June 6, 2026

Global Capital Flow Realignment Signals New Era for Alternative Assets

The traditional investment landscape faces unprecedented disruption as institutional capital allocation models confront structural challenges that emerged from decades of conventional portfolio theory. Financial institutions worldwide grapple with the limitations of the classic 60/40 equity-bond framework, particularly after the synchronized decline of both asset classes during 2022 market volatility. This fundamental breakdown has accelerated exploration of alternative diversification strategies, with precious metals emerging as a critical component in modern asset allocation components.

The sophistication of investable assets has evolved dramatically over recent decades, introducing master limited partnerships, private equity, and floating rate instruments into mainstream institutional portfolios. However, one asset class remains conspicuously absent from most professional allocations: physical precious metals. This absence becomes increasingly problematic as traditional diversification assumptions prove inadequate for contemporary market dynamics.

When big ASX news breaks, our subscribers know first

Understanding the Magnitude of Chinese Silver Demand Acceleration

Quantifying the Import Surge Phenomenon

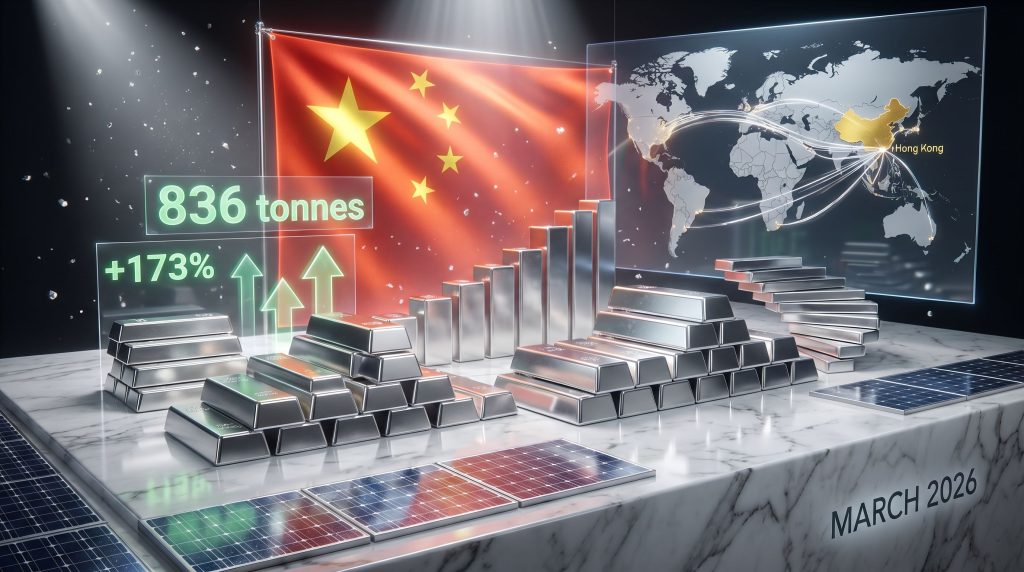

Chinese silver imports surge 78% in recent monthly data, representing a dramatic departure from historical purchasing patterns. This acceleration occurred alongside broader precious metals volatility, with silver retreating from approximately $80 per ounce to current levels around $76, while gold consolidated near $4,700 after reaching parabolic highs above $5,300 in March.

The magnitude of this import increase becomes more significant when contextualised against long-term price appreciation. Silver prices have increased approximately 1,800% over the past 25 years, rising from roughly $4 per ounce in 2001 to current levels. Furthermore, this surge coincides with broader market trends, as seen in China's silver imports driven by retail and solar demand.

Market Structure Implications of Physical vs. Paper Trading

A fundamental divergence has emerged between Eastern physical purchasing behaviour and Western risk-asset trading patterns. While Chinese entities accumulate physical silver through import channels, Western markets continue treating silver as a high-beta risk asset subject to equity market correlation dynamics. This geographical split in market interpretation raises questions about which approach accurately reflects silver's intrinsic value proposition.

The persistence of zero precious metals allocation among most financial advisors contrasts sharply with the demonstrated diversification benefits these assets provided during recent market stress periods. During 2022's simultaneous equity and bond market decline, gold maintained approximate price stability while both traditional asset classes experienced significant drawdowns. Consequently, the silver market squeeze continues to impact global financial markets.

Monetary Policy Transmission Mechanisms and Asset Allocation Shifts

Extended Timeline Effects of Federal Reserve Policy Implementation

The Federal Reserve initiated rate cutting cycles in late 2024, followed by additional accommodation in the fourth quarter of 2025. This created a 19-month period of cumulative monetary easing that remains relevant for current market dynamics due to the lagged transmission mechanisms of monetary policy through the broader economy.

