June 27, 2026

The 50-Year Cage: Why Silver's Structural Break Could Be the Most Significant Commodity Event of This Decade

Most commodity repricing cycles begin quietly. They build beneath the surface for years, even decades, until the weight of suppressed fundamentals, monetary distortion, and accumulated physical deficits reaches a breaking point. When that break finally arrives, it rarely looks like what observers expect. The Michael Oliver $300 to $500 silver prediction follows this same pattern — a structural case that deserves rigorous examination rather than reflexive dismissal.

Copper's 2005 breakout was dismissed as speculative excess. Lead's 2007 surge was treated as an anomaly. Both turned out to be structural regime changes that rewrote the floor for those metals permanently. Michael Oliver, founder of Momentum Structural Analysis (MSA), applies the same analytical template to silver today.

When big ASX news breaks, our subscribers know first

What Is Momentum Structural Analysis and Why Does It Diverge from Conventional Methods?

Understanding why Oliver's forecast carries analytical weight requires first understanding the methodology behind it. MSA does not rely on the standard technical indicators most traders are familiar with. It does not use RSI, MACD, or conventional moving average crossovers as primary signals.

Instead, MSA converts raw price data into momentum oscillator charts that visually resemble standard bar charts but measure price behaviour relative to long-term moving averages. The result is a structural picture of a market's momentum architecture — one that reveals whether a trend is genuinely changing at a deep level or simply experiencing surface noise.

A critical concept within MSA is what Oliver describes as momentum age. When an oscillator pattern has persisted for an extended period such as five to six months, it accumulates analytical weight. The longer a pattern holds without being resolved in the expected direction, the more significant the eventual breakout becomes.

Key MSA Buy Signals in Silver: A Documented Timeline

Oliver's framework has produced three major buy signals on silver in recent years, each confirmed by structural momentum breakouts rather than price chart patterns alone:

| Signal Period | Price Level | Structural Trigger |

|---|---|---|

| Early 2024 | ~$25 to $26 | Annual and quarterly momentum breakout |

| June 2024 | ~$35 | Third test of resistance confirms acceleration |

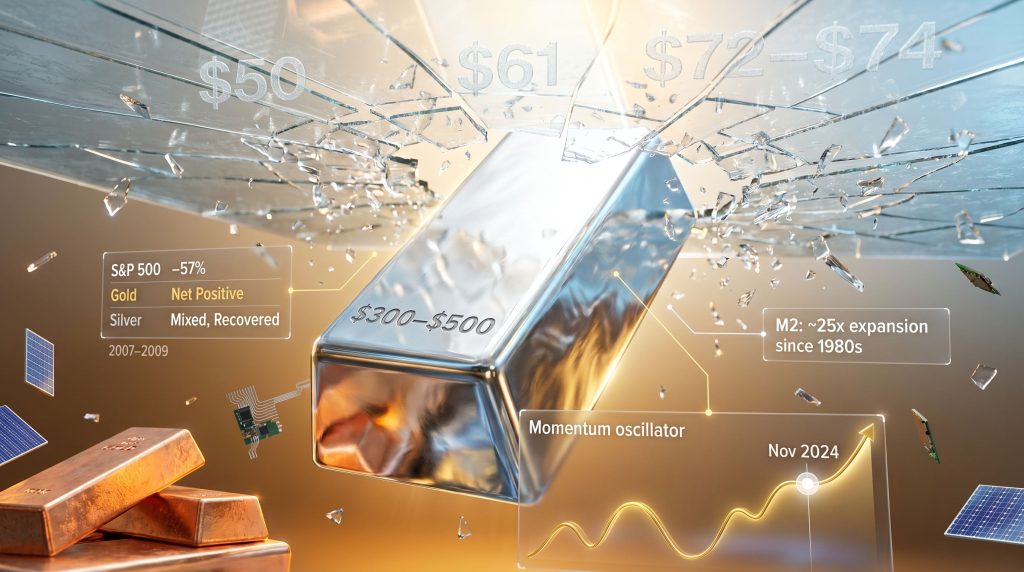

| November 2024 | ~$56 | 10-year ceiling on silver-to-gold spread broken |

The November 2024 signal is considered the most structurally consequential. Oliver's methodology involves dividing the silver price into the gold price, expressing the result as a percentage, and plotting it monthly. For a full decade prior to November 2024, this spread had maintained a ceiling at very low relative valuation levels for silver. That ceiling broke on the monthly close in November and, critically, has not been reclaimed — indicating a structural shift in silver versus gold valuations, not merely a temporary sentiment swing.

