May 17, 2026

The Slow Fracture of the Open Seas: Why Beijing's Silence Is Fueling the Hormuz Crisis

Every generation or so, the global trading system encounters a stress test severe enough to expose the hidden assumptions holding it together. For decades, one assumption has stood above all others: that the world's critical maritime chokepoints remain accessible to all nations on equal commercial terms, underwritten by a combination of American naval power and a functional, if imperfect, multilateral order. That assumption is now being dismantled in real time, and the mechanism of its dismantling is not a missile strike or a naval blockade but something far more strategically corrosive: the deliberate, calculated silence of the world's second-largest economy at precisely the moment when decisive action could alter the trajectory of a global crisis.

Beijing's silence is fueling the Hormuz crisis in ways that conventional military and diplomatic analysis consistently underestimates. Understanding why requires moving beyond the event-driven framing of summits and statements, and into the deeper structural logic of how great powers manage crises when their interests are simultaneously aligned and opposed.

When big ASX news breaks, our subscribers know first

The Chokepoint That Cannot Be Replaced

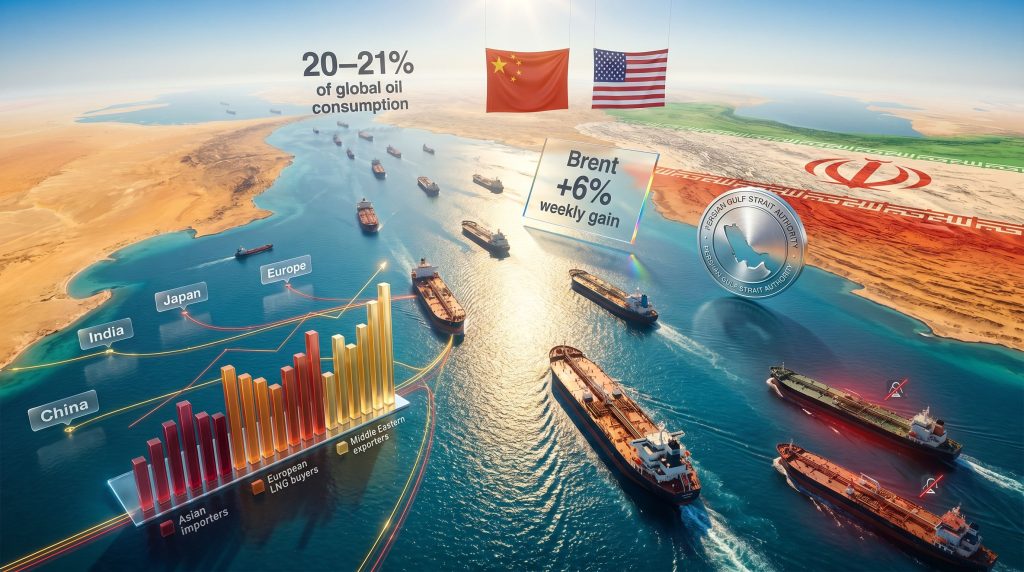

The Strait of Hormuz is not simply an important waterway. It is the singular, irreplaceable artery through which approximately 20 to 21 percent of total global oil consumption passes every day. No other maritime corridor carries this concentration of strategic consequence. The Suez Canal can be partially circumvented. The Red Sea has alternatives, however costly. Hormuz has none. The UAE's Abu Dhabi Crude Oil Pipeline offers limited bypass capacity, and even ADNOC's announced plans to double that capacity by 2027 will not come close to absorbing the full volume of Hormuz traffic.

This geographic reality creates a form of systemic leverage that no other waterway possesses. Any disruption to Hormuz does not merely affect the nations whose ships transit it. It instantaneously reprices energy across every downstream market on earth, amplifying geopolitical oil risks that were already elevated before the current crisis began.

