June 9, 2026

The Invisible Industrial Metal Hiding in Plain Sight

Most conversations about gold fixate on price charts, central bank reserves, and the age-old debate about whether it belongs in an investment portfolio. What rarely surfaces in these discussions is something far more concrete: gold is quietly embedded in the infrastructure of the modern digital economy, and its industrial footprint is expanding in ways that most investors and commentators have not fully accounted for.

The rise of artificial intelligence hardware, electric vehicle powertrains, and next-generation wireless networks has created a new class of gold consumer, one that is less sensitive to price movements and more driven by technical necessity. Understanding how gold demand in technology and electronics actually works, where it flows, why it is growing, and where it faces pressure, offers a genuinely different lens through which to evaluate this metal's long-term relevance. Furthermore, exploring why gold remains valuable in modern industrial applications helps contextualise this demand within the broader investment landscape.

When big ASX news breaks, our subscribers know first

How Much Gold Does the Technology Sector Actually Use?

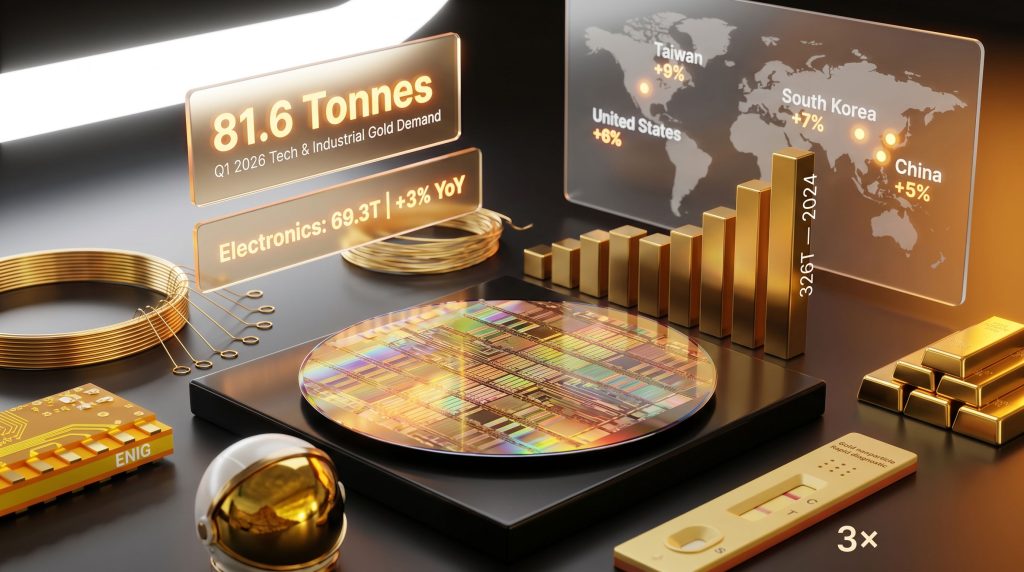

In the first quarter of 2026, technology and industrial applications consumed a combined 81.6 tonnes of gold, representing a 1% year-on-year increase. That figure alone challenges the persistent narrative that gold serves no functional purpose beyond ornamentation and wealth storage.

The electronics segment was the primary driver, accounting for 69.3 tonnes of that total, up 3% compared to Q1 2025. Other industrial uses outside electronics declined by 8% to 10.4 tonnes, while dentistry continued its structural retreat, falling below 2 tonnes for the first time on record.

Q1 2026 Technology and Industrial Gold Demand at a Glance

| Application Segment | Q1 2026 Volume | Year-on-Year Change |

|---|---|---|

| Total Tech and Industrial | 81.6 tonnes | +1% |

| Electronics (total) | 69.3 tonnes | +3% |

| Other Industrial Applications | 10.4 tonnes | -8% |

| Dentistry | Below 2 tonnes | Declining trend |

To contextualise these numbers within the broader gold market, technology and electronics typically represent somewhere between 5% and 10% of total global gold demand, though some broader industry analyses place this figure closer to 17.6% depending on the scope of the dataset used. Jewellery fabrication remains the single largest demand category at roughly 44% of total consumption, with approximately 300 tonnes used in jewellery production in Q1 2026 alone. Investment flows and central bank gold buying continue to dominate price discovery, but technology demand is accumulating structural weight that is increasingly difficult to dismiss.

