June 2, 2026

Australia's energy sector faces mounting pressure as experts warn of a potential gas supply shortfall that could significantly impact winter heating demands and industrial operations. The complex interplay between export commitments, domestic consumption patterns, and infrastructure limitations has created a challenging environment for energy planners and consumers alike. Furthermore, recent geopolitical tensions and supply chain disruptions have amplified concerns about energy security across the region.

What Are the Primary Drivers Behind Current Global Gas Supply Shortfalls?

Geopolitical Disruptions and Infrastructure Vulnerabilities

Middle East conflicts have emerged as a critical factor disrupting global liquefied natural gas flows through strategic shipping corridors. The ongoing tensions involving Iran have created bottlenecks in Persian Gulf routes, where a significant portion of global LNG transit occurs. These disruptions extend beyond immediate regional impacts, cascading through international supply chains and affecting markets thousands of miles away from the conflict zones.

Pipeline capacity constraints compound these challenges by limiting regional distribution networks' ability to reroute supplies efficiently. When primary transport routes face disruption, alternative pathways often lack sufficient capacity to compensate fully, creating localised shortages even when global production remains stable.

Strategic reserve depletion following extreme weather events has further strained the system's resilience. Many regions experienced inventory drawdowns during recent severe weather periods, leaving storage levels below optimal thresholds as demand recovery accelerated.

Demand-Supply Imbalance Fundamentals

Post-winter inventory recovery challenges plague major consuming regions as they struggle to rebuild stockpiles before peak summer demand arrives. This seasonal timing mismatch creates structural market tightness, particularly when combined with supply disruptions.

Industrial demand growth continues outpacing production capacity expansions across multiple sectors. Manufacturing facilities, data centres, and other energy-intensive operations have maintained robust demand growth, while new production capacity comes online more slowly than anticipated.

Seasonal consumption patterns reveal deeper structural vulnerabilities. India's experience illustrates this dynamic clearly: despite gas comprising only 2% of total power generation capacity, the country relies on approximately 8-10 gigawatts of gas-based generation during peak demand periods and heatwave events. This seemingly small percentage becomes critically important during extreme weather when alternative sources cannot easily substitute.

When big ASX news breaks, our subscribers know first

How Do Regional Gas Shortfalls Manifest Across Global Energy Markets?

North American Market Dynamics

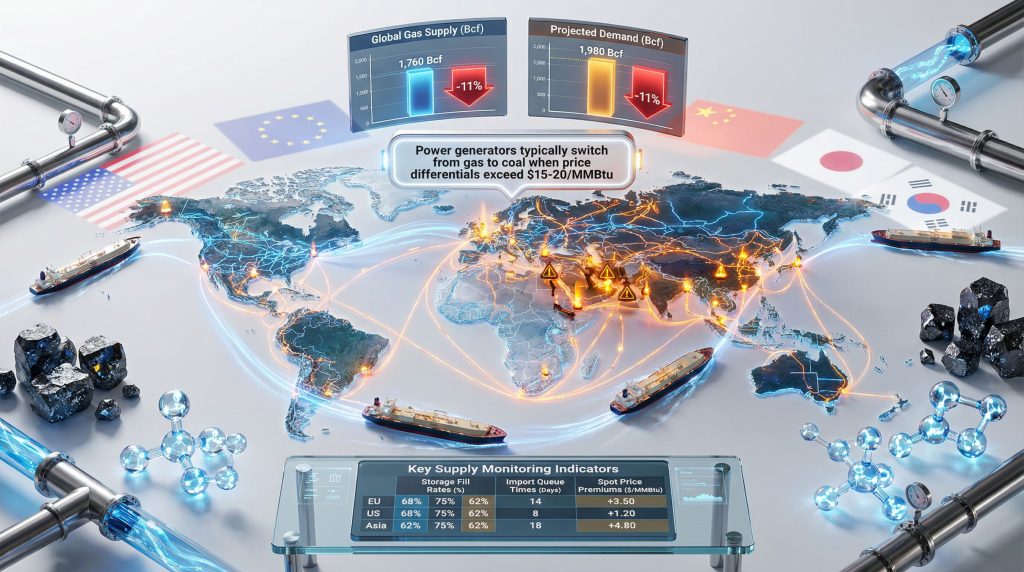

Current storage metrics reveal significant deviations from historical norms across key regions. Additionally, the US gas forecast indicates continued volatility ahead as demand patterns shift seasonally.