The commodity data illustrates this with brutal clarity:

| Benchmark | Movement | Period |

|---|---|---|

| Brent Crude | +6% weekly gain | Current disruption period |

| WTI Crude | Surging | Current disruption period |

| India WPI (fuel component) | +25% | Recent reading |

| India Wholesale Price Index | 3.5-year high | May 2026 |

| Japan refinery utilisation | 73% | Current period, drawing strategic stocks |

| Chinese gasoline consumption forecast | -5.5% projected decline | 2026, if prices hold |

India's wholesale price index reaching a 3.5-year high with fuel costs up approximately 25% is not an abstraction. It represents direct, measurable economic pain cascading through one of the world's most import-dependent energy consumers. Two India-bound LPG tankers reportedly transited Hormuz in what shipping professionals describe as dark mode, meaning their Automatic Identification System transponders were disabled, a practice that reflects the depth of commercial risk aversion now pervasive in the Gulf.

What Insurance Markets Know That Politicians Won't Admit

One of the most analytically underappreciated dimensions of the current Hormuz disruption is the shift occurring in maritime insurance underwriting. War-risk insurance pricing functions as a real-time market signal of geopolitical risk, largely free from the diplomatic theatre that surrounds official government statements.

The critical insight here is that insurance markets are not pricing the current Hormuz situation as a temporary geopolitical shock. They are pricing it as a semi-permanent structural condition. This distinction carries profound implications for commercial shipping economics:

- Tanker owners are building geopolitical risk premiums into freight rates that previously would have been unimaginable outside wartime conditions

- Marine underwriters are restricting cover, demanding higher premiums, and in some cases declining Gulf voyages entirely

- Shipping financiers are reassessing the bankability of tanker assets with significant Gulf exposure

- Commercial charterers are restructuring voyage terms to account for routing uncertainty that was absent from contract templates even twelve months ago

The U.S. naval escort program publicly described as Operation Project Freedom has demonstrably failed to restore commercial confidence. The reason is instructive: military capability and commercial insurability are entirely separate requirements. Shipowners and marine underwriters require predictable, legally certain, insurable conditions. A naval escort guarantees neither the absence of incident nor the ability to claim against a policy should an incident occur. Furthermore, the Trump administration's inability to translate military presence into commercial confidence represents one of the most consequential strategic failures of the current crisis. For those engaged in commodity volatility hedging, this environment demands an entirely revised approach to Gulf exposure.

The Leverage Paradox at the Heart of Beijing's Position

China's relationship with Iran produces one of the most analytically complex strategic paradoxes in contemporary geopolitics. Beijing is Iran's largest single oil customer, purchasing Iranian crude at heavily discounted prices that reflect the sanctions environment Tehran operates within. This relationship theoretically endows China with enormous leverage over Iranian behaviour.

In practice, the leverage paradox operates in the opposite direction. China's dependency on discounted Iranian crude as a captive, sanctions-constrained supply source creates a structural disincentive to apply pressure that might alter that supply relationship. Every barrel of diplomatic pressure Beijing applies to Tehran risks accelerating Iranian political instability, reducing Iranian export capacity, or pushing Tehran toward more aggressive postures that increase transit disruption.

Three competing interpretations of Beijing's current posture deserve serious consideration:

- Passive beneficiary: China allows Hormuz instability to persist because elevated energy costs disproportionately burden Western-aligned economies while Beijing secures preferential access arrangements with Tehran

- Constrained mediator: China genuinely lacks sufficient influence over Iranian decision-making to produce a diplomatic breakthrough, despite the scale of the bilateral trade relationship

- Strategic position manager: Beijing is deliberately calibrating its public statements to signal general support for open waterways while avoiding any binding commitment that would constrain its Iran relationship or appear to align with Washington's strategic objectives

The most analytically honest assessment is that all three interpretations are simultaneously partially correct. Beijing's silence is not one thing. It is a layered, multi-purpose strategic instrument that achieves different objectives for different audiences at the same time.

Senior maritime and geopolitical analysts have noted that generalised calls for de-escalation from Beijing carry no operational weight unless accompanied by concrete pressure on Iranian maritime conduct. The observable gap between China's diplomatic language and its operational posture in the Gulf is itself a strategic communication to all parties. Source: OilPrice.com analysis by Cyril Widdershoven, May 2026

The Diplomat's analysis of the Hormuz crisis reinforces this reading, noting that China faces a genuine energy security dilemma that makes unequivocal support for open transit politically and economically costly. However, as the CSIS assessment has highlighted, even Beijing is not fully insulated from the consequences of prolonged Hormuz disruption, complicating any assumption that China is operating from a position of pure strategic comfort.

