July 7, 2026

The Architecture of a New Bullion Era: Why Asia's Gold Infrastructure Moment Has Arrived

For decades, the geography of gold pricing has been a story of institutional inertia. London sets the morning and afternoon benchmarks. New York drives futures positioning. Asia, despite consuming the majority of the world's physical gold, has functioned largely as a price-taker rather than a price-setter. That structural asymmetry is now being challenged in a deliberate and architecturally significant way, and the Hong Kong gold clearing and settlement system sits at the very centre of that challenge.

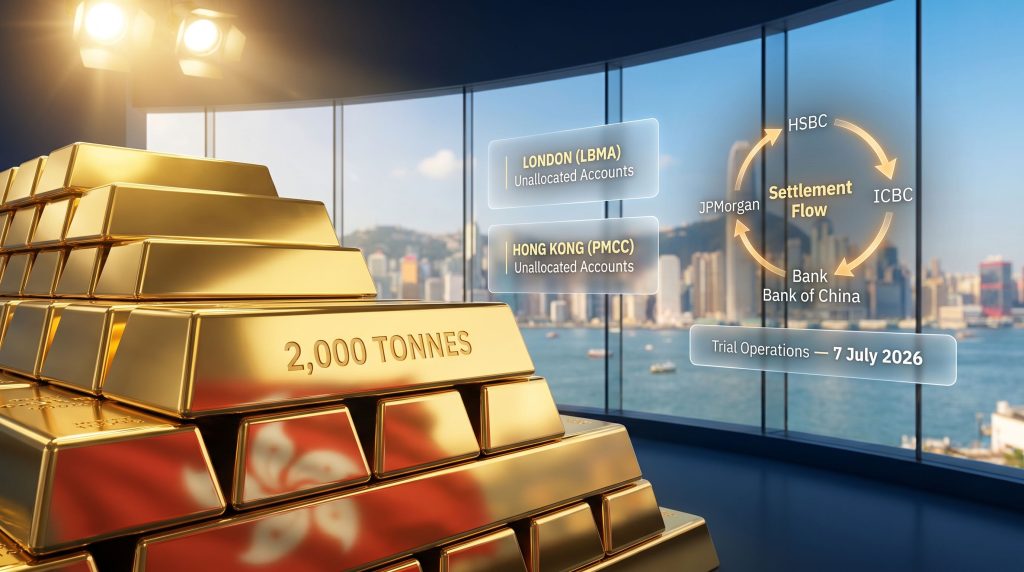

On 7 July 2026, Hong Kong inaugurated the trial operation of its gold clearing and settlement system at the Hong Kong FIC & Bond Connect Summit, a development announced by Chief Executive John Lee Ka-chiu. The operating entity behind the system is the government-owned Hong Kong Precious Metals Central Clearing Company, widely referred to as the PMCC. What makes this more than a ceremonial launch is the combination of institutional participants, settlement mechanics, currency options, and physical storage ambitions that underpin it.

When big ASX news breaks, our subscribers know first

Understanding the Strategic Gap the PMCC Is Designed to Fill

Asia's Consumption vs. Asia's Market Power

The fundamental tension driving Hong Kong's gold market ambitions is straightforward. Asia accounts for a dominant share of global physical gold demand, yet the pricing and clearing infrastructure that governs gold transactions has historically been concentrated in Western financial centres. Furthermore, China and India together represent the world's two largest gold-consuming nations, and mainland China has been the world's largest gold producer for over a decade.

Despite this, benchmark pricing has remained anchored to the LBMA and COMEX gold markets — specifically the London Bullion Market Association framework and USD-denominated futures on the COMEX exchange in New York. This mismatch creates practical inefficiencies for Asian market participants:

- Asian buyers and sellers must transact at prices set during London and New York hours, often accepting spread costs that reflect timezone and infrastructure gaps.

- Physical gold flowing into and out of mainland China passes through Hong Kong, yet there has been no dedicated central clearing mechanism in the city to formalise and net those flows.

- RMB-denominated gold settlement has been structurally unavailable at the institutional OTC level in Hong Kong, limiting yuan internationalisation in one of the asset classes where China holds genuine physical leverage.

The PMCC is designed to address each of these gaps simultaneously.

Geopolitical Volatility as a Structural Catalyst

Chief Executive John Lee framed the clearing system's launch within a broader macroeconomic argument: that gold is increasingly being used by sovereign and institutional actors as a core instrument for liquidity management and risk mitigation. This perspective reflects observable trends in central bank behaviour globally, where net gold purchases have risen sharply following the freezing of Russian sovereign reserves in 2022.