| Storage Region | Current Level | 5-Year Average | Variance |

|---|---|---|---|

| Total US Storage | 1,760 Bcf | 1,980 Bcf | -11% |

| Midwest Region | Below Average | Historical Baseline | -22% |

| Eastern Region | Below Average | Historical Baseline | -21% |

These inventory shortfalls indicate sustained demand pressure that extends beyond typical seasonal variations. The Midwest's particularly acute shortage reflects both increased industrial consumption and infrastructure constraints limiting inter-regional transfers.

European Energy Security Challenges

European Union storage mandates clash with market realities as member states struggle to balance regulatory requirements with economic constraints. Competition dynamics with Asian LNG buyers intensify during shortage periods, often resulting in European importers facing premium pricing to secure necessary volumes.

Infrastructure dependency risks remain elevated as alternative supply routes continue developing. The transition away from traditional pipeline sources requires substantial lead times for new import terminal construction and supply agreement negotiations.

Asia-Pacific Supply Vulnerabilities

India's coal sector provides compelling evidence of gas shortage impacts on regional energy dynamics. Coal India's March 2026 offtake reached 69.5 million tons, representing a 0.7% increase despite 1.5% lower production output at 84.5 million tons. This marked the first sales increase in six consecutive months, directly attributed to natural gas trends and approaching summer demand.

As the world's largest coal producer by output, Coal India accounts for over 80% of India's domestic coal production. The company's inventory deployment strategy reveals sophisticated demand management: accumulated stockpiles from temperate weather months were strategically released as gas supply disruptions emerged.

Critical shipping route dependencies remain a persistent vulnerability. Regional demand growth trajectories suggest continued pressure on import infrastructure, while diversification strategies require substantial capital investment and long-term planning horizons.

What Economic Mechanisms Drive Gas-to-Coal Switching During Supply Crunches?

Price Signal Transmission and Fuel Substitution Economics

Relative cost advantages during supply crunches extend beyond simple commodity price comparisons. When gas supply becomes constrained, the economics of fuel switching involve multiple variables including availability premiums, transportation costs, and operational flexibility requirements.

India's experience demonstrates how supply constraints can drive substitution independent of price signals. Vasudev Pamnani from Gujarat-based coal trader iEnergy Natural Resources noted that domestic coal remained relatively more attractive in certain segments while disruptions in liquefied natural gas supply and reduced gas-based power generation boosted reliance on coal for power generation.

During gas supply constraints, power generators often activate coal capacity not solely based on economic dispatch principles, but due to availability and reliability considerations that override traditional cost optimisation.

Market Response Patterns and Timing

Fuel switching decisions follow complex hierarchies that blend market signals with policy directives. India's government response illustrates this multi-layered approach: coal plants received directions to run at maximum capacity and avoid planned outages, while industries were asked to produce their own power through captive generation plants to free up supplies for households.

This policy-driven switching mechanism prioritises residential consumers over industrial demand, creating a cascading effect through different economic sectors. Industrial users absorb higher costs through captive generation deployment rather than experiencing direct supply curtailment.

Regional Substitution Capacity Analysis

Available coal generation capacity utilisation rates become critical during gas shortages. Coal plants operating at maximum capacity sacrifice typical maintenance scheduling, creating both immediate benefits through increased output and long-term concerns regarding accelerated equipment wear.

Grid flexibility requirements during fuel transitions challenge system operators who must balance reliability with economic dispatch. The loss of gas-fired generation's rapid ramping capabilities requires alternative flexibility sources, often involving higher-cost peaking units or demand response programmes.

Environmental compliance considerations add complexity during emergency operations. Regulators often provide temporary flexibility on emission standards during supply emergencies, but these exceptions carry environmental costs and political sensitivities.

How Do Supply Shortfalls Impact Different Economic Sectors?

