June 12, 2026

Revolutionising Resource Control in Modern Industrial Networks

The intricate architecture of modern industrial supply networks reveals a fundamental tension between efficiency and resilience that extends far beyond conventional commodity markets. Furthermore, as global economies increasingly depend on specialised materials for technological advancement, the strategic importance of resource control becomes magnified through geographic concentration and processing capabilities. This dynamic has reached critical significance in the battery materials sector, where demand growth trajectories intersect with supply chain vulnerabilities to create profound market implications for the global lithium supply chain over the coming decade.

When big ASX news breaks, our subscribers know first

How Does Global Lithium Supply Chain Architecture Shape Market Control?

The global lithium supply chain operates through a three-tier structure that creates distinct leverage points for market participants. Mining operations form the foundation, where extraction methods determine both cost structures and geographic constraints. However, processing facilities represent the critical transformation stage, converting raw materials into battery-grade products through capital-intensive operations. Finally, integration into battery manufacturing creates the ultimate demand pull that drives pricing dynamics across the entire network.

Concentration Patterns in Mining Operations

Mining concentration has evolved significantly over the past decade, with production shifting toward fewer but larger-scale operations. Australia dominates hard rock lithium extraction, producing approximately 55,000 tonnes of lithium carbonate equivalent annually, representing 42% of global mining output according to U.S. Geological Survey data. Moreover, the country's Greensboro operations, managed by Pilbara Minerals, exemplify this concentration trend through integrated spodumene extraction and initial processing capabilities.

South American brine operations follow a different concentration pattern, where geographic constraints limit viable extraction sites to specific high-altitude regions. Chile's Atacama Desert hosts operations producing approximately 37,000 tonnes of lithium carbonate equivalent, representing roughly 28% of global production. In addition, these brine-based systems offer lower operating costs, typically ranging from $6,000 to $8,000 per tonne compared to $10,000 to $14,000 per tonne for hard rock alternatives.

The concentration metrics reveal strategic implications beyond simple production volumes. Major operators like Albemarle, SQM, and Livent historically controlled approximately 50% of global output, though this share has declined as new entrants expand capacity. Consequently, this evolution suggests that while mining remains concentrated, the degree of concentration may decrease as demand growth attracts additional investment.

Processing Bottlenecks and Refining Capacity Distribution

Processing capacity represents the most significant bottleneck in the global lithium supply chain architecture. China controls approximately 60% of global lithium processing capacity, according to International Energy Agency analysis, creating a structural asymmetry between mining and processing capabilities. This concentration enables Chinese processors to influence global pricing and market access regardless of mining location.

The processing stage requires substantial infrastructure investments, typically ranging from $500 million to $1.5 billion for greenfield facilities capable of producing battery-grade materials. These operations demand specialised chemical inputs including sulfuric acid, lime, and hydrochloric acid, creating secondary supply dependencies that compound concentration risks. Furthermore, energy intensity adds another constraint, with processing requiring 8-12 MWh per tonne of lithium carbonate equivalent produced.

Processing capacity utilisation rates vary significantly by region and technology. Chinese facilities typically operate at 80-90% capacity during peak demand periods, while Western processing capacity remains limited. This utilisation differential creates pricing power for established processors and extends lead times for new market entrants seeking processing services.

Battery Manufacturing Ecosystem Dynamics

Battery manufacturing represents the final concentration point in lithium value creation, where China controls approximately 65-70% of global cell production capacity. This vertical integration from processing through manufacturing creates compound leverage effects, where Chinese companies can optimise material flows across multiple supply chain stages simultaneously.

The integration pattern differs markedly from Western approaches, where companies typically specialise in individual supply chain segments. Ganfeng Lithium exemplifies this integrated model through ownership positions spanning Argentine mining operations, Chinese processing facilities, and downstream battery material production. Consequently, their 2023 processing capacity exceeded 300,000 tonnes of lithium carbonate equivalent across all facilities.

Battery chemistry evolution influences concentration dynamics as manufacturers optimise for different performance characteristics. Lithium iron phosphate batteries require different material specifications compared to nickel manganese cobalt alternatives, creating segmented demand patterns that affect processing requirements and market positioning strategies.

What Are the Critical Vulnerabilities in Current Lithium Supply Networks?

Supply chain vulnerabilities manifest through multiple vectors that create cascading risk scenarios for market participants. Geographic concentration, processing dependencies, and transportation chokepoints combine to create systemic fragilities despite operational efficiency under normal conditions. However, these vulnerabilities have demonstrated material impact through recent disruption events that highlighted structural weaknesses in current network architecture.

