August 10, 2026

What Defines the Current Gold Market Transformation?

Global financial markets are witnessing a profound recalibration of monetary systems as institutional investors and sovereign entities fundamentally reassess their relationship with traditional reserve assets. This transformation extends far beyond cyclical investment patterns, representing a structural shift in how capital allocators perceive risk, value preservation, and monetary sovereignty in an era of unprecedented fiscal expansion and geopolitical uncertainty.

The precious metals sector has emerged as a focal point for this broader monetary evolution, with gold specifically demonstrating behaviour that defies conventional market relationships and historical precedents. Furthermore, this paradigm shift in gold market dynamics reflects deeper concerns about the stability and neutrality of existing monetary infrastructure. Rather than responding to traditional drivers such as interest rate differentials or inflation expectations, gold has exhibited characteristics suggesting its role as a monetary asset is being reestablished at the institutional level.

The convergence of weaponised financial systems, unsustainable fiscal trajectories, and the erosion of traditional safe-haven asset reliability has created conditions where gold's historical monetary function becomes increasingly relevant to modern portfolio construction. For instance, recent analysis suggests the historic gold surge represents fundamental market realignment rather than speculative behaviour.

When big ASX news breaks, our subscribers know first

Why Are Central Banks Driving Unprecedented Gold Accumulation?

Record-Breaking Official Sector Purchases

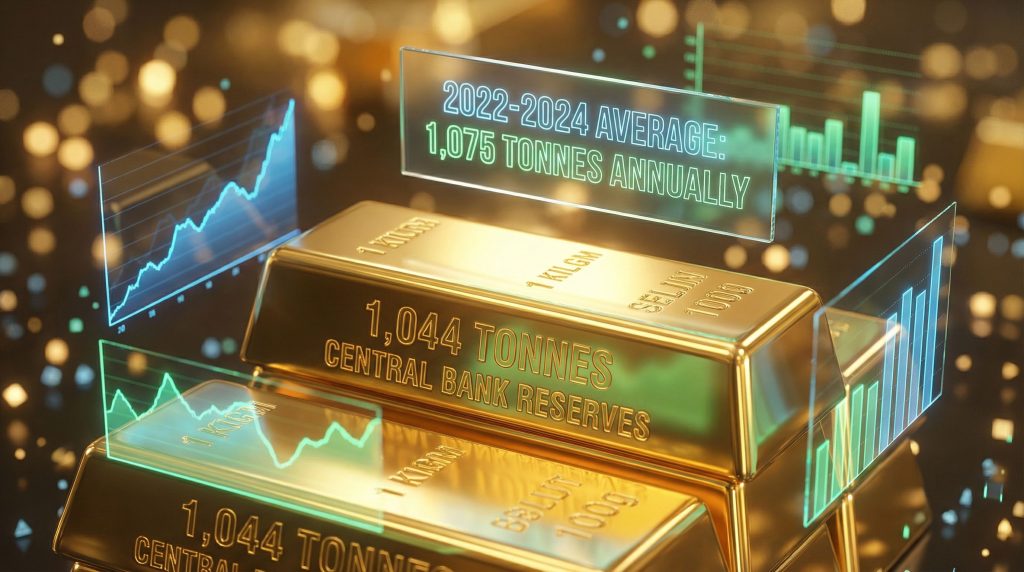

Central banking institutions have orchestrated the most sustained precious metals acquisition campaign in modern monetary history. Official sector net purchases reached 1,044.6 tonnes in 2024, marking the third-highest annual accumulation since comprehensive records began in 1950. This figure represents only a marginal decrease of 6.2 tonnes from 2023 levels and sits just 91 tonnes below the all-time record of 1,136 tonnes established in 2022.

The magnitude of this institutional accumulation becomes clear when compared to historical baselines. Between 2010 and 2021, central banks averaged 473 tonnes of net gold purchases annually. However, the three-year period from 2022-2024 has witnessed average annual purchases of 1,075 tonnes, representing a 127% acceleration above the previous decade's baseline.

Central Bank Gold Accumulation Trends:

• 2022: 1,136 tonnes (record high since 1971)

• 2023: 1,051 tonnes

• 2024: 1,045 tonnes

• Historical average (2010-2021): 473 tonnes annually

• Growth rate above baseline: +127%

This sustained accumulation pattern indicates deliberate policy implementation rather than opportunistic purchasing. Consequently, the consistency across multiple years demonstrates coordinated institutional decision-making reflecting structural concerns about existing reserve asset frameworks.

