June 15, 2026

The Crowded Trade Problem: Why Consensus Kills Momentum in Commodity Markets

There is a peculiar phenomenon in financial markets where an asset becomes so universally embraced that its very popularity becomes the obstacle to further gains. When every analyst, every fund manager, and every retail investor agrees that something is going higher, the pool of prospective buyers has already been exhausted. The price has, in effect, already consumed its own future demand. This dynamic sits at the heart of the question investors are asking in mid-2026: why isn't gold running higher?

The answer is not simple, and it is certainly not the result of gold losing its fundamental investment credentials. What is happening instead is a collision between positioning psychology, macro headwinds, and a set of counterintuitive institutional flows that most market participants have not fully processed.

When big ASX news breaks, our subscribers know first

Strong Returns That Still Feel Like Failure

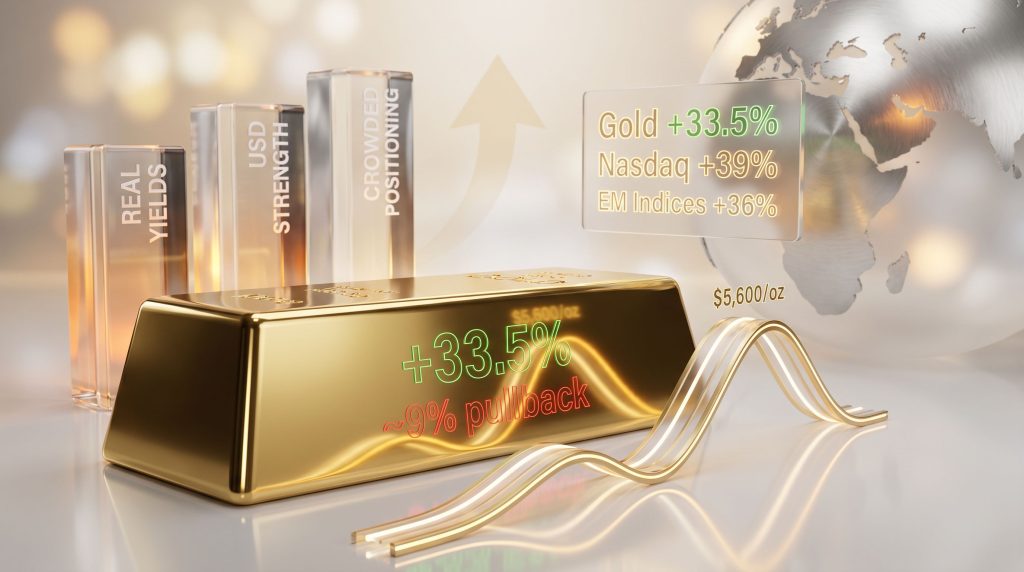

Gold has delivered a 33.5% return over the past 12 months, a figure that, by almost any historical yardstick, would be celebrated as exceptional. To put that in context, three-year average annual returns of that magnitude would generate headlines and attract billions in fresh allocations. Yet the gold community is anxious, not celebratory.

The reason lies in the psychological anchoring effect created by gold's extraordinary January 2026 peak near $5,600 per ounce. After surging from approximately $4,300 at the start of the year, the metal's rapid ascent and equally rapid pullback of roughly 9% have left investors feeling burned rather than enriched. The speed of the reversal matters enormously to investor psychology: a slow, grinding decline is processed differently than a sharp retreat from a perceived peak.

Compounding this is the relative performance problem. Gold's 33.5% gain sits below the Nasdaq's 39% return over the same period and trails select emerging market indices that have gained approximately 36% in US dollar terms. When investors benchmark across asset classes, gold transitions from hero to also-ran in a single comparison.

"Gold's recent consolidation is not evidence of structural failure. It is evidence of what happens when a trade becomes too crowded too quickly, and the market needs time to digest that positioning before the next leg higher can begin."

This anchoring to a recent peak, combined with relative underperformance versus risk assets, has created a narrative of disappointment that does not match the underlying investment case at all. Furthermore, the gold price forecast for 2025 and beyond had already primed many investors to expect continued momentum, making any pause feel disproportionately discouraging.