Silver's 50-Year Trading Box: An Anomaly Among Metals

To appreciate the magnitude of what may be unfolding, it is necessary to place silver's price history in comparative context. From roughly the mid-1970s through October 2024, silver traded within an approximate tenfold range, bottoming near $4 to $5 per ounce and repeatedly failing to sustain moves above $50. That $50 ceiling was tested in 1980, in 2011, and again in 2021 before each time retreating. No other major industrial or monetary metal exhibited this kind of sustained range compression over such an extended period.

Gold, by contrast, made vastly new highs during each successive bull cycle. Measuring from the 1976 bear market low, gold appreciated approximately eightfold by 1980. Starting from its 2001 bear low of roughly $256 per ounce, gold again achieved an approximately eightfold gain by 2011. Furthermore, in each case, prior highs were not revisited — new structural floors were established well above old ceilings.

Copper followed an analogous pattern. For multiple decades, copper traded between approximately $0.50 and $1.50 per pound. In late 2005, it punched above that $1.50 ceiling and within several quarters reached approximately $4.10. Copper has not traded back to $1.50 since. Lead mirrored this dynamic in 2007, achieving a similar multi-decade breakout in a vertical, compressed surge.

The Copper Precedent as a Logarithmic Framework for Silver

Oliver's logarithmic projection methodology applies the dimension of silver's historical trading range to its breakout level on a ratio scale. The calculation is straightforward in concept:

- Silver's historical range spanned approximately $4 to $50, representing roughly a tenfold dimension on a ratio scale.

- The breakout above the $50 ceiling, once confirmed and sustained, is treated as a base.

- Adding the tenfold dimension logarithmically to the breakout level produces a projection in the vicinity of $500 per ounce.

This is not a fundamental supply-demand forecast. It is a structural geometry argument — the same methodology that would have predicted copper's $4+ target from a $1.50 breakout using the same logarithmic framework.

The copper breakout of 2005 was not widely believed at the time. Analysts anchored to prior price history expected mean reversion. Instead, copper entered a new structural reality and established a new average well above its former ceiling. The silver case, when examined through the same analytical lens, produces a target range of $300 to $500.

Three Independent Analytical Pathways to $300 to $500 Silver

Oliver's price target is not derived from a single analytical thread. Three distinct frameworks independently converge on the same approximate range.

Scenario 1: The Monetary Supply Parity Framework

The Federal Reserve Bank of St. Louis publishes monthly M2 data going back to the early 1970s. That data shows an approximately 20 to 25-fold expansion in the US money supply from the early 1980s to the present. Gold has broadly tracked this expansion over the same period. However, silver has not. The gold-silver ratio analysis makes this divergence structurally apparent.

If silver were to merely catch up to the relative relationship to money supply growth that gold has already achieved, the implied price would sit in the $500 range from current levels. The gap between silver's current price and its implied monetary parity level represents decades of structural underperformance compressed into a single, unresolved divergence.

Scenario 2: The Government Bond Market Dislocation Framework

A second independent pathway to the $300 to $500 target runs through the bond market. The traditional 60/40 portfolio framework has functioned as the bedrock of institutional asset allocation for decades. That assumption is now being publicly questioned at the highest levels of institutional finance.

Morgan Stanley reportedly shifted its recommended allocation to a 60/20/20 framework, replacing a portion of bond exposure with gold. T-bond futures have been technically deteriorating, with yield highs from 2007 being tested. Furthermore, a New York Fed president indicated in November 2024 that the Fed would begin purchasing bonds under the guise of providing market liquidity — a tacit admission that the long end of the bond market requires active defence.

If US Treasury bonds lose their traditional portfolio hedge function, the capital that has historically rotated into bonds during equity drawdowns must find an alternative destination. With commercial real estate under structural pressure, that alternative — historically — has been monetary metals.

Scenario 3: The Equity Market Rotation Framework

Oliver's equity market analysis adds a third, independent catalyst pathway. MSA's work identifies the S&P 500 as having been in a topping process, with a distribution ceiling identified in the 6,900 to 7,000 zone over approximately six consecutive months. He draws a direct parallel to the momentum structure that preceded the 1987 crash.

Within the equity market, Oliver flags the financial sector as a specific area of weakness. The bank ETF KBE was sitting approximately 5% above its 2022 levels at the time of discussion — essentially flat over three years despite the broader market's advance.

Comparison: Equity Bear Markets and Precious Metal Performance

| Period | S&P 500 Approximate Decline | Gold Performance | Silver Performance |

|---|---|---|---|

| 1975 to 1980 (Stagflation) | Flat to weak | ~8x from 1976 low | Rose to ~$50 |

| 2000 to 2002 (Dot-com) | ~49% | Net positive | Positive |

| 2007 to 2009 (GFC) | ~57% | Net positive through cycle | Mixed, recovered strongly |

The distinguishing factor in the current cycle is the absence of T-bonds as a credible alternative. If bonds are no longer functioning in that role, the entirety of safe-haven rotation could flow into monetary metals, consequently compressing the repricing timeline for silver significantly.

Reading the Six-Month Consolidation: Accumulation or Distribution?

Since the January 2025 peak near $120, silver has been consolidating in a range that many observers have interpreted as a distribution top. However, Oliver's structural analysis reaches the opposite conclusion.

The sequence of events is analytically important:

- January 31, 2025: Silver collapsed to approximately $64 in a single session, establishing the initial range low.

- March 23, 2025: A deliberate stop-run pushed silver to approximately $61, below the February low, before recovering within hours and gaining approximately $10 within a week.

- June 2025 (interview date): Silver is trading either side of $70, with the most recent pullback representing the third test of support since the January low.

The stop-run on March 23 is particularly significant. When a market violates a prior low, triggers stop orders, and then reverses sharply within hours without any follow-through, it is characteristic of accumulation behaviour, not distribution.

The key momentum trigger level identified for upside confirmation is a sustained move into the $72 to $74 range. At that level, the third pullback would be confirmed as having failed, and the overhead momentum structure built over six months of consolidation would begin to resolve upward.

Why Fed Policy Is Irrelevant to the Structural Silver Thesis

A significant test of Oliver's framework came on the day of the interview. The Bureau of Labor Statistics reported 172,000 US jobs added in May — nearly double the Bloomberg consensus estimate of approximately 88,000. Silver sold off approximately 6 to 7% on the session.

Oliver's response is analytically instructive. His core position is that Fed policy is a trend-following mechanism, not a trend-making one. The historical evidence supports this view: during 1975 to 1980, the Federal Funds Rate reached approximately 14%, and gold and silver both surged dramatically during this period of extreme rate increases. From 2007 to 2009, emergency rate reductions failed to stabilise equities, while gold trended higher through the cycle.

There is, moreover, an additional often-overlooked point regarding employment data specifically. In both the 2000 and 2007 equity market tops, unemployment data did not deteriorate until well after markets had already declined 20% or more. Strong jobs data at a market top is not a contradiction of the topping thesis — historically, it is consistent with it.

The next major ASX story will hit our subscribers first

The Gold-Silver Spread and the Miner Confirmation Layer

Oliver's November 2024 buy signal was generated not from silver's price chart but from a spread chart — a structural shift in silver's relative valuation that remains intact today. The mining sector adds a secondary confirmation layer through the XAU-to-gold spread:

- The XAU-to-gold spread currently sits at approximately 8%.

- During the decades from the mid-1980s through approximately 2008, this spread oscillated between roughly 17.5% and 35%.

- The 2015 bear market low compressed the spread to approximately 4%, near historical minimum relative valuations for miners.

- The GDX, as an ETF, has an 11-year resistance line on this spread chart that has not yet been broken.

If the miner-to-gold spread breaks out of its 11-year basing structure, miners could double or triple in relative value versus gold. Silver miners, in Oliver's view, represent the most leveraged expression of this thesis.

For investors who do not want to select individual names, broad silver miner ETF exposure is identified as an accessible expression of this theme. Oliver's specific insight is that silver miners are likely to outperform gold miners in the period ahead, building on silver's established structural outperformance versus gold since November 2024.

Institutional Forecasts Versus Structural Analysis: The Regime-Change Gap

Mainstream bank forecasts for silver have clustered in the $80 range for 2025 year-end — representing roughly a 60 to 70% discount to the lower bound of Oliver's structural target. The divergence reflects a fundamental modelling difference.

Conventional commodity models are largely mean-reverting. They perform well during normal commodity cycles but break down in the presence of genuine structural regime changes. It is worth noting that even some institutional actors are beginning to acknowledge the magnitude of what may be occurring. JP Morgan reportedly published analysis projecting gold could reach approximately $9,200, which would represent roughly an eightfold move from gold's 2015 bear market low. If that gold target gains acceptance, the implied silver target through monetary parity analysis would be significantly above current mainstream forecasts. For additional context on the Michael Oliver $300 to $500 silver prediction, Michael Oliver's full interview provides a comprehensive breakdown of his MSA methodology.

