July 20, 2026

Global energy markets operate within an intricate web of geopolitical vulnerabilities, where single chokepoints can trigger cascading effects across continents. Among these critical junctures, few possess the transformative power of maritime passages that control the flow of essential commodities. When transportation corridors face disruption, the resulting market dynamics extend far beyond immediate supply constraints, reshaping investment strategies, industrial policies, and international relations for years to come. Understanding the Iran Strait of Hormuz closure scenario requires examining not just the immediate tactical responses, but the strategic adaptations that emerge when critical infrastructure faces sustained pressure.

Furthermore, the complexity of modern energy security reveals itself most starkly during periods of potential supply disruption, when financial markets must rapidly price in scenarios ranging from temporary inconvenience to fundamental restructuring of global trade flows.

Maritime Chokepoints and Global Energy Vulnerability

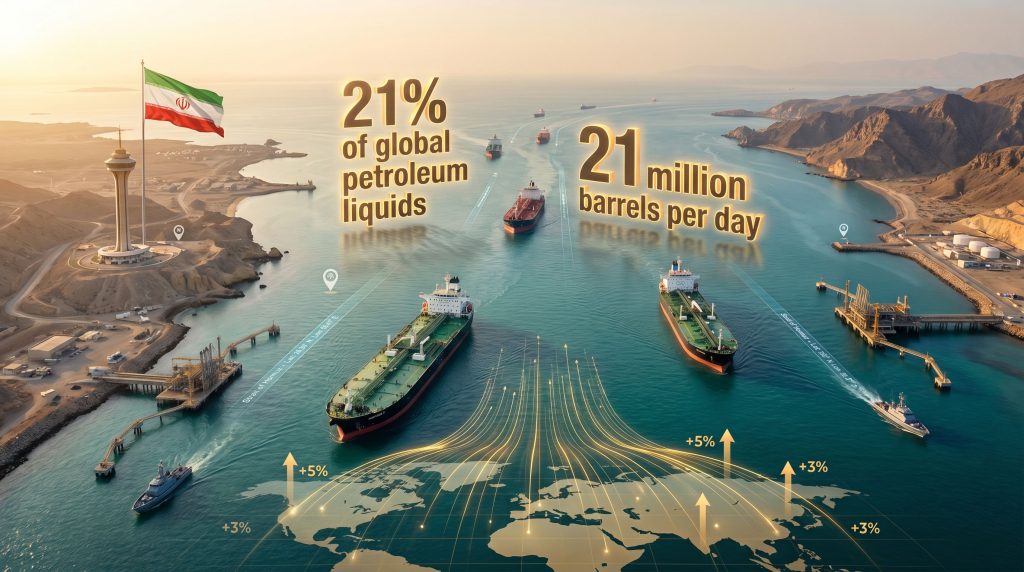

The strategic significance of the Strait of Hormuz extends beyond its geographic position, representing a fundamental pressure point in the global energy system. Recent market data from April 2026 illustrates this vulnerability in real terms. According to vessel tracking information from Kpler, more than 20 ships carrying oil products, metals, gas, and fertilizer transited the waterway on April 19, 2026, marking the busiest single day since March 1 of that year.

This operational baseline becomes critical when examining market responses to potential disruption. Brent crude futures demonstrated immediate sensitivity, rising approximately 5% to $95.16 per barrel as geopolitical tensions escalated in the region. The price movement reflected not just current supply concerns, but broader market recognition of the strait's irreplaceable role in global energy flows, contributing to an oil price rally that rippled across international markets.

Key Regional Dependencies:

- Asian refineries rely heavily on Middle Eastern crude supplies

- European markets face limited alternative routing options

- North American shale production cannot immediately offset Middle Eastern volumes

- Strategic petroleum reserves provide only temporary supply buffers

The economic mathematics of chokepoint vulnerability become apparent when examining alternative transportation costs. Rerouting shipments around the Cape of Good Hope adds approximately 14 days to transit times, significantly increasing transportation costs and working capital requirements for energy companies. These additional expenses ultimately transmit through the entire supply chain, affecting everything from petrochemical feedstocks to consumer fuel prices.