Full-year 2024 technology demand reached 326 tonnes, up 7% year-on-year, with the electronics subsegment contributing 271 tonnes for a 9% annual gain. Into 2025, the sector broadly held its ground at 323 tonnes total, with electronics stable at 270 tonnes, suggesting the demand base has consolidated rather than retreated.

The AI Infrastructure Effect: A Structural Shift, Not a Cyclical Blip

The most consequential development reshaping gold demand in technology and electronics over the past two years has been the aggressive scaling of artificial intelligence hardware. This is not a temporary demand spike driven by speculative excitement. It is a structural change rooted in the physical requirements of running large-scale AI computations.

AI servers differ fundamentally from conventional server hardware in their thermal and reliability demands. These machines generate substantially more heat per unit, require significantly higher memory density, and must operate continuously without failure across multi-year lifecycles. Each of these characteristics points directly toward increased gold content.

According to the World Gold Council's technology demand research, AI servers and automotive power modules require greater quantities of gold specifically to manage heat dissipation and to ensure long-term operational reliability and longevity. In these applications, technical specifications take precedence over material cost considerations, which is precisely why record gold prices have not dampened demand in this segment.

The flow-on effects through the semiconductor supply chain are considerable:

- AI server shipments are driving sharp growth in demand for DRAM and NAND memory chips, both of which use gold in bonding wire, interconnects, and contact metallisation

- Higher memory requirements per AI server compound total gold use, since each additional memory module introduces additional gold-bearing components

- The proliferation of AI-enabled PCs and mobile devices is extending this demand dynamic further down the consumer hardware stack

- Automotive power modules in electric vehicles and advanced driver-assistance systems are absorbing more gold as performance and longevity thresholds tighten

- The rollout of Wi-Fi 7 and the continued expansion of power amplifiers in wireless infrastructure are supporting gold use in compound semiconductor processes

The World Gold Council has noted that the growing share of advanced applications is strengthening and diversifying technology-sector demand while simultaneously making the sector more resilient to fluctuations in traditional consumer electronics purchasing.

Consumer Electronics: The Counter-Current

While premium AI and industrial applications are pulling gold demand upward, the mass consumer electronics market is moving in the opposite direction. Manufacturers of smartphones, standard laptops, and commodity peripherals have intensified gold thrifting and substitution programmes in response to elevated metal prices.

This creates a genuinely two-speed dynamic within the same sector. At the high end, gold intensity per device is rising. At the commodity end, it is falling. The net result in Q1 2026 was modest overall growth, which may actually understate the magnitude of the shift occurring beneath the surface: the applications consuming more gold are precisely those where demand is least price-elastic and most structurally durable.

Why Gold Cannot Simply Be Replaced in Advanced Electronics

A common assumption among those unfamiliar with materials science is that gold's industrial role is largely a historical artefact, and that cheaper alternatives will eventually displace it. The reality is considerably more complicated, particularly in high-reliability applications.

Gold possesses a specific combination of physical and chemical properties that competing materials cannot fully replicate at the tolerances required by advanced semiconductor manufacturing:

- Corrosion and oxidation resistance at the nanoscale, where even trace degradation of a contact surface can introduce signal errors

- Electrical conductivity sufficient to minimise resistance losses across micro-scale interconnects operating at high frequencies

- Thermal conductivity capable of managing heat loads in processors running at sustained high power output

- Malleability that permits the drawing of bonding wire to diameters measured in microns without compromising tensile integrity

- Chemical stability in environments where contamination at the parts-per-billion level can compromise yields across an entire production batch

In lower-tier semiconductor packaging and commodity electronics, copper and aluminium bonding wire have made meaningful inroads as substitutes. Advanced ceramics have replaced gold in dentistry and certain industrial sealing contexts. Silver and palladium compete in specific connector applications. However, these substitution pressures are predominantly concentrated in cost-sensitive, lower-margin segments. The applications generating new demand, specifically AI accelerator chips, automotive power modules, and compound semiconductors for 5G and Wi-Fi 7 infrastructure, remain technically constrained in their ability to substitute away from gold.