Silver's Industrial Deficit: The Fundamental Layer Beneath the Monetary Thesis

While Oliver's framework is primarily momentum-driven, he acknowledges the fundamental demand layer beneath the structural thesis. Silver supply deficits have reportedly persisted for approximately five consecutive years, driven by accelerating industrial consumption across solar photovoltaic panels, electronics, and electric vehicles.

Furthermore, silver's dual nature as both a monetary metal and a critical industrial input creates a compounding demand dynamic. Monetary repricing pressure and industrial supply shortfalls are not competing narratives — they are additive forces bearing simultaneously on the same constrained supply base. Oliver characterises silver as having been money alongside gold for approximately 3,000 years, with its current underpricing representing a historical anomaly approaching resolution.

The Exit Strategy Problem: Planning for a $300 to $500 Silver Scenario

One of the most practically valuable aspects of Oliver's framework is his explicit discussion of what happens after the structural price target is reached. Oliver's own portfolio is described as approximately 95% in silver exposure, split roughly equally between silver bullion held through ETFs and silver mining equities.

His stated strategy upon reaching the target zone is to take profits and rotate into gold — not because he expects silver to collapse back to prior levels, but because gold represents monetary wealth preservation in a post-surge environment. His analogy to the NASDAQ is instructive: the internet fundamentally changed commerce, and yet the NASDAQ 100 still declined approximately 82% from its 2000 peak. Silver, after 50 years in a structural box, carries the risk of a similar excess high in its final surge phase.

A Framework for Position Management Across Silver's Structural Bull Cycle

| Phase | Price Range | Recommended Approach | Rationale |

|---|---|---|---|

| Current consolidation | $60 to $80 | Hold or accumulate on momentum signals | Bears failing to establish new lows; structure intact |

| Initial breakout | $80 to $120 | Maintain core position | Momentum overhead clearing; volatility remains high |

| Acceleration phase | $120 to $300 | Maintain exposure; monitor intermediate signals | Vertical phase most rapid and volatile |

| Excess high zone | $300 to $500+ | Begin systematic profit-taking | Excess moves followed by sharp corrections |

| Post-surge stabilisation | New structural floor | Rotate into gold | Gold as monetary preservation vehicle |

In addition, the silver squeeze dynamics currently unfolding in physical markets may accelerate the timeline of this framework considerably, particularly during the acceleration phase.

Frequently Asked Questions: The $300 to $500 Silver Thesis

What specific event would invalidate the structural silver bull case?

Oliver's framework is explicit about what would constitute structural failure rather than intermediate noise:

- A sustained break below the February 2025 low of approximately $61 with genuine follow-through, not a brief stop-run that reverses within hours.

- A structural reversal in the gold-silver spread back below the November 2024 breakout level, which has not occurred as of the interview date.

- A scenario in which government bond markets stabilise without central bank monetisation, removing the primary monetary debasement catalyst.

- A deflationary shock severe enough to simultaneously suppress all commodity demand and reverse monetary metals trends.

How does silver differ from gold in this analytical framework?

Gold is characterised as the primary monetary metal with a longer institutional adoption track record and central bank accumulation support. Silver, however, is a higher-beta expression of the same monetary debasement thesis, amplified by decades of structural underperformance relative to gold and a five-year industrial supply deficit. In Oliver's words, silver is in a tantrum, catching up to a monetary reality that gold has been reflecting for years.

Is this a guaranteed outcome?

No. This represents a long-duration, high-conviction speculative scenario derived from technical and macroeconomic structural analysis. It should be evaluated alongside mainstream institutional forecasts, independent supply-demand analysis, and individual risk tolerance. For a broader perspective on where silver prices could head, analysts' price forecasts from multiple sources offer useful supplementary context. Past structural breakout analogies in copper and lead do not guarantee identical outcomes for silver.

What is the post-$500 scenario?

Oliver speculates that the monetary and economic dislocations required to produce the Michael Oliver $300 to $500 silver prediction scenario would likely accompany a broader re-evaluation of monetary frameworks globally. He suggests the possibility of precious metals being re-legalised as currency in various jurisdictions as a consequence of fiat currency credibility loss at scale. This is presented as a speculative long-term scenario, not a near-term forecast, and represents one of the more unconventional dimensions of his broader thesis. Whether such a monetary reset materialises remains deeply uncertain and subject to profound political and institutional constraints that are beyond the scope of technical analysis alone.

Want to Identify the Next Major Commodity Breakout Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into actionable insights for both short-term traders and long-term investors — the same analytical edge that could position subscribers ahead of the next structural regime change in commodities. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial to secure a market-leading advantage.