The Summit That Produced Its Most Important Output Through Absence

The Xi-Trump summit in Beijing was framed publicly by both sides as a stabilising event. The strategic reality was precisely the inverse. What the summit revealed was not diplomatic progress but the depth of structural incompatibility between the two powers on the single question most directly threatening global economic stability.

The Trump administration's public position was that Xi Jinping agreed the Strait of Hormuz must remain open. Chinese officials neither confirmed nor elaborated upon this characterisation in any binding way. The summit produced:

- No joint maritime-security framework for the Gulf

- No coordinated diplomatic roadmap for engaging Tehran

- No sanctions-relief mechanism linked to transit guarantees

- No multinational Hormuz stabilisation force proposal

- No joint shipping-security architecture

- No published agreement on energy market stabilisation

The absence of these outputs is not a negotiating footnote. It is the primary strategic signal. It indicates that U.S.-China distrust has reached a threshold at which joint crisis management of a shared systemic threat is no longer operationally viable, regardless of the economic incentives both parties have to resolve the situation. Consequently, the geopolitical trade tensions now reshaping global commerce are being compounded rather than contained.

Xi Jinping's explicit warning during the summit that mishandling Taiwan could produce clashes and conflicts introduced a second major maritime flashpoint into an already critically stressed environment. For energy and shipping markets, the simultaneous activation of Hormuz instability and Taiwan Strait tension represents a dual-chokepoint risk scenario without modern precedent.

Iran's Institutional Innovation: When Disruption Becomes Administration

A development that has received insufficient analytical attention is Iran's establishment of the Persian Gulf Strait Authority, a formal administrative body designed to regulate and monetise transit through the Strait of Hormuz. This represents a qualitative shift in the nature of the threat to maritime commerce.

Previously, Hormuz disruption was episodic, military, and unpredictable. Iran's institutionalisation of differentiated transit access transforms the nature of that threat fundamentally:

- Episodic disruption can be absorbed through strategic reserves and temporary routing changes

- Institutionalised access control requires permanent repricing of all commerce that depends on the strait

- Differentiated access by political alignment destroys the legal and commercial foundations of the open-market maritime system

Reports indicate that Chinese-flagged and Chinese-affiliated vessels have negotiated transit arrangements with Iranian authorities independently of the broader international shipping community. If accurate, this suggests Beijing is pursuing bilateral access management rather than multilateral stabilisation, a posture entirely consistent with the leverage paradox analysis above.

A world where Chinese-flagged tankers transit Hormuz freely while European and Japanese operators face prohibitive war-risk premiums does not produce one disrupted oil market. It produces two functionally separate global oil markets operating at structurally different cost bases, a fragmentation with implications extending far beyond energy pricing into the architecture of global trade itself.

The next major ASX story will hit our subscribers first

How Asia and Europe Are Hedging in Real Time

Import-dependent economies are not waiting for diplomatic resolution. They are adapting, at considerable cost, to what is increasingly being treated as the new baseline.

| Region | Primary Exposure | Hedging Strategy |

|---|---|---|

| India | LNG, LPG, crude imports | UAE reserve deal; Russian oil waiver extension; domestic fuel price increases |

| Japan | Crude oil imports | Strategic stock drawdown; refinery utilisation at 73% |

| Europe | LNG imports, refined products | Increased U.S. LNG dependency; storage mandate review |

| China | Iranian crude, Gulf energy | Bilateral transit arrangements; Sinopec ultra-deep shale gas expansion |

| Pakistan | LNG supply | Active diplomacy with Hormuz transit stakeholders |

India's dual-track approach is particularly instructive. New Delhi simultaneously signed emergency LPG and strategic oil reserve agreements with the UAE while pushing Washington to extend Russian oil import waivers as Indian imports from Russia reached record highs. This is not confusion. It is the rational hedging behaviour of a major economy that has concluded no single supplier or security guarantor can be relied upon exclusively.