That moment accelerated institutional re-evaluation of exposure to USD-denominated settlement systems. Consequently, the way central banks influencing gold prices has shifted considerably in recent years. A gold clearing system that operates in RMB and integrates with mainland Chinese infrastructure offers institutional actors an alternative settlement pathway that does not rely on Western financial rails.

What the PMCC Actually Is and How It Operates

Government Ownership and Institutional Mandate

The PMCC is a government-owned entity, which distinguishes it from privately operated clearing houses or exchange-affiliated settlement mechanisms. The Financial Services and the Treasury Bureau (FSTB) holds oversight responsibility for the rollout, and the system has been positioned as a deliberate act of public financial infrastructure development rather than a commercial venture seeking short-term profitability.

This ownership structure matters because it signals long-term commitment to building the ecosystem even through periods of low utilisation or teething challenges during the trial phase. The PMCC's core service offering spans three primary functions:

- Gold deposits and withdrawals: Participants can move physical gold in and out of the system against unallocated account balances.

- OTC transaction settlement: The clearing house nets and settles over-the-counter gold trades between participating institutions, reducing bilateral settlement risk.

- Multi-currency settlement: The system is designed to accommodate both RMB and USD-denominated transactions, a critical design feature for attracting both mainland-oriented and internationally oriented participants.

The Mechanics of Unallocated Gold Accounts

The operational model at the heart of the PMCC mirrors the mechanism that made London the world's dominant bullion trading centre. Unallocated gold accounts allow participants to hold a claim on a specific quantity of gold without being assigned ownership of individually identified, numbered bars held in a specific vault. Instead, the participant holds a fungible claim against the pool of gold held by the clearing institution.

This structure delivers several critical advantages for institutional trading:

- Transaction velocity: Trades settle as ledger entries rather than requiring physical movement of bars, dramatically accelerating settlement cycles.

- Scalability: Large-volume trading can occur without the logistical bottlenecks of bar-by-bar allocation and physical delivery.

- Netting efficiency: A central counterparty can calculate net positions across multiple institutions and settle only the residual differences, reducing the total volume of gold that needs to physically change hands.

- Market access: Smaller participants, including refiners and jewellers, can access institutional-grade clearing without maintaining their own bilateral clearing relationships with every counterparty.

The unallocated account model is often misunderstood by retail observers as a form of fractional gold ownership that implies risk of non-delivery. In institutional clearing contexts, it is instead a mechanism for operational efficiency within a system where physical gold underpins the total pool of claims, and participants retain the right to convert to allocated holdings or take physical withdrawal.

Step-by-Step: How a Settlement Transaction Flows Through the PMCC

Understanding the mechanics of a single settlement cycle clarifies why central clearing represents a meaningful structural improvement over bilateral OTC arrangements:

- A participating institution executes a buy or sell order in Hong Kong's OTC gold market with a counterparty.

- Both sides submit trade details to the PMCC for central clearing.

- The PMCC validates each counterparty's unallocated account position and available balances.

- Net settlement is calculated across all participating institution positions at the end of the settlement cycle, reducing gross exposure to a single net figure per participant.

- Final settlement entries are posted across member unallocated accounts, with gold credits and debits reflecting net positions rather than gross trade volumes.

- Participants requiring physical gold can request withdrawal of bars against their unallocated balance, converting paper claims into physical metal held in certified vault facilities.

The Founding Participants: Who Is Already Inside the System

The first settlement transaction conducted through the PMCC involved multiple banks, refiners, mining companies, and jewellery firms. The breadth of participant types is strategically important: a clearing system that captures the full supply chain from mine to end consumer has significantly greater utility than one limited to financial institutions.

The 11 founding participants include a cross-section of Western and Asian financial institutions:

| Institution | Headquarters | Market Role |

|---|---|---|

| HSBC | London / Hong Kong | Global bullion dealer and custodian |

| JPMorgan Chase | United States | Major OTC gold market maker |

| UBS | Switzerland | Precious metals trading desk |

| ICBC | China | Largest Chinese state-owned bank |

| Bank of China | China | Key RMB clearing institution |

| 6 additional participants | Various | Refiners, mining companies, jewellers |

The inclusion of refiners and mining companies is particularly noteworthy from a market structure perspective. Historically, these participants have accessed bullion markets through intermediary banks, accepting pricing and settlement terms set by institutions with greater market power. A clearing system that admits them directly reduces their dependency on financial intermediaries and potentially improves the economics of their market access.

