July 18, 2026

Africa's Resource Nationalism Tide Is Rewriting the Rules for Foreign Gold Miners

Across the African continent, a generational shift is underway in how resource-rich nations think about the relationship between sovereign wealth, foreign capital, and mining tenure. The old bargain, struck during an era of subdued commodity prices and urgent need for foreign direct investment, offered multinational miners long lease terms, stable fiscal conditions, and near-automatic renewal rights in exchange for bringing capital and technical expertise. That bargain is being systematically unwound. Ghana's proposed Ghana mining law revamp represents one of the most consequential expressions of this continental realignment, and Gold Fields' lease renewal challenge at Tarkwa has become its highest-profile test case.

When big ASX news breaks, our subscribers know first

Ghana's Mining Framework: Two Decades of Policy in Reverse

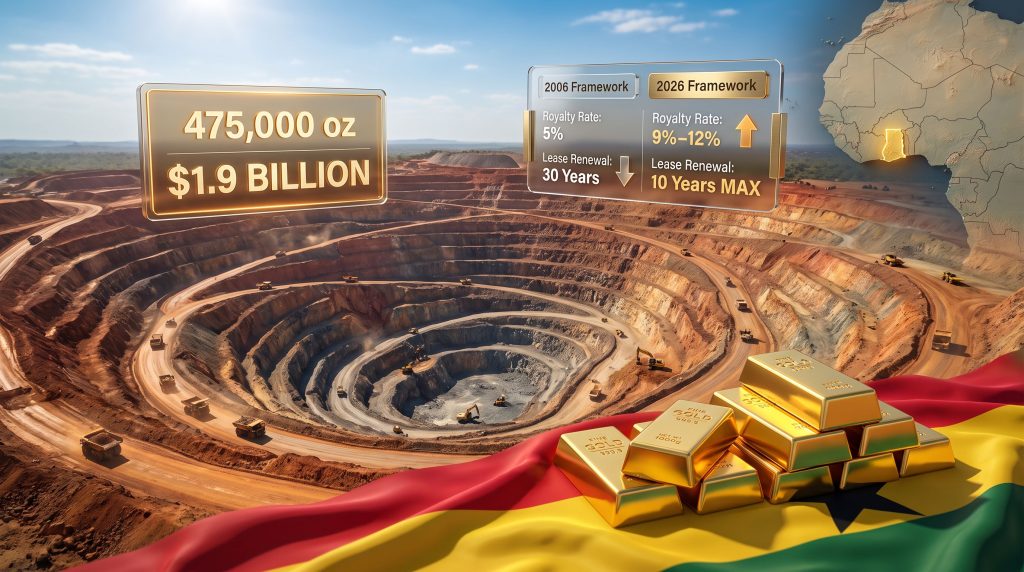

When Ghana introduced its Minerals and Mining Act in 2006, the policy logic was straightforward. The country needed foreign capital to develop its geological endowment, and competing for that capital meant offering competitive terms. Thirty-year leases, multi-decade stability agreements, and automatic renewal pathways were not signs of weakness, they were deliberate instruments designed to attract the kind of patient capital that billion-dollar open-pit gold mines require.

The world that justified those terms no longer exists. Gold has surpassed $4,000 per ounce and continued climbing toward levels that were unimaginable when the 2006 framework was drafted. The fiscal mathematics that once made generous lease terms seem like a reasonable trade-off now look, from Accra's perspective, like a systematic undervaluation of the country's sovereign resource wealth. Ghana's cabinet-approved legislative overhaul, the first comprehensive rewrite of the country's mining law in approximately twenty years, is the direct consequence of that reassessment.

Ghana holds a position of significant strategic weight in the global gold industry. As Africa's largest gold producer, the country's regulatory posture carries weight that extends far beyond its own borders, influencing how investors, operators, and governments elsewhere on the continent calibrate their own resource nationalism ambitions. This shifting dynamic is also reshaping the broader gold market outlook for producers with significant African exposure.

What the New Law Actually Changes: A Framework Comparison

The proposed legislation restructures nearly every dimension of mining tenure in Ghana. The changes are not incremental refinements; they represent a structural reorientation of the balance between state and operator.

| Regulatory Element | Previous Framework (2006) | Proposed Framework (2026) |

|---|---|---|

| Maximum mining lease term | 30 years | 20 years |

| Lease renewal extension | Up to 30 years | Maximum 10 years |

| Exploration/prospecting licence | Up to 9 years | Single licence, capped at 5 years |

| Automatic lease renewal | Permitted | Abolished |

| Stability agreements | Multi-decade fiscal lock-in | Capped at 5 years; key law categories excluded |

| Development agreements | Available | Abolished |

| Royalty rate | Up to 5% | 9% to 12% (price-linked escalation) |

| Medium-scale mining category | Not defined | New tier, minimum 60% Ghanaian ownership |

| Community Development Agreements | Discretionary | Mandatory, fixed % of gross mineral sales |

Each of these changes carries a distinct implication for how mining companies model project economics, structure financing, and assess sovereign risk.