Geographic Risk Concentration Analysis

The "Lithium Triangle" comprising Argentina, Bolivia, and Chile contains approximately 58% of global lithium reserves, creating significant geographic concentration risk. Argentina brine insights reveal that the Atacama region alone holds estimated reserves of 9.2 million tonnes of lithium metal equivalent, while Chile possesses approximately 9.3 million tonnes according to U.S. Geological Survey assessments. This concentration means that regional disruptions can impact global supply availability significantly.

Weather dependency creates additional geographic vulnerabilities, particularly for brine operations that rely on specific climatic conditions for evaporation processes. Heavy rainfall in Argentina's lithium-producing regions during 2022-2023 disrupted brine evaporation operations, reducing production by approximately 30% in affected areas. This single weather event contributed to global price volatility and demonstrated how localised conditions can cascade through international markets.

Political stability represents another geographic risk factor, where policy changes or regulatory modifications can affect production timelines and investment attractiveness. Bolivia's substantial reserves of approximately 23 million tonnes remain largely undeveloped due to historical political constraints and infrastructure limitations, producing only 400 tonnes of lithium carbonate equivalent in 2023 despite massive resource potential.

Single-Point-of-Failure Assessment in Processing

Processing concentration in China creates multiple single-point-of-failure scenarios that could disrupt global supply chains. With 60% of processing capacity concentrated in one country, disruptions affecting Chinese operations would impact global battery-grade lithium availability significantly. Furthermore, energy rationing during 2021-2022 peak demand periods temporarily constrained Chinese processing volumes, causing shipment delays and highlighting infrastructure vulnerabilities.

Chemical input dependencies compound processing vulnerabilities through secondary supply chain risks. Lithium processing requires substantial quantities of sulfuric acid, with a typical 10,000 tonne capacity facility consuming over 10,000 tonnes annually. Disruptions to chemical suppliers would cascade through lithium production, creating compound effects that extend beyond primary processing operations.

Processing facility lead times create temporal vulnerabilities where supply disruptions cannot be quickly resolved through capacity additions. New processing plants require 3-5 years from initial investment to production capacity, meaning that current processing bottlenecks persist until planned facilities become operational. Consequently, this temporal mismatch between disruption response times and capacity development creates persistent vulnerability windows.

Cascading Impact Scenarios from Supply Disruptions

Supply chain disruptions demonstrate amplification effects as constraints propagate through interconnected systems. The 2020-2021 logistics disruptions caused lithium prices to spike from approximately $6,000 per tonne to over $15,000 per tonne in 2022, illustrating how transportation bottlenecks can create price volatility that exceeds the scale of physical supply reductions.

Port infrastructure represents a critical vulnerability point where cargo concentration creates cascading risk potential. Major lithium shipments flow through specific port facilities in Australia, Chile, and China, meaning that port disruptions or congestion can affect multiple production streams simultaneously. Container shipping constraints during pandemic periods demonstrated how logistics bottlenecks cascade through global supply networks.

Inventory management practices throughout the supply chain influence disruption amplification effects. Just-in-time inventory approaches optimise working capital efficiency but reduce buffer capacity during disruption events. Battery manufacturers typically maintain 30-60 days of lithium inventory, meaning that processing disruptions longer than inventory coverage periods force production adjustments or alternative sourcing arrangements.

Which Countries Control the Strategic Chokepoints in Lithium Value Creation?

Strategic control in the global lithium supply chain operates through multiple mechanisms spanning resource ownership, processing capabilities, and market access. Different countries have established dominance at specific value chain stages, creating interdependencies that shape pricing power and supply security for downstream industries. Understanding these control points reveals how geographic advantages translate into market influence across the lithium ecosystem.

The Lithium Triangle's Resource Dominance

The Lithium Triangle's strategic importance stems from both absolute reserve size and production cost advantages. Brine-based lithium extraction from Argentina and Chile delivers the lowest global production costs, with operating expenses approximately 30-40% below Australian hard rock alternatives according to industry benchmarking data. This cost advantage provides sustained competitiveness despite geographic concentration risks.

Chile's position within the Triangle demonstrates how resource control translates into market influence. SQM operates extensive evaporation pond systems covering approximately 65,000 hectares in the Atacama region, controlling roughly 30% of Chilean lithium production through this infrastructure. The company's integrated approach from brine extraction through initial processing enables cost optimisation across multiple operational stages.

Argentina's emergence as a major producer illustrates how resource development can shift regional dynamics. The country increased production from minimal levels to approximately 16,000-17,000 tonnes of lithium carbonate equivalent in 2023, representing significant capacity additions that reduced global dependence on Chilean operations. Multiple development projects across Argentine salars suggest continued expansion potential that could further redistribute Triangle production shares.

