July 7, 2026

The Architecture of a New Bullion Order: How Asia Is Rewriting the Rules of Gold Settlement

For most of the twentieth century, the global gold market operated on a simple geographic assumption: prices were set in the West, and the rest of the world followed. London's over-the-counter interbank market became the de facto nerve centre of international bullion trading, with New York's COMEX futures exchange providing the paper-market counterpart. Asia, despite accounting for the majority of the world's physical gold consumption, remained structurally subordinate to this arrangement, absorbing pricing signals from time zones that closed before Asian markets fully opened. That arrangement is now being challenged at its foundation.

The Hong Kong gold clearing system, launched in trial operation in July 2026, represents the most consequential structural intervention in global bullion market infrastructure in decades. But to understand why it matters, it helps to start not with the announcement itself, but with the fundamental mechanics of how gold clearing actually works and why its absence in Asia has been so costly.

When big ASX news breaks, our subscribers know first

What Gold Clearing Actually Does, and Why It Matters

A gold clearing system is not simply a record-keeping function. It is the operational infrastructure that allows institutions to trade large volumes of bullion without requiring each counterparty to extend unlimited bilateral credit to the other. When two banks trade gold in the LBMA and COMEX markets, they do not actually transfer physical bars between themselves for every transaction. Instead, they maintain positions in a shared clearing system that nets their obligations, reduces settlement risk, and allows capital to be deployed more efficiently.

The critical distinction in any clearing architecture is between allocated and unallocated gold accounts. Understanding this distinction is essential for grasping how the Hong Kong system is designed to attract institutional participation.

| Account Type | Ownership Structure | Liquidity Impact | Common Use Case |

|---|---|---|---|

| Allocated | Specific bars assigned to owner | Lower, tied to physical bars | Long-term storage, central banks |

| Unallocated | Pooled gold ownership claim | Higher, no bar assignment needed | Active trading, OTC settlement |

Allocated accounts assign specific, identifiable gold bars to a named owner. They are favoured by central banks and long-term investors who want legal certainty over specific physical metal. Unallocated accounts represent a claim on a pool of gold held by a custodian, with no specific bars earmarked. Because they do not require the logistical overhead of bar assignment for every transaction, unallocated accounts are the preferred instrument for high-frequency institutional trading.

Hong Kong's system deliberately adopted the unallocated account model, mirroring the conventions of the London market. This was not an accident of design. By replicating the structural familiarity that international institutions already work within, the system dramatically lowers the operational friction required for global banks to participate. Pair that with physical delivery capability anchored to the London Good Delivery standard, which specifies 400-troy-ounce bars refined to a minimum of 99.5% purity, and the system presents a credible, internationally legible infrastructure from day one.

The Institutional Architecture Behind Hong Kong's PMCC

The entity operating the system is Hong Kong Precious Metals Central Clearing Company Limited, known as PMCC, a wholly government-owned organisation established under the Financial Services and the Treasury Bureau. Government ownership is a deliberate design signal. In financial infrastructure, counterparty risk is everything. Institutions committing capital to a clearing system need confidence that the operator itself will not fail. Sovereign ownership provides that assurance in a way that a private consortium cannot easily replicate.

Eleven financial institutions are represented on the PMCC board, spanning six international banks and five Chinese lenders. Among the international institutions, JPMorgan Chase, HSBC Holdings, and UBS Group provide a tier of global systemically important bank credibility that carries enormous weight with institutional counterparties worldwide. Their presence signals that the system meets the compliance, risk management, and operational standards required by the world's most heavily regulated financial institutions.

The Chinese bank representation on the board is equally strategic. It provides direct connectivity to mainland Chinese capital flows, which represent the largest physical gold demand base in the world. This dual-track board structure, combining Western institutional legitimacy with Chinese financial network access, is one of the more sophisticated aspects of the system's design.

Standard Chartered completed inaugural transactions with Chow Sang Sang, Haitong International Securities, JD Technology, and Shanghai Pudong Development Bank during the trial launch phase. HSBC announced a commitment to scale its Hong Kong gold storage capacity to 200 metric tons in the near term, a statement made publicly by the bank's chief executive at the Hong Kong FIC and Bond Connect Summit in July 2026.

The 400-Ounce Bar Import Signal

One of the more telling indicators of genuine institutional commitment ahead of the trial launch was the pattern of physical gold imports into Hong Kong. At least four participating banks were actively importing 400-ounce London Good Delivery bars to build physical inventory ahead of the system's activation. These bars are standard in London but historically uncommon in Asian vaulting infrastructure, which has traditionally accommodated smaller bar sizes more typical of retail and jewellery-grade demand.