Geographic Distribution of Official Demand

The geographic pattern of gold accumulation reveals distinct regional strategies driven by specific monetary and geopolitical considerations. Emerging Asian economies have prioritised currency diversification initiatives, targeting reductions in USD reserve allocations below 60% thresholds while building gold positions as hedge against sanctions exposure and trade tension escalation.

Regional Gold Accumulation Strategies:

| Region | Primary Motivation | Strategic Implementation |

|---|---|---|

| Emerging Asia | Currency diversification | Reduce USD dependency to <60% of reserves |

| Middle East | Oil revenue recycling | Neutral asset amid regional tensions |

| Eastern Europe | Monetary sovereignty | Buffer against external monetary shocks |

| Latin America | Inflation protection | Hedge against currency devaluation |

Middle Eastern sovereign entities have utilised oil revenue recycling mechanisms to establish gold positions serving dual functions as geopolitical insurance and portfolio diversification tools. The neutral, non-correlated nature of gold provides these nations with reserve assets independent of major power bloc monetary systems.

Eastern European central banks have emphasised gold's role in monetary sovereignty assertion, particularly as protection against external monetary policy transmission and currency manipulation. These institutions view gold accumulation as essential infrastructure for maintaining domestic monetary policy independence.

The scope of this accumulation extends beyond traditional geopolitical adversaries to include nations historically aligned with Western monetary systems. This broad-based participation indicates the driving forces are structural monetary concerns rather than purely political considerations.

How Has Geopolitical Risk Restructured Investment Paradigms?

The Weaponisation Impact on Reserve Management

The spring 2024 threat by the U.S. administration to liquidate approximately $300 billion in frozen Russian sovereign assets fundamentally altered global perceptions of reserve asset security. This action demonstrated that even U.S. Treasury holdings, previously considered the ultimate safe-haven investment, carry seizure and liquidation risks that were previously theoretical considerations.

The timing correlation between this weaponisation threat and gold's bubble behaviour indicates direct market recognition of the precedent being established. Reserve managers at over 40 central banks initiated formal gold allocation reviews following this demonstration of monetary infrastructure weaponisation.

The foundations of the international monetary system, in which the U.S. dollar had long served as lynchpin, experienced fundamental disruption as reserve managers sought assets that could not be seized and were not the liability of another sovereign.

Institutional Response to Asset Weaponisation:

• Central banks conducting gold allocation reviews: 40+

• Sovereign wealth funds increasing non-USD allocations: 15-25%

• Regional monetary unions exploring gold-backed settlements

• Alternative payment system development acceleration

The absence of subsequent policy statements reversing or limiting the use of asset seizure as foreign policy tools perpetuates institutional uncertainty. This ongoing ambiguity maintains pressure for reserve diversification even among traditional allies of the United States.

De-dollarisation Acceleration Patterns

The systematic reduction of USD exposure across global reserve managers reflects recognition of fundamental changes in American fiscal sustainability and international creditor status. Current U.S. government debt of $38 trillion combined with November 2025 deficit spending of $173.28 billion illustrates the structural nature of fiscal deterioration despite increased tariff revenues.

This fiscal backdrop contrasts sharply with conditions during gold's previous major bull market in the late 1970s. At that time, the United States maintained significant international creditor status with government debt representing approximately 30% of GDP. Today's debt-to-GDP ratio exceeds 120%, whilst the nation has become the world's largest debtor.

Comparative Fiscal Analysis: 1979 vs. 2025

| Metric | 1979 | 2025 | Change Factor |

|---|---|---|---|

| Debt-to-GDP Ratio | ~30% | ~120% | 4x deterioration |

| International Status | Net creditor | Largest debtor | Complete reversal |

| Fiscal Deficit | ~1.5% GDP | ~6% GDP | 4x increase |

| Real Interest Rates | Positive | Variable/Negative | Structural shift |

The current environment combines unprecedented debt levels with demonstrated willingness to weaponise monetary infrastructure, creating rational incentives for reserve diversification regardless of geopolitical alignment. This represents creditor behaviour responding to demonstrable unsustainability rather than political opposition.

What Role Do Fiscal Dynamics Play in This Transformation?

US Debt Trajectory and Creditor Confidence

The mathematical reality of American fiscal dynamics presents challenges fundamentally different from previous monetary crisis periods. Current structural deficits averaging 6% of GDP over the past three years represent roughly four times the budget shortfall experienced in 1979, whilst occurring against a backdrop of significantly higher baseline debt levels.