Bolivia represents the Triangle's latent resource potential, holding approximately 23 million tonnes of lithium metal equivalent reserves while producing only 400 tonnes annually. Political and infrastructure constraints have limited development despite massive resource endowments, creating opportunities for future capacity additions that could dramatically alter regional production patterns if development barriers are resolved.

China's Vertical Integration Strategy

China's control mechanisms operate through vertical integration that spans multiple supply chain stages simultaneously. The country processes approximately 60% of global lithium while manufacturing 65-70% of battery cells, creating compound leverage effects where Chinese companies can optimise material flows across integrated operations. This approach contrasts with Western specialisation strategies that focus on individual supply chain segments.

Ganfeng Lithium exemplifies China's integrated model through diverse asset ownership spanning continents. The company maintains mining interests in South American operations, processing facilities in China and Ireland, and downstream battery material production capabilities. This geographic diversification combined with vertical integration creates multiple revenue streams while reducing dependency on external suppliers.

Chinese companies have established strategic positions in foreign lithium assets through direct investment and partnership arrangements. These ownership stakes provide supply security while enabling technology transfer and operational knowledge sharing. Moreover, the approach creates bilateral dependencies where host countries benefit from Chinese investment while China secures long-term resource access.

Processing technology capabilities represent another dimension of Chinese control, where specialised knowledge and equipment manufacturing create barriers for potential competitors. Chinese engineering companies design and construct lithium processing facilities globally, maintaining technological influence even in operations located outside China. This technical expertise extends Chinese influence beyond direct ownership arrangements.

Australia's Mining Infrastructure Advantages

Australia's competitive position relies on developed mining infrastructure, regulatory stability, and geographic proximity to Asian markets. The country produces approximately 42% of global lithium from mining operations while maintaining established logistics networks that enable efficient export operations. Furthermore, Australian lithium innovations demonstrate how port facilities and transportation infrastructure provide operational advantages that reduce logistics costs compared to other mining regions.

Pilbara Minerals demonstrates Australia's infrastructure advantages through integrated operations spanning mining and initial processing. The company's Greensboro mine produces approximately 1.8 million tonnes of spodumene concentrate annually while operating processing facilities at Kwinana, Western Australia. This integration within Australian borders reduces international transportation requirements while maintaining quality control across operational stages.

Regulatory frameworks provide Australia with competitive advantages through predictable permitting processes and established mining law systems. Environmental assessments follow established procedures with defined timelines, reducing development uncertainty compared to jurisdictions with evolving regulatory approaches. This predictability attracts international investment while supporting long-term operational planning.

Australia's weakness lies in limited domestic processing capacity for battery-grade materials, creating dependency on international processors predominantly located in China. While Australian operations excel at mining and initial concentration, final processing requirements typically necessitate exports to Asian facilities for completion. This dependency limits Australia's value capture despite significant mining advantages.

How Do Supply-Demand Imbalances Drive Future Market Dynamics?

Market dynamics in the global lithium supply chain increasingly reflect structural imbalances between accelerating demand growth and constrained supply capacity additions. Electric vehicle adoption trajectories combined with energy storage deployment create compound demand pressures that exceed current production scaling capabilities. These imbalances generate pricing volatility while influencing investment patterns across the entire value chain.

Production Scaling Challenges Through 2030

Production capacity expansion faces significant technical and financial barriers that limit scaling speed relative to demand projections. Current global production of approximately 130,000 tonnes of lithium carbonate equivalent must increase to an estimated 320,000-350,000 tonnes by 2030 to meet projected demand according to International Energy Agency analysis. This implies annual growth rates exceeding 15%, requiring substantial capital investment and operational execution.

Brine operations encounter specific scaling constraints due to geographic limitations and evaporation timelines. Suitable brine resources exist in limited geographic areas with appropriate mineral concentrations and climatic conditions. Evaporation pond systems require 12-24 months to achieve full production rates, creating extended development timelines that compound capacity planning challenges.

Hard rock mining expansion requires different infrastructure investments but faces equally significant challenges. New spodumene operations typically require 4-6 years from discovery through production, including exploration, permitting, construction, and commissioning phases. Processing facility development adds additional timeline requirements, often extending total development periods to 7-10 years for integrated operations.

Capital requirements for expansion create financing constraints that limit development speed. Greenfield lithium operations typically require $800 million to $1.5 billion in initial investment, while processing facilities demand additional $500 million to $1.5 billion. These capital intensities mean that expansion depends on favourable financing conditions and commodity price expectations that support project economics.