Regional Demand: Where the Growth Is Concentrated

The geographic distribution of electronics gold demand in Q1 2026 reflects the underlying concentration of advanced semiconductor manufacturing capacity globally.

Regional Electronics Gold Demand: Q1 2026

| Country/Region | YoY Demand Change | Primary Growth Driver |

|---|---|---|

| Taiwan | +9% | AI-related chip and semiconductor demand |

| South Korea | +7% | High memory output, strong fab utilisation |

| United States | +6% | Domestic AI infrastructure buildout, EV demand |

| Mainland China | +5% | Domestic supply chain expansion |

| Japan | -1% | Weak manufacturing growth |

| Europe | -3% | Stagnant consumer demand, slow industrial recovery |

Taiwan's 9% surge directly reflects its position at the centre of global AI chip fabrication. South Korea's 7% growth was described by the World Gold Council as unexpectedly strong, driven by high memory chip output and robust fab utilisation rates, both of which are direct consequences of AI server procurement cycles. The United States posted 6% growth on the back of domestic AI data centre buildout and electric vehicle demand. China recorded 5% growth tied to the continued expansion of its domestic semiconductor supply chain.

Japan and Europe's underperformance highlights a structural vulnerability. Both regions remain disproportionately exposed to traditional consumer electronics manufacturing without a compensating industrial base in AI hardware or EV powertrains, the two segments generating the strongest incremental gold demand globally.

Gold's Broader Industrial Footprint Beyond Electronics

Medical Diagnostics: Gold at the Molecular Scale

One of the least widely understood applications of gold in industry is its central role in rapid diagnostic testing. Gold nanoparticles form the detection mechanism in hundreds of millions of Rapid Diagnostic Tests deployed globally each year. These lateral flow assays, the same fundamental technology platform used in COVID-19 home testing kits, rely on gold nanoparticles as colourimetric indicators to signal the presence of target antigens.

The World Gold Council has characterised gold as being at the heart of this diagnostic technology, which has fundamentally changed the way infectious diseases including malaria, HIV, and hepatitis are detected and managed in healthcare systems with limited laboratory infrastructure. The optical and chemical properties of gold nanoparticles make them uniquely suited to this application, and no cost-competitive substitute has emerged at scale.

Research published in 2018 by a team of Chinese scientists demonstrated that nanowires constructed from gold and titanium could partially restore light sensitivity in blind mice by acting as photoreceptor replacements. While this research remains at an early experimental stage, it illustrates the expanding frontier of gold's biomedical relevance beyond its established diagnostic applications.

Space Exploration and Extreme-Environment Technology

Gold-coated visors on astronaut helmets serve a function that no alternative material currently matches at the required weight and performance specification: reflecting infrared radiation while maintaining optical clarity against solar glare. NASA and international space agencies continue to incorporate gold in mission-critical satellite components and deep-space instrumentation, where corrosion resistance and thermal stability over decade-long operational lifespans are non-negotiable requirements.

The Decline of Dental Gold

Perhaps the clearest illustration of gold facing genuine displacement is in dentistry. Gold used in dental restorations fell below 2 tonnes in Q1 2026, a historic low driven by the widespread adoption of advanced ceramic and composite materials. These alternatives offer comparable durability with superior aesthetic results, and their adoption has been essentially irreversible. This segment's contraction serves as a useful reminder that gold's industrial demand profile is not uniformly expanding: legacy applications are being phased out even as advanced technology applications grow.

The next major ASX story will hit our subscribers first

Emerging Applications Expanding Gold's Technology Role

Several next-generation technology domains are establishing new demand vectors for gold beyond its established semiconductor applications. In addition, analysts tracking the gold market outlook are increasingly factoring these emerging use cases into longer-term price projections:

- Micro-LED displays use gold in bonding and contact layers for premium screen panels and automotive display systems, a fast-growing market segment

- UV LED technology deployed in medical sterilisation, diagnostic equipment, and industrial curing processes incorporates gold contacts to maintain performance at high power densities

- Wi-Fi 7 infrastructure rollout is expanding gold consumption in compound semiconductor power amplifiers built on gallium arsenide and gallium nitride processes

