May 17, 2026

The global energy sector stands at an unprecedented crossroads as traditional supply route dependencies face systematic disruption through naval interdiction strategies. Modern economies have constructed intricate petroleum distribution networks optimised for efficiency rather than resilience, creating vulnerabilities that geopolitical tensions can exploit with devastating economic consequences. Understanding these dynamics becomes essential as market participants navigate an environment where energy security assumptions undergo fundamental reassessment, particularly when examining the OPEC production impact on global markets.

Strategic Chokepoint Vulnerabilities Transform Oil Market Dynamics

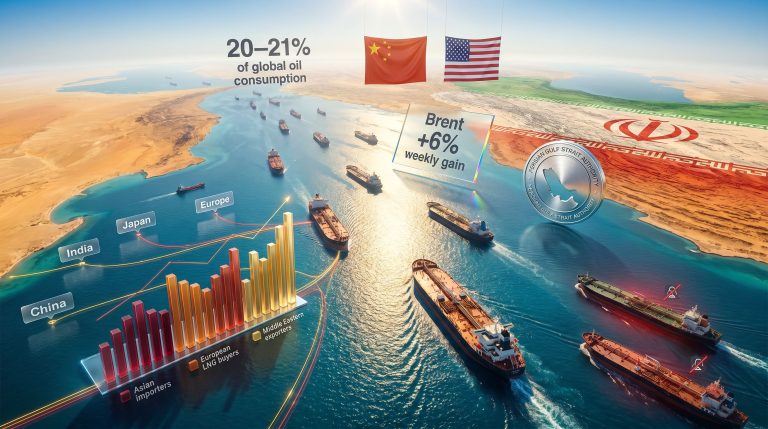

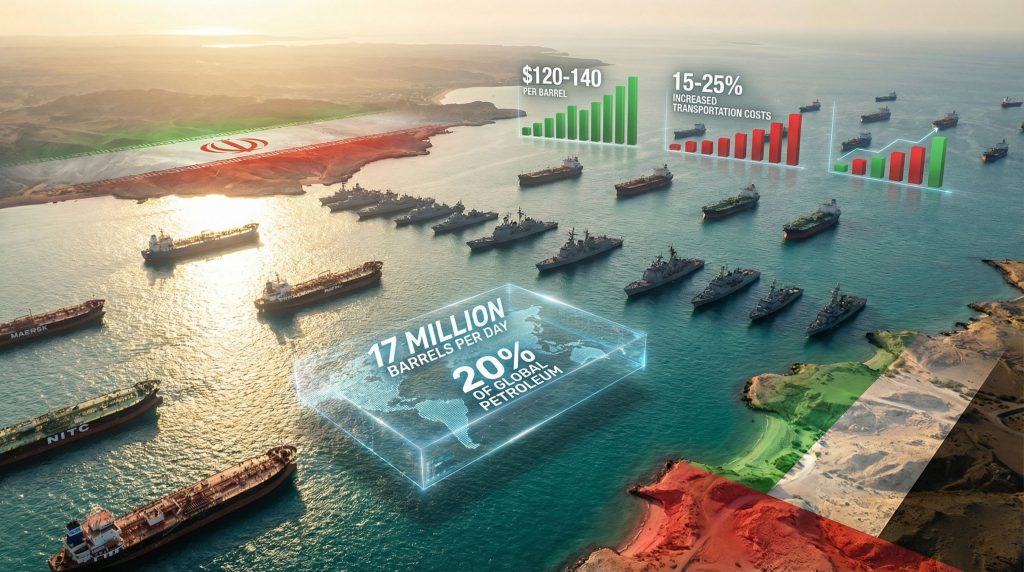

The Strait of Hormuz represents the world's most critical energy transit corridor, facilitating the movement of approximately 17 million barrels per day through a waterway spanning just 21 nautical miles at its narrowest point. Trump's Hormuz blockade has transformed theoretical supply disruption scenarios into immediate market realities, with Brent crude surging 7% to over $101 per barrel as of April 13, 2026.

Current market data reveals the immediate impact of escalating tensions:

- Oil prices: Brent crude exceeding $101/barrel after morning surge

- Natural gas futures: +2% movement to approximately $2.70 per gigajoule

- Australian dollar: Strengthening to 70.1¢ USD amid commodity rally

Critical Transit Volume Distribution

| Destination Region | Daily Volume (Million Barrels) | Economic Impact (USD Billions/Month) |

|---|---|---|

| Asia-Pacific | 12.3 | 45.2 |

| Europe | 2.8 | 10.1 |

| Americas | 1.9 | 6.8 |

The failure of U.S.-Iran peace negotiations in Pakistan has eliminated diplomatic resolution prospects, with escalation accelerating despite initial market underreaction. Transportation costs through alternative routes face 15-25% increases, while strategic petroleum reserves across major consuming nations prepare for coordinated releases to maintain market stability. Furthermore, the US oil production decline compounds supply concerns amid heightened geopolitical tensions.