Power Generation Sector Responses

Peak demand management strategies undergo fundamental modifications during gas supply constraints. India's approach demonstrates this transformation: despite gas providing only approximately 2% of total power generation, the 8-10 GW of gas capacity becomes critically important during peak periods when renewable sources face capacity factor limitations.

Capacity factor adjustments across fuel types create ripple effects throughout the generation fleet. Coal plants forced into extended maximum output operations experience higher maintenance requirements, potentially reducing future availability during subsequent peak periods.

Grid stability considerations become paramount when switching from flexible gas units to less responsive coal generation. System operators must implement additional ancillary services and maintain higher reserve margins to compensate for reduced operational flexibility.

Industrial Manufacturing Implications

Production scheduling modifications reflect industrial users' adaptation to supply constraints through captive generation deployment. This strategy shifts energy costs from grid-based pricing to self-generation economics, often resulting in higher per-unit costs but greater supply security.

Captive power generation activation requires substantial planning and capital deployment. Industries maintaining backup generation capacity gain competitive advantages during shortage periods, while those dependent solely on grid supply face potential production disruptions.

Supply chain cost pass-through mechanisms enable industrial users to transfer energy cost increases to downstream customers, though this transmission often occurs with time lags and may impact demand for energy-intensive products.

Residential and Commercial Market Effects

Heating cost volatility creates direct impacts on household budgets, particularly during extreme weather periods when demand peaks coincide with supply constraints. Policy prioritisation of residential consumers provides some protection from curtailment but cannot eliminate price exposure entirely.

Energy efficiency investment acceleration often follows supply shortage episodes as consumers and businesses seek to reduce vulnerability to future disruptions. This behavioural shift can create lasting demand reductions that persist beyond immediate shortage periods.

Demand response programme participation rates typically increase during shortage episodes as consumers become more conscious of energy consumption patterns. These programmes provide system operators with additional tools for managing peak demand without involuntary curtailments.

What Are the Macroeconomic Implications of Sustained Gas Supply Constraints?

Inflation Transmission Mechanisms

Energy cost inputs propagate through economic sectors via multiple pathways during sustained supply constraints. Manufacturing costs increase through higher electricity and direct fuel expenses, while transportation costs rise through diesel and other fuel price increases linked to overall energy market tightness.

India's situation exemplifies these transmission mechanisms as coal utilisation increases during an expected hotter-than-normal summer with heat wave days in May expected to exceed seasonal average. Higher coal consumption rates suggest increased production costs and potential price pressures throughout the economy.

Consumer spending pattern adjustments occur as households allocate larger budget shares to energy expenses, potentially reducing discretionary spending in other sectors. This reallocation can create broader economic impacts beyond the energy sector itself.

Trade Balance and Currency Effects

LNG market opportunities emerge as countries seek to diversify supply sources and reduce vulnerability to regional disruptions. LNG import cost pressures strain current account balances for net energy importers, particularly when global prices spike during shortage periods.

Countries with limited domestic energy production face difficult choices between energy security and fiscal sustainability. Energy security premiums in currency valuations reflect market perceptions of different countries' vulnerability to supply disruptions.

Nations with diverse energy portfolios and substantial domestic production often experience relative currency strength during global shortage episodes. Regional competitiveness shifts emerge as energy-intensive industries migrate toward locations with more reliable and cost-effective energy supplies.

Investment Flow Redirections

Infrastructure development prioritisation accelerates during shortage episodes as governments and private investors recognise the strategic importance of energy security. Emergency investment programmes often receive expedited approvals and funding that would normally require extended negotiation periods.

Energy transition timeline modifications may result from supply security concerns, with some regions temporarily increasing fossil fuel capacity to ensure reliability while renewable infrastructure develops. This creates tension between climate goals and energy security transition objectives.

Strategic reserve accumulation policies expand as governments seek to buffer against future supply disruptions. These programmes require substantial capital commitments and storage infrastructure investments that compete with other fiscal priorities.

Which Market Indicators Signal Emerging Supply-Demand Imbalances?

Forward Curve Analysis and Price Discovery

Contango versus backwardation patterns in futures markets provide early warning signals of developing imbalances. When near-term prices exceed longer-dated contracts (backwardation), markets signal immediate supply tightness that may intensify without intervention.