EV Demand Growth Trajectory Impact

Electric vehicle adoption rates continue exceeding historical projections, creating upward pressure on lithium demand forecasts. Global EV sales reached approximately 14 million units in 2023, representing 18% of total vehicle sales, with International Energy Agency projections indicating growth to 35 million units annually by 2030. This growth trajectory implies compound annual growth rates exceeding 15% over the projection period.

Battery chemistry evolution influences lithium demand intensity per vehicle, where different technologies require varying lithium quantities. Current battery packs typically contain 8-12 kg of lithium carbonate equivalent per 60 kWh capacity, though this ratio varies by chemistry selection and energy density improvements. Lithium iron phosphate batteries generally require higher lithium content per kWh compared to nickel manganese cobalt alternatives.

Vehicle electrification extends beyond passenger cars into commercial transportation segments that multiply demand impacts. Electric trucks and buses contain significantly larger battery packs, often exceeding 300 kWh capacity for long-haul applications. Commercial vehicle electrification represents approximately 15-20% of projected lithium demand growth, though this segment remains earlier in adoption curves compared to passenger vehicles.

Regional adoption patterns create geographic demand concentration that influences supply chain logistics. China represents approximately 50% of global EV sales, while Europe and North America account for additional 30-35% combined. This geographic concentration affects transportation requirements and processing location optimisation as battery manufacturers locate operations near major consumption centres.

Energy Storage Market Expansion Effects

Battery energy storage systems represent the fastest-growing demand segment for lithium, with deployment rates accelerating as renewable energy integration increases globally. Grid-scale storage installations require massive battery systems, often exceeding 100 MWh capacity for utility-scale projects. These installations create concentrated demand events that can significantly impact regional lithium markets.

Stationary storage applications typically utilise different battery chemistries compared to automotive applications, often favouring lithium iron phosphate technologies for cost and safety advantages. These chemistry selections create demand patterns that differ from automotive requirements, requiring supply chain participants to manage multiple product specifications simultaneously.

Energy storage deployment follows renewable energy installation patterns, creating geographic clustering effects in regions with favourable renewable resources. California, Texas, Australia, and Germany represent major deployment regions where grid-scale storage supports renewable integration. This geographic clustering influences transportation logistics and regional pricing dynamics.

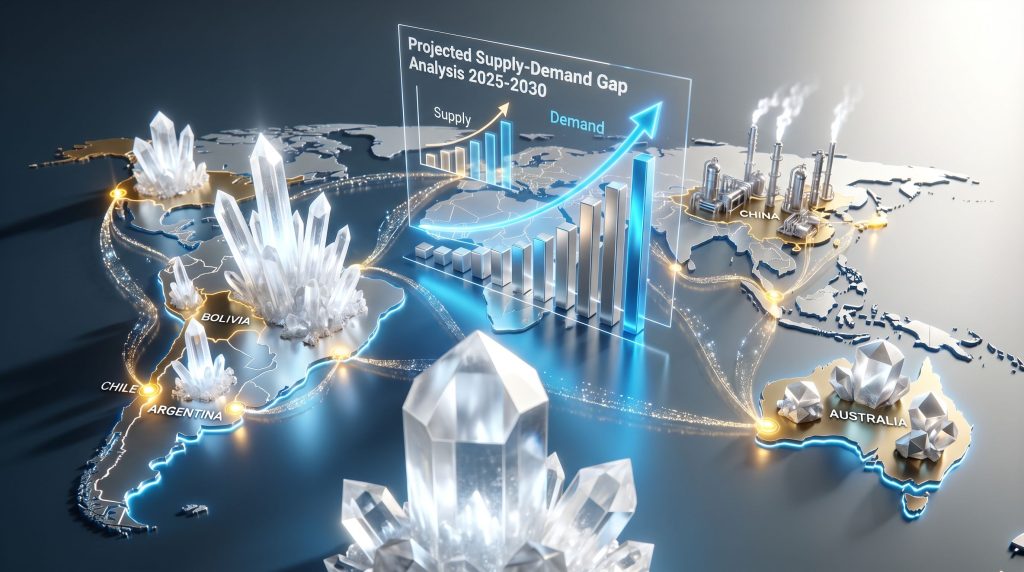

Projected Supply-Demand Gap Analysis 2025-2030

| Year | Projected Demand (tLCE) | Estimated Supply (tLCE) | Deficit (tLCE) | Deficit Percentage |

|---|---|---|---|---|

| 2025 | 180,000 | 155,000 | 25,000 | 14% |

| 2026 | 210,000 | 175,000 | 35,000 | 17% |

| 2027 | 245,000 | 200,000 | 45,000 | 18% |

| 2028 | 285,000 | 230,000 | 55,000 | 19% |

| 2029 | 320,000 | 265,000 | 55,000 | 17% |

| 2030 | 350,000 | 300,000 | 50,000 | 14% |

What Strategic Responses Are Reshaping Global Lithium Competition?