The Macro Forces Actually Suppressing Gold's Price

Real Yields and the Opportunity Cost Equation

Gold is a non-yielding asset. It pays no dividend, generates no coupon, and produces no cash flow. This means that when investors can earn meaningful real returns from cash, Treasury bills, or money market instruments, the cost of holding gold increases in relative terms. When real yields rise or remain persistently elevated, that opportunity cost acts as a mechanical ceiling on gold's price momentum.

J.P. Morgan's market strategists have characterised Federal Reserve policy uncertainty as one of the primary suppressors of gold's upside in the current environment. The logic is straightforward: gold historically performs best when real yields are falling, when the Fed is in easing mode, or when credible threats to bond market stability emerge. None of those conditions have been firmly established in the current macro backdrop, which means gold lacks the yield environment it needs to break decisively higher.

The specific rate conditions that would unlock the next gold rally are:

- A credible Fed pivot signalling rate reductions are coming

- Falling real yields on US Treasuries, reducing the appeal of fixed income versus bullion

- A material deterioration in US fiscal credibility that undermines bond market confidence

Until one or more of these materialises, the opportunity cost headwind remains a structural cap on gold price momentum.

The US Dollar's Mechanical Suppression Effect

Because gold is priced globally in US dollars, the strength of the dollar directly influences its price in international markets. A stronger dollar means foreign buyers face higher local-currency costs for the same ounce of gold, compressing international demand at the margin. This inverse relationship between dollar strength and gold performance is one of the most reliable correlations in commodity markets.

For gold to stage a sustained breakout from its current consolidation range, dollar weakness is not merely helpful: it is arguably a prerequisite. The macroeconomic conditions that would generate that dollar weakness — including a Fed policy shift, a narrowing of US-international interest rate differentials, or a loss of confidence in US fiscal management — overlap substantially with the conditions that would independently support gold demand. When these forces align, the rally tends to be powerful precisely because multiple tailwinds reinforce each other simultaneously.

Why Inflation Alone Is Not Enough

One of the most persistent misconceptions in gold investing is that rising inflation is a reliable and consistent bullish catalyst. Academic research published through financial economics literature challenges this assumption directly, demonstrating that gold's relationship with consumer price inflation is non-linear and frequently inconsistent.

| Inflation Scenario | Historical Gold Response | Reliability Rating |

|---|---|---|

| Moderate, rising inflation | Mixed, often lagged | Low to Medium |

| Hyperinflationary shock | Strong positive response | High |

| Supply-driven energy inflation | Inconsistent | Low |

| Stagflation (low growth, high inflation) | Historically supportive | Medium to High |

What gold actually responds to is the expectation of monetary instability, not the CPI print itself. When investors believe that central banks are losing control of inflation or that fiscal dominance is eroding monetary policy independence, gold benefits. Rising energy costs and the secondary food price inflation they generate are supportive factors, but they are not sufficient in isolation to drive sustained gold price appreciation.

The Supply Shock Nobody Expected: Sovereign Selling Into Strength

Central Banks That Believe in Gold but Still Sell It

Perhaps the least understood dynamic currently suppressing gold prices is the tactical liquidation of gold reserves by central banks and sovereign wealth funds that remain strategically committed to the metal. This sounds paradoxical, but the logic is straightforward once the mechanism is understood.

When a central bank's gold holdings triple in value over a few years, even a small percentage liquidation of those reserves generates enormous US dollar liquidity. For sovereigns facing currency pressure or fiscal stress, the temptation to monetise a portion of appreciated gold reserves is rational and, importantly, does not signal a change in long-term reserve policy philosophy. Understanding central bank gold demand is therefore essential for interpreting short-term price behaviour without drawing misleading conclusions.

The Central Bank of the Republic of Turkey provides the clearest recent example. Following the US military action against Iran in early 2026, Turkey's central bank sold approximately $8 billion in gold reserves, deploying those proceeds to defend the lira against depreciation pressure and to offset the rising cost of energy imports. This was not a bearish call on gold. It was sovereign balance sheet management under acute fiscal stress.