How Hong Kong's System Compares to London and Shanghai

Benchmarking the Three Major Global Bullion Hubs

| Feature | London (LBMA) | Shanghai (SGE) | Hong Kong (PMCC) |

|---|---|---|---|

| Settlement Model | Unallocated accounts | Physical delivery-focused | Unallocated accounts |

| Primary Currency | USD | RMB | RMB and USD |

| Vault Infrastructure | London-based vaults | SGE-certified HK vaults | Expanding toward 2,000 tonnes |

| Price-Setting Role | Global benchmark | Regional benchmark | Emerging participant |

| Regulatory Jurisdiction | UK / FCA | Mainland China | HKSAR / FSTB |

The SGE Connection: Infrastructure That Already Exists

One of the least-appreciated advantages Hong Kong brings to this ambition is that Shanghai Gold Exchange-certified vault infrastructure already exists within the territory. The SGE established vault facilities in Hong Kong in earlier years as part of its international board operations, meaning the PMCC does not need to build physical storage capacity from scratch. The detailed clearing and settlement rules of the Shanghai Gold Exchange, furthermore, have provided a regulatory blueprint that informed the PMCC's own operational framework.

This pre-existing SGE relationship also creates a structural bridge between the onshore mainland gold market and the offshore Hong Kong market. Gold traded on the SGE's international board in Shanghai can flow into and out of Hong Kong's PMCC system, enabling cross-border gold movements that link China's vast domestic demand with internationally oriented clearing and pricing mechanisms. In addition, China's gold market dominance as both the world's largest producer and consumer adds considerable weight to this infrastructure's long-term significance.

The 2,000-Tonne Storage Expansion Target

Hong Kong's stated ambition to expand gold storage capacity to 2,000 tonnes within three years of the PMCC launch is a significant signal of long-term commitment. Vault capacity is not merely a logistical detail; it is the physical foundation that distinguishes a serious bullion hub from a paper clearing mechanism. Without meaningful sovereign-scale storage, a clearing system cannot credibly offer physical settlement as a backstop for unallocated account holders.

Scaling to 2,000 tonnes of storage capacity would position Hong Kong's vault infrastructure in a comparable tier to the facilities that underpin London's role as the world's largest physical gold trading centre, where the Bank of England alone holds approximately 400,000 gold bars in its vaults on behalf of central banks and commercial institutions.

The RMB Settlement Dimension and Yuan Internationalisation

Why Currency Denomination Matters in Gold Clearing

The PMCC's capacity to settle gold transactions in RMB rather than exclusively in USD introduces a dimension that extends well beyond bullion market mechanics. Gold priced and settled in yuan creates a pathway for countries accumulating excess RMB balances through trade surpluses with China to convert those balances into a universally accepted hard asset without passing through USD-denominated systems.

This mechanism is particularly relevant for commodity-exporting nations in Asia, Africa, and the Middle East that have increased trade invoicing in RMB as bilateral trade with China has grown. The ability to exchange RMB for gold through a regulated, institutionally credible clearing mechanism in Hong Kong reduces the friction associated with holding large yuan balances. Moreover, it strengthens the case for accepting RMB in trade settlement in the first place. This dynamic forms part of a broader global monetary shift and gold reorientation that has accelerated meaningfully since 2022.

Counterparty Risk Reduction Through Central Clearing

One of the most technically significant but least publicly discussed benefits of the PMCC model is counterparty risk reduction in the OTC gold market. Bilateral OTC gold trading, which has historically dominated the market outside of exchange-traded futures, exposes each counterparty to the credit risk of the other. If one side of a trade defaults before settlement, the other party faces both replacement cost risk and potential loss of principal.

Central clearing interposes the PMCC as the buyer to every seller and the seller to every buyer, concentrating and managing counterparty risk within a regulated, capitalised entity. This is the same structural rationale that drove the migration of interest rate swaps and credit derivatives toward central clearing after the 2008 financial crisis, and it applies with equal force to the gold OTC market.

The next major ASX story will hit our subscribers first

Key Milestones and the PMCC Rollout Timeline

| Phase | Timeline | Primary Objective |

|---|---|---|

| Preparatory Stage | Pre-July 2026 | Regulatory approvals and participant onboarding |

| Trial Operations | July 2026 | First live settlements and system stress testing |

| Operational Stability Review | Late 2026 | Performance validation and participant expansion |

| Full Commercial Launch | TBC 2026-2027 | Open market participation and full RMB settlement |

| Storage Expansion | Within 3 years | Scale vault capacity to 2,000 tonnes |

The trial operations phase is critically important and frequently underestimated in market commentary. Trial periods for financial market infrastructure serve multiple simultaneous functions: they identify operational failure points before full commercial volumes stress the system, they allow participant compliance teams to validate internal procedures against live settlement flows, and they build the institutional confidence needed to attract secondary waves of participants who were unwilling to join at inception.

Implications for Gold Price Discovery in Asian Trading Hours

Perhaps the most consequential long-term question surrounding the Hong Kong gold clearing and settlement system is whether Hong Kong can eventually influence the gold price benchmark during Asian trading hours. At present, the LBMA Gold Price auction produces the globally recognised USD reference price at 10:30am and 3:00pm London time — both outside Asian business hours.