Strategic responses to supply chain vulnerabilities are reshaping competitive dynamics across the global lithium ecosystem. Western governments and companies are pursuing diversification strategies that reduce dependency on concentrated supply sources while investing in alternative technologies and recycling capabilities. These responses create new competitive dynamics that may redistribute market power over the coming decade.

Diversification Initiatives in Western Markets

Western diversification efforts focus on developing alternative supply sources outside traditional geographic concentrations. The United States has launched initiatives to develop domestic lithium production from geothermal brines and historic mining regions, though these efforts remain in early development stages with limited near-term production potential.

European companies are establishing processing facilities to reduce dependency on Chinese processing capacity. These investments typically require 3-5 years for completion and substantial capital commitments, but offer strategic supply security benefits for European battery manufacturers. Germany and Poland represent focal points for European processing development, leveraging industrial infrastructure and skilled workforces.

Partnership arrangements between Western companies and South American producers create alternative supply channels that bypass traditional Chinese processing routes. These partnerships often include technology transfer, financing arrangements, and long-term offtake agreements that provide supply security for Western battery manufacturers while supporting South American development.

Canadian lithium development represents another diversification avenue, where multiple projects across Quebec and other provinces target North American supply requirements. These projects benefit from established mining infrastructure, stable regulatory frameworks, and proximity to North American automotive production centres. However, development timelines remain extended, with most projects targeting production in the late 2020s.

Recycling Technology Development Programs

Recycling technology advancement creates potential alternative supply sources that reduce primary lithium requirements while addressing waste management challenges. Current recycling processes can recover 90-95% of lithium from end-of-life batteries, though economic viability depends on feedstock availability and processing costs relative to primary production.

Battery recycling facility development accelerates as EV adoption creates larger volumes of end-of-life batteries. Current battery lifespans of 8-15 years mean that significant recycling feedstock volumes will emerge in the 2030s as first-generation EV batteries reach replacement cycles. This timing creates opportunities for recycling capacity development that aligns with peak demand growth periods.

Closed-loop recycling systems under development by major battery manufacturers aim to capture materials within integrated supply chains. Tesla, Contemporary Amperex Technology (CATL), and BYD have announced recycling initiatives that target material recovery for internal battery production. These systems reduce external supply dependencies while creating circular economy benefits.

Technology advancement in direct recycling methods could improve economic viability by reducing processing energy requirements and chemical inputs. Current hydrometallurgical recycling processes are energy-intensive and require substantial chemical inputs, limiting economic competitiveness compared to primary production. However, direct recycling approaches under development aim to maintain battery material structure while reducing processing intensity.

Alternative Chemistry Research Impact

Alternative battery chemistry research aims to reduce lithium content requirements while maintaining performance characteristics necessary for automotive and grid applications. Solid-state battery technologies under development by multiple companies could potentially reduce lithium requirements per kWh while improving energy density and safety characteristics.

Sodium-ion battery development represents a potential substitute technology for stationary storage applications where weight and energy density requirements are less stringent compared to automotive uses. Chinese companies including CATL and BYD have announced sodium-ion production capabilities for grid storage applications, though performance characteristics remain inferior to lithium-based alternatives.

Lithium-sulphur and lithium-metal battery technologies could increase energy density while potentially reducing total lithium requirements through improved utilisation efficiency. These technologies remain in development phases with commercialisation timelines extending into the 2030s, but could significantly alter lithium demand patterns if successfully deployed at scale.

Advanced lithium iron phosphate formulations aim to improve energy density while maintaining cost and safety advantages relative to nickel-based alternatives. Chinese manufacturers continue advancing LFP technology that narrows performance gaps with higher-cost chemistries, potentially expanding LFP market share in automotive applications that traditionally required higher energy density solutions.

The next major ASX story will hit our subscribers first

How Do Geopolitical Tensions Influence Supply Chain Resilience?

Geopolitical dynamics increasingly influence global lithium supply chain architecture as governments recognise critical material dependencies and strategic vulnerabilities. Trade policies, investment restrictions, and national security considerations create additional complexity layers that affect commercial decision-making and investment patterns across the industry.

Trade Policy Effects on Resource Access

Export restrictions and tariff policies create barriers that fragment global lithium markets and increase supply chain complexity. Argentina implemented temporary lithium export restrictions during 2022 periods of domestic political transition, demonstrating how trade policy uncertainty can affect global supply availability. These restrictions contributed to price volatility and highlighted dependency risks for importers.