When big ASX news breaks, our subscribers know first

Alternative Route Infrastructure Faces Capacity Constraints

Trump's Hormuz blockade forces immediate reassessment of global energy distribution architecture, highlighting the limitations of alternative transit corridors that have remained secondary considerations for decades. Pipeline networks through Central Asia, expanded Red Sea shipping capabilities, and overland transport systems now represent critical economic lifelines rather than backup options.

Primary Rerouting Mechanisms:

- Suez Canal expansion: Current throughput limitations create secondary bottlenecks requiring immediate capacity enhancement

- Trans-Arabian Pipeline reactivation: Dormant infrastructure necessitating rapid recommissioning and modernisation

- Caspian Sea route development: Multi-national coordination challenges requiring unprecedented diplomatic cooperation

The Qantas Project Sunrise initiative exemplifies corporate adaptation to Middle Eastern transit disruption, with new aircraft designs enabling non-stop Australia-Europe and Australia-Americas routes that bypass traditional Middle Eastern refuelling hubs. These operational adjustments demonstrate how Trump's Hormuz blockade forces systematic reconfiguration of global transportation networks.

Infrastructure Investment Requirements:

Alternative routing development demands immediate capital allocation toward previously overlooked transport corridors, fundamentally altering energy sector investment priorities and geographic risk assessments.

Arctic shipping routes gain strategic importance as climate change enables extended navigation windows, while transcontinental pipeline networks reduce dependence on maritime chokepoints susceptible to military interdiction. Energy companies must now evaluate permanent supply chain diversification strategies rather than temporary crisis management approaches.

Economic Scenario Modelling Reveals Escalation Pathways

Trump's Hormuz blockade creates three distinct economic trajectories based on enforcement duration and international response mechanisms. Each scenario carries specific market implications requiring differentiated portfolio positioning and risk management approaches.

Scenario Analysis Framework:

1. Short-Term Enforcement (30-90 Days)

- Oil price trajectory: $120-140 per barrel range

- Global inflation acceleration: 2-3 percentage points above baseline

- Strategic reserve coordination: Major economies maintaining market stability through coordinated releases

- Recession probability: Limited risk with appropriate monetary policy response

2. Extended Standoff (6-12 Months)

- Sustained energy pricing: Above $150 per barrel consistently

- Industrial sector impact: Production slowdowns in energy-intensive manufacturing

- Investment acceleration: Renewable energy project timelines compressed by 2-5 years

- Economic contraction: Stagflation characteristics with simultaneous inflation and growth deceleration

3. Military Escalation Scenario

- Peak pricing potential: Oil exceeding $200 per barrel during acute phases

- Export disruption: Complete Middle Eastern petroleum supply interruption

- Emergency protocols: Consumer rationing systems across major economies

- Structural transformation: Fundamental global energy architecture reconstruction

Current market positioning suggests 35% probability of diplomatic resolution within 60 days, 25% likelihood of direct military confrontation, and 40% chance of third-party international mediation efforts. However, the collapse of Pakistan-hosted negotiations has reduced diplomatic pathway viability significantly. Additionally, experts continue monitoring how this impacts natural gas forecasts for the coming months.

Australian Energy Markets Position for Supply Premium Capture

Australia's dual role as major energy exporter and import-dependent economy creates complex market dynamics during Trump's Hormuz blockade implementation. LNG production capabilities and Asian market proximity provide strategic advantages, while domestic energy costs and manufacturing competitiveness face pressure from global price increases.

ASX Energy Sector Positioning:

Santos (ASX:STO): LNG export capacity expansion gains strategic value as Asian buyers seek non-Middle Eastern supply sources. Existing long-term contracts provide pricing escalation opportunities while spot market exposure enables premium capture.

Woodside Energy (ASX:WDS): Established Asian supply relationships position the company for contract renegotiation premiums as supply scarcity intensifies. Geographic proximity to demand centres reduces transportation risks affecting Middle Eastern competitors.

BHP Group (ASX:BHP): Petroleum division benefits from supply shortage premiums while mining operations face increased energy input costs. Net exposure depends on production mix and hedging strategies.

Market Performance Indicators:

- Iron ore: Steady at $103.60/tonne in Singapore markets

- Gold: Maintaining stability at $4,689/ounce during crisis

- Currency impact: Australian dollar appreciation from commodity export revenues

Energy-intensive manufacturing sectors face margin compression as input costs escalate, while transportation and logistics companies adapt operational strategies to manage fuel price volatility. The divergent impact across industry sectors creates stock selection opportunities for investors capable of identifying relative value positions. Meanwhile, Australian energy export challenges require careful navigation amid this complex geopolitical landscape.