- Hyperscale data centre power modules are increasing gold content per installation to manage thermal loads generated by AI accelerator clusters

- LED demand in Q1 2026 fell modestly by 1%, with price pressures in general lighting offset by growth in micro-LED, automotive lighting, and UV LED categories

The World Gold Council has observed that while traditional gold wire faces substitution in lower-end applications, the AI boom is increasing demand for high-purity gold in advanced applications at a rate that more than offsets legacy declines, reinforcing gold's critical role in high-performance semiconductor manufacturing. According to industry analysis on technology-driven demand, this trend is expected to intensify as semiconductor architectures become increasingly complex.

What This Means for Investors: Technology as a Structural Demand Floor

For investors evaluating gold's long-term demand fundamentals, the technology sector's trajectory offers a perspective that is frequently overlooked in mainstream analysis. Technology demand is not the dominant price driver for gold, that distinction remains with investment flows and central bank purchasing. However, it provides something those categories cannot: a structurally sticky demand base that is less cyclically volatile and increasingly concentrated in applications where price elasticity is low.

Consequently, investors considering physical gold vs ETFs as exposure vehicles should factor in this expanding industrial base as a meaningful contributor to long-term demand resilience. Furthermore, those evaluating gold as a safe haven will find that technology demand adds an additional layer of fundamental support that is structurally distinct from macroeconomic sentiment cycles.

The five structural forces that are most likely to shape gold demand in technology and electronics over the next decade are:

- AI infrastructure scaling at both the hyperscale data centre level and the edge computing tier, driving sustained demand for high-purity gold in advanced semiconductor packaging

- Electric vehicle adoption increasing gold content per vehicle through power modules, battery management systems, and ADAS components across a growing global fleet

- Next-generation wireless standards including Wi-Fi 7, 5G Advanced, and early 6G research expanding compound semiconductor demand where gold remains technically essential

- IoT device proliferation adding cumulative demand from billions of connected sensors and edge devices, each containing trace gold quantities that aggregate to meaningful volumes

- Advanced medical technology expanding gold's role in diagnostic platforms, nanomedicine research, and next-generation imaging applications globally

Disclaimer: The analysis and projections presented in this article are based on publicly available data and research, including World Gold Council publications. They do not constitute financial advice. Forecasts about future demand trends involve uncertainty and should not be relied upon as the sole basis for investment decisions.

Frequently Asked Questions: Gold Demand in Technology and Electronics

Why is gold used in electronics rather than cheaper metals?

Gold's combination of corrosion resistance, long-term chemical stability, and electrical conductivity makes it uniquely reliable in high-stakes electronic environments. In systems where a single contact failure could compromise an entire server rack or safety-critical automotive module, the cost premium is routinely judged to be justified by the performance characteristics.

How much gold is in a typical smartphone?

A standard smartphone contains approximately 0.03 grams of gold, primarily concentrated in circuit board connectors, bonding wires, and processor contacts. Individually negligible, but across billions of devices manufactured annually, the cumulative volume is substantial.

Does a rising gold price reduce technology demand?

In consumer electronics, yes. Manufacturers actively pursue substitution and thrifting programmes when prices are elevated. In AI hardware, automotive power modules, and medical diagnostics, the answer is largely no. At the component level, performance requirements override material cost considerations in these segments.

What percentage of global gold demand comes from technology?

Estimates range from approximately 5% to 10% of total global demand under standard methodology, with some broader analyses reaching 17.6%. The World Gold Council reported full-year 2024 technology demand at 326 tonnes, against a global demand base of several thousand tonnes annually.

Is AI demand for gold permanent or cyclical?

The mechanism driving AI-related gold demand is structural rather than cyclical. It is rooted in the physical requirements of high-performance chip packaging, memory density, and thermal management, none of which are resolved by next-generation architecture alone. The transition to more advanced semiconductor nodes typically increases, not decreases, precision material requirements per chip.

Want to Track ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, transforming complex mineral data into actionable investment insights across more than 30 commodities — from gold to the metals powering next-generation technology infrastructure. Start your 14-day free trial at Discovery Alert today, or explore the historic returns major discoveries have delivered to understand the opportunity at stake.