Seasonal spread relationships reveal underlying market stress beyond normal weather-driven variations. Unusual summer-winter price differentials often indicate structural supply constraints that cannot be resolved through typical seasonal adjustments.

Volatility indicators capture market uncertainty regarding future supply availability. Elevated implied volatility in options markets reflects trader concerns about potential supply disruptions that may not yet be visible in spot pricing.

Physical Market Metrics

Key monitoring indicators help identify developing supply stress before acute shortages emerge:

| Indicator | Normal Range | Stress Level | Critical Threshold |

|---|---|---|---|

| Storage Fill Rates | 85-95% | 75-85% | <75% |

| Import Queue Times | 2-3 weeks | 3-4 weeks | >4 weeks |

| Spot Price Premiums | 5-10% | 15-25% | >25% |

| Regional Price Spreads | Historical Average | 2x Average | 3x Average |

Import queue times provide particularly valuable insights into infrastructure stress levels. When normal delivery schedules extend significantly, it often indicates that import terminals and distribution networks approach capacity constraints.

Regional price spreads reveal transportation and distribution bottlenecks that may not appear in national or global average pricing data. Unusual price differentials between connected markets signal infrastructure constraints limiting arbitrage opportunities.

Cross-Commodity Correlation Patterns

Coal price responsiveness to gas shortages demonstrates fuel substitution dynamics in real-time. India's coal sector response illustrates this correlation: Coal India's first sales increase in six months coincided with gas supply disruptions, despite lower production output.

Renewable energy capacity factor impacts become more pronounced during gas shortages as system operators maximise available clean generation to offset fossil fuel constraints. Wind and solar generation patterns receive increased scrutiny during shortage periods.

Carbon credit market reactions reflect the environmental implications of fuel switching during emergencies. Increased coal utilisation typically drives higher carbon prices as overall system emissions increase.

The next major ASX story will hit our subscribers first

How Do Governments and Regulators Respond to Gas Supply Emergencies?

Emergency Protocol Activation

Strategic reserve release mechanisms provide immediate supply relief during acute shortages, though reserve sizes limit the duration of intervention effectiveness. Government stockpiles require careful management to balance immediate needs with longer-term security requirements.

Industrial demand curtailment procedures follow established priority hierarchies that protect essential services while reducing non-critical consumption. India's approach of requesting industries to activate captive generation illustrates voluntary curtailment strategies that avoid mandatory rationing.

Cross-border cooperation agreements enable rapid supply sharing during regional emergencies, though political tensions can complicate implementation during crisis periods. Pre-negotiated arrangements prove more effective than ad-hoc emergency negotiations.

Market Intervention Tools

Price cap implementations attempt to protect consumers from extreme cost increases but often create additional market distortions and supply disincentives. Effectiveness varies significantly based on implementation design and duration.

Import acceleration programmes may include expedited permitting for new terminals, temporary tariff reductions, or direct government purchasing to secure additional supplies. These interventions require substantial fiscal resources and coordination with international suppliers.

Domestic production incentive structures can stimulate additional output through tax incentives, expedited permitting, or direct subsidies. However, production increases often require substantial lead times limiting effectiveness during immediate crises.

Long-term Policy Adaptations

Energy security framework updates typically follow major shortage episodes as governments reassess vulnerability and preparedness. These reviews often result in enhanced monitoring systems, larger strategic reserves, and improved emergency response protocols.

Infrastructure resilience investments receive increased political and financial support following supply disruptions. Projects that previously faced funding challenges may gain approval as energy security concerns override cost considerations.

Diversification mandate implementations accelerate as policymakers recognise concentration risks in supply sources, transportation routes, or fuel types. These mandates often carry economic costs but provide insurance against future disruptions.

What Long-term Structural Changes Result from Recurring Supply Shortfalls?

Investment Pattern Shifts

Accelerated renewable energy deployment gains momentum as investors and policymakers seek to reduce dependence on volatile fossil fuel markets. Supply security concerns often provide political cover for renewable energy investments that face economic challenges.

Enhanced storage infrastructure development becomes a priority for both governments and private investors. Battery storage, pumped hydro, and compressed air energy storage receive increased attention as tools for managing supply variability.