Import volumes during this pre-launch period exceeded the two-year seasonal average by a significant margin, running counter to the typical seasonal lull that characterises mid-year bullion flows into Hong Kong. This is not behaviour associated with regulatory compliance theatre. It reflects genuine preparation for large-scale institutional settlement activity and suggests the participating banks were positioning for meaningful transaction volumes from the outset.

HAU: Anatomy of a New Gold Price Benchmark

At the centre of Hong Kong's ambitions sits a new gold price reference rate designated HAU, now live on Bloomberg terminals globally. A benchmark rate is not merely a number. It is a shared reference point that counterparties use to price contracts, value portfolios, settle disputes, and construct derivative instruments. The LBMA Gold Price, published twice daily in London, currently serves this function for the vast majority of global gold transactions.

For a new benchmark to gain traction, it requires three conditions to be met simultaneously: sufficient transaction volume to make the price statistically meaningful, a transparent and reproducible price discovery methodology, and broad institutional participation that creates the network effects necessary for adoption.

HAU's immediate distribution through Bloomberg's global data infrastructure addresses the adoption barrier directly. Bloomberg terminal access means that any institution already using the LBMA price as a reference can see HAU alongside it from day one, without requiring any additional infrastructure investment. This is not a trivial advantage. The historical difficulty of establishing competing benchmarks has often come down to distribution, not methodology.

The most important feature of any benchmark is not its technical design, but whether enough market participants are willing to use it. Bloomberg distribution does not guarantee that outcome, but it removes the single largest structural barrier to adoption.

HAU is specifically designed to reflect gold prices during Asian trading hours, filling a genuine gap in the current global pricing cycle. Between the close of London's afternoon fixing and the opening of the following day's European session, a significant portion of global gold trading occurs in a relative information vacuum. A credible Asian-hours benchmark with sufficient institutional backing could systematically improve price discovery efficiency across the full twenty-four-hour trading cycle.

Competitive Positioning: London, Shanghai, and Hong Kong

Hong Kong does not exist in isolation. It is entering a competitive landscape that already includes two established global gold market centres and a new rival in the immediate region.

| Feature | London LBMA | Shanghai Gold Exchange | Hong Kong PMCC |

|---|---|---|---|

| Benchmark Currency | USD | RMB | USD (HAU); RMB futures under development |

| Settlement Standard | London Good Delivery (400 oz) | Domestic Chinese standard | London Good Delivery (400 oz) |

| Physical Delivery | Yes | Yes | Yes |

| Unallocated Accounts | Yes | Limited | Yes |

| Government Ownership | No | State-linked | Yes, wholly government-owned |

| Time Zone Coverage | European hours | Asian hours | Asian hours |

| Central Bank Targeting | Yes | Yes | BRI nation central banks |

Singapore announced its own gold clearing infrastructure initiative in June 2026, targeting completion by year-end. Hong Kong's July 2026 trial launch secured a clear first-mover advantage. In financial market infrastructure, this timing matters considerably more than it might in other industries.

Financial infrastructure exhibits powerful network effects. A clearing system that attracts early liquidity becomes more attractive to the next participant, which attracts more liquidity still. The self-reinforcing nature of this dynamic means that early market position is structurally difficult for later entrants to erode, even with technically superior products.

The Shanghai Gold Exchange comparison is particularly instructive. The SGE operates the world's largest physically delivered gold spot market, but its transactions are denominated in renminbi and its participation is primarily domestic. Hong Kong's system is designed to be internationally accessible in a way that the SGE currently is not, making the two systems more complementary than competitive in the near term.

The Shanghai Gold Exchange Linkage: Bridging Two Liquidity Pools

A formal mechanism linking Hong Kong's PMCC with the Shanghai Gold Exchange is under active development. The objective is to allow participants to use gold holdings in either market to settle transactions in the other, effectively treating the combined physical inventories of both systems as a single accessible liquidity pool.

Three banks were already participating in an early-stage version of this cross-border initiative at the time of the trial launch. The significance of this linkage extends well beyond operational convenience. It creates a continuous gold trading and settlement corridor that spans Asian hours from Shanghai through to Hong Kong, with connectivity to European markets through the London Good Delivery standard that both systems share at the Hong Kong end.

Gold as a Renminbi Internationalisation Tool

The linkage also serves a broader strategic function that operates at the level of Chinese monetary policy. Furthermore, China's gold influence over regional financial architecture has grown considerably as the country pursues renminbi internationalisation over more than a decade, though progress has been constrained by the absence of full capital account liberalisation. Opening China's capital account would expose the domestic financial system to external volatility in ways that Chinese policymakers have been unwilling to accept.