International maritime law frameworks governing passage rights add another layer of complexity. While the United Nations Convention on the Law of the Sea establishes principles for transit passage through international straits, enforcement mechanisms during periods of heightened tension remain limited. This legal ambiguity contributes to market uncertainty and risk premium calculations.

When big ASX news breaks, our subscribers know first

Financial Market Responses During Energy Supply Disruptions

Market psychology during potential energy supply disruptions reveals distinct patterns across asset classes and geographic regions. The April 2026 market response demonstrated these dynamics clearly, with equity markets showing divergent reactions based on regional exposure to energy price volatility. Moreover, the US-China trade war impact added additional complexity to global market dynamics during this period.

Global Equity Market Performance (April 20, 2026):

| Market Index | Performance | Regional Context |

|---|---|---|

| S&P 500 Futures | -0.6% | Energy cost concerns for US manufacturers |

| European Futures | -1.1% | High dependence on energy imports |

| Hong Kong Hang Seng | +0.8% | Relative insulation from immediate supply disruption |

| Japan Nikkei | +1.0% | Diversified energy procurement strategies |

| South Korea KOSPI | +1.4% | Strong domestic industrial base |

| Taiwan Index | Record High | Technology sector resilience |

The divergent performance patterns reflect underlying economic structures and energy dependencies. Asian markets, despite geographic proximity to potential disruption zones, demonstrated remarkable resilience. This counterintuitive response stems from several factors: diversified energy procurement strategies, substantial strategic reserves, and economic structures less immediately vulnerable to short-term energy price spikes.

Bond markets provided additional insight into investor sentiment and inflation expectations. The 10-year U.S. Treasury yield climbed 2.2 basis points to 4.266%, indicating market concerns about potential inflationary pressures from sustained energy price increases. This yield movement suggests investors were pricing in scenarios extending beyond temporary supply disruption.

Currency markets reflected the complex interplay between safe-haven demand and commodity price inflation. The U.S. dollar strengthened to 158.8 yen and traded at $1.1760 per euro, demonstrating its continued role as a crisis currency despite potential negative impacts from higher energy costs on the American economy.

Financial institution responses provided forward-looking indicators of economic impact expectations. National Australia Bank's announcement of a $500 million impairment charge reflected institutional preparation for increased credit risks stemming from energy price volatility and economic uncertainty.

Alternative Energy Infrastructure and Supply Route Analysis

The development of alternative energy transportation routes represents a critical component of long-term energy security strategy. When primary chokepoints face disruption, the capacity and reliability of backup infrastructure determine both immediate market stability and longer-term supply chain resilience. Additionally, the LNG market implications of such disruptions create significant investment opportunities across various sectors.

Primary Alternative Route Options:

- UAE Pipeline Infrastructure: The Fujairah bypass pipeline provides approximately 1.8 million barrels per day of capacity, offering partial mitigation for strait closures

- Suez Canal Route: Mediterranean access reduces dependence on Gulf transportation, though capacity limitations and canal vulnerability create additional risk factors

- Cape of Good Hope: Traditional alternative requiring significant additional transit time and vessel capacity

- Overland Pipeline Networks: Central Asian and Turkish routes provide limited but strategically important alternatives

The economic viability of alternative routes depends heavily on duration expectations and price differentials. Short-term disruptions favour expensive but rapid alternatives, while extended closures justify infrastructure investments in longer-term routing solutions. This calculation affects everything from tanker charter rates to pipeline expansion financing.

Strategic petroleum reserve policies across major consuming nations provide another layer of supply security. The International Energy Agency coordinates release mechanisms among member countries, with approximately 60 days of emergency supply available through coordinated deployment. However, reserve utilisation represents a finite resource requiring careful management during extended disruption periods.

National Reserve Capacities and Policies:

- United States: Strategic Petroleum Reserve maintains approximately 714 million barrels

- China: National reserves estimated at 500+ million barrels with ongoing expansion

- Japan: 324-day import requirement maintained through government and private reserves

- European Union: 90-day import equivalent distributed across member states

Refinery adaptation capabilities represent a crucial but often overlooked component of supply chain flexibility. Different crude oil grades require specific processing configurations, and rapid switching between supply sources can take 2-4 weeks for full optimisation. This adaptation period creates temporary inefficiencies and potential product quality variations during supply transitions.

Long-Term Energy Market Structural Transformations

Sustained energy supply disruptions accelerate structural changes that might otherwise develop over decades. Investment priorities shift rapidly as market participants reassess the reliability of traditional supply chains and the economic viability of alternative energy sources. In this context, gold safe-haven insights become particularly relevant for investors seeking portfolio protection during uncertain periods.

Renewable Energy Investment Acceleration

The relationship between fossil fuel price volatility and renewable energy investment follows predictable patterns. Higher oil and gas prices improve the relative economics of solar, wind, and battery storage projects, leading to accelerated deployment timelines and increased financing availability. However, renewable energy infrastructure development requires 3-5 years for significant capacity additions, limiting immediate supply substitution capabilities.

LNG Infrastructure Development Priority

Liquefied natural gas projects gain strategic importance during Middle Eastern supply disruptions. Floating LNG terminals offer rapid deployment capabilities, providing energy security benefits that justify premium pricing. American and Australian LNG exports become particularly valuable, with long-term contract negotiations reflecting geopolitical risk premiums.

Nuclear power renaissance considerations become more prominent as energy import-dependent nations reconsider nuclear policies during sustained fossil fuel supply uncertainty. Nuclear projects require 10-15 year development timelines, making them strategic rather than tactical responses to current crises. However, policy framework development and site preparation can begin immediately, positioning countries for long-term energy independence.

Battery storage and grid modernisation investments accelerate as utilities seek to maximise renewable energy utilisation and improve system resilience. Grid-scale battery deployment can provide both energy storage and frequency regulation services, improving overall system reliability during supply disruptions.

Regional Geopolitical Responses and Naval Security Strategies

Maritime security arrangements evolve rapidly during chokepoint crises, with regional powers adapting naval deployment strategies and international cooperation frameworks to maintain commercial shipping flows. The Iran Strait of Hormuz closure scenario illustrates these complex dynamics across multiple dimensions.

The current geopolitical situation, as of April 2026, illustrates these dynamics. A ceasefire between Iran and the U.S. was scheduled to expire on April 21, 2026, but faced immediate challenges following the U.S. seizure of an Iranian cargo vessel and Tehran's subsequent retaliation threats. According to CNN's live coverage of the Iran war developments, Iran rejected new peace talks with the United States while President Trump indicated he was dispatching envoys for discussions in Pakistan.

Naval Coalition Formation Strategies:

- U.S. Fifth Fleet: Maintains permanent Gulf presence with enhanced escort capabilities during crisis periods

- European Naval Coordination: Joint EU maritime mission provides merchant vessel protection

- Regional Gulf State Cooperation: UAE, Saudi Arabia, and Kuwait coordinate coastal defence systems

- Insurance Market Adaptation: Lloyd's of London war risk committees adjust coverage terms and pricing

Pakistan's potential mediation role reflects the complex diplomatic landscape surrounding energy chokepoint security. Historical precedents suggest successful mediation requires economic incentives for all parties, including guaranteed market access and revenue sharing arrangements that address underlying economic pressures driving conflict.

Qatar's position as both a regional power and major LNG exporter provides unique diplomatic leverage. Qatar's LNG infrastructure remains largely protected from direct conflict, allowing continued energy exports that generate revenue for diplomatic initiatives and regional stability programmes. As reported by the BBC's analysis of the crisis, regional diplomatic efforts continue despite ongoing tensions.

Investment Strategy Implications During Energy Crisis Periods

Energy security crises create distinct investment opportunities across multiple asset classes, with timing and positioning strategies determining portfolio performance during volatile periods. For investors navigating these complex markets, consulting a comprehensive commodity investment guide becomes essential for understanding exposure options and risk management strategies.

Commodity Market Positioning

Oil futures markets during geopolitical uncertainty require careful risk management balancing potential upside from supply disruption against downside risks from demand destruction. Brent crude's 5% single-day increase to $95.16 demonstrates the velocity of price movements during crisis periods, requiring sophisticated hedging strategies for both producers and consumers.