"The distinction between structural demand and tactical selling is critical for understanding why aggregate gold demand can remain positive on a 12-month basis while short-term price action appears confused and directionless."

Gulf Sovereign Wealth Funds and the Oil-Revenue Compression Problem

The geopolitical conflict that erupted in early 2026 created an additional and underappreciated supply-side dynamic. Gulf state sovereign wealth funds, which had been significant net buyers of gold as part of reserve diversification programmes, faced a simultaneous compression of their primary revenue source as conflict-related market disruptions affected oil income.

When a government's hydrocarbon revenues fall sharply, sovereign wealth funds may be required to liquidate liquid assets, including gold, to fund domestic fiscal obligations. This creates a perverse outcome: the geopolitical event that should drive safe-haven flows into gold simultaneously forces some of the world's largest institutional gold holders to become net sellers. The two effects partially offset each other, leaving the price range-bound despite a fundamentally bullish narrative.

Technical Positioning and the No-Man's Land Problem

J.P. Morgan's market analysts have used the term no-man's land to describe gold's current technical position: capped below meaningful resistance levels with insufficient momentum to attract systematic trend-following capital, but supported well enough above key support zones to prevent a capitulation sell-off.

This technical indeterminacy creates its own feedback loop. Investors who bought near the January peak have negative short-term experiences. Stop-loss cascades and margin calls during the post-peak correction pushed additional sellers into the market, reinforcing the downside move. Now a cohort of sidelined investors exists with the psychological scar of having bought near the high, and they are unlikely to re-enter until the price demonstrates convincing upside momentum.

CFTC futures positioning data serves as a useful leading indicator of this dynamic. When speculative long positioning reaches extreme levels, the probability of a sentiment reversal increases regardless of what the fundamental picture suggests. The crowded trade problem — articulated succinctly in the Alpine Macro framing that if something becomes too obvious it probably is not true — applies with particular force when everyone has already positioned for the move. Consequently, the gold-stock relationship becomes especially relevant here, as positioning extremes in one market frequently signal broader shifts across both.

Geopolitical Risk: Priced In, Not Additive

Why New Conflicts Are Not Automatically Bullish

Conventional financial market wisdom holds that military conflict is an automatic catalyst for gold as a safe haven. The reality in 2026 has been more complicated. The US attack on Iran in early 2026, along with subsequent US actions involving Venezuelan leadership, did generate safe-haven inflows, but those flows were partially offset by the institutional selling described above.

More importantly, gold had already incorporated a substantial geopolitical risk premium during its multi-year rally from sub-$2,000 levels to the $5,600 peak. For a new geopolitical event to generate incremental safe-haven demand, it must exceed the risk level that markets had already priced in. Events that simply confirm an already-elevated risk environment generate headline anxiety but not necessarily net new buying.

The de-dollarisation thesis, which has been a meaningful structural tailwind for gold across multiple years, continues to progress but at a pace that is slower than many gold bulls anticipated. Central bank reserve diversification away from US Treasuries and dollar-denominated assets is structurally intact as a multi-year trend, however its incremental pace in any given quarter is insufficient to overwhelm the positioning and macro headwinds described above.

The next major ASX story will hit our subscribers first

Building a Portfolio Framework Around Gold's Consolidation

Physical Gold vs. Mining Equities: Complementary, Not Competing

For investors assessing their gold exposure during this consolidation phase, the choice between physical gold vs ETFs and gold mining equities is not binary. Each instrument serves a different function within a portfolio.

| Attribute | Physical Gold | Gold Mining Equities |

|---|---|---|

| Income generation | None | Dividend yield, often substantial |

| Leverage to gold price | 1:1 | Amplified via operational leverage |

| Portfolio stabilisation | High | Moderate |

| Volatility profile | Lower | Higher |

| Operational risk exposure | None | Significant |

| Liquidity | High via ETFs or bullion | Variable by company size |

Mining equities carry what analysts call operational leverage: when the gold price rises above a miner's all-in sustaining cost, profits increase at a rate that outpaces the gold price gain itself. A 10% increase in the gold price can translate to a 30% or 40% increase in mining company earnings, depending on the cost structure. This amplification works in reverse during downturns, which explains why gold stocks are revaluing higher in some instances even as physical gold consolidates.