Europe's position is arguably the most strategically precarious. European economies carry significant Hormuz exposure through LNG imports and refined product flows, yet the continent lacks any independent maritime-security doctrine for the Gulf. European dependence on U.S. LNG is set to surge further as Gulf supply routes become less commercially viable, deepening a strategic dependency that was already politically contentious before the current crisis. In addition, the European gas industry is simultaneously seeking relief from storage mandates that were designed for a different risk environment.

Four Scenarios for What Comes Next

Scenario A: Managed Bilateralism (Most probable near-term)

China and Iran maintain a de facto preferential access arrangement. U.S. naval presence continues. Commercial shipping adapts through higher costs, alternative routing, and elevated insurance premiums. Global energy markets gradually fragment into politically aligned supply corridors. No return to pre-crisis open-market dynamics.

Scenario B: Third-Party Mediated Framework (Low probability)

A mediating party, potentially Gulf Arab states, Turkey, or a UN mechanism, brokers a transit-access agreement acceptable to all major powers. Requires U.S.-China coordination that current strategic distrust renders operationally implausible in the near term.

Scenario C: Military Escalation and Full Closure (Tail risk)

Miscalculation or Iranian domestic political pressure triggers full Hormuz closure. Global oil prices spike to levels not seen since the 1970s energy crisis. Strategic petroleum reserves are activated globally; emergency rationing introduced in import-dependent economies.

Scenario D: Iranian Political Transition (Uncertain timeline)

Internal Iranian political dynamics produce a leadership willing to negotiate transit terms in exchange for meaningful sanctions relief. Requires U.S. diplomatic flexibility that current Washington posture does not suggest is available.

The most probable near-term trajectory is Scenario A: a costly, structurally damaging new normal in which Hormuz functions as a partially open, politically mediated corridor rather than a free international waterway. Energy market participants should price accordingly.

What This Means for Energy Market Participants

The strategic verdict emerging from the current Hormuz crisis is that Beijing's silence is fueling the Hormuz crisis in ways that extend well beyond any single diplomatic episode. It is a durable strategic condition reflecting the structural incompatibility of U.S. and Chinese interests in the Gulf. Furthermore, the trade war and oil dynamics already straining global energy markets are being amplified by this unresolved maritime standoff. For market participants, this requires a fundamental recalibration of risk frameworks:

- Shipowners and operators must treat elevated Gulf war-risk premiums and routing uncertainty as permanent inputs, not temporary exceptions

- Energy traders should incorporate a structurally elevated geopolitical risk premium into Gulf crude pricing models that does not revert to pre-crisis baselines on diplomatic announcements alone

- LNG buyers in Europe and Asia face compounding exposure as both supply route reliability and commodity pricing mechanisms are simultaneously disrupted

- Maritime insurers and shipping financiers must recalibrate risk models to reflect a world where major chokepoints are no longer reliably accessible as open international waterways

- Policymakers in import-dependent economies must accelerate investment in strategic reserve capacity, supply diversification, and independent maritime-security capabilities

The foundational assumption of the modern global energy trading system — that maritime arteries remain open and protected by American naval dominance and multilateral cooperation — is under strain of a kind not experienced in the post-Cold War era. OPEC's market influence adds yet another layer of complexity to an already fraught environment. The Xi-Trump summit's failure to produce any stabilising mechanism has not simply left that assumption unrepaired. It has accelerated the timeline of its unravelling.

Markets that continue pricing Hormuz risk as a temporary geopolitical shock rather than a structural transition are not engaging in optimism. They are engaging in denial.

This article is intended for informational and analytical purposes only. It does not constitute financial or investment advice. All forward-looking statements, scenario projections, and market analyses involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent research and consult qualified advisors before making investment decisions.

Want to Capitalise on the Commodity Volatility Reshaping Global Energy Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex market shifts into actionable investment opportunities for traders and long-term investors alike — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.