The result is that Asian market participants begin their trading day reacting to a price set in a prior timezone rather than participating in its formation. A functioning, liquid clearing and settlement system in Hong Kong creates the preconditions, though not the guarantee, of Asian price discovery. For benchmark influence to materialise, the PMCC would need to develop sufficient daily trading volume to generate observable price signals and attract the participation of price-sensitive large-scale buyers.

None of these developments are confirmed at the trial operations stage, and investors and analysts should consequently treat them as speculative long-term possibilities rather than near-term certainties.

Frequently Asked Questions: Hong Kong Gold Clearing and Settlement System

What is the Hong Kong Precious Metals Central Clearing Company?

The PMCC is a government-owned entity established to provide gold clearing and settlement services in Hong Kong, including gold deposits and withdrawals, and OTC transaction settlement.

How does unallocated gold settlement differ from physical gold ownership?

An unallocated gold account represents a claim on a quantity of gold held within a pool rather than ownership of specific numbered bars. It enables faster, scalable institutional trading while retaining the right to convert to physical metal.

Which institutions are participating in the system?

The 11 founding participants include HSBC, JPMorgan Chase, UBS, ICBC, Bank of China, and additional institutions from the refining, mining, and jewellery sectors.

Will the system settle in RMB or USD?

The PMCC is designed to accommodate both RMB and USD settlement, with the RMB capability being particularly significant for yuan internationalisation objectives.

How does the system relate to the Shanghai Gold Exchange?

SGE-certified vault infrastructure already exists in Hong Kong, providing a pre-existing physical foundation for the PMCC and a mechanism for cross-border gold flows between mainland China and the offshore Hong Kong market.

What is the vault storage expansion target?

Hong Kong aims to expand its gold storage capacity to 2,000 tonnes within three years of the PMCC launch.

When did trial operations begin?

Trial operations were inaugurated on 7 July 2026, announced at the Hong Kong FIC & Bond Connect Summit by Chief Executive John Lee Ka-chiu.

Could Hong Kong eventually influence global gold price benchmarks?

This remains a long-term possibility rather than a near-term certainty. Benchmark influence would require significant growth in PMCC trading volumes and the potential establishment of a formal Asian price discovery mechanism. However, the gold reserves and central banks accumulation trend suggests institutional appetite for such a mechanism is growing.

Key Facts at a Glance

| Metric | Detail |

|---|---|

| Trial Launch Date | 7 July 2026 |

| Operating Entity | Hong Kong Precious Metals Central Clearing Company (PMCC) |

| Settlement Model | Unallocated accounts, mirroring London's LBMA structure |

| Founding Participants | 11 institutions including HSBC, JPMorgan, UBS, ICBC, Bank of China |

| Settlement Currencies | RMB and USD |

| Vault Expansion Target | 2,000 tonnes within three years |

| SGE Integration | Certified vault infrastructure already in place |

| Regulatory Oversight | Financial Services and the Treasury Bureau (FSTB) |

From Infrastructure to Influence: What Still Needs to Happen

Inaugurating trial operations is a necessary first step, but the distance between a functioning clearing system and a genuinely influential bullion hub is measured in liquidity, not just architecture. London's dominance was not built on regulatory frameworks alone; it was built on centuries of accumulated trading relationships, vault expertise, and the network effects that arise when market participants default to the most liquid venue because everyone else does too.

For the Hong Kong gold clearing and settlement system to meaningfully shift the global bullion landscape, several conditions need to develop beyond the current trial phase. Participant numbers need to expand well beyond the founding 11. Daily clearing volumes need to reach thresholds that make the PMCC a necessary rather than optional routing point for Asian gold flows. Furthermore, the RMB settlement capability needs to attract sovereign-level users, including central banks, whose participation would validate the system's credibility as an alternative to Western clearing networks.

None of this diminishes the significance of what was inaugurated on 7 July 2026. The creation of institutional infrastructure is the essential prerequisite for everything that follows. What Hong Kong has built is the foundation; what gets constructed on top of it will be determined by the choices of institutions, sovereigns, and market participants over the years ahead.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and speculative analysis regarding market development, price discovery influence, and institutional participation are inherently uncertain and should not be relied upon as the basis for investment decisions. Readers should conduct their own independent research and consult qualified financial advisers before making any investment-related decisions.

Want to Track the ASX Mining Companies Positioned in the Gold Sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into clear, actionable insights for investors at every level — explore historic discovery returns on Discovery Alert's discoveries page to understand the scale of opportunity, and begin your 14-day free trial today to secure a market-leading edge.