Gold-backed settlement offers a partial workaround. By denominating cross-border transactions in a commodity-anchored reference rather than a purely fiat currency, the system creates a pathway for international financial flows that does not require the full capital account openness that a purely RMB-denominated system would demand.

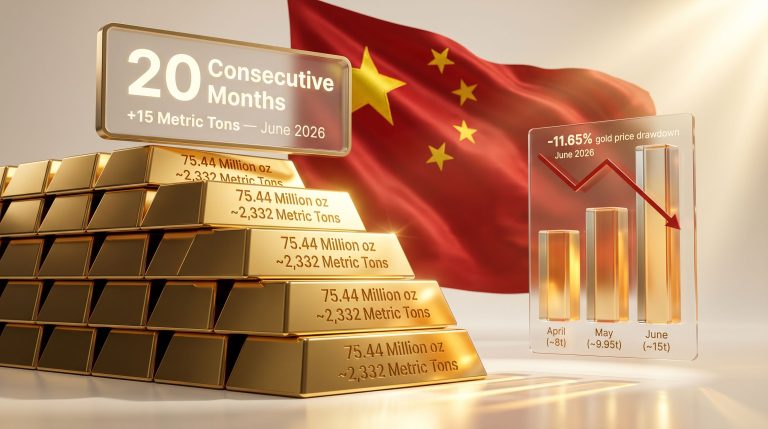

The People's Bank of China maintained central bank gold demand for 20 consecutive months, with its reserves reaching 75.44 million fine troy ounces by the end of June 2026, representing the largest monthly increase since 2023. This sustained accumulation directly expands the physical inventory base that underpins a credible clearing and settlement system. The PBOC governor confirmed at the Hong Kong FIC and Bond Connect Summit that China's central bank will continue increasing the proportion of national foreign reserves allocated to Hong Kong, functioning as both a capital commitment and a political signal of confidence in the system's long-term architecture.

The next major ASX story will hit our subscribers first

Central Bank Participation and the BRI Connection

Hong Kong has specifically targeted central banks from countries engaged in China's Belt and Road Initiative as prospective participants in the clearing system. This targeting strategy reflects a clear-eyed assessment of where institutional gold demand growth is most likely to originate over the coming decade.

BRI-aligned nations collectively hold significant central bank gold reserves and are, for a variety of geopolitical and economic reasons, increasingly motivated to conduct cross-border financial transactions through infrastructure that falls outside Western jurisdictional reach. The 2022 application of sanctions to Russia's financial system demonstrated with considerable clarity the vulnerability of nations heavily reliant on dollar-denominated clearing infrastructure. For many BRI-aligned central banks, Hong Kong's system offers an alternative settlement pathway with a commodity anchor that cannot be frozen or seized through extraterritorial financial measures.

Central bank participation serves the system's commercial interests as well as its geopolitical ones. Central banks provide large-volume, low-frequency transaction flow that stabilises clearing volumes and provides the credibility anchor necessary for a benchmark rate to be taken seriously by private sector participants.

HKEX Futures and the Completion of Hong Kong's Gold Market Stack

Hong Kong Exchanges and Clearing has relaunched its USD-denominated gold futures contract as part of the broader hub strategy. HKEX is also evaluating the development of a yuan-denominated gold futures contract, with physical delivery supported by Shanghai Gold Exchange infrastructure.

Previous HKEX attempts to establish durable gold futures liquidity did not achieve lasting traction. The current initiative is structurally different because it is built on top of an active physical clearing system with real inventory and real institutional participants, rather than being launched as a standalone instrument seeking liquidity from scratch.

The development of a yuan-denominated futures contract would, if successful, complete what might be called Hong Kong's gold market infrastructure stack. Indeed, the role of gold in the monetary system is increasingly evident in how this layered architecture is being constructed:

- OTC physical clearing provided by PMCC, using London Good Delivery bars and unallocated accounts.

- Spot price benchmark provided by HAU, distributed globally through Bloomberg.

- Futures price discovery provided by HKEX contracts, denominated in both USD and potentially RMB.

- Cross-border settlement linkage with Shanghai Gold Exchange, bridging mainland and international liquidity pools.

This four-layer architecture, if it achieves sufficient depth at each level, would constitute a fully integrated gold market ecosystem capable of operating independently of Western clearing infrastructure for the full range of institutional gold market activities.