Unlike the late 1970s period when the United States could implement aggressive monetary tightening from a position of international creditor strength, current conditions require debt service on $38 trillion in outstanding obligations. Interest payments now consume an increasing percentage of federal revenues, creating constraints on monetary policy flexibility.

Debt Service and Monetary Policy Constraints:

• Total government debt: $38 trillion (November 2025)

• Monthly deficit: $173.28 billion (November 2025, despite increased tariff revenue)

• Interest service costs: Growing percentage of federal budget

• Federal Reserve policy constraints: Limited ability for aggressive rate increases

The absence of a Paul Volcker-style monetary policy option reflects these structural constraints. The current Federal Reserve leadership demonstrates inclination toward monetary accommodation rather than aggressive tightening, eliminating the historical precedent most often cited for potential gold market correction.

Structural Spending Pressures

Current fiscal dynamics incorporate spending pressures absent during previous monetary crisis periods. Demographic transitions driving healthcare and social security obligations create baseline spending growth independent of discretionary policy choices. Infrastructure modernisation requirements, defence spending escalation, and climate transition investments represent additional structural commitments.

These obligations occur within a framework where traditional fiscal adjustment mechanisms face political and economic constraints. Tax increase limitations, entitlement reform resistance, and economic growth dependencies create scenarios where monetary accommodation becomes the path of least resistance for fiscal financing.

Structural Spending Categories:

• Demographic-driven entitlement expansion

• Infrastructure modernisation requirements

• Defence spending escalation amid global tensions

• Climate transition and energy security investments

• Interest service on existing debt obligations

How Are Portfolio Allocation Models Evolving?

The 60/20/20 Revolution

Traditional portfolio construction frameworks based on 60% equity and 40% bond allocations are experiencing systematic replacement by models incorporating substantial precious metals exposure. The emerging 60/20/20 framework allocates 60% to equities, 20% to bonds, and 20% to gold, representing recognition that bonds no longer provide adequate inflation protection or portfolio diversification benefits.

This allocation shift reflects institutional recognition that gold has evolved from a rate-sensitive trade to a fiscal-risk hedge. Furthermore, understanding effective gold investment strategies becomes crucial as institutions adjust their allocation models. Morgan Stanley's Chief Investment Officer recently advocated for the 60/20/20 allocation strategy, describing gold as the anti-fragile asset to own, rather than Treasuries in current market conditions.

Goldman Sachs analysis suggests that optimal portfolio construction over the past decade would have allocated 50% of assets to gold, indicating current institutional allocations remain significantly below mathematically optimal levels based on historical performance data.

Portfolio Evolution Timeline:

• Traditional model: 60% stocks, 40% bonds

• Emerging model: 60% stocks, 20% bonds, 20% gold

• Goldman Sachs optimal: 50% gold allocation over past decade

• Current average allocation: Less than 1% gold in most portfolios

Mathematical Implications of Reallocation

The mathematical implications of widespread adoption of 20% gold allocations would create unprecedented demand pressures on available physical supply. With current institutional allocations averaging below 1% of portfolio values, achieving 20% targets would require massive increases in gold holdings across multiple asset classes.

Demand Projection Analysis:

| Portfolio Segment | Assets Under Management | Required Gold Increase | Additional Demand |

|---|---|---|---|

| Global Pension Funds | $50 trillion | 19.7% increase | ~15,000 tonnes |

| Insurance Companies | $30 trillion | 19.9% increase | ~8,000 tonnes |

| Sovereign Wealth Funds | $10 trillion | 18% increase | ~5,000 tonnes |

| Endowments/Foundations | $2 trillion | 19.8% increase | ~1,000 tonnes |

Annual gold mine production of approximately 3,300 tonnes would be insufficient to satisfy reallocation demand if institutional adoption occurred simultaneously. This supply-demand imbalance would require either extended transition periods or significant price adjustments to balance market clearing mechanisms.

The absence of speculative positioning in current gold markets suggests reallocation demand would represent genuine portfolio optimisation rather than momentum-driven speculation, potentially creating more sustained price support than traditional bull market cycles. Additionally, these trends support the broader gold price forecast for sustained upward momentum.

What Technical Market Dynamics Support This Shift?

Correlation Structure Breakdown

Traditional relationships between gold prices and real interest rates have experienced fundamental structural breaks since late 2022. Historical inverse correlations, where gold prices declined with rising real yields, have transformed into positive correlations when higher rates reflect sovereign credit stress rather than economic growth strength.