The Royalty Escalation Mechanism

The shift from a 5% maximum royalty to a price-linked structure ranging from 9% to 12% is among the most financially material changes in the package. The escalation trigger activates the ceiling rate of 12% when gold prices reach or exceed $4,500 per ounce, a level that, given the current gold price outlook, is no longer a remote scenario.

This price-indexed royalty architecture follows a pattern increasingly seen in resource-sovereign jurisdictions. Chile uses a similar mechanism for copper revenue capture, and Indonesia has deployed escalating fiscal regimes for nickel. The underlying logic is the same: governments want automatic participation in commodity supercycles without having to renegotiate contracts every time prices spike. For mining companies, the consequence is that project-level cash flow models must now incorporate a variable royalty line that expands precisely when margins are highest.

Key Consideration for Investors: A royalty calculated on gross mineral revenue, not net profit, means the obligation applies regardless of operating cost inflation, capital expenditure cycles, or processing inefficiencies. At Tarkwa's approximate annual production of 475,000 ounces, the difference between a 5% and 12% royalty rate at $4,000/oz gold represents a shift in annual fiscal obligation of roughly $266 million, a figure that fundamentally changes the project's free cash flow profile.

Stability Agreements: Removing the Cornerstone of Mining Finance

Perhaps no single element of the reform carries more weight for project financing than the abolition of development agreements and the severe curtailment of stability agreements. These instruments have historically served as the foundation upon which project lenders and equity investors underwrite long-cycle capital commitments.

A stability agreement's core function is not simply to lock in a low tax rate; it is to provide the contractual certainty that allows a company to model a 20-year investment with sufficient confidence to justify initial capital expenditure that may take a decade or more to recover. When that certainty is removed and replaced with a capital-recovery framework, the details of which remain largely undefined in implementing regulations, the risk calculus for new greenfield investment changes materially.

Benjamin Boakye, Executive Director at the Africa Centre for Energy Policy, has argued that removing stability agreements altogether risks making Ghana less competitive relative to peer jurisdictions that continue to offer long-term fiscal certainty. His position rests on a fundamental insight about how exploration capital behaves: it is highly mobile, it flows toward geological prospectivity combined with regulatory predictability, and it responds to perceived sovereign risk with a speed that takes years to reverse.

Boakye has also noted that the reform lacks a compelling evidence-based foundation demonstrating that Ghana's existing mining regime required such a comprehensive overhaul. His concern centres on the distinction between extracting maximum fiscal value in the short term and optimising mining's broader contribution to economic development over time.

Tarkwa and the Stakes of Gold Fields' Lease Renewal

No single asset makes the stakes of the Ghana mining law revamp more concrete than the Tarkwa mine. Tarkwa is not simply a large gold mine; it is one of the continent's most productive open-pit operations and represents a genuinely significant share of Gold Fields' global output. Furthermore, the Gold Fields takeover offer discussions elsewhere have placed additional scrutiny on the company's asset base and long-term strategic direction.

The operational profile is striking:

- Annual production: approximately 475,000 ounces in 2025

- Share of Gold Fields' global output: close to one-fifth of total company production

- Implied annual revenue at $4,000/oz gold: approximately $1.9 billion

- Lease expiry: April 2027

- Renewal application submitted: November 2025, requesting a 20-year extension

- Maximum permitted under proposed new law: 10 years

The collision between the 20-year extension Gold Fields applied for and the 10-year cap proposed under the new framework is not merely procedural. It signals a fundamental disagreement about the investment horizon required to justify continued capital deployment into a capital-intensive open-pit operation.

The Tarkwa Mineralogy Factor: Why Tenure Length Matters More Here Than Elsewhere

Tarkwa's geological character adds a dimension to this tenure debate that is rarely discussed in policy circles. The deposit sits within the Tarkwaian sedimentary sequence, a Palaeoproterozoic conglomerate-hosted system that is broadly analogous to the Witwatersrand Basin in South Africa. Unlike many African gold deposits hosted in shear zones or intrusive systems, Tarkwaian reefs are low-grade, high-tonnage ore bodies where profitability is fundamentally a function of processing scale and efficiency, not head grade.