Geopolitical Risk Assessment Frameworks Guide Investment Strategy

Trump's Hormuz blockade represents a paradigm shift from theoretical geopolitical risk modelling to active crisis management requiring real-time probability assessment and scenario planning. Traditional diplomatic channels have proven inadequate, forcing market participants to develop alternative analytical frameworks for navigation uncertainty.

Coalition Response Dynamics:

- European Union coordination: Energy security cooperation mechanisms activating strategic reserve sharing protocols

- Chinese supply diversification: Alternative supplier relationship acceleration reducing Middle Eastern dependence

- Indian Ocean militarisation: Naval force positioning creating secondary shipping route vulnerabilities

Market sentiment reflects initial underestimation of escalation speed, with participants adjusting probability matrices upward for military confrontation scenarios. The rapid transition from diplomatic engagement to active blockade implementation demonstrates the inadequacy of traditional geopolitical risk models during crisis acceleration phases. According to recent naval blockade developments, the situation continues evolving rapidly.

Intelligence Assessment Integration:

Military analysts develop probability matrices for escalation pathways, incorporating naval capability assessments, economic resilience metrics, and diplomatic intervention potential to guide strategic decision-making processes.

Risk management frameworks must now incorporate non-linear escalation patterns where diplomatic failures trigger immediate military responses rather than graduated tension increases. This acceleration dynamic requires portfolio positioning capable of rapid adjustment as scenarios unfold.

Investment Positioning for Energy Security Disruption

Trump's Hormuz blockade creates investment opportunities across multiple asset classes while simultaneously generating portfolio risks requiring sophisticated hedging strategies. Traditional energy sector exposure provides obvious upside participation, but indirect beneficiaries and defensive positioning become equally important for comprehensive strategy development.

Strategic Asset Allocation:

Energy Infrastructure Exposure:

- Pipeline operators with non-Hormuz dependent networks capturing increased throughput premiums

- LNG terminal facilities in alternative geographic regions experiencing capacity utilisation increases

- Renewable energy developers benefiting from accelerated adoption timelines and government policy support

Defensive Positioning Mechanisms:

- Oil futures positioning: Long exposure capturing sustained price elevation during supply disruption

- Currency hedging: Managing import cost inflation impact on consumer-dependent sectors

- Strategic metals allocation: Energy transition acceleration increasing demand for battery materials and grid infrastructure components

Growth Opportunity Identification:

- Energy storage solutions: Grid stability requirements during supply disruption creating deployment acceleration

- Alternative fuel development: Government and private sector investment in supply chain independence

- Maritime security logistics: Shipping route optimisation and protection services experiencing demand growth

Technology companies developing energy independence solutions gain strategic value as governments prioritise domestic production capabilities. Defense contractors specialising in maritime security and logistics optimisation benefit from increased government spending on supply chain protection. Consequently, investors should also consider the broader oil price rally analysis when positioning portfolios.

The next major ASX story will hit our subscribers first

Long-Term Energy Architecture Transformation Accelerates

Trump's Hormuz blockade serves as a catalyst for structural energy system changes that extend far beyond immediate crisis resolution. Governments and corporations recognise single-point-of-failure vulnerabilities in current infrastructure, driving permanent investment toward redundancy and geographic diversification.

Permanent Infrastructure Development:

- Arctic shipping route expansion: Climate change enabling year-round navigation creating permanent alternative corridors

- Transcontinental pipeline construction: Overland networks reducing maritime chokepoint dependencies

- Distributed energy production: Localised generation reducing import vulnerability and transportation risks

Policy frameworks undergo fundamental reassessment as energy security becomes national security priority requiring immediate resource allocation. Strategic alliance formation for energy cooperation accelerates, while emergency petroleum reserve expansion programmes receive unprecedented government funding support.

Regulatory Response Evolution:

- Accelerated permitting processes: Alternative energy infrastructure receiving expedited approval mechanisms

- International cooperation agreements: Multilateral frameworks for crisis response and supply sharing

- Domestic production incentives: Tax policy and regulatory support for energy independence initiatives

The crisis demonstrates how geopolitical tensions can rapidly transform global economic architecture, forcing adaptation timelines that would normally require decades of gradual development. Market participants must recognise that Trump's Hormuz blockade represents not just a temporary disruption but a fundamental shift toward energy security prioritisation in investment and policy decision-making. As tensions continue, military analysts warn of potential escalation if diplomatic solutions remain elusive.

Market participants should carefully evaluate their exposure to energy price volatility and consider consulting qualified financial advisors before making investment decisions based on geopolitical scenarios. The analysis presented reflects current market conditions as of April 2026 and may not predict future outcomes accurately.

Want to Profit from Energy Security Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant energy and mineral discoveries across the ASX, empowering subscribers to identify actionable opportunities ahead of the broader market during volatile periods. Begin your 14-day free trial today to secure your market-leading advantage as geopolitical tensions reshape global commodity markets.