Regional production capacity expansions focus on reducing import dependencies, even when domestic production carries higher costs than international supplies. Energy security premiums justify investments that pure economic analysis might not support.

Market Structure Evolution

Contract term modifications in LNG markets reflect buyer preferences for supply security over price optimisation. The LNG import structure becomes increasingly important as longer-term agreements with take-or-pay provisions become more attractive despite reduced flexibility.

Risk management tool development accelerates as market participants seek better hedging instruments for supply disruption scenarios. New financial products emerge to address risks that traditional commodity hedging cannot capture adequately.

Regional integration acceleration occurs as neighbouring markets recognise mutual benefits from improved interconnection and coordination. Emergency sharing arrangements often evolve into permanent structural integration.

Technology Adoption Acceleration

Demand response system implementations expand rapidly following shortage episodes as utilities and regulators recognise the value of demand flexibility. Smart grid technologies that enable real-time demand management receive priority investment.

Grid flexibility enhancement projects gain support as system operators confront the operational challenges of managing supply constraints. Energy storage, advanced forecasting, and rapid-response generation receive increased attention.

Alternative fuel infrastructure development accelerates as economies seek to reduce vulnerability to single-fuel dependencies. Hydrogen, biofuels, and synthetic fuels may receive increased investment despite higher current costs.

How Can Market Participants Prepare for Future Gas Supply Volatility?

Risk Management Framework Development

Portfolio diversification strategies across fuel types become essential for large energy consumers seeking to minimise exposure to single-fuel supply risks. Industrial users increasingly maintain capability to switch between gas, coal, oil, and renewable sources based on availability and cost.

Financial hedging instrument utilisation expands beyond simple price hedging to include supply availability contracts and force majeure insurance. These sophisticated risk management tools help participants manage both price and quantity risks simultaneously.

Operational flexibility enhancement involves maintaining multiple fuel capabilities, backup generation capacity, and demand reduction protocols. Organisations that invest in flexibility during stable periods gain competitive advantages during shortage episodes.

Strategic Planning Considerations

Scenario modelling for supply disruption events requires consideration of multiple variables including geopolitical risks, weather extremes, and infrastructure failures. Robust planning incorporates low-probability, high-impact events that traditional forecasting may underweight.

Alternative supplier relationship development reduces dependence on single sources or regions. Diversified supplier portfolios provide insurance against localised disruptions while maintaining negotiating leverage during normal periods.

Technology investment timing optimisation balances current costs against future supply security benefits. Early adopters of flexibility technologies often achieve better returns when supply constraints increase the value of operational flexibility.

What Role Do Weather Patterns Play in Gas Supply Shortfall Predictions?

Extreme weather events significantly influence gas supply shortfall patterns through both demand spikes and infrastructure disruptions. Consequently, heatwaves increase cooling demands whilst simultaneously straining gas-fired power generation capacity.

Winter storm impacts create dual pressures by elevating heating demands whilst potentially disrupting production and transportation infrastructure. Pipeline freeze-offs and platform shutdowns during severe weather can eliminate substantial supply volumes precisely when demand peaks.

Furthermore, weather-related energy forecasting has become increasingly sophisticated as meteorological services work closely with energy planners to anticipate potential shortfalls before they materialise.

Seasonal transition periods present particular challenges as storage systems must balance inventory rebuilding with ongoing consumption demands. The timing of seasonal weather shifts can dramatically impact whether regions enter peak demand periods with adequate reserve margins.

Please note: This analysis is based on current market conditions and publicly available information. Energy market dynamics involve significant uncertainties, and actual outcomes may differ materially from projections discussed. Readers should conduct their own research and consult with qualified professionals before making investment or operational decisions based on this analysis.

Further Exploration: Readers interested in learning more about global energy market dynamics can explore additional educational content from established energy research institutions and market analysis platforms that provide ongoing coverage of supply-demand fundamentals and geopolitical impacts on commodity markets.

Ready to Capitalise on Energy Market Disruptions?

Gas supply shortfalls create significant ripple effects across commodity markets, particularly for energy-focused companies listed on the ASX. Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant mineral discoveries, including those in the energy transition space, enabling subscribers to identify actionable opportunities ahead of broader market recognition during periods of supply volatility.