June 21, 2026

The Architecture of Dependency: How Western Nations Lost Control of Critical Mineral Supply Chains

The story of Western vulnerability in critical minerals did not begin with a single policy failure or trade dispute. It unfolded across decades of rational-seeming commercial decisions, each one individually defensible, collectively catastrophic. Manufacturers outsourced processing to wherever it was cheapest. Governments allowed domestic refining capacity to atrophy. Investors avoided the long-horizon, capital-intensive projects that building competitive mineral supply chains demands. The result is a structural dependency that now sits at the intersection of clean energy ambition, defense readiness, and technological sovereignty.

Understanding the G7 critical minerals alliance against China requires first understanding how deep that dependency runs, and why undoing it will take far more than a summit declaration.

When big ASX news breaks, our subscribers know first

What China Actually Controls: Beyond the Mining Headlines

Public debate about China's mineral dominance tends to focus on mining, but the more strategically dangerous concentration lies further down the value chain. Any nation can discover a deposit. Processing it into usable materials, separating individual elements, and manufacturing the finished components that go into motors and turbines is where China's position becomes nearly unassailable.

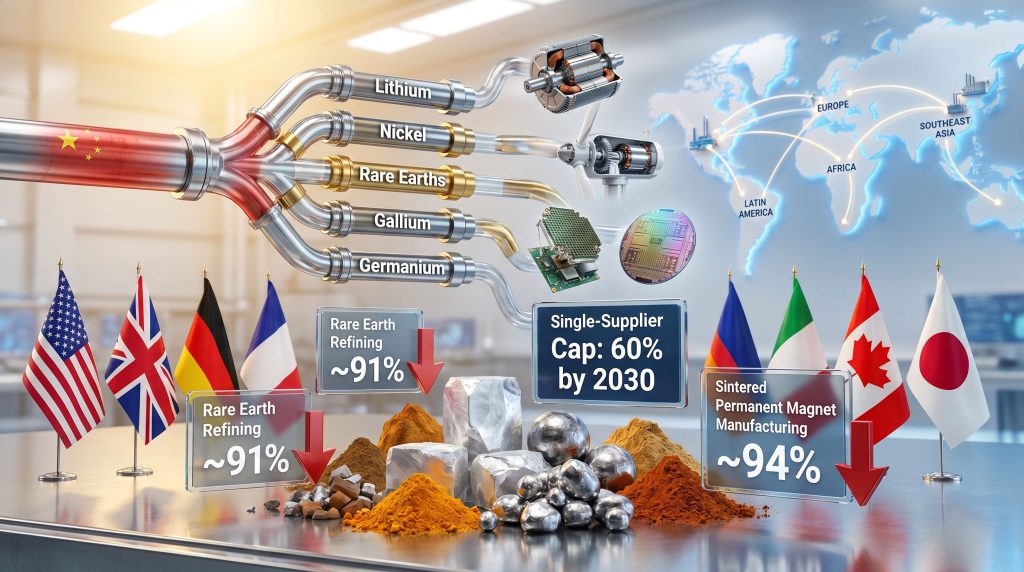

The International Energy Agency's analysis of 20 critical minerals found that China dominates refining across 19 of them, holding an average market share of approximately 70%. In rare earths specifically, the picture is starker still.

| Mineral / Processing Stage | China's Estimated Market Share |

|---|---|

| Rare Earth Mining | ~59% |

| Rare Earth Refining | ~91% |

| Sintered Permanent Magnet Manufacturing | ~94% |

| Critical Mineral Refining (avg. across 20 minerals) | ~70% |

Source: IEA Critical Minerals Market Review

The sintered permanent magnet figure deserves particular attention. These components are not niche industrial products. They are the physical heart of electric vehicle traction motors, direct-drive wind turbines, precision-guided munitions, submarine propulsion systems, industrial motors, and the high-efficiency motors that power data centres. Two decades ago, China accounted for roughly half of global sintered permanent magnet production. According to IEA estimates, that share has risen to approximately 94% today, representing one of the most dramatic consolidations of industrial capacity in modern economic history.

What makes this particularly difficult to reverse is the nature of the manufacturing knowledge involved. Producing high-performance neodymium-iron-boron (NdFeB) sintered magnets requires highly specific metallurgical expertise, precision sintering furnaces, and tightly controlled alloy compositions. The grade and consistency of the magnet directly determines the performance characteristics of the end product. Western manufacturers attempting to re-enter this space are not simply building factories; they are reconstructing an entire industrial knowledge base that eroded over two decades of offshoring.

The Export Control Lever: Economic Coercion as Policy Tool

China's dominance is not merely a function of market efficiency. A bipartisan investigation by the U.S. Congress' Select Committee on China concluded that Beijing has pursued a coordinated, multi-decade strategy to treat critical minerals as instruments of geopolitical leverage rather than conventional market commodities. Central to this strategy is a domestic legal framework governing mineral price reporting that effectively gives Chinese state authorities the ability to influence benchmark prices in ways that serve national economic and security objectives.

The practical consequences of this framework are visible in China's rare earth export restrictions used as a coercive instrument:

- Gallium and germanium restrictions imposed in mid-2023, targeting semiconductor and solar panel supply chains

- Graphite export licensing requirements introduced in late 2023, affecting EV battery anode material supply

- Rare earth magnet-related controls tightened progressively since 2023, targeting downstream manufacturers in Japan, South Korea, Europe, and the United States

- Antimony export restrictions introduced in 2024, affecting flame retardant and ammunition manufacturing

The dual-use classification is a particularly powerful instrument. When Beijing designates a mineral as having both civilian and military applications, it creates a legal basis for export restrictions that can simultaneously disrupt commercial supply chains and defence procurement while appearing consistent with international norms on controlled goods.

"China's ability to influence global rare earth benchmark prices through domestic regulatory mechanisms means that Western mining projects are not simply competing against Chinese producers on geology or operational efficiency. They are competing against a state-directed pricing apparatus that can move reference prices to undercut any commercial project that threatens Chinese market share."

The G7 Alliance: What Was Actually Agreed at Evian

At the G7 launch of the critical minerals alliance in Evian, France, in June 2026, leaders issued a formal declaration committing to coordinate efforts to build alternative processing and industrial capacity for critical minerals value chains. The declaration deliberately avoided naming China explicitly, instead referencing concerns about non-market policies, economic coercion, arbitrary export restrictions, and retaliatory measures on critical minerals and dual-use items.

The four structural pillars of the alliance are:

- Processing capacity development through coordinated investment and financing across member nations and partner countries

- Supply chain diversification with quantified concentration targets tied to specific timelines

- Strategic stockpiling in both industrial and public-sector reserves

- Data-sharing infrastructure enabling coordinated responses to supply disruptions and market stress signals

The quantified targets provide the most concrete measure of the alliance's ambition:

| Policy Target | Detail |

|---|---|

| Single-supplier concentration cap | Reduce to 60% by 2030 |

| Longer-term concentration goal | Below 50% as soon as practicable |

| Initial pilot minerals | Lithium and nickel |

| Annual expansion rate | Five additional minerals per year |

| Special priority category | Rare earths |

The IEA is designated as the coordinating platform for stockpiling alerts and market stress data, drawing on its established role in oil market coordination. Lithium and nickel were selected as initial pilot minerals partly because they have more geographically distributed upstream mining bases compared to rare earths, making near-term diversification more achievable and providing proof-of-concept before tackling the harder problem of the rare earth supply chain importance.

The diplomatic ambiguity around China's non-naming reflects a genuine tension within the G7. Germany, Japan, and other members with deep commercial exposure to Chinese markets have economic reasons to avoid language that formally designates China as an adversary. Whether this ambiguity undermines enforcement credibility or simply reflects pragmatic coalition management remains the central question surrounding the alliance's durability.

Why Previous Western Initiatives Failed to Shift the Dial

The G7 critical minerals alliance against China is not the first multilateral effort to address supply concentration. A clear-eyed assessment of prior initiatives reveals a consistent pattern: ambitious announcements followed by financing gaps, permitting bottlenecks, and the slow attrition of political attention.

- The Minerals Security Partnership (MSP), launched in 2022, brought together the United States, European Union, Japan, South Korea, Australia, and others to accelerate investment in critical mineral supply chains. Despite high-level backing, IEA data indicates that China's market share in critical mineral processing continued to increase in the years following its launch.

- The EU Critical Raw Materials Act, which came into force in 2024, set targets for domestic extraction, processing, and recycling of strategic minerals. Implementation has proven slower than anticipated, constrained by permitting timelines that can stretch to a decade or more in European jurisdictions.

- U.S. Inflation Reduction Act domestic content requirements created incentives for non-Chinese mineral sourcing but encountered immediate supply chain reality: the processing capacity and qualified supply simply did not exist at the volumes required, forcing regulators to extend phase-in timelines.

Furthermore, according to IEA analysis published in 2025, critical minerals demand surge pressures are intensifying even as concentration is increasing rather than decreasing, making the urgency of the G7 alliance's execution timeline the defining variable in its relevance.

What potentially distinguishes the 2026 G7 alliance from its predecessors is the combination of a leader-level multilateral commitment, the inclusion of novel price floor mechanisms, and the explicit involvement of multilateral development banks in financing architecture. Whether these structural differences translate into actual capacity building remains to be demonstrated.

The Rare Earth Price Floor: A New Instrument for an Old Problem

Among the most technically significant elements of the allied response is the U.S.-led proposal to establish a minimum price mechanism for rare earth elements across allied markets. Understanding why this matters requires understanding the economics of rare earth project development.

A rare earth mining and processing project typically requires between 10 and 15 years from initial exploration to sustained commercial production. Capital requirements for a fully integrated facility covering mining, hydrometallurgical separation, and downstream alloy or magnet production can run into multiple billions of dollars. The commercial viability of any such project depends critically on the projected long-term price of the rare earth elements it will produce.

China has a documented history of flooding markets with subsidised rare earth supply during periods when Western projects approach commercial viability, suppressing prices below the threshold at which outside investment remains rational. This price suppression trap has derailed multiple non-Chinese rare earth development efforts over the past three decades.

A price floor mechanism would establish a guaranteed minimum price within allied procurement channels, providing the long-term price certainty that project finance requires. However, the conceptual precedent that exists in agricultural commodity support programmes raises distinct challenges when applied to industrial minerals:

- WTO compatibility questions around whether minimum price guarantees constitute prohibited subsidies

- Consensus challenges among allied nations with different industrial structures and fiscal positions

- Moral hazard risks if guaranteed prices reduce competitive discipline among allied producers

- Market distortion effects if floor prices are set too far above marginal cost

The agricultural analogy is instructive but imperfect. Rare earth elements are not storable commodities with annual production cycles. They are intermediate industrial inputs whose pricing dynamics interact with downstream manufacturing decisions in complex ways. Getting the mechanism design right is a substantially harder problem than the headline concept suggests.

Sector Vulnerability: Who Bears the Most Risk?

Supply concentration risk is not evenly distributed across industrial sectors. The exposure profile varies depending on which specific minerals are involved, how much flexibility exists in substitution, and how deep existing inventory positions run.

| Sector | Key Mineral Dependencies | Substitution Difficulty |

|---|---|---|

| Electric Vehicles | NdFeB magnets (traction motors), lithium (cathodes) | High for magnets, moderate for lithium |

| Wind Energy | NdFeB magnets (direct-drive turbines), dysprosium (heat resistance) | High |

| Defense Systems | Rare earths across guidance, propulsion, radar | Very high |

| Semiconductor/AI Hardware | Gallium, germanium, indium | High |

| Industrial Motors and Data Centers | NdFeB sintered magnets | High |

A detail often overlooked in mainstream coverage is the role of dysprosium as a heavy rare earth element added to NdFeB magnets specifically to preserve their magnetic performance at elevated operating temperatures. Without adequate dysprosium content, EV traction motor magnets demagnetise under the thermal loads generated during hard acceleration or regenerative braking. China's dominance in heavy rare earth supply creates a second-order vulnerability within the already concentrated rare earth supply chain.

Defence applications compound the strategic risk further. When the same upstream mineral source supplies both commercial EV manufacturers and military precision guidance systems, any supply disruption creates simultaneous pressure across civilian and defence procurement. The inability to segregate supply chains by end-use sector means that commercial export controls automatically have defence implications, and vice versa. Consequently, the link between critical minerals and energy security extends well beyond clean energy infrastructure into national defence readiness.

The next major ASX story will hit our subscribers first

The Capital and Timeline Gap: Industrial Reality vs. Political Urgency

Perhaps the most important dimension of the G7 critical minerals alliance against China that summit communiqués tend to understate is the sheer scale of the capital formation challenge. Building competitive processing capacity outside China across the key rare earth and magnet manufacturing stages is not a question of years. It is a question of decades and hundreds of billions of dollars in coordinated investment.

The processing bottleneck is particularly acute because mining project development, while lengthy and expensive, is relatively well-understood by capital markets. In addition, the rare earth processing challenges involved in separation and alloy manufacturing are not. Rare earth separation facilities require sophisticated solvent extraction circuits, management of radioactive thorium and uranium byproducts in many ore types, highly trained chemical engineering workforces, and continuous process optimisation that takes years to master.

The financing architecture being developed under the G7 framework draws on several instruments:

- Multilateral development bank lending from institutions including the World Bank, Asian Development Bank, and European Bank for Reconstruction and Development to de-risk capital-intensive projects in jurisdictions with adequate geology but insufficient commercial returns

- Export credit agency guarantees from agencies such as the U.S. Export-Import Bank, UK Export Finance, and their counterparts, enabling project finance at lower cost of capital than purely commercial markets would permit

- Allied procurement commitments that underwrite long-term offtake agreements, providing the revenue certainty that project lenders require to reach financial close

- Private capital mobilisation through blended finance structures that bring institutional investors into projects that would not otherwise meet their return thresholds on a standalone basis

Three Scenarios for the Alliance's Trajectory

The following scenarios are speculative projections based on current trends and policy commitments. They should not be treated as forecasts or investment guidance.

Scenario A: Accelerated Execution

Allied financing mechanisms reach operational scale by 2027 to 2028. Price floor mechanisms for rare earths attract private capital into non-Chinese processing facilities. By 2030, the 60% single-supplier concentration cap is within reach for lithium and nickel, while rare earth refining concentration falls from 91% to the mid-70s. This scenario requires sustained political cohesion, successful mechanism design, and no major geopolitical fractures within the G7.

Scenario B: Partial Diversification

Progress is made in lithium and nickel, driven by the relatively distributed nature of upstream mining resources. However, rare earth processing concentration remains above 75% through 2035 due to the combined effect of timeline constraints, dysprosium supply limitations, and the difficulty of replicating Chinese magnet manufacturing expertise at competitive cost. This is arguably the base case given historical precedent.

Scenario C: Institutional Stall

Geopolitical consensus within the G7 fractures under the pressure of bilateral trade negotiations with China. Financing commitments are made but not deployed at scale. China continues to deepen vertical integration in Africa and Latin America through Belt and Road mineral infrastructure investment, locking in long-term supply relationships. Western concentration exposure worsens through 2030.

The metrics that will provide the clearest early signal of which scenario is materialising include the annual change in China's share of global rare earth refining capacity, the volume of allied processing capacity brought online per year, and the actual deployment rate of multilateral financing instruments into qualifying projects. For further context on how the G7 is balancing coordination and competition, this analysis from The National News offers useful additional perspective.

Frequently Asked Questions: G7 Critical Minerals Alliance

What minerals does the G7 alliance initially cover?

The alliance begins with lithium and nickel as pilot minerals, adding approximately five additional minerals per year. Rare earths are designated as a priority category due to their extreme supply concentration.

What is the G7's single-supplier concentration target?

The alliance targets reducing dependence on any single supplier nation to no more than 60% of supply by 2030, with a longer-term ambition to bring that figure below 50%.

Why doesn't the declaration name China explicitly?

The declaration references non-market practices, economic coercion, and arbitrary export restrictions without identifying specific nations. This reflects the need to maintain consensus among G7 members with varying degrees of commercial exposure to China.

What is a rare earth price floor mechanism?

A minimum guaranteed price within allied procurement channels that protects Western mining and processing projects from being commercially undermined by subsidised Chinese supply. It is designed to provide the long-term price certainty that project finance for capital-intensive rare earth facilities requires.

Why is rare earth magnet manufacturing so difficult to replicate?

Producing high-performance sintered NdFeB magnets requires specialised metallurgical expertise, precision manufacturing infrastructure, and tightly controlled alloy compositions including heavy rare earth additions such as dysprosium. This knowledge base eroded significantly in Western countries over two decades of offshoring and cannot be reconstituted quickly through financial investment alone.

Has G7-level coordination on critical minerals been attempted before?

Prior initiatives including the Minerals Security Partnership and various bilateral agreements have sought similar goals. IEA data indicates that China's market share in critical mineral processing continued to rise despite these efforts, making the execution design of the current alliance more important than the existence of the commitment itself. Indeed, discussions on Reddit's critical mineral stocks community reflect broad scepticism about whether this iteration will prove any different.

This article is intended for informational purposes only and does not constitute financial or investment advice. Scenario projections and forward-looking statements involve material uncertainty and should not be relied upon as predictions of future outcomes. Readers seeking primary source data on critical mineral supply chain dynamics are encouraged to consult the IEA's Critical Minerals Market Review series at iea.org.

Want to Track ASX Mineral Discoveries Before the Market Moves?

As Western nations race to secure alternative critical mineral supply chains, the exploration opportunities emerging across the ASX represent a significant and fast-moving investment landscape — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across more than 30 commodities and delivering actionable alerts to subscribers ahead of the broader market. Explore historic discoveries and their returns to understand the scale of opportunity, then begin a 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.