Chinese export policies for processed lithium materials influence global pricing and availability, where administrative procedures and export licensing create potential control mechanisms. While China has not implemented formal lithium export restrictions, the administrative framework exists for policy implementation if geopolitical tensions escalate further.

Tariff structures affect processing location decisions and supply chain routing optimisation. U.S. tariffs on Chinese battery materials encourage processing facility development in alternative locations, though these investments require extended development timelines. European Union trade policies similarly influence supply chain configuration decisions for companies serving European markets.

Free trade agreements create preferential access arrangements that influence investment location decisions. The United States-Mexico-Canada Agreement provides preferential treatment for North American battery materials, encouraging supply chain development within member countries. Similar preferential arrangements in other regions create fragmented global markets with regional optimisation incentives.

Investment Restrictions and Technology Transfer

Foreign investment screening mechanisms in multiple countries create barriers that limit cross-border capital flows and technology sharing. U.S. Committee on Foreign Investment reviews of Chinese investments in critical material sectors have blocked multiple transactions, reducing Chinese access to Western lithium assets while limiting capital availability for development projects.

Technology transfer restrictions affect equipment procurement and operational optimisation across international operations. Export controls on specialised mining and processing equipment create compliance complexities that increase project development costs and timelines. These restrictions particularly affect countries seeking to develop domestic processing capabilities using advanced technologies.

Intellectual property protection concerns influence technology sharing arrangements between international partners. Western companies increasingly require enhanced IP protections when engaging in technology transfer agreements, particularly for advanced processing and recycling technologies. These requirements can limit partnership arrangements and slow technology deployment.

Strategic partnership restrictions limit collaboration arrangements that could optimise global supply chain efficiency. Government policies that discourage partnerships with specific countries or companies create suboptimal supply chain configurations that prioritise political considerations over commercial efficiency, potentially increasing costs and complexity throughout the system.

National Security Considerations in Critical Materials

Critical materials designation by multiple governments elevates lithium supply chain security to national priority levels, influencing policy approaches and investment incentives. The U.S. Department of Defense and other Western defence establishments have classified lithium as strategically important, creating policy frameworks that support domestic supply chain development.

Strategic reserves and stockpiling programmes represent government responses to supply security concerns, though implementation remains limited due to storage challenges and market impact considerations. Government stockpile purchases can influence market pricing and provide demand support for domestic producers, while releases can moderate price increases during supply disruptions.

Defence sector requirements for secure supply chains create parallel market segments where premium pricing compensates for enhanced security measures and domestic sourcing requirements. Military and aerospace applications require lithium materials from verified supply chains with enhanced documentation and traceability, creating niche markets within broader lithium demand.

Economic security frameworks increasingly treat critical material supply chains as infrastructure requiring protection and resilience investment. These frameworks justify government intervention in commercial markets through subsidies, loan guarantees, and regulatory support that would not typically apply to conventional commodity markets.

Current lithium supply chain architecture optimises for efficiency rather than resilience, creating vulnerabilities that compound during crisis periods when alternative sources prove insufficient to replace disrupted capacity.

Which Investment Strategies Address Long-Term Supply Security?

Investment strategies addressing supply security operate across multiple dimensions spanning mining development, processing capacity expansion, and vertical integration approaches. Successful strategies balance risk management with return optimisation while considering extended development timelines that characterise lithium supply chain investments. These strategies must account for both commercial returns and strategic supply security objectives.

Upstream Mining Project Development

Mining project development requires substantial capital commitments over extended timelines with significant technical and regulatory risks. Successful development strategies typically begin with resource exploration and feasibility studies that require 2-3 years for completion before construction decisions. Project economics depend on long-term lithium price assumptions that must justify development costs ranging from $800 million to $1.5 billion for integrated operations.

Geographic diversification represents a critical component of mining investment strategies, where resource development across multiple jurisdictions reduces political and regulatory concentration risks. Companies like Albemarle operate across Chile, Australia, and potential North American projects to distribute geographic exposure while optimising cost structures through diverse extraction methods.

Joint venture arrangements enable risk sharing while accessing specialised technical expertise and local market knowledge. Many successful lithium projects utilise partnership structures that combine international financing and technical capabilities with local operational expertise and regulatory knowledge. These arrangements can accelerate permitting processes while reducing individual company risk exposure.

Technology selection decisions influence both capital requirements and operating cost structures for new mining projects. Direct lithium extraction technology development creates opportunities for enhanced recovery rates and reduced environmental impact, though commercial deployment remains limited. Investment strategies must evaluate technology risks alongside resource and market risks when making development decisions.

