June 5, 2026

The Structural Forces Reshaping Gold's Role as a Reserve Asset

Few financial instruments carry as much historical, psychological, and monetary weight as gold. Yet even among seasoned investors, the mechanics of what actually supports a gold price floor and central bank buying at any given level remain surprisingly misunderstood. Price floors in commodity markets are not legislated or guaranteed. They emerge from the intersection of institutional behaviour, sovereign strategy, and the shifting psychology of market participants. Understanding why that floor exists, how firm it actually is, and who is responsible for holding it up has never been more important than it is right now.

When big ASX news breaks, our subscribers know first

Why the Gold Price Floor Debate Has Reached an Inflection Point

Gold's Volatility Reveals a Structural Problem

The gold market demonstrated something deeply unusual in the opening months of 2025. Within a roughly three-month window, prices moved from approximately $4,300 per troy ounce at the start of January, surged to a peak near $5,600, and then retreated sharply toward the $4,400 level by March. A price range of more than $1,200 within a single quarter is extraordinary for an asset that traditionally behaves as a low-beta store of value.

This kind of movement does not happen in a market that is primarily driven by patient, long-term institutional capital. It reflects a market where short-term, leveraged participants are disproportionately setting the marginal price. The scale of these swings forces a critical reassessment of the gold price floor concept. Where exactly is the floor? Who is defending it? And what happens if those defenders step back?

What Is a Gold Price Floor?

A gold price floor refers to the price level at which sustained institutional or sovereign demand is expected to absorb selling pressure and prevent further downside. Critically, it is not a fixed number. It shifts as the composition of buyers, macroeconomic conditions, and reserve allocation strategies evolve over time.

The concept matters because gold, unlike equities or bonds, does not generate cash flows. Its price is entirely a function of what participants believe it is worth relative to alternatives. When the largest and most consistent buyers change their behaviour, the floor moves with them. Furthermore, understanding gold in the monetary system helps contextualise why these shifts carry such significant weight for long-term investors.

What Is Actually Driving Gold's Long-Term Structural Demand?

The Five Macro Pillars Behind the Multi-Year Rally

Gold's ascent to record highs did not emerge from speculation alone. The structural architecture supporting this bull market includes a set of well-documented macro forces that most serious market observers acknowledge as credible drivers.

| Structural Driver | Core Mechanism | Current Status |

|---|---|---|

| Central bank reserve diversification | Reduces sovereign dependency on the US dollar | Active but showing signs of deceleration |

| Ballooning sovereign debt and fiscal deficits | Erodes long-term confidence in fiat currency systems | Accelerating in most developed economies |

| Negative real interest rates | Reduces the opportunity cost of holding non-yielding gold | Cyclically persistent through rate cycles |

| Geopolitical fragmentation and sanctions regimes | Elevates demand for politically neutral reserve assets | Intensifying across multiple regions |

| Retail and speculative momentum flows | Amplifies short-term price moves through leveraged positioning | Currently the dominant marginal price setter |

Why the Blurring of Gold's Identity Creates Risk

Gold has historically been classified as a safe haven asset, one that behaves counter-cyclically to risk assets like equities. That classification underpins its role in portfolio construction, sovereign reserve management, and crisis hedging. The gold safe-haven appeal has long been a cornerstone of institutional portfolio logic, however recent price behaviour has seen gold trade with risk sentiment on certain time horizons, moving in sympathy with momentum-driven markets rather than against them.

This blurring is not a permanent structural shift, but it does reflect the changed composition of market participants. When retail investors using margin accounts become the dominant price setters, gold begins to trade like a high-momentum speculative vehicle rather than a monetary anchor. That is a temporary but consequential dynamic.

How Much Gold Are Central Banks Actually Buying?

2025 Central Bank Purchasing in Context

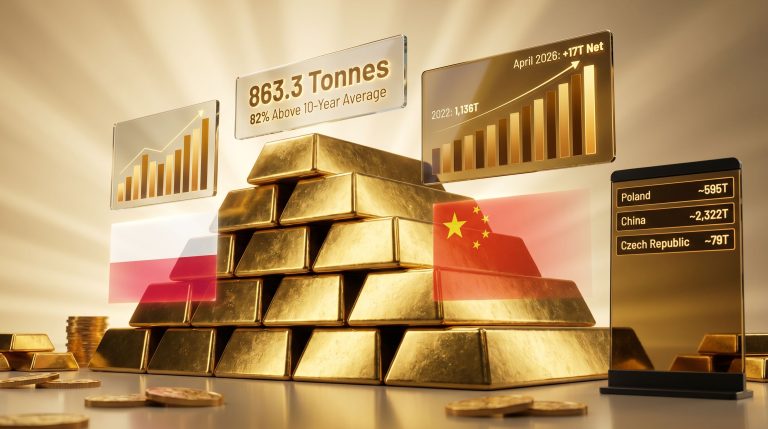

According to World Gold Council data, central banks collectively acquired approximately 863 tonnes of gold across 2025, with the fourth quarter alone accounting for around 230 tonnes. These figures confirm that sovereign demand has remained structurally elevated even at historically high price levels.

