July 10, 2026

The Quiet Giant Waking Up: Gold's Return to the Top of Australia's Export Table

Few economic shifts signal a genuine structural realignment quite like a change in a country's commodity export hierarchy. For most of the past six decades, Australia's resource story has been told through the lens of iron ore and energy exports, with gold playing a supporting role despite the nation's extraordinary geological endowment. That narrative is now changing in ways that carry real implications for investors, policymakers, and the broader economy.

In 2025-26, Australia gold exports second-largest commodity export status was formally confirmed, with gold reclaiming its position last held in the early 1960s, with only a brief resurgence in 1987. This is not simply a price story, though prices have certainly been extraordinary. It reflects something deeper about Australia's structural position in global resource markets and the forces reshaping demand for hard assets worldwide.

When big ASX news breaks, our subscribers know first

Australia's Commodity Export Rankings: A New Order

The latest Resources and Energy Quarterly published by the Department of Industry, Science and Resources paints a compelling picture of how significantly gold's position in Australia's export mix has shifted.

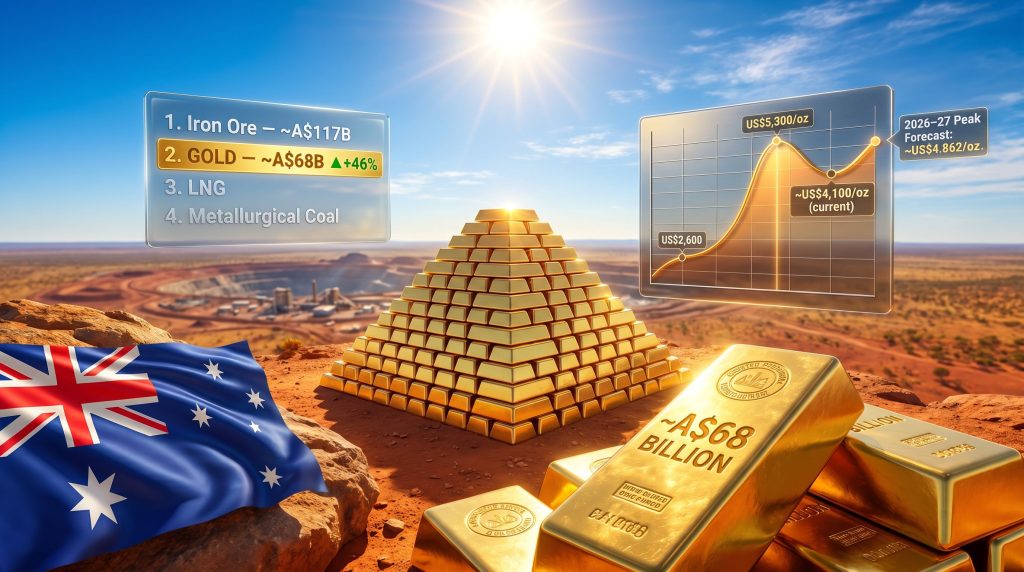

| Rank | Commodity | Estimated Export Value (2025-26) | Year-on-Year Change |

|---|---|---|---|

| 1 | Iron Ore | ~A$117 billion | Stable |

| 2 | Gold | ~A$68 billion | +46% |

| 3 | LNG | ~A$47-50 billion | Overtaken |

| 4 | Metallurgical Coal | ~A$47-50 billion | Overtaken |

Gold's 46% surge in export earnings to approximately A$68 billion has pushed both liquefied natural gas and metallurgical coal down the rankings. Iron ore remains firmly in first position, accounting for more than 25% of all Australian commodity exports at roughly A$117 billion, a dominance that is expected to continue across the five-year forecast horizon.

What makes gold's rise to second place so notable is not merely the dollar figure but the historical rarity of the achievement. According to the World Gold Council, the last sustained period in which gold occupied this position was over 60 years ago, making 2025-26 a genuinely generational milestone in Australian resource history.

What Drove the Price Surge That Changed Everything

To understand gold's ascent, it is essential to examine the extraordinary price environment that preceded it. Gold prices more than doubled between late 2024 and early 2025, reaching a peak above US$5,300 per ounce before moderating toward current levels around US$4,100 per ounce. Even at these moderated levels, the gold price remains at extraordinary elevations relative to historical norms.

Several converging forces drove this movement:

- Geopolitical supply disruptions, particularly in the Middle East, created risk-off conditions that historically benefit gold as a safe-haven asset.

- Central bank accumulation accelerated as sovereign wealth managers sought alternatives to US dollar-denominated reserves, a trend that has been building since 2022 but intensified through 2024 and 2025.

- Currency debasement concerns across major economies pushed institutional and retail investors toward hard asset allocations, compressing the available supply of investable gold.