Three Scenarios for Hong Kong's Gold Hub Trajectory

The system's ultimate impact on global gold market structure will depend on factors that cannot be predicted with certainty. Three plausible trajectories are worth considering:

Scenario One: Successful Regional Hub (Base Case)

Hong Kong establishes clear primacy in Asian institutional gold clearing. HAU gains recognition as a legitimate Asian-hours benchmark used alongside the LBMA price. HKEX's yuan-denominated futures contract achieves meaningful liquidity within three to five years. BRI nation central bank participation expands the system's reserve credibility. This scenario represents the most straightforward extension of the current trajectory.

Scenario Two: Competitive Fragmentation

Both Hong Kong and Singapore develop functioning clearing systems, dividing Asian gold liquidity between two competing hubs. Neither achieves the scale required to meaningfully challenge London's global dominance. Regional infrastructure dependency on Western systems is reduced, but a single Asian pricing centre does not emerge. HAU and any Singapore equivalent coexist as regional references without displacing the LBMA price globally.

Scenario Three: Geopolitical Disruption

Escalating tensions in the US-China relationship trigger pressure on Western financial institutions to withdraw from PMCC participation. The dual-track credibility model, which depends on the simultaneous presence of global G-SIBs and Chinese state-linked banks, breaks down. The system continues operating with Chinese and BRI-aligned participants but loses the international legitimacy required for HAU to function as a globally recognised benchmark outside the Chinese sphere of influence.

Key Market Context: Gold Prices and Structural Demand Drivers

Spot gold was trading near $4,130 per ounce at the time of the Hong Kong gold clearing system's trial launch in July 2026. Gold's multi-year bull run had encountered headwinds from rising energy prices linked to Middle East conflict, associated inflation concerns, and expectations around central bank borrowing costs, all of which traditionally weigh on a non-yielding asset. A strengthened US dollar compounded the headwind by increasing the effective cost of gold for buyers transacting in other currencies.

Despite these near-term pressures, the structural demand drivers supporting long-term gold accumulation across Asia remain intact.

| Demand Driver | Mechanism | Regional Relevance |

|---|---|---|

| Central bank reserve diversification | Reducing USD concentration | High, multiple Asian central banks actively accumulating |

| Retail wealth preservation | Gold as alternative store of value | High, deep cultural affinity across China, India, Southeast Asia |

| Geopolitical risk hedging | Flight to non-sovereign assets | Elevated, ongoing geopolitical realignments |

| RMB internationalisation | Gold as settlement medium | Growing, supported by PBOC policy signals |

| Inflation hedging | Real asset allocation | Moderate, varies with regional inflation profiles |

Several major banks reduced near-term price forecasts in mid-2026. However, year-end estimates across the institutional consensus remained above prevailing spot levels, with longer-term outlooks remaining constructive on the basis of reserve diversification and de-dollarisation dynamics.

Disclaimer: Price forecasts, scenario projections, and market outlooks discussed in this article reflect conditions and institutional estimates current at the time of the July 2026 trial launch. Gold prices are subject to significant volatility. Nothing in this article constitutes financial advice or a recommendation to buy or sell any financial instrument.

Frequently Asked Questions: Hong Kong Gold Clearing System

What is the Hong Kong gold clearing system?

It is a centrally operated settlement infrastructure for institutional gold transactions, run by Hong Kong Precious Metals Central Clearing Company Limited. Services include OTC transaction settlement, physical gold deposits and withdrawals, and delivery against the London Good Delivery standard.

What is the HAU gold benchmark?

HAU is a new gold price reference rate introduced alongside the clearing system's trial launch, now distributed through Bloomberg terminals. It is designed to provide a credible gold price reference during Asian trading hours.

Which banks are involved?

Eleven institutions are represented on the PMCC board, including JPMorgan Chase, HSBC, UBS, Standard Chartered, and five Chinese banks. HSBC has publicly committed to scaling Hong Kong gold storage to 200 metric tons.

How does it differ from the London LBMA system?

Both use the London Good Delivery standard and unallocated accounts. The key distinctions are PMCC's full government ownership, its Asian time zone coverage, direct integration with the Shanghai Gold Exchange, and the prospective development of a yuan-denominated futures contract through HKEX.

What is the connection to the Shanghai Gold Exchange?

A cross-border linkage is being built to allow gold holdings in either market to be used for settlement in the other. Three banks were participating in this initiative at launch, with the objective of creating a unified physical liquidity pool spanning both markets.

How does this relate to China's broader financial strategy?

The system provides a commodity-anchored settlement pathway that reduces reliance on US dollar clearing infrastructure. Combined with PBOC reserve allocation commitments, BRI nation central bank targeting, and the prospective RMB-denominated futures contract, it supports renminbi internationalisation without requiring full capital account liberalisation.

Want to Track the ASX Stocks Positioned to Benefit From Shifting Gold Market Dynamics?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including gold — instantly translating complex data into actionable opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.