Midstream Processing Capacity Expansion

Processing facility development addresses critical bottlenecks in global lithium supply chains while capturing higher value-added margins compared to mining operations. Processing investment strategies require 3-5 year development timelines and substantial technical expertise in hydrometallurgical processes. Facility locations must balance access to raw materials, energy availability, skilled labour, and market proximity.

Integrated processing approaches that combine mining and processing operations optimise material flows while reducing transportation costs and supply chain complexity. Companies pursuing integration must manage increased capital requirements and operational complexity while capturing enhanced margins and supply security benefits. These strategies work particularly well for companies with established mining operations seeking vertical integration.

Contract processing arrangements provide alternative approaches that reduce capital intensity while serving diverse customer bases. Companies can develop processing capabilities that serve multiple mining operations through long-term processing agreements, distributing fixed costs across larger volumes while reducing dependency on individual mining operations.

Technology advancement investments in processing efficiency and environmental impact reduction create competitive advantages while addressing regulatory requirements. Companies investing in advanced processing technologies can achieve cost advantages while meeting increasingly stringent environmental standards that affect facility permitting and operational licenses.

Downstream Integration Opportunities

Downstream integration strategies extend supply chain participation into battery materials and component manufacturing, capturing additional value while securing end-market access. These strategies require substantial investment in technical capabilities and market development, though they provide enhanced margin opportunities and customer relationship development.

Battery precursor material production represents an intermediate integration opportunity between lithium processing and final battery manufacturing. Companies can develop capabilities in lithium carbonate and lithium hydroxide production that serve battery manufacturers while avoiding complete battery manufacturing complexity. This approach captures processing margins while maintaining focus on lithium expertise.

Partnership arrangements with battery manufacturers create long-term offtake agreements that provide demand security while enabling supply chain optimisation. These partnerships often include technical collaboration on material specifications and quality requirements that enhance product differentiation and customer relationships.

Recycling integration creates circular economy opportunities that reduce primary lithium requirements while addressing waste management challenges. Furthermore, the battery recycling breakthrough demonstrates how companies can develop recycling capabilities that serve their own operations while providing services to broader markets, creating additional revenue streams while supporting sustainability objectives.

Regional Investment Flows in Lithium Infrastructure

| Region | Mining Investment (2023-2024) | Processing Investment | Government Incentives | Private Investment Share |

|---|---|---|---|---|

| North America | $8.5 billion | $3.2 billion | $1.8 billion | 85% |

| Europe | $2.1 billion | $4.7 billion | $2.3 billion | 75% |

| Australia | $12.3 billion | $1.9 billion | $650 million | 92% |

| South America | $6.8 billion | $2.4 billion | $1.1 billion | 88% |

| China | $15.2 billion | $8.9 billion | $3.7 billion | 78% |

What Role Does Technology Innovation Play in Supply Chain Evolution?

Technology innovation drives fundamental changes in global lithium supply chain economics, operational efficiency, and environmental impact. Advanced extraction methods, processing optimisation, and recycling technologies create opportunities to overcome traditional constraints while reducing costs and environmental footprints. These innovations influence competitive positioning and investment priorities across the entire value chain.

Direct Lithium Extraction (DLE) Technology Adoption

Direct lithium extraction technology represents a paradigm shift from traditional evaporation pond methods that could accelerate brine resource development while reducing environmental impact. DLE technologies utilise selective separation processes that extract lithium directly from brines without extensive evaporation requirements, reducing water consumption and land use while shortening production timelines from 18-24 months to 6-12 months.

Multiple DLE technology approaches are under development, including selective adsorption, membrane separation, and electrochemical extraction methods. Each approach offers different advantages depending on brine characteristics, with adsorption technologies typically suitable for brines with higher lithium concentrations while membrane technologies may work better for lower-grade resources. Commercial deployment remains limited, though pilot projects across Argentina, Chile, and Nevada demonstrate technical feasibility.

Economic advantages of DLE technology include reduced capital requirements for pond construction and faster time-to-production compared to conventional evaporation methods. DLE facilities typically require $400-600 million in capital investment compared to $600-800 million for equivalent evaporation operations, while achieving production timelines that are 12-18 months shorter. These advantages could accelerate brine resource development in regions previously considered marginal.

Environmental benefits include significantly reduced water consumption and smaller surface footprints compared to evaporation pond systems. DLE operations typically consume 80-90% less water than conventional brine processing while requiring 90-95% less surface area for operations. These benefits address growing environmental concerns about lithium extraction impact on local water resources and ecosystems.