Correlation Analysis Evolution:

• Pre-2022: Gold/10-Year Real Yields correlation = -0.65

• Post-2022: Gold/10-Year Real Yields correlation = +0.23

• Statistical significance: 99% confidence interval for structural break

• Market interpretation: Rates reflecting fiscal stress rather than growth

This correlation inversion indicates market recognition that gold now functions as a fiscal-risk hedge rather than purely an inflation or monetary debasement play. When interest rate increases reflect concerns about sovereign creditworthiness rather than economic overheating, gold provides portfolio protection rather than experiencing pressure.

Portfolio managers have begun re-engineering portfolios for an era of structural deficits and active fiscal policy, according to WisdomTree analysis. This represents fundamental changes in how institutional investors model gold's relationship to macroeconomic variables.

Supply-Demand Fundamentals

Physical gold supply dynamics present structural constraints independent of demand variables. Annual mine production growth has decelerated to 1-2% annually whilst experiencing increasing production costs, declining ore grades, and extended development timelines for new projects.

Supply-Side Constraint Analysis:

• Annual global production: ~3,300 tonnes

• Production growth rate: 1-2% annually (declining)

• Average development timeline: 8-12 years for new mines

• Ore grade deterioration: 15-20% decline over past decade

• ESG compliance costs: Increasing 15-20% annually

Geopolitical risks affect approximately 30% of global production through mines located in politically unstable regions or nations subject to sanctions regimes. This geographic concentration creates supply vulnerability to geopolitical developments independent of market demand dynamics.

Demand Component Analysis:

| Demand Category | Annual Volume (tonnes) | Growth Rate | Price Sensitivity |

|---|---|---|---|

| Central Bank Purchases | 1,000+ | Accelerating | Low |

| Jewellery Demand | 2,000+ | Stable | Moderate |

| Technology Applications | 300+ | Growing | Low |

| Investment Demand | 1,000+ | Variable | High |

| ETF Holdings | Variable | Institutional shift | Moderate |

Central bank demand exhibits low price sensitivity, as sovereign reserve allocation decisions prioritise strategic considerations over cost optimisation. Technology demand continues growing due to gold's unique properties in electronics and renewable energy applications, creating baseline demand floors.

The next major ASX story will hit our subscribers first

How Do Current Conditions Differ From Historical Bubbles?

Absence of Speculative Characteristics

Current gold market dynamics lack traditional speculative bubble indicators that characterised previous precious metals manias. Retail investor participation remains minimal, media coverage stays subdued, and leverage usage shows conservative rather than aggressive positioning patterns.

Bubble vs. Paradigm Shift Comparison:

| Characteristic | Typical Asset Bubble | Current Gold Market |

|---|---|---|

| Retail Participation | Extreme euphoria, FOMO behaviour | Minimal retail involvement |

| Media Coverage | Saturation, mainstream headlines | Limited, specialised coverage |

| Leverage Usage | Widespread margin trading | Conservative institutional positioning |

| Price Volatility | Extreme daily swings | Relatively stable trend advance |

| ETF Flows | Massive speculative inflows | Modest institutional accumulation |

| Correlation Breakdown | Momentum-driven | Fundamental driver evolution |

Exchange-traded fund gold holdings remain approximately 10% below 2020 pandemic peak levels despite gold reaching multiple record highs throughout 2024 and 2025. This indicates institutional rather than speculative demand driving current price appreciation.

The absence of irrational exuberance noted by market analysts reflects investor attention focused on cryptocurrencies and artificial intelligence sectors rather than precious metals. Speculative capital allocation has generally avoided gold in favour of higher-volatility technology-related investments.

Fundamental Value Anchoring

Unlike speculative bubbles driven by momentum and sentiment, current gold valuations appear anchored to measurable fundamental drivers. Central bank demand provides quantifiable price floor support through sustained institutional purchasing programs independent of market sentiment.

Fundamental Support Mechanisms:

• Central bank demand: 1,000+ tonnes annually with low price sensitivity

• Fiscal deterioration: Ongoing debasement pressure from structural deficits

• Geopolitical risk premiums: Sustained uncertainty supporting valuations

• Supply constraints: Limited production growth constraining downside

• Portfolio reallocation: Institutional demand independent of speculation

Gabelli Gold Fund analysis notes that despite historical knowledge of 1970s gold market volatility, current market behaviour feels different with quick recovery occurring after each correction rather than extended downward pressure characteristic of bubble deflation.