However, the trend within the trend is what deserves closer scrutiny. The headline numbers remain positive, but the rate of accumulation has been decelerating meaningfully from the peaks observed in 2022 and 2023. In addition, central bank gold demand continues to be one of the most closely watched variables for analysts assessing the durability of the current bull market.

Country-by-Country Central Bank Activity

| Central Bank | 2025 Activity | Reported Holdings | Key Notes |

|---|---|---|---|

| Poland | Largest single buyer in 2025 | Not fully disclosed | Part of a consistent multi-year accumulation strategy |

| Turkey | Steady net buyer with periodic selling | Approximately 644 tonnes including Treasury | Sells periodically to defend the lira, then re-accumulates |

| China (PBoC) | Sharply slowing pace | Approximately 2,306 tonnes (~9% of reserves) | Added only 3 tonnes in Q4, smallest quarterly addition since early 2024 |

| India | Active buyer | Not fully disclosed | Part of broader emerging market diversification wave |

| Russia | Strategic buyer and user | Not publicly disclosed | Uses gold to settle energy transactions outside Western financial systems |

Why China's Slowdown Deserves Attention

China's People's Bank added only 3 tonnes of gold in the fourth quarter of 2025, a figure that stands in stark contrast to its earlier buying pace. This deceleration raises a legitimate question: at what price point does sovereign acquisition appetite begin to moderate?

At spot prices above $4,500 per troy ounce, the cost of meaningful reserve diversification into gold becomes significantly higher in local currency terms. For central banks managing large and growing reserves, this creates a practical constraint on how aggressively they can accumulate. China's slowdown may not represent a loss of strategic conviction, but it does suggest that price sensitivity exists even at the sovereign level.

Is Central Bank Buying Actually Responsible for the Price Rally?

What Official Sector Demand Actually Does to Markets

Central bank buying influences gold markets through several distinct mechanisms, and understanding each one separately matters for assessing the floor's durability:

- Physical float reduction: When a central bank acquires gold and holds it in reserve, that metal is effectively removed from the tradeable supply. This creates a structural tightening of available inventory over time.

- Sentiment signalling: Official sector confidence in gold as a reserve asset functions as a psychological anchor for institutional investors. Central bank buying legitimises the asset class for participants who might otherwise avoid it.

- Reflexive downside support: Sovereign buyers have historically increased their purchasing activity during price dips, creating a self-reinforcing support mechanism that sets a de facto floor in declining markets.

What Central Bank Buying Cannot Do

There are important limitations to the floor that central bank demand provides:

- It cannot prevent short-term price volatility driven by leveraged retail positioning or macro shock events.

- It cannot guarantee a rising price trajectory when institutional headwinds intensify.

- It is not a substitute for broad-based institutional participation from insurers, pension funds, and endowments, which represent the largest pools of professionally managed capital.

Are Central Banks Showing Signs of Buying Fatigue?

Fourteen Consecutive Quarters Without a Record Purchase

The last record quarter for central bank gold purchases occurred more than 14 quarters ago. Since then, buying has remained net positive in most quarters but has trended persistently below the peaks observed during 2022 and 2023.

This sustained deceleration is not catastrophic in isolation. However, when combined with the emergence of net selling in early 2025 — which represented the first episode of net central bank selling in three years — it challenges the assumption that sovereign demand will automatically backstop prices at elevated levels. According to Brookings Institution analysis, the strategic importance of central bank gold holdings is well established, yet the pace of accumulation remains a critical variable.

Gold Performing Its Designated Function

A critical reframe is necessary here. When Turkey sells gold reserves to defend the lira, or when Russia uses gold to facilitate energy trade outside Western financial infrastructure, those transactions are not evidence of a loss of confidence in gold. They are evidence of gold working exactly as intended.

Gold's role as a politically neutral, liquid, globally accepted reserve asset means that usage is a feature, not a defect. The important metric is not whether individual nations periodically sell, but whether net demand across the global central bank community remains positive. In 2025, it did. But the margin has narrowed, and the automatic bid that characterised 2022 and 2023 buying cycles is no longer guaranteed.

The next major ASX story will hit our subscribers first

Who Is Setting the Marginal Gold Price Right Now?

The Retail Investor Problem

In a traditional commodity bull market, large institutional buyers establish positions early, providing both a price floor and a stabilising force on upside momentum. The current gold market has inverted this structure. Retail investors, many trading on margin, have become the dominant marginal price setters. This dynamic produces exaggerated upside moves and an uncomfortably ambiguous downside.

This structural inversion explains the $1,000-plus price swings that have become a feature of recent gold trading. Leveraged retail positions amplify directional moves in both directions, and unlike institutional buyers who operate within mandated allocation frameworks, retail participants can exit rapidly when sentiment shifts.

The Institutional Buyers Who Have Not Yet Arrived

The most consequential development for gold's next major price leg is not what central banks do next. It is whether large institutional capital finally rotates into precious metals at scale. Several signals suggest this transition is approaching, but has not yet occurred:

- In September 2024, Morgan Stanley publicly suggested that the conventional 60/40 portfolio was no longer appropriate for long-term retirement planning, proposing a 60/20/20 model where a 20% allocation would be directed toward alternative assets including gold.

- A pilot programme has been established allowing a select group of insurance companies to hold up to 1% of their assets in gold, representing an early but meaningful regulatory shift.

- Executive Order 14330, signed in August 2024, directed federal agencies to reduce restrictions on including alternative assets, including precious metals, in 401(k) retirement plans.

- BlackRock and other major asset managers have begun signalling potential interest in precious metals exposure within target-date fund and lifecycle product structures.

Furthermore, record gold ETF inflows observed throughout much of 2025 suggest that broader investor appetite is forming, even if large institutional mandates have not yet formally shifted.

The critical gap: policy frameworks and institutional interest are forming, but capital has not yet moved at scale. This gap between signalling and actual deployment is the single largest source of structural uncertainty in the current gold market.

What Scenarios Could Define Gold's Next Price Range?

Three Possible Paths Forward

Scenario 1: Slow Grind Higher (Base Case)

Gold consolidates between $4,500 and $6,000 per troy ounce as institutional adoption materialises gradually. Central bank buying stabilises at a lower but still positive level. Gold begins reverting toward its historically low-beta character, moving incrementally rather than in dramatic surges.

Scenario 2: Crisis-Driven Rotation (Bull Case)

A major dislocation in private equity valuations, commercial real estate repricing, or a significant dysfunction in equity or bond markets triggers forced reallocation out of traditional 60/40 portfolio structures. Institutional capital rotates into alternative assets at scale, potentially driving gold toward $8,000 per troy ounce or higher.

Scenario 3: Stalled Bull Market (Bear Case)

Institutional buyers fail to materialise in meaningful size. Central bank demand continues to decelerate. The market remains structurally dependent on leveraged retail participation, historically the least stable source of sustained demand. Gold consolidates in a $3,000 to $4,000 range for an extended period.

Scenario probability note: The bear case is significantly underacknowledged in mainstream gold market commentary. It represents a legitimate structural risk if institutional adoption timelines extend well beyond what current signals suggest. No scenario should be dismissed.

How the Iran Conflict Affects Gold's Price Floor

A Correlation That Tightened Under Pressure

The relationship between gold prices and oil markets is not always consistent. However, during periods of active Middle East conflict, the correlation has historically tightened in ways that create short-term headwinds for gold.

| Market Condition | Gold-Oil Relationship | Underlying Mechanism |

|---|---|---|

| Stable geopolitical environment | Loose and inconsistent | Independent macro drivers dominate separately |

| Active Middle East conflict | Tight and inverse | Oil spike raises inflation expectations, reducing rate cut probability, pressuring gold |

| Prolonged conflict with supply disruption | Strongly inverse | Sustained inflation narrative suppresses gold rally momentum |

The logic is straightforward: when oil prices spike due to Middle East tensions, markets interpret this as a prolonged inflationary impulse. Higher expected inflation reduces the probability of near-term rate cuts. With rate cut expectations dwindling, the opportunity cost argument for holding gold weakens, and prices respond negatively despite the apparent geopolitical safe-haven case.

Conversely, meaningful peace progress in the region could remove this headwind and create conditions for renewed gold rally momentum. Understanding the interplay between gold and bond dynamics is equally important when assessing how rate expectations and inflation pressures shape gold's directional bias across different market cycles.

Key Indicators to Watch for the Gold Price Floor

Three Data Points That Will Define Gold's Next Move

1. World Gold Council Q2 2025 Central Bank Data

Net purchases in Q1 2025 were reported at approximately 244 tonnes, but selling activity within that figure was rising. A continued deceleration or a second consecutive quarter of net selling would materially weaken the floor narrative and force a reassessment of sovereign demand assumptions.

2. Institutional Commitment Signals from Major Asset Managers

The most impactful development for gold's structural outlook would be a formal announcement by BlackRock, Morgan Stanley, Vanguard, or a comparable institution that gold allocations are being incorporated into target-date funds or large retirement product ranges. This would represent a genuine demand inflection point rather than a policy signal.

3. Iran Conflict Trajectory and Oil Price Stability

Escalation that drives oil prices higher will likely suppress gold's near-term upside through the inflation-rate cut mechanism described above. De-escalation or ceasefire progress would remove a meaningful overhang and potentially catalyse renewed institutional interest in the safe-haven allocation thesis.

Frequently Asked Questions: Gold Price Floor and Central Bank Buying

What is the current gold price floor estimate?

There is no single consensus figure. Based on current central bank acquisition patterns and the behaviour of leveraged retail participants, analysts broadly suggest the floor may sit somewhere between $3,000 and $4,500 per troy ounce depending on which buyer category provides support at any given time.

Do central banks actually control the gold price?

No. Central banks are significant participants and provide structural support through consistent accumulation and sentiment signalling, but they cannot control short-term price direction. Leveraged retail traders and institutional macro funds often exert greater influence over near-term pricing.

Why did central banks engage in net selling in early 2025?

The selling activity most likely reflects gold performing its function as a liquid reserve asset. Nations facing currency pressure, trade settlement requirements, or sanctions-related financing needs deploy gold for those purposes. It is strategic usage, not a loss of confidence.

What would push gold to $8,000 per troy ounce?

A large-scale rotation of institutional capital out of traditional 60/40 portfolios into alternatives, triggered by a significant dysfunction in equity, bond, or private asset markets, represents the most plausible catalyst for a price target in that range.

Is the gold bull market over if central banks slow their buying?

Not necessarily, but the nature of the market changes. A bull market sustained primarily by retail leverage is structurally fragile. A transition to institutional-led demand would be necessary for the rally to extend meaningfully and sustainably.

How does the 60/20/20 portfolio model affect gold demand?

If widely adopted, a 20% alternative asset allocation within the US retirement savings system would represent a historically unprecedented flow of capital into assets including gold. Even partial adoption across large pension and insurance portfolios would create structural demand that dwarfs current central bank buying volumes.

What is the relationship between gold prices and interest rate decisions?

Gold becomes more attractive when real interest rates are negative or falling, as the opportunity cost of holding a non-yielding asset decreases. When inflation expectations rise but rate cuts are delayed or reversed, gold faces headwinds because the case for holding it relative to yield-bearing alternatives weakens.

The Floor Is Real, But It Is Not Guaranteed

Gold's Utility as Its Strongest Long-Term Argument

Gold's enduring value proposition is not simply that prices rise over time. It is that the asset has genuine, multi-dimensional utility across sovereign finance, crisis management, trade settlement, and portfolio construction. No currency crisis, geopolitical shock, or institutional restructuring has yet produced a world in which gold ceased to have a function. That durable utility provides a baseline that speculative assets simply cannot replicate.

The Difference Between a Supported Floor and a Rising Price

These are two fundamentally different things, and conflating them is a common analytical error. A supported floor means that demand exists at certain price levels sufficient to absorb selling pressure. A rising price requires that demand exceeds supply at progressively higher price points. Central bank buying can provide the former. Only institutional-scale capital rotation can reliably deliver the latter.

What Investors Should Monitor Over the Next 12 Months

The gold price floor and central bank buying relationship will continue to evolve. The three variables that matter most are the trajectory of net sovereign purchases, the timing and scale of institutional capital deployment into precious metals, and the resolution or escalation of the Iran conflict's impact on oil markets and inflation expectations.

Gold's price floor is a dynamic equilibrium, not a fixed line. It is shaped by sovereign reserve strategies, institutional allocation cycles, macro policy trajectories, and geopolitical risk premiums acting simultaneously. Central bank buying has been foundational to that support structure, but it is neither unconditional nor unlimited. The next leg of any sustained rally requires institutional capital to move from signalling to deployment. Until that transition occurs, the market remains structurally exposed to the volatility that defines retail-dominated, momentum-driven price discovery.

Want to Know When the Next Major Gold Discovery Hits the ASX?

While macro forces and central bank strategies shape gold's long-term price floor, the most explosive returns in the sector have historically come from being first to act on a significant new discovery — and Discovery Alert's proprietary Discovery IQ model scans every ASX announcement in real time, instantly alerting subscribers to high-potential opportunities before the broader market reacts. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position yourself at the forefront of the next major find.