix, Arizona headquarters. This creates a dual-authority operating environment where local management may reflect national policy priorities, operational conservatism, or community relations considerations that differ from the investor-facing guidance framework.

PT Freeport Indonesia's local leadership operates within a sovereign stakeholder framework that prioritises worker safety, community relations, and Indonesian government communication protocols. These priorities may generate more conservative operational timelines than the committed guidance Freeport-McMoRan's securities law obligations require. The May 2026 discrepancy reflects this structural tension rather than any fundamental disagreement about the mine's physical recovery trajectory.

For investors monitoring the Freeport Grasberg mine recovery 2027 forecast, the authoritative information source is Freeport's formal SEC filings and earnings releases. Statements from PT Freeport Indonesia's local management, while operationally informed, reflect a different governance context and should not be treated as revisions to formal investor guidance.

The Phased Recovery Roadmap: Stage-by-Stage Production Restoration

Freeport's recovery plan for Grasberg follows four distinct stages, each tied to specific engineering milestones rather than calendar targets alone. Understanding what each stage represents physically helps interpret timeline revisions when they occur.

Stage 1: Stabilisation (Q4 2025 to Q2 2026)

Force majeure period concluded with unaffected mines restarted. GBC partially reopened in undamaged production zones. Operating capacity established at 40-50%, representing the genuine output ceiling of non-GBC Block 1 production streams.

Stage 2: Structural Repair and Partial Ramp-Up (H2 2026)

GBC Production Block 1 active remediation underway. Ore handling and logistics infrastructure upgrades proceeding alongside underground repairs. Target production recovery reaches 65% of full capacity, revised downward from an initial 85% target due to extended Block 1 remediation requirements.

Stage 3: Accelerated Recovery (Early to Mid-2027)

GBC Block 1 repairs expected to reach completion by early 2027, enabling more rapid production increases as additional draw points and production zones return to service. Pre-incident extraction rates become achievable. Capacity target reaches 80%, reflecting Block 1 returning to standard operational parameters while final infrastructure commissioning continues.

Stage 4: Full Operational Restoration (End-2027 to Early 2028)

Complete GBC restart across all production blocks. Full logistics and processing capacity commissioned. 100% capacity target achieved, completing the return to pre-incident production baseline.

The difference between the "end-2027" official position and "early 2028" conservative commentary hinges primarily on the pace of GBC Block 1 structural repairs and ore handling system integration, two variables where geological uncertainty and engineering validation timelines create legitimate scenario divergence.

The next major ASX story will hit our subscribers first

Benchmarking Grasberg Against Historical Mine Disruptions

Context is useful when evaluating what the Grasberg recovery timeline means for long-term copper supply. The following table compares the 2025–2027 Grasberg event against notable historical mine disruptions:

| Mine | Disruption Type | Recovery Duration | Estimated Production Loss |

|---|---|---|---|

| Grasberg (2025-2027) | Underground wet material collapse | 24 to 30 months | ~591,000 tonnes Cu through 2026 |

| Escondida (2017) | Labour strike action | Approximately 6 weeks | ~200,000 tonnes Cu |

| Chuquicamata (2019 transition) | Open-pit to underground conversion | Multi-year managed transition | Planned production decline |

| Olympic Dam (periodic events) | Processing plant outages | Weeks to months | Moderate, event-specific |

The Grasberg event is distinguished from most comparable disruptions by its combination of fatal casualties, force majeure declaration, structural underground damage, complex dual-governance ownership, and an orebody where copper and gold production are jointly affected. This multi-dimensional complexity places it among the more operationally demanding mine recovery scenarios in recent copper market history.

Long-Term Strategic Significance: Grasberg's Role in the Copper Supply Decade

Beyond the immediate recovery mechanics, the Grasberg situation illuminates a broader structural reality in global copper markets. The pipeline of new copper projects capable of replacing production at Grasberg's scale is extremely thin. Greenfield copper discoveries of comparable grade and scale have become increasingly rare, while the average time from discovery to production has extended to between 16 and 20 years at major projects.

In early 2026, Freeport secured a life-of-resource extension agreement with the Indonesian government, providing operational certainty for the Grasberg complex well beyond the current recovery period. This agreement represents long-term tenure security for one of the few remaining high-grade, high-scale copper-gold operations with confirmed resources and established infrastructure globally. Furthermore, major copper expansion plans by other producers are unlikely to offset Grasberg's contribution within the critical supply window of the late 2020s.

