June 22, 2026

The Hidden Transmission Belt: How Energy Markets Quietly Drive Gold Prices

Most commodity investors think of gold and oil as separate asset classes responding to separate forces. One is a monetary metal. The other is an industrial fuel. Yet the relationship between them is deeper and more mechanically precise than most market participants appreciate. When energy prices shift, they alter the inflation calculus, which in turn reshapes monetary policy expectations, ultimately changing the opportunity cost of holding a non-yielding asset like gold. Lower oil prices support gold and Fed rate expectations through this precise transmission mechanism, which operates whether or not there is a war, a banking crisis, or a flight to safety.

Understanding this chain is not just academically interesting. In mid-2026, it is the central framework for interpreting why spot gold climbed 1.2% to approximately $4,210 per ounce whilst simultaneously facing meaningful headwinds from the Federal Reserve. The two forces are pulling in opposite directions, and the outcome of that tension will determine whether gold reaches Morgan Stanley's $5,200/oz target or consolidates below $4,300/oz through the remainder of the year.

When big ASX news breaks, our subscribers know first

Two Pathways: How Lower Oil Prices Support Gold Through Distinct Channels

The relationship between crude oil and gold is not a single mechanism but two overlapping ones, each with its own timing and sensitivity.

The Inflation Compression Channel operates over weeks to months. When Brent crude falls, the energy component of consumer price indices follows relatively quickly. Headline CPI softens. Inflation expectations measured in market instruments like Treasury Inflation-Protected Securities begin to decline. Central banks, whose primary mandate concerns price stability, then face reduced pressure to maintain aggressive tightening postures.

The Rate Expectation Channel operates more rapidly, often within days of a significant energy price move. When traders reprice inflation downward, they also reprice the likely path of central bank policy. Futures markets shift. Rate-hike probabilities change. Furthermore, because gold competes directly against interest-bearing assets for investor capital, any reduction in expected yields makes gold comparatively more attractive almost immediately.

Understanding gold and bond dynamics helps clarify why both channels matter simultaneously. Both are currently active, but they are being partially neutralised by an unusually hawkish Fed posture, creating a complex environment where lower oil prices support gold in theory whilst rate expectations limit its upside in practice.

What Triggered the June 2026 Gold Rebound: Commodity Rotation, Not Safe-Haven Fear

The 1.2% spot gold rebound to $4,210/oz in mid-June 2026 was frequently characterised in financial media as a gold rally. A more precise description, however, is a commodity reallocation event.

The proximate cause was a diplomatic development: US and Iranian officials formalised a 60-day roadmap toward a broader peace agreement, extending the ceasefire framework that had been in place since April. The immediate market consequence was a reduction in the perceived probability of Middle East supply disruption. Consequently, the oil price impact was swift, driving Brent crude down approximately 2% to $79.10 per barrel.

Capital that had been positioned in energy markets as a geopolitical hedge needed a new home. Gold, which carries some thematic overlap with oil in portfolio construction as a real asset and inflation proxy, absorbed a portion of that rotation. Critically, this happened without the typical signatures of a genuine safe-haven episode:

- Equity markets did not weaken materially.

- Credit spreads did not widen.

- Volatility indices did not spike.

- The VIX remained subdued.

This distinction carries important implications for investors sizing positions. A capital rotation move is inherently more fragile than a structural safe-haven demand shift. If geopolitical risk re-emerges, or if oil prices recover, the rotation can reverse just as quickly as it formed.

The spot-futures divergence reinforces this caution. August gold futures fell between 0.4% and 0.7% to approximately $4,220/oz even as spot prices rose. Institutional investors, who typically express multi-week conviction through futures positioning rather than spot purchases, were not aggressively adding length. This futures discount relative to spot is a meaningful signal that the professional investor community viewed the move with scepticism.

The Fed's Hawkish Stance and Its Direct Impact on Gold's Ceiling

If lower oil prices support gold through the inflation and rate expectation channels, the Federal Reserve's current posture works in the opposite direction. Fed Chair Kevin Warsh has consistently communicated a preference for keeping monetary policy restrictive, and markets have responded by repricing the probability of further tightening sharply higher.

| Indicator | Previous Level | Current Level | Direction |

|---|---|---|---|

| December Fed Rate-Hike Odds | 61% | 89% | Hawkish repricing |

| Brent Crude | ~$81/barrel | $79.10/barrel | Softening |

| Spot Gold | ~$4,160/oz | ~$4,210/oz | Mild recovery |

| US Dollar Index | ~100.80 | 100.93 | Strengthening |

| Net Long Dollar Positions | Elevated | ~$30 billion | 16-month high |

The jump in December rate-hike odds from 61% to 89% is not a marginal shift. It represents a fundamental change in market consensus about where US interest rates are heading. For gold, which generates no yield, this matters enormously. Every basis point of expected rate increase widens the opportunity cost gap between holding gold and holding interest-bearing Treasuries or money market instruments.

The dollar dimension compounds this pressure. The US Dollar Index near 100.93, supported by approximately $30 billion in net long dollar positioning — the largest such figure in 16 months — creates a structural headwind for gold from two directions simultaneously. First, a stronger dollar makes gold more expensive in foreign currency terms, directly suppressing demand from non-USD buyers. Second, dollar strength signals that global capital continues to find the US interest rate environment attractive, which is itself a reflection of sustained Fed hawkishness.

According to current gold price data, analyst commentary in this cycle has consistently emphasised that gold is unlikely to sustain meaningful upward momentum whilst the Fed maintains its current stance. The disinflationary benefit flowing from lower energy prices has not yet translated into any observable softening of Fed guidance.

Scenario Analysis: Two Divergent Paths for Gold Through H2 2026

The most useful framework for investors is not a single price target but a scenario map that identifies which variables need to move, and in which direction, to produce each outcome.

| Scenario | Required Conditions | Likely Gold Range |

|---|---|---|

| Hawkish Continuation | December hike odds hold at 85-89%, ETF inflows absent, dollar stays above 100 | $4,000 to $4,300/oz; central-bank demand limits downside |

| Partial Dovish Shift | Oil holds below $80, inflation data softens, hike odds fall to ~70-75% | $4,300 to $4,700/oz; tactical positioning rebuilds |

| Full Dovish Pivot | Hike odds fall toward 61%, ETFs resume inflows, dollar index breaks below 99 | Potential move toward $5,200/oz (Morgan Stanley target) |

The Three-Pillar Requirement for $5,200/oz Gold

Morgan Stanley's second-half 2026 target of $5,200 per ounce is achievable within the current macro framework, but it requires a specific and sequential set of developments:

- Sustained energy price softness. Brent crude remaining at or below $79/barrel over multiple weeks, not just a single-session dip, is necessary to progressively compress inflation expectations in a way that influences Fed thinking.

- Fed communication shift. December rate-hike odds declining from 89% back toward 61% would represent the most powerful near-term bullish catalyst available to gold. This shift would need to be reflected in official Fed communications, not just in market pricing.

- ETF inflow resumption. The demand-side catalyst that bridges the gap between $4,500/oz and $5,200/oz is institutional money flowing back into gold-backed exchange-traded funds. Without this, price appreciation lacks the volume and sustained buying pressure required for a structural breakout.

In addition, the broader gold price forecast underlines just how much geopolitical and macroeconomic variables remain pivotal drivers of any sustained bull run.

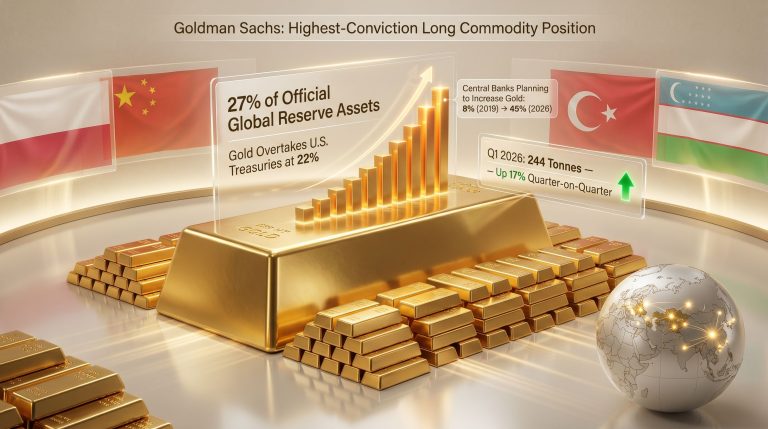

Central-Bank Demand: The Structural Floor That Changes the Downside Calculation

One aspect of the current gold market that is frequently underweighted in short-term analysis is the role of sovereign buyers. Central-bank gold demand has been running at historically elevated levels since 2022, driven by a multi-year trend of reserve diversification away from US dollar assets.

This demand is categorically different from ETF flows or speculative futures positioning. Central banks operate on multi-year institutional mandates. Their purchasing decisions are insensitive to monthly CPI prints, Fed press conferences, or short-term dollar fluctuations. They buy gold because they are building long-term reserve buffers, and that objective does not change materially based on whether December rate-hike odds are 61% or 89%.

The practical consequence is that central-bank demand creates a price floor that is both real and relatively durable. Analyst views across the spectrum suggest this buying base could support medium-to-long-term price stability even in a sustained hawkish monetary environment. The $4,000/oz level is widely cited as a threshold where sovereign accumulation would likely accelerate, providing a demand cushion that limits the downside of any Fed-driven correction.

Furthermore, positioning gold as an inflation hedge remains a core rationale for many sovereign buyers. Indeed, gold as an inflation hedge continues to anchor the long-term strategic case for reserve diversification, independent of near-term rate dynamics.

For investors, this creates an important distinction between two types of gold exposure: tactical positions that depend on a near-term Fed pivot, and structural positions anchored to the ongoing sovereign accumulation trend. The risk profiles of these two rationales are materially different and should be sized accordingly.

The next major ASX story will hit our subscribers first

The Investor Monitoring Framework: Which Variables Actually Matter

Given the competing forces currently acting on gold, position management requires tracking the right indicators in the right sequence. Not all variables carry equal weight.

Primary Indicators

- December Fed rate-hike odds. The single most important near-term variable. A decline from 89% toward 61% would be the clearest available signal of a dovish shift. This should be monitored weekly using Fed Funds futures markets.

- Brent crude price. Sustained trading below $80/barrel reinforces the disinflationary narrative. A recovery above $85/barrel would reignite inflation concerns and support continued Fed hawkishness, directly capping gold's upside.

- US Dollar Index. The 101 threshold is critical. A sustained break below 99 would signal that the extreme long-dollar positioning is unwinding, removing one of gold's two primary headwinds simultaneously.

- Gold ETF flow data. Weekly inflow and outflow figures from major gold-backed ETFs provide the most reliable real-time signal of whether institutional sentiment is genuinely shifting toward gold.

- US CPI releases. Monthly inflation prints will either validate or challenge the disinflationary thesis built on lower energy prices. A softer-than-expected CPI reading, particularly in the energy-influenced headline figure, would accelerate the rate expectation repricing that gold needs.

Secondary Indicators

- 10-year TIPS real yields. Lower real yields directly reduce the opportunity cost of holding non-yielding gold. A move lower here often precedes formal shifts in rate-hike probability.

- Fed meeting language. Any evolution from the current higher-for-longer framing toward data-dependent flexibility in official communications would represent a leading indicator of rate expectation repricing.

Analysts at JP Morgan's commodities research have outlined similar monitoring frameworks, reinforcing the view that macro variables rather than technical chart levels are currently the primary drivers of gold's directional bias.

Frequently Asked Questions

Does a falling oil price always translate into higher gold prices?

Not automatically and not immediately. Lower oil prices create the conditions for gold to benefit by softening inflation expectations and reducing the urgency for sustained monetary tightening. However, if dollar strength persists and Fed officials continue signalling hawkish intent, the disinflationary benefit from cheaper energy can be fully offset. The net effect on gold depends entirely on which force dominates market pricing at any given time.

Why does the 89% December rate-hike probability matter so much for gold?

Gold generates no income. Its attractiveness relative to other assets is therefore highly sensitive to the prevailing and expected level of interest rates. When the market prices an 89% probability of another rate hike, it is signalling consensus belief that interest-bearing assets will remain competitively rewarding. This raises the implicit cost of allocating capital to gold, which is why this figure functions as a ceiling on near-term price enthusiasm.

What makes central-bank buying different from speculative ETF demand?

Central-bank purchases are executed under multi-year reserve diversification mandates that are largely insensitive to short-term market conditions. ETF demand, by contrast, reacts dynamically to real yield movements, dollar strength, and investor sentiment shifts. Central-bank buying provides durable structural support. ETF flows provide the momentum required to push prices into new territory. Both are necessary for a sustained bull run; however, only one of them is currently present in meaningful volume.

What combination of events could push gold below $4,000/oz?

A convergence of persistently elevated rate-hike expectations, a US Dollar Index sustained above 102, continued absence of ETF inflows, and an oil price recovery above $85/barrel could create sufficient headwind to test the $4,000/oz level. Most analysts view central-bank demand as the buffer most likely to prevent a sustained break below this threshold, but the scenario is not impossible if multiple headwinds align simultaneously.

This article is intended for informational purposes only and does not constitute financial advice. All price targets, scenario projections, and market forecasts involve significant uncertainty and should not be relied upon as the basis for investment decisions. Past performance of any asset class does not guarantee future results.

Want to Position Yourself Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across more than 30 commodities into clear, actionable insights for both traders and long-term investors — explore Discovery Alert's discoveries page to see the historic returns major discoveries have generated, and begin your 14-day free trial today to secure a genuine market-leading edge.