The practical implications of this policy accommodation manifest through multiple channels:

- Consumer credit utilisation: Home equity line of credit availability at lower floating rates encourages household spending and investment

- Small business lending: Reduced borrowing costs support business expansion and capital investment

- Opportunity cost calculations: Overnight money market rates declined from 5.25%-5.50% to approximately 3%, reducing the relative cost of holding non-yielding assets

Money Supply Growth and Inflation Dynamics Context

Current M2 money supply growth measures approximately 3.5% on a year-over-year basis, significantly lower than pandemic-era growth rates that reached "the teens" during COVID-19 stimulus periods. This moderate growth trajectory supports continued economic expansion without generating the extreme inflationary pressures that might necessitate aggressive monetary tightening.

The relationship between money supply growth, economic expansion, and precious metals demand creates favourable conditions for continued Chinese silver imports surge. Industrial metals like copper have recovered above $6 per pound after recent weakness, with "Dr. Copper" suggesting continued economic expansion rather than recessionary conditions.

Portfolio Construction Evolution and Institutional Adoption Barriers

Global Investable Asset Allocation Discrepancies

Research indicates gold represents approximately 12.7% of the global investable asset base, yet most institutional portfolios maintain zero allocation to precious metals. This structural underallocation creates significant potential for capital flow acceleration if institutional rebalancing occurs toward more representative weightings. In addition, the gold record highs demonstrate the growing appeal of precious metals as an inflation hedge.

| Asset Category | Global Weight | Typical Allocation | Allocation Gap |

|---|---|---|---|

| Gold | 12.7% | 0% | +12.7% |

| Emerging Market Stocks | ~40% | <10% | +30% |

| US Stocks | ~60% | >90% | -30% |

The career risk implications of deviating from peer allocations create institutional inertia against precious metals adoption. Financial advisors maintaining 5% gold allocation face competitive pressure from colleagues maintaining zero allocation, despite the theoretical diversification benefits of modest precious metals exposure.

Innovation in Portfolio Implementation Mechanisms

Exchange-traded product innovations have created new implementation pathways that address traditional allocation constraints. For instance, equity-plus-gold mandates allow investors to achieve 105% portfolio exposure through structured products that layer gold futures exposure over equity positions, effectively creating enhanced diversification without requiring asset reallocation decisions.

This efficient capital approach enables portfolio construction modifications from traditional 60/40 structures to approximately 60/40/5 configurations. The additional 5% represents precious metals exposure funded through leverage rather than asset substitution. However, investors should carefully consider the ETCs investment guide before implementing such strategies.

Economic Resilience Factors Supporting Sustained Import Demand

Oil Shock Analysis and Consumer Spending Capacity

Current oil market dynamics with Brent crude above $106 per barrel demonstrate significantly different economic impact characteristics compared to historical oil shocks. Fuel economy improvements and wage growth have substantially reduced the consumer demand destruction typically associated with energy price increases.

Historical Fuel Economy and Wage Comparison:

- 1979 Oil Shock: Average vehicle fuel economy 6 miles per gallon below current Chrysler Pacifica standards

- 2008 Crisis: 21 miles per gallon average vs. 28 miles per gallon for current late-model vehicles

- Wage Adjustment: Average hourly earnings increased from $17 (2008) to $32 (current), requiring approximately $95 per gallon gasoline to create equivalent economic pressure

This reduced sensitivity to oil price volatility supports continued economic expansion and industrial metal demand, including silver's industrial applications alongside its investment characteristics. Market intelligence suggests that both investors and manufacturers are scrambling to secure silver supplies.

China's Structural Investment Preference Evolution

Traditional Chinese wealth accumulation strategies centred on perpetual property ownership have undergone fundamental transformation over the past five years. This structural shift in domestic asset allocation preferences creates conditions favouring alternative investments, including precious metals, as Chinese investors reassess portfolio construction assumptions.

The breakdown of real estate as a primary wealth vehicle necessitates diversification into alternative asset classes. Consequently, silver and gold provide both store-of-value characteristics and portfolio diversification benefits for Chinese retail and institutional investors.

Technology-Driven Investment Behaviour and Generational Preferences

Bitcoin Performance Context and Alternative Asset Competition

Bitcoin's performance during 2025 equity market selloffs provided critical comparative data for alternative asset evaluation. While gold demonstrated effective portfolio diversification during S&P 500 decline periods, Bitcoin exhibited high correlation with equity markets, failing to provide the defensive characteristics many investors expected.

This performance differential influenced generational investment preferences, with investors who might have instinctively chosen Bitcoin during 2015-2020 market stress reconsidering precious metals as more reliable portfolio diversifiers. The historical precedent from 1979-1980 oil shock periods, when investor instincts favoured Krugerrands and physical metals, appears to be reasserting itself among younger demographic cohorts.