The mine operates on ore grades that are modest by global standards, which means the economics are deeply sensitive to royalty rates, processing throughput, and infrastructure investment continuity. Compressing the lease term reduces the window over which capital investments in throughput improvement can be recovered, making the operation more economically marginal at the margins precisely when royalty rates are also increasing.

The Damang Precedent: A Warning That Cannot Be Ignored

Any analysis of Tarkwa's renewal prospects must be read through the lens of what happened at the Damang mine. The sequence of events there has established a template that reshapes how every future lease renewal in Ghana must be evaluated. According to reporting from Reuters, Gold Fields ceased operations at Damang after the government rejected its lease renewal application, underscoring the very real consequences of discretionary ministerial decision-making.

Gold Fields' lease extension request at Damang was denied in April 2025. Operational control was subsequently transferred, and the lease was awarded to Engineers and Planners Co. Ltd. in April 2026. The firm that won the Damang award had pre-existing operational involvement at the asset.

The Damang outcome demonstrated several things simultaneously:

- Lease expiry is a genuine decision point, not an administrative formality requiring only paperwork.

- The government is prepared to transfer producing assets to locally owned operators.

- Historical operating performance does not guarantee renewal for foreign operators.

- The political economy of indigenisation has reached a level of maturity where it can be operationalised at producing assets, not just at the exploration stage.

For Gold Fields, Damang was a financially contained loss. Tarkwa is categorically different in scale, making its outcome a company-defining event rather than a manageable asset write-down.

What Gold Fields Must Demonstrate: The New Renewal Calculus

The government has publicly stated its intention to renew the Tarkwa lease while simultaneously making clear that renewal will not be automatic. This creates a structured negotiation environment in which Gold Fields must make a credible case across several dimensions:

- Local economic linkages: Demonstrated commitments to Ghanaian suppliers, contractors, and workforce development programmes that go beyond existing obligations.

- Technology transfer: Evidence that operational and technical expertise is being transferred to Ghanaian nationals in meaningful and measurable ways.

- Community Development Agreement structure: A binding framework with a clearly defined percentage of gross mineral sales directed to host community development, structured to satisfy both legal requirements and community expectations.

- Capital investment roadmap: A development plan that justifies the requested tenure extension and demonstrates continued mine life development rather than a production-extraction posture.

The added complexity is that authorities have signalled an intention to pass the new mining law before concluding the review of pending lease-renewal applications. Consequently, Gold Fields' application may ultimately be assessed under the revised legal framework rather than the existing 2006 law, a procedural point with significant substantive consequences. Gold Fields has publicly outlined its rationale for why the Tarkwa renewal represents a compelling case worthy of favourable consideration.

The next major ASX story will hit our subscribers first

Continental Context: Ghana Is Not an Outlier

It would be analytically convenient but factually incorrect to treat Ghana's legislative overhaul as an isolated policy aberration. Across the continent, a consistent pattern is emerging, and the mining geopolitical risk dimension of these reforms is becoming increasingly central to how institutional investors evaluate African-exposed portfolios.

| Country | Recent Resource Nationalism Measure |

|---|---|

| Ghana | Lease term compression, royalty escalation, indigenisation tiers |

| Tanzania | State ownership requirements in new mining agreements |

| Zimbabwe | Mandatory beneficiation rules and ownership thresholds |

| Burkina Faso | Increased state equity participation requirements |

| Côte d'Ivoire | Strengthened local content requirements |

The common thread is elevated commodity prices providing fiscal motivation, combined with domestic political pressure for visible economic benefit from natural resource extraction. The timing across these jurisdictions is not coincidental; the commodity supercycle has created the revenue justification for reforms that would have been economically and politically difficult to implement during lower price environments.

For international gold miners with African portfolios, this continental pattern means that the regulatory risk premium attached to African operations must be reassessed systematically, not on an asset-by-asset basis.

Investor Implications: Repricing Sovereign Risk in African Gold Equities

The Ghana mining law revamp and Gold Fields' lease renewal challenge present a broader investor question: how should equity markets price the sovereign risk component of African-exposed gold producers? Indeed, this question is central to how analysts are currently evaluating gold M&A activity involving companies with material African production exposure.

Several analytical frameworks are relevant:

Terminal value compression: When lease terms shorten and renewals become discretionary rather than rule-based, the terminal value of an asset in a discounted cash flow model must be adjusted to reflect the probability-weighted outcome of renewal under uncertain terms. For a mine like Tarkwa, which has significant remaining geological potential, this creates a meaningful disconnect between intrinsic value under favourable renewal terms and the risk-adjusted value under the new regime.

Royalty rate sensitivity: At $4,000/oz gold and 475,000 ounces per year, every percentage point change in the effective royalty rate represents approximately $19 million in annual fiscal impact. The proposed shift from 5% to a potential 12% represents a swing of approximately $133 million per year from Tarkwa alone, before accounting for any gold price escalation that would push the rate toward the 12% ceiling.

Capital allocation competition: Mining capital is internationally mobile. If Ghana's risk-adjusted return profile deteriorates relative to peer jurisdictions offering greater regulatory predictability for comparable geological prospectivity, exploration and development capital will migrate. This is not a hypothetical; it is a documented pattern observable across multiple previous resource nationalism cycles in Africa, Latin America, and Southeast Asia.

Speculative Scenario: If the Tarkwa lease is renewed at only 10 years rather than the requested 20, and the new royalty regime applies from 2027, the net present value of Gold Fields' Ghanaian operations could be substantially lower than current market consensus estimates reflect. This potential valuation gap is a risk that institutional investors with significant Gold Fields exposure should be actively stress-testing in their portfolio models.

Frequently Asked Questions: Ghana Mining Law and Gold Fields Lease Renewal

What is the current status of Gold Fields' Tarkwa lease renewal?

The Tarkwa lease expires in April 2027. Ghana's government has confirmed its intention to renew the lease but has explicitly stated that renewal will not be automatic. Gold Fields is required to submit detailed development proposals for technical committee review at the Minerals Commission, followed by ministerial-level assessment. The application may be evaluated under the proposed new legislative framework if the law passes parliament before the renewal decision is finalised.

How long can mining leases run under the proposed new law?

Under the draft legislation approved by cabinet in 2026, new mining leases are capped at a maximum of 20 years, reduced from 30 years under the 2006 framework. Lease renewals are limited to a maximum of 10 years, reduced from 30 years. Automatic renewal rights have been abolished entirely.

What happened to Gold Fields' Damang mine lease?

The government denied Gold Fields' Damang lease extension in April 2025. Operational control was subsequently transferred, and the lease was awarded to Engineers and Planners Co. Ltd. in April 2026. This outcome established a concrete precedent for the reallocation of producing gold assets to locally owned firms upon lease expiry.

What are Ghana's new gold royalty rates?

The proposed framework sets royalties at 9% of gross mineral revenue, escalating to 12% when gold prices reach or exceed $4,500 per ounce. This compares to the previous maximum rate of 5%, representing a substantial increase in the fiscal burden on producers at current and projected gold price levels.

Will existing stability agreements with major miners be cancelled immediately?

No. Existing stability agreements with major operators including Newmont, AngloGold Ashanti, and Gold Fields remain in force until their scheduled expiry in 2027, at which point the new legislative regime applies in full.

What is the medium-scale mining category?

A newly defined operational tier requiring a minimum of 60% Ghanaian ownership, positioned between the existing small-scale and large-scale categories. This creates a formal indigenisation requirement for operators in this size bracket, mirroring ownership threshold frameworks seen in Nigeria's petroleum sector and Zimbabwe's mining industry.

Key Takeaways

The Ghana mining law revamp and Gold Fields' lease renewal dilemma collectively represent more than a bilateral negotiation between a mining company and a host government. They reflect a structural repricing of how African governments value their resource endowments in a sustained high-price environment.

- Lease tenure compression from 30-year to 20-year maximum terms fundamentally alters the investment horizon for capital-intensive gold mining projects with long payback periods.

- Discretionary ministerial approval replacing automatic renewal rights introduces a sovereign risk premium that will increasingly be reflected in project financing costs and equity market valuations.

- The Damang precedent demonstrates that lease reallocation to local operators is now an operational reality, not a theoretical policy position.

- Stability agreement abolition removes the fiscal certainty instrument that has historically provided the underwriting confidence for major capital commitments in Ghana's gold sector.

- Mandatory community development agreements and escalating royalties tied to gross revenue increase the fixed cost base for all producers, with the royalty escalator specifically targeting windfall capture at elevated gold prices.

- The medium-scale indigenisation tier creates new structural requirements for foreign participation across a broader segment of Ghana's mining industry.

This article contains forward-looking assessments, financial modelling scenarios, and speculative projections regarding mining regulatory outcomes and asset valuations. These represent analytical perspectives based on publicly available information and should not be construed as investment advice. Mining investment involves material risks including sovereign risk, commodity price volatility, and regulatory change. Readers should conduct independent due diligence before making any investment decisions.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

As resource nationalism reshapes the risk landscape for gold producers across Africa, identifying high-quality discoveries in more stable jurisdictions has never been more critical — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex mineral data into actionable insights for both short-term traders and long-term investors. Explore why historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.