During periods of gold price consolidation, mining equities offer an important advantage: dividend income. Miners with strong balance sheets and low all-in sustaining costs continue generating and distributing cash even when the gold price is range-bound. This income generation provides a return stream that physical gold cannot replicate, making a combined allocation to both instruments a rational approach during uncertain periods.

Three Catalysts That Could End the Stall

The structural investment case for gold remains intact. What is missing is the specific macro trigger that converts existing positioning into a sustained new rally. Three potential catalysts stand out:

- A credible Federal Reserve pivot, including explicit signalling of rate reductions or yield curve control measures, which would directly compress the opportunity cost of holding gold.

- A sustained weakening of the US dollar, driven by narrowing interest rate differentials, deteriorating US fiscal credibility, or accelerated de-dollarisation flows from reserve managers.

- An unexpected financial or geopolitical shock that materially exceeds current risk pricing, triggering fresh safe-haven demand from investors not already positioned in gold.

Critically, gold does not require all three catalysts to align simultaneously. A single powerful trigger, particularly a convincing Fed pivot, could be sufficient to reignite substantial upside momentum from a consolidated base.

Frequently Asked Questions About Gold's Current Stall

Why did gold stop going up after reaching $5,600 per ounce?

The January 2026 peak triggered a wave of profit-taking from investors who had accumulated positions during the preceding rally. This coincided with elevated speculative futures positioning and unexpected institutional selling by sovereign entities managing acute fiscal and currency pressures. The correction reflects positioning dynamics and short-term supply factors more than any deterioration in gold's fundamental investment case.

Does geopolitical conflict always push gold higher?

Not automatically, and the 2026 experience illustrates why. Conflict can simultaneously generate safe-haven buying from retail and institutional investors while forcing affected sovereigns to liquidate gold reserves for liquidity. When geopolitical risk is already substantially priced into the gold level after a prolonged rally, new events must exceed existing risk expectations to generate net incremental demand.

Why are central banks selling gold if they remain strategically bullish on it?

Central banks that have seen their gold reserves triple in value over several years face a straightforward arithmetic reality: a modest percentage liquidation generates enormous dollar liquidity without meaningfully reducing strategic exposure to the asset. Turkey's approximately $8 billion in gold sales following the Iran conflict represents tactical treasury management under currency and energy cost pressure, not a philosophical change in reserve policy.

What is the single biggest risk to the gold bull case?

A sustained increase in real yields combined with dollar strength and meaningful de-escalation of geopolitical tensions would represent the most challenging environment gold could face. This combination would simultaneously increase the opportunity cost of holding gold, suppress its USD price mechanically, and reduce the safe-haven premium embedded in current valuations.

Key Takeaways for Gold Investors in 2026

- Gold's 33.5% annual return is objectively strong by historical standards; the disappointment is relative, anchored to a January peak rather than a genuine assessment of performance

- Real yield dynamics, US dollar strength, and crowded speculative positioning are the primary near-term suppressors of gold price momentum

- Sovereign selling from institutions under fiscal stress, including Turkey's $8 billion gold liquidation, represents a temporary but meaningful supply-side headwind

- The structural investment case encompassing inflation trajectory, de-dollarisation momentum, and geopolitical risk remains fundamentally intact

- Gold consolidation phases historically precede renewed rallies when macro conditions shift in the metal's favour

- A portfolio combining physical gold for stabilisation and mining equities for dividend income offers a balanced and complementary approach to gold exposure during periods of price uncertainty

This article is intended for informational and educational purposes only and does not constitute financial advice. All forecasts, price references, and analyst assessments involve inherent uncertainty. Past performance is not indicative of future results. Readers should conduct their own due diligence or consult a licensed financial adviser before making investment decisions.

Want to Know When the Next Major Gold Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable opportunities — so investors can position themselves ahead of the broader market. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure a market-leading edge.