Exchange-Traded Product Flow Analysis and Institutional Adoption

Despite unprecedented precious metals price performance during recent bull markets, exchange-traded product creation activity remained subdued, with capital flows continuing to concentrate in S&P 500 tracker funds. This persistent flow pattern suggests institutional adoption of precious metals remains in early stages, despite demonstrated portfolio benefits during market stress periods.

The disconnect between price performance and institutional adoption creates potential for accelerated capital allocation shifts. This occurs when market participants recognise the portfolio construction benefits that precious metals provide during periods of traditional asset class correlation breakdown.

The next major ASX story will hit our subscribers first

Long-Term Sustainability Assessment for Import Growth Trajectories

Bond Market Stability and Portfolio Allocation Dynamics

Current 10-year Treasury note trading ranges between 395-450 basis points provide relative stability compared to more volatile periods. This creates conditions where precious metals can compete effectively with fixed income alternatives and supports precious metals valuations by improving relative attractiveness compared to cash and short-term instruments.

The stability of this trading range reduces the erratic bond market conditions that historically created headwinds for all alternative assets, including precious metals. Portfolio managers can implement precious metals allocation decisions with greater confidence in the underlying interest rate environment, particularly given the positive gold price outlook driven by geopolitical and economic factors.

Industrial Demand Components and Economic Expansion Continuation

The broader economic expansion context, confirmed by copper price recovery and continued industrial metal strength, supports sustained silver import demand beyond temporary import surge factors. Dr. Copper's prescription of economic health, evidenced by sustained pricing above $6 per pound, indicates continued industrial consumption patterns that underpin silver's dual investment/industrial metal characteristics.

Key Industrial Demand Indicators:

- Copper recovery to $6+ per pound after temporary weakness

- Sustained economic expansion despite geopolitical disruptions

- Limited demand destruction from oil market volatility

- Continued money supply growth supporting economic activity

Strategic Portfolio Implications for Investment Management

Risk Management Framework Evolution

The traditional portfolio risk management framework requires fundamental reassessment given the breakdown of historical asset class correlation assumptions. Zero precious metals allocation no longer represents neutral positioning but constitutes an active bearish stance on alternative diversification strategies.

Portfolio construction sophistication has evolved substantially over recent decades, incorporating master limited partnerships, private equity, private credit, and floating rate instruments. The absence of precious metals from this evolution creates structural gaps in diversification frameworks that Chinese silver imports surge patterns may be addressing more effectively than Western institutional approaches.

Implementation Strategy Considerations for Institutional Adoption

The career risk management aspects of precious metals adoption require careful navigation by institutional portfolio managers. Moving from zero to modest 5% allocation represents substantial tracking error risk relative to peer institutions, despite theoretical portfolio construction benefits.

Allocation Strategy Framework:

- Conservative Implementation: 2-3% initial allocation to minimise tracking error

- Moderate Implementation: 5% allocation funded from fixed income reallocation

- Enhanced Implementation: Leveraged structures maintaining equity exposure while adding metals overlay

The most practical implementation pathway involves reallocating from fixed income rather than equity positions. This approach recognises the demonstrated breakdown of bonds as effective portfolio diversifiers during recent market stress periods.

Future Market Structure Evolution and Global Trade Patterns

International Price Discovery Mechanism Changes

The substantial Chinese import volumes create new dynamics in global silver price discovery mechanisms, potentially establishing different equilibrium points for international precious metals valuation. This shift reflects broader changes in global trade patterns and regional market integration levels.

The geographical arbitrage opportunities created by price differentials between Chinese domestic markets and international benchmarks demonstrate the sophisticated trading infrastructure available for capitalising on cross-border flow optimisation. These mechanisms may establish new baseline levels for international silver trade patterns.

Market Psychology and Investment Behaviour Evolution

Current market psychology reflects a generational transition in alternative asset preferences, with Bitcoin's correlation failures during equity market stress periods redirecting attention towards traditional precious metals. This preference evolution may establish more durable demand foundations compared to previous cryptocurrency-driven alternative asset cycles.

The sophistication gap between Eastern physical accumulation strategies and Western paper trading approaches suggests potential for continued divergence in regional market behaviour patterns. This geographical split in market interpretation may persist as Chinese silver imports surge reflects longer-term portfolio construction considerations rather than short-term trading dynamics.

Disclaimer: This analysis contains forward-looking statements and market projections that involve inherent uncertainties and risks. Precious metals investments carry volatility risks and past performance does not guarantee future results. Readers should conduct independent research and consult qualified financial advisors before making investment decisions. The information presented is for educational purposes and should not be considered personalised investment advice.

Ready to Capitalise on the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, transforming complex market data into actionable investment insights that keep you ahead of market movements. Explore why major mineral discoveries can generate substantial returns and begin your 14-day free trial today to position yourself at the forefront of emerging opportunities in the rapidly evolving precious metals sector.