- Supply chain sovereignty movements led nations to diversify away from concentrated commodity dependencies, with gold serving as both a financial and strategic asset.

Furthermore, gold's geopolitical rally has been one of the defining financial narratives of recent years, with the February 2026 surge of approximately 30% adding further momentum. This was driven by a combination of renewed geopolitical tension and a weakening US dollar. This compressed timeline of price appreciation translated directly into elevated export revenue for Australian producers, who benefited from both higher spot prices and, in many cases, favourable hedging positions unwound at opportune moments.

The confluence of risk-off demand, central bank buying, and supply disruptions created a price environment that Australia's gold sector was uniquely positioned to capitalise on, given its existing production scale and infrastructure depth.

How Central Bank Buying Shaped the Rally

In addition to geopolitical pressures, central bank gold demand has played a pivotal role in sustaining elevated price levels. Sovereign buyers across emerging and developed markets continued to accumulate physical gold at a pace not seen in decades, removing significant supply from open markets and reinforcing the structural floor beneath spot prices.

Australia's Structural Advantages in Gold Production

Price alone cannot explain why Australia captured such a disproportionate share of global gold export value. The country's geological endowment, built around world-class ore bodies concentrated primarily in the Goldfields-Kalgoorlie region of Western Australia, provides a cost-competitive production base that few nations can match.

Australia ranks as the world's second-largest gold producer behind China, and in 2025 placed sixth globally in gold export value at approximately US$38.4 billion. The combination of large, long-life deposits with relatively low strip ratios, established processing infrastructure, and deep capital market access gives Australian producers structural advantages that amplify the benefit of elevated gold prices.

Several factors reinforce this competitive positioning:

- Regulatory stability and transparent permitting frameworks reduce sovereign risk relative to competing jurisdictions in Africa and parts of South America.

- Skilled workforce availability and institutional knowledge accumulated over more than a century of commercial gold mining in Western Australia.

- Proximity to Asian markets, particularly Singapore, Hong Kong, and increasingly India, shortens logistics chains and reduces the frictional cost of moving refined product to end buyers.

- Perth Mint's refining capacity adds a critical layer of value creation by converting doré bars into LBMA-accredited refined gold, enabling Australian product to command premium positioning in international markets.

The Perth Mint's role is often underappreciated in discussions of Australia's gold export value. Refining transforms raw output into a globally tradeable commodity with standardised purity certifications, effectively adding export value that would otherwise accrue to offshore refiners.

Forward Projections: How Long Can the Boom Last?

The Department of Industry's forecasts suggest gold's elevated position in Australia's export hierarchy will persist for several years, though the trajectory points to gradual normalisation. The gold price forecast through to the end of the decade reflects this moderated but still historically elevated outlook.

| Financial Year | Projected Gold Export Value | Projected Average Gold Price |

|---|---|---|

| 2025-26 | ~A$68 billion | ~US$4,100/oz (current) |

| 2026-27 | ~A$73 billion (peak) | ~US$4,862/oz |

| 2030-31 | Declining | ~US$4,000/oz |

The forecast peak of approximately A$73 billion in 2026-27 represents a further uplift from current levels, driven by an assumed average gold price of US$4,862 per ounce across that financial year. Beyond this peak, a gradual glide path toward US$4,000 per ounce by 2030-31 is anticipated as geopolitical risk premiums compress and supply responses from global miners materialise.

It is worth noting that these projections carry material uncertainty. The Department's forecasts are explicitly built on the assumption that shipping through the Strait of Hormuz resumes from July 2026, with trade volumes gradually returning to pre-conflict levels. Any deviation from this geopolitical assumption could significantly alter both energy price dynamics and broader risk sentiment, with knock-on effects for gold demand.

Disclaimer: Forward-looking projections from government departments represent modelled scenarios based on specific assumptions, not guaranteed outcomes. Investors should treat commodity price forecasts as indicative planning tools rather than reliable financial guidance.

The Broader Context: Australia's Total Resource Export Revision

Gold's rise has contributed to a substantial upward revision in Australia's total resource export revenue forecasts. Total projected earnings were lifted to A$405 billion in 2025-26 and A$416 billion in 2026-27, representing upward revisions of A$22 billion and A$42 billion respectively compared to the December 2024 outlook. These are not marginal adjustments but reflect a genuine step-change in the revenue base flowing through Australia's resource sector.

The Department of Industry also pointed to several demand-side forces expected to sustain this elevated export base over the medium term:

- AI infrastructure investment is driving unprecedented demand for electricity generation capacity, creating downstream demand for the energy commodities and critical minerals that underpin grid expansion.

- The global energy transition continues to generate sustained demand for Australian commodities, from metallurgical coal in the near term to battery minerals over the longer horizon.

- Supply chain sovereignty is prompting major economies to formalise long-term commodity procurement relationships with reliable producers, and Australia's institutional credibility positions it well in these conversations.

- IMF growth projections for both China and the US remain supportive, with the report characterising these two economies as locomotives driving broader global demand for Australian exports.

- Vietnam and India are identified as high-growth emerging trading partners whose accelerating industrialisation creates structural new demand channels beyond Australia's traditional export relationships.

The next major ASX story will hit our subscribers first

Iron Ore vs. Gold: Comparing Australia's Two Export Giants

While gold's ascent is remarkable, iron ore's structural dominance remains the defining feature of Australia's commodity export profile. Understanding how these two commodities compare reveals important nuances about revenue quality and risk.

| Metric | Iron Ore | Gold |

|---|---|---|

| 2025-26 Export Value | ~A$117B | ~A$68B |

| Share of Total Exports | 25%+ | ~17% |

| Primary Region | Pilbara, WA | Goldfields-Kalgoorlie, WA |

| Key Price Driver | Chinese steel demand | Global risk sentiment / USD |

| Key Competitive Risk | Brazil, Guinea supply growth | Price normalisation |

| Outlook to 2030-31 | Stable, competitive pressure | Gradual decline from peak |

Iron ore's price is tightly coupled to Chinese steel production volumes, making it highly sensitive to property sector dynamics in China, a relationship that has generated significant volatility over recent years. The iron ore demand outlook remains consequential to Australia's overall export story, particularly given the commodity's outsized share of total revenue. Gold, by contrast, tends to move inversely to risk appetite and the US dollar, creating a natural diversification effect within Australia's export revenue base.

The report acknowledges that Australia's iron ore position faces competitive pressure from expanding Brazilian output and the emergence of Guinea as a significant future iron ore producer. Maintaining cost competitiveness in the Pilbara will be central to preserving Australia's dominant position through the decade.

What the Gold Export Milestone Tells Us About Economic Resilience

At a structural level, gold's rise to second place in Australia's export hierarchy is more than a commodity cycle story. It demonstrates the value of maintaining a diversified resource export portfolio capable of rotating leadership depending on global conditions. Indeed, Australia's resource export outlook is being fundamentally reassessed in light of these structural shifts.

When iron ore prices face headwinds from Chinese demand weakness, elevated gold revenues provide a partial offset. This diversification dividend is often overlooked in discussions focused on individual commodity cycles, but it materially reduces the volatility of Australia's aggregate resource export income.

There is also a capability dimension that matters for long-term investors. Australia's ability to capture value from an extraordinary gold price environment reflects decades of compounding investment in exploration geology, processing technology, workforce training, and regulatory frameworks. These capabilities do not appear overnight and cannot be replicated quickly by competing jurisdictions.

Australia gold exports second-largest commodity export status in 2025-26 is ultimately the product of patient, long-cycle investment meeting a period of exceptional market conditions. As reported by Bloomberg, gold has now decisively overtaken both LNG and metallurgical coal, marking a structural moment in the nation's economic history that few analysts had anticipated occurring so rapidly.

Frequently Asked Questions: Australia's Gold Export Boom

What is Australia's second-largest commodity export in 2025-26?

Gold has become Australia's second-largest commodity export in 2025-26, with estimated export earnings of approximately A$68 billion, overtaking both LNG and metallurgical coal.

How much did Australian gold exports earn in 2025-26?

Australian gold exports are estimated to have earned approximately A$68 billion in 2025-26, representing a 46% increase year-on-year.

When did gold last hold second place in Australia's export rankings?

According to the World Gold Council, gold last held second place in Australia's commodity export rankings in the early 1960s, with only a brief interruption in 1987.

How does Australia's gold production rank globally?

Australia is the world's second-largest gold producer behind China and ranked sixth globally in gold export value in 2025 at approximately US$38.4 billion.

What is the forecast gold price through to 2030-31?

The Department of Industry forecasts an average gold price of approximately US$4,862 per ounce in 2026-27, easing to around US$4,000 per ounce by 2030-31.

Will gold remain Australia's second-largest export beyond 2027?

Current forecasts suggest Australia gold exports second-largest commodity export earnings will peak around A$73 billion in 2026-27 before gradually declining as gold prices normalise, though gold is expected to remain among the top tier of Australian exports through the forecast horizon.

What commodities did gold overtake to reach second place?

Gold overtook both LNG and metallurgical coal to reach second position in Australia's commodity export rankings in 2025-26.

Want to Know Which ASX Gold Explorers Could Benefit From Australia's Historic Export Boom?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including gold — and translating complex data into actionable investment insights, with historic discoveries demonstrating the potential for extraordinary returns. Start your 14-day free trial at Discovery Alert and position yourself ahead of the market before the next major find is announced.