Natural gas price arbitrage opportunities emerge as regional markets decouple during supply disruptions. European natural gas prices typically experience larger volatility than North American markets during Middle Eastern crises, creating inter-regional trading opportunities for sophisticated market participants.

Precious metals often benefit from safe-haven demand during energy crises, though the relationship depends on broader economic conditions and currency market dynamics. Gold and silver prices typically rise during initial crisis phases but may face pressure if central banks raise interest rates to combat energy-driven inflation.

Infrastructure Investment Themes

- Maritime Security Technology: Vessel tracking, communication systems, and automated defence platforms

- Energy Storage Solutions: Grid-scale batteries, pumped hydro storage, and compressed air systems

- Pipeline Expansion Projects: Alternative route development and capacity enhancement initiatives

- Floating LNG Terminals: Rapid deployment energy import/export capabilities

Equity Sector Performance Analysis:

| Sector | Crisis Performance | Duration Sensitivity |

|---|---|---|

| Upstream Oil & Gas | Immediate beneficiary | High price sensitivity |

| Renewable Energy | Medium-term beneficiary | Policy-dependent |

| Shipping Companies | Mixed results | Route-dependent |

| Utilities | Defensive positioning | Fuel cost exposure |

| Manufacturing | Negative impact | Energy intensity factor |

The next major ASX story will hit our subscribers first

Economic Winners and Losers in Regional Supply Disruption Scenarios

Energy supply disruptions create asymmetric economic impacts across regions and sectors, with some areas benefiting from higher prices while others face severe economic strain. The Iran Strait of Hormuz closure scenario demonstrates these divergent outcomes across multiple economic sectors.

Middle Eastern Economic Divergence

Saudi Arabia and the UAE typically benefit from higher oil prices during Iranian supply disruptions, as their production capacity can partially offset lost Iranian output. Spare production capacity becomes a strategic asset, allowing these nations to capture premium pricing while maintaining market share. However, regional instability creates offsetting risks to infrastructure and investment confidence.

Kuwait and Iraq face more complex challenges due to their geographic proximity to potential conflict zones and dependence on shared transportation infrastructure. Export route diversification becomes critical for maintaining revenue flows during extended disruption periods.

Qatar's LNG market positioning provides relative isolation from oil market volatility while creating opportunities for premium pricing in constrained gas markets. Qatar's North Field expansion projects gain strategic importance as global markets seek supply security and long-term contract availability.

Global Manufacturing Impact Assessment

Petrochemical industry participants face immediate input cost pressures, with ethylene and propylene prices rising rapidly during crude oil supply disruptions. Downstream manufacturers of plastics, synthetic fibres, and specialty chemicals experience margin compression and potential production curtailments.

Transportation fuel costs affect logistics and distribution networks across all economic sectors. Airlines face particularly acute pressure from jet fuel price increases, while shipping companies may benefit from higher freight rates that more than offset increased bunker fuel costs.

Industrial energy intensity determines sectoral vulnerability to sustained energy price increases. Steel, aluminium, and cement production face significant cost pressures, potentially leading to production shifts toward regions with more stable energy costs and supply security.

Crisis Resolution Pathways and Market Recovery Scenarios

Market participants continuously assess the probability and timeline for crisis resolution, with these expectations driving both short-term trading strategies and long-term investment decisions. Understanding potential resolution pathways helps investors position portfolios for various outcome scenarios.

Based on expert analysis during the April 2026 situation, resolution expectations remained cautiously optimistic despite immediate tensions. Paul Chew from Phillip Securities noted that the base case scenario continued to favour war resolution, with President Trump maintaining focus on November midterm elections as a key motivating factor for diplomatic progress.

Damien Boey from Wilson Asset Management provided additional perspective on market sentiment, observing that while headlines appeared concerning and suggested disagreement leading to re-escalation, both sides ultimately appeared motivated to reach an agreement, contributing to market optimism and limiting sell-offs.

Historical Resolution Pattern Analysis:

- 1980s Tanker War: Resolution required international naval intervention and economic pressure

- 1990-1991 Gulf War: Swift military resolution with immediate market normalisation

- 2019 Tanker Incidents: Diplomatic pressure and economic sanctions avoided escalation

Post-Crisis Market Structure Evolution

Successful crisis resolution typically results in permanent changes to energy market structure and risk management practices. Middle Eastern crude oil may carry permanent risk premiums reflecting demonstrated vulnerability to geopolitical disruption. Enhanced strategic reserve policies become standard practice among major consuming nations.

Maritime security infrastructure investments continue beyond immediate crisis resolution, creating long-term demand for naval vessels, surveillance systems, and communication networks. Energy diplomacy frameworks require restructuring to address underlying tensions and create sustainable conflict prevention mechanisms.

Recovery Timeline Scenarios:

- Immediate Normalisation (2-4 weeks): Markets return to pre-crisis levels with minimal structural change

- Gradual Reopening (2-6 months): Phased restoration of normal shipping with ongoing risk premiums

- Extended Disruption (6+ months): Fundamental restructuring of supply chains and alternative route development

Risk Management Frameworks for Energy Security Investment

Effective risk management during energy security crises requires sophisticated frameworks that address both immediate volatility and long-term structural changes in global energy markets. The Iran Strait of Hormuz closure scenario demonstrates the importance of comprehensive risk assessment across multiple dimensions.

Portfolio Diversification Strategy

Energy sector exposure optimisation requires balancing potential upside from higher prices against downside risks from demand destruction and economic recession. Geographic diversification across oil-producing regions reduces concentration risk while maintaining energy sector participation.

Renewable energy investment acceleration timing becomes crucial during fossil fuel supply disruptions. Solar and wind project development benefits from improved economics relative to volatile fossil fuel alternatives, but requires careful attention to supply chain dependencies and construction timeline risks.

Currency hedging considerations become complex for energy-importing nations during supply disruptions. Petroleum product imports require foreign currency, typically U.S. dollars, creating additional exposure to exchange rate volatility during crisis periods. Central bank intervention capabilities and international reserve adequacy affect hedging strategy effectiveness.

Corporate Supply Chain Resilience Planning

Energy procurement strategy modifications require balancing cost optimisation with supply security objectives. Long-term contracts provide price stability but may limit flexibility to capture spot market opportunities during surplus periods.

Transportation route diversification requirements extend beyond energy commodities to affect all internationally traded goods. Inventory management policies require adjustment to account for longer lead times and higher transportation costs during crisis periods.

Force majeure clause activation and insurance claims processes become critical during extended supply disruptions. Legal frameworks governing supply contract suspension vary significantly across jurisdictions and commodity types, requiring specialised expertise for effective risk management.

Investment Risk Assessment Framework:

| Risk Category | Assessment Criteria | Mitigation Strategies |

|---|---|---|

| Geopolitical Risk | Regional stability indicators | Geographic diversification |

| Price Volatility | Historical volatility patterns | Options hedging strategies |

| Supply Chain Risk | Alternative route availability | Multi-supplier agreements |

| Currency Risk | Exchange rate correlation | Forward contract hedging |

| Regulatory Risk | Policy change probability | Compliance monitoring systems |

The intersection of geopolitical tensions with energy market dynamics creates complex investment environments requiring sophisticated analytical frameworks and adaptive strategies. Success depends on understanding both immediate market mechanics and longer-term structural transformations that emerge from sustained supply chain disruptions.

This analysis is based on market conditions and geopolitical developments as of April 2026. Energy markets remain highly volatile and subject to rapid changes in geopolitical conditions, supply chain dynamics, and regulatory frameworks. Investors should consult qualified financial advisors and conduct independent research before making investment decisions in energy-related assets or during periods of geopolitical uncertainty.

Considering investments during energy market volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mining and exploration discoveries that often benefit during commodity price surges and supply disruptions, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Visit Discovery Alert's discoveries page to understand how major mineral discoveries can generate substantial returns during periods of market uncertainty, then begin your 14-day free trial to position yourself ahead of the market.