The resilience demonstrated during October 2025's 9.8% correction and subsequent recovery to record-high gold prices within two months indicates underlying fundamental support rather than speculative momentum. This recovery pattern contrasts with typical bubble behaviour where corrections accelerate into major reversals.

What Are the Long-Term Implications for Monetary Systems?

Multipolar Reserve Architecture

The emerging global monetary framework suggests evolution toward multipolar reserve systems where no single currency maintains dominant settlement status. Gold's neutral, unencumbered characteristics position it as natural bridge asset between competing monetary blocs and regional clearing systems.

BRICS+ nations have accelerated development of payment systems incorporating gold settlement mechanisms, creating infrastructure for trade settlement outside traditional dollar-based clearing systems. These developments represent formalisation of gold's monetary role rather than symbolic gestures. Moreover, experts suggest this represents a financial market paradigm shift affecting global monetary architecture.

Regional Monetary Development Initiatives:

• BRICS+ payment systems: Gold-backed settlement mechanisms

• European strategic autonomy: Reduced USD dependency frameworks

• Asian regional clearing: Precious metals-backed transactions

• Middle Eastern innovations: Oil-gold linkage experiments

• African monetary unions: Gold-denominated regional currencies

These parallel system developments create optionality for nations seeking alternatives to existing monetary infrastructure whilst maintaining international trade capabilities. Gold provides the neutral reserve asset enabling these alternative systems to function independently.

Technology Integration Opportunities

Blockchain-based gold tokenisation and molecular tracking systems are creating new infrastructure enabling gold-backed digital currencies and ESG-compliant supply chain verification. These technological developments expand gold's monetary utility beyond traditional physical holdings whilst maintaining the underlying asset's fundamental properties.

Smart contract integration allows for programmable gold-backed settlement systems, enabling automatic execution of international trade agreements with precious metals backing. This technology infrastructure supports the multipolar monetary architecture development whilst preserving gold's essential monetary characteristics.

Technological Innovation Applications:

• Blockchain tokenisation: Digital gold with physical backing

• Molecular tracking: ESG compliance and provenance verification

• Smart contracts: Programmable gold-backed settlements

• Central Bank Digital Currencies: Gold-backed CBDC frameworks

• Trade finance: Precious metals-backed international commerce

The convergence of traditional monetary properties with modern technological capabilities positions gold for expanded utility in evolving international monetary systems. These innovations address previous limitations regarding transportability and divisibility whilst maintaining store-of-value characteristics.

Structural vs. Cyclical Analysis Framework

The comprehensive evidence suggests 2025's gold market performance represents structural paradigm shift in gold market dynamics rather than cyclical speculation destined for correction. The convergence of fiscal unsustainability, monetary weaponisation, institutional portfolio reallocation, and supply-demand fundamentals creates sustained demand dynamics transcending traditional precious metals cycles.

This transformation reflects broader recalibration of global monetary architecture where gold's historical role as ultimate money reasserts itself amid declining confidence in fiat currency systems and associated counterparty risks. The institutional nature of current demand, combined with fundamental supply constraints and geopolitical uncertainty, suggests durability beyond typical speculative cycles.

Paradigm Shift Evidence Summary:

• Central bank accumulation: Sustained 3-year institutional buying campaign

• Correlation breakdown: Fundamental changes in rate-gold relationships

• Portfolio reallocation: Structural shifts in institutional allocation models

• Geopolitical recognition: Asset weaponisation driving reserve diversification

• Supply constraints: Limited production growth amid increasing demand

• Technology integration: Enhanced monetary utility through innovation

The mathematical implications of widespread institutional adoption of higher gold allocations, combined with constrained physical supply and ongoing fiscal deterioration, suggest the current paradigm shift in gold market dynamics represents sustainable structural change rather than temporary speculative excitement.

Brien Lundin's analysis indicates that gold has already returned to official recognition as money, specifically as the only money that cannot be debased. This recognition by institutional investors, sovereign entities, and monetary authorities signals completion of the paradigm shift in gold market rather than its beginning, suggesting current valuations reflect new structural equilibrium rather than speculative excess.

Ready to Profit from Gold's Historic Market Transformation?

Discovery Alert's proprietary Discovery IQ model identifies significant gold and precious metals discoveries across the ASX, ensuring you never miss the next breakthrough announcement. With central banks accumulating over 1,000 tonnes annually and institutional investors adopting 20% gold allocations, positioning yourself ahead of major mineral discoveries has never been more crucial for capitalising on this unprecedented market paradigm shift.