Once fully restored, Grasberg's contribution to global copper supply will be critical in partially offsetting the structural deficit building across copper markets. The mine's significance is therefore not merely historical or financial. It is a forward-looking supply security question for every sector that depends on copper availability at scale. Decisions around copper project capital allocation across the broader industry are consequently being re-evaluated in light of this prolonged disruption.

Key Risk Factors That Could Affect the Official 2027 Recovery Target

Several variables could shift the recovery timeline in either direction, and investors should monitor each as Freeport progresses through its staged restoration plan:

- Geological risk: Additional instability in GBC underground workings, whether from seismic activity, groundwater infiltration, or unexpected rock mass behaviour during Block 1 remediation, could extend repair timelines beyond current engineering estimates

- Regulatory and governance risk: Indonesian government policy decisions affecting PT Freeport Indonesia's operational permissions, capital deployment approvals, or community relations requirements could introduce non-technical delays

- Infrastructure risk: Ore handling system upgrades, dewatering capacity installation, and processing plant modifications represent critical path dependencies where equipment procurement and commissioning timelines are sensitive to supply chain conditions

- Labour and community risk: Post-fatality safety culture reassessment, workforce availability constraints, and community relations management in Papua following the September 2025 incident may affect operational tempo at key recovery milestones

None of these factors has caused Freeport to formally revise its end-2027 full recovery commitment as of the most recent regulatory filings. However, the April 2026 downgrade from 85% to 65% for H2 production capacity demonstrates that timeline revisions, when warranted by engineering reality, are communicated promptly through formal channels.

Frequently Asked Questions: Grasberg Mine Recovery and the 2027 Timeline

When will Grasberg return to full production?

Freeport-McMoRan's official guidance, confirmed through U.S. securities regulatory filings, targets full production restoration by the end of 2027. More conservative operational commentary from PT Freeport Indonesia has referenced early 2028 as a possibility, though this has not been adopted as Freeport's formal investor-facing timeline. As Freeport has stated publicly, the company stands by its 2027 forecast despite alternate commentary from local management.

What caused the Grasberg mine shutdown in 2025?

A large-scale underground wet material collapse at the Grasberg Block Cave section on September 8, 2025, involving approximately 800,000 tonnes of saturated material, killed seven workers and forced operational suspension for approximately one month. Force majeure was formally declared shortly after the incident.

How much copper production has been lost due to the Grasberg disruption?

The cumulative copper supply loss attributable to the Grasberg disruption through the end of 2026 is estimated at approximately 591,000 tonnes, representing a roughly 35% reduction from Freeport's pre-incident annual guidance of approximately 1.7 billion pounds.

What is Freeport's current production capacity at Grasberg?

As of May 2026, Grasberg is operating at approximately 40-50% of full pre-incident capacity, with production sourced primarily from the Deep Mill Level Zone and Big Gossan mines while GBC Production Block 1 undergoes phased structural repairs.

How does Grasberg's disruption affect copper prices?

Grasberg supplies approximately 5% of global copper production annually. Any revision to its recovery timeline creates immediate supply-side price sensitivity in copper markets, as demonstrated when the May 2026 PT Freeport Indonesia commentary alone was sufficient to push copper prices to a three-month high.

Who controls the Grasberg mine?

PT Freeport Indonesia operates the mine, with Indonesian government entities holding a 51.24% majority stake and Freeport-McMoRan holding 48.76%. Freeport manages day-to-day operations from Phoenix, Arizona under a contractual management arrangement that has been extended through a life-of-resource agreement reached in early 2026.

This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities. Production forecasts, recovery timelines, and market projections involve inherent uncertainty. Readers should conduct independent research and consult qualified financial advisers before making investment decisions. Past operational performance does not guarantee future recovery outcomes. All figures referenced reflect publicly available information as reported through formal regulatory disclosures and media reporting attributed to Reuters and Kitco News.

Want to Track the Next Major Copper Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and translating complex data into actionable insights for investors at every experience level. Explore how historic mineral discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial to position ahead of the next major market-moving find.