Battery Recycling Efficiency Improvements

Advanced recycling technologies enable higher recovery rates while reducing processing costs and environmental impact compared to conventional hydrometallurgical approaches. Current recycling processes achieve 90-95% lithium recovery rates, though new technologies target 98%+ recovery while reducing energy consumption and chemical inputs required for material separation.

Direct recycling methods under development aim to maintain battery material crystalline structures during processing, reducing energy requirements while preserving material performance characteristics. These approaches could reduce recycling costs by 30-40% compared to conventional methods while producing materials equivalent to newly produced alternatives. Commercial deployment remains in early stages, though multiple companies have announced development programmes.

Automated disassembly technologies improve recycling economics by reducing labour costs while enhancing material separation efficiency. Robotic systems can systematically disassemble battery packs and separate different material streams with greater precision than manual methods, increasing recovery rates while reducing safety risks for workers handling potentially hazardous materials.

Closed-loop recycling systems integrate recycling operations directly into battery manufacturing facilities, creating circular material flows that reduce external supply dependencies. Tesla's Nevada facility and Contemporary Amperex Technology's planned recycling capabilities demonstrate integrated approaches that capture recycling margins while securing material supplies for battery production.

Alternative Processing Methods Development

Innovative processing technologies address cost reduction and environmental impact improvement opportunities across multiple extraction and processing stages. Microwave-assisted processing and ultrasonic extraction methods can reduce energy requirements while accelerating reaction rates, potentially reducing processing costs by 15-25% compared to conventional approaches.

Biological processing methods utilise microorganisms to extract lithium from ores or brines through selective bioaccumulation processes. These biotechnology approaches remain in research phases, though they offer potential advantages including reduced chemical inputs and lower environmental impact. Commercial viability depends on achieving extraction rates and costs competitive with conventional methods.

Electrochemical processing techniques provide opportunities for selective lithium extraction and purification using electrical separation methods rather than chemical processing. These approaches can achieve high purity levels while reducing chemical waste generation, though energy requirements may limit economic viability depending on electricity costs and availability.

Integrated processing systems combine multiple separation and purification technologies to optimise overall efficiency while reducing waste generation. These systems can adapt to different input materials and quality specifications while maintaining consistent output quality, providing operational flexibility that supports diverse resource utilisation strategies.

How Will Environmental Regulations Transform Supply Chain Operations?

Environmental regulations increasingly constrain lithium supply chain operations while creating incentives for technology adoption and operational optimisation. Water usage restrictions, carbon footprint requirements, and waste management standards influence facility design, location selection, and operational procedures. Compliance costs affect project economics while creating competitive advantages for companies that exceed regulatory requirements.

Water Usage Restrictions in Brine Operations

Water scarcity concerns in major lithium-producing regions drive regulatory restrictions that limit traditional evaporation pond operations while encouraging alternative extraction technologies. Chile's Atacama region faces increasing water usage oversight from environmental authorities concerned about impacts on local ecosystems and indigenous communities. These restrictions could limit expansion of conventional brine operations while favouring direct lithium extraction technologies.

Water rights allocation systems in Argentina and Chile create competitive dynamics where lithium producers must compete with agricultural, municipal, and industrial users for limited water resources. Regulatory frameworks increasingly require comprehensive water impact assessments and mitigation measures that add complexity and costs to project development. Companies must demonstrate sustainable water usage practices to obtain and maintain operating permits.

Groundwater monitoring requirements mandate extensive data collection and reporting that increase operational costs while providing regulatory oversight mechanisms. Companies must install comprehensive monitoring systems that track water level changes, quality impacts, and ecosystem effects. This data enables regulatory enforcement while creating operational constraints during drought periods or aquifer stress events.

Alternative water sourcing strategies including seawater desalination and wastewater recycling are becoming necessary for operations in water-constrained regions. Thacker Pass US production exemplifies how new projects must incorporate advanced water management technologies to meet environmental compliance requirements while maintaining operational efficiency.

Carbon Footprint Reduction Requirements

Carbon emission regulations create requirements for renewable energy utilisation and process efficiency improvements across lithium supply chain operations. Processing facilities face particular pressure due to high energy intensity, with typical operations consuming 8-12 MWh per tonne of lithium carbonate equivalent produced. Companies must invest in energy efficiency improvements or renewable energy sources to meet emission reduction targets.

Scope 3 emission reporting requirements extend carbon accounting across entire supply chains, creating pressure for transparency and reduction throughout lithium value networks. Battery manufacturers increasingly require suppliers to demonstrate carbon footprint reductions and provide detailed emission reporting for all material inputs. This creates cascading effects where emission reduction requirements propagate through multiple supply chain

Ready to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why major mineral discoveries can lead to significant market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes.