July 10, 2026

The relationship between gold prices and US Federal Reserve rate policy has fundamentally shifted in 2026, creating unprecedented challenges for investors navigating precious metals markets. The Federal Reserve's unwavering commitment to restrictive monetary policy, despite escalating geopolitical tensions, has disrupted traditional safe-haven demand patterns that historically supported gold during international crises. This transformation reflects a structural change in how central banking frameworks operate, prioritising price stability over immediate market accommodation.

The evolution of central banking frameworks since the 2008 financial crisis has created new transmission mechanisms that operate differently during periods of economic stress. Understanding these dynamics becomes crucial for investors navigating precious metals markets, particularly as traditional hedging strategies confront modern monetary policy realities.

Understanding the Fed's Current Monetary Policy Framework

The Federal Reserve maintained its benchmark interest rate at the 3.50%-3.75% range during its March 2026 meeting, marking a continuation of its restrictive stance initiated in December 2025. This decision reflects the central bank's commitment to controlling inflationary pressures despite mounting geopolitical tensions across global markets.

The monetary policy environment has transitioned from aggressive easing to what market participants characterise as a hawkish pause. Unlike previous cycles where geopolitical uncertainty prompted accommodative policy responses, the Fed's current approach prioritises price stability over immediate crisis management. This represents a significant departure from post-2008 monetary policy frameworks that typically provided market support during international conflicts.

Key Policy Metrics:

- Federal funds rate: 3.50%-3.75% (held since December 2025)

- Real interest rate: Approximately 0.8%-1.25% based on inflation projections

- Policy stance: Restrictive territory by historical standards

- Duration of current hold: Four consecutive meetings

The distinction between a policy pause and an extended hold carries technical significance for market participants. A pause typically signals potential future adjustments, while sustained holding suggests the current stance remains appropriate for extended periods. Fed communications regarding rate maintenance, coupled with upward inflation revisions, indicate prioritisation of price stability over growth accommodation.

Market expectations for rate cuts have diminished substantially as the central bank maintains its anti-inflationary focus. This shift has created challenging conditions for non-yielding assets like gold, which traditionally benefit from lower interest rate environments. Furthermore, the Fed's commitment to restrictive policy overrides conventional safe-haven demand drivers during geopolitical stress.

When big ASX news breaks, our subscribers know first

What Economic Indicators Drive Fed Decision-Making on Interest Rates?

Core Inflation Metrics and Their Gold Market Impact

Personal Consumption Expenditures (PCE) inflation projections currently stand at 2.7%, representing persistence above the Fed's 2% target despite previous tightening measures. This sustained inflationary pressure maintains the central bank's commitment to restrictive policy even as labour market resilience might otherwise suggest room for accommodation.

The Federal Reserve's dual mandate framework requires balancing price stability with maximum employment objectives. These mandates occasionally create policy tensions, particularly when unemployment remains low while inflation stays elevated. Current economic conditions present exactly this scenario, with the Fed perceiving sufficient inflation-fighting work remains to justify continued rate maintenance at restrictive levels.

Critical Inflation Components:

- Core PCE: Excludes volatile food and energy prices

- Headline PCE: Includes all consumption expenditures

- Services inflation: Often more persistent than goods inflation

- Housing costs: Largest component of consumer price indices

Energy price volatility from Middle East tensions creates secondary inflation effects through transportation and production cost increases. The Fed must assess whether current price pressures represent transitory disruptions or structural inflationary forces requiring sustained policy responses.

GDP Growth Projections and Monetary Policy Balance

Economic growth forecasts continue supporting the Fed's higher-for-longer rate approach, with revised projections indicating sufficient economic momentum to withstand restrictive monetary conditions. However, regional economic variations influence policy decisions, though national aggregates drive primary policy considerations.

Real interest rates serve as the policy-relevant metric for Fed decision-making. With nominal rates at 3.50%-3.75% and inflation expectations at 2.7%, real rates maintain approximately 0.75%-1.25%, remaining in restrictive territory though less restrictive than during the peak 2022-2023 tightening cycle.

The Fed typically weights forward-looking indicators alongside concurrent economic data. For instance, emphasis on higher inflation projections rather than current readings suggests central bank concern about future inflationary pressures rather than immediate economic conditions. This forward-looking approach has implications for asset classes sensitive to interest rate expectations.

Why Has Gold's Traditional Safe-Haven Status Been Challenged?

Opportunity Cost Analysis of Non-Yielding Assets

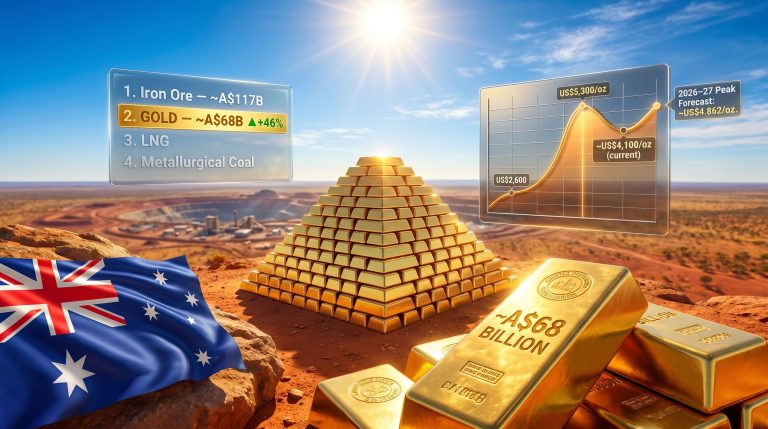

Gold's decline from approximately $5,300 per ounce in early March to around $4,500 by late March represents a 15% deterioration despite ongoing geopolitical tensions. This performance breakdown challenges fundamental assumptions about precious metals serving as reliable crisis hedges in modern financial markets.

The opportunity cost mechanics create substantial headwinds for gold investment. As a non-yielding asset generating no coupon, dividend, or interest income, gold's returns derive entirely from price appreciation. When interest rates remain elevated, the opportunity cost of holding gold relative to Treasury securities increases substantially.

Comparative Yield Analysis:

- 3-month Treasury bills: Approximately 3.5%-3.75%

- Gold yield: 0% plus/minus price changes

- Real return threshold: Gold must appreciate beyond real interest rates

- Current real rate: 0.8%-1.25% annually

Empirical research indicates gold demonstrates elasticity of approximately -0.5 to -0.7 relative to real interest rates. This means for every 100 basis points increase in real rates, gold prices typically decline 5-7%. Current real rate levels suggest gold faces structural headwinds from both absolute rate levels and stability expectations.

Dollar Strength Dynamics and Commodity Pricing

The US Dollar Index appreciated more than 2% during March 2026, demonstrating foreign exchange flows favouring dollar-denominated assets over traditional safe havens. This dollar strength creates additional pressure on commodities priced in dollars, as international buyers face higher local currency costs for gold purchases.

Currency dynamics interact with monetary policy through multiple transmission channels. Higher US interest rates attract international capital flows, strengthening the dollar while simultaneously increasing the opportunity cost of holding non-yielding assets. Consequently, this dual pressure mechanism has proven particularly challenging for gold market performance during the current cycle.

Trade-weighted dollar impacts extend beyond direct pricing effects to influence global commodity demand patterns. Emerging market central banks and sovereign wealth funds face higher acquisition costs for gold reserves, potentially dampening official sector demand that traditionally supports prices during crisis periods.

How Do Geopolitical Events Interact with Monetary Policy Effects?

Oil Price Shocks and Inflation Expectations

The March 14, 2026 oil facility strikes in Fujairah, UAE, followed earlier US-Israeli strikes on Iran, creating supply disruption concerns across energy markets. Historically, such events would generate sustained support for gold as investors sought inflation protection and safe-haven assets.

However, the Federal Reserve's inflation-fighting commitment has fundamentally altered market reaction functions. Rather than anticipating accommodative policy responses to cushion economic impacts from higher energy costs, markets recognise that oil price increases may prompt additional monetary tightening to prevent second-round inflation effects.

Energy-Inflation Transmission Mechanisms:

- Direct effects: Higher petrol and heating costs

- Indirect effects: Increased production and transportation costs

- Expectation effects: Wage and price-setting behaviour changes

- Policy responses: Central bank reactions to prevent wage-price spirals

This policy reaction function reversal explains why traditional commodity-gold correlations have weakened. During the 1970s and early 2000s, escalating commodity prices triggered accommodative responses; in 2026, the Fed maintains restrictive policy despite inflationary impulses, reversing normal support mechanisms for precious metals.

Central Bank Gold Purchasing Patterns

Official sector demand patterns have evolved significantly as central banks navigate competing objectives of reserve diversification and yield optimisation. Emerging economy central banks face particular challenges as dollar strength increases gold acquisition costs while domestic currency pressures limit foreign reserve deployment.

Sovereign wealth fund allocation strategies increasingly emphasise yield-generating assets over traditional stores of value. This shift reflects modern portfolio theory applications to official reserves, where opportunity costs receive greater consideration than during previous decades of reserve accumulation.

Reserve diversification trends among emerging economies continue supporting long-term gold demand, though timing and pace adjustments reflect current market conditions. Chinese central bank accumulation strategies particularly influence global demand patterns given the scale of potential purchases.

What Market Mechanisms Transmit Fed Policy to Gold Prices?

Exchange-Traded Fund Flow Analysis

Gold ETF creation and redemption patterns during rate cycles provide crucial insights into investor behaviour and market sentiment. Institutional versus retail investor responses differ significantly, with institutional flows typically more sensitive to interest rate differentials while retail investors focus on geopolitical headlines.

ETF Flow Indicators:

- Creation units: Large investor buying through authorised participants

- Redemption patterns: Institutional selling pressure indicators

- Premium/discount analysis: Supply-demand imbalances in ETF shares

- Volume trends: Overall investor engagement levels

Liquidity conditions in precious metals markets affect price discovery mechanisms, particularly during periods of heightened volatility. ETF flows serve as transmission channels between broader financial market conditions and physical gold demand, though timing lags can create temporary disconnects.

Futures Market Positioning and Speculation

COMEX positioning data reveals significant shifts in speculative interest as monetary policy expectations evolve. Hedge fund and managed money flows respond rapidly to Fed communications, creating volatility patterns that extend beyond fundamental supply-demand dynamics.

In addition, technical trading patterns during policy uncertainty often amplify underlying trends as algorithmic systems respond to momentum signals. These automated responses can accelerate price movements beyond levels justified by fundamental factors, particularly during periods of reduced liquidity.

Futures Market Dynamics:

- Open interest levels: Total outstanding contract positions

- Commitment of traders data: Commercial versus speculative positioning

- Roll patterns: Contract expiration and delivery considerations

- Basis relationships: Spot versus futures pricing differentials

Investment Strategy Implications Across Rate Scenarios

Portfolio Allocation Models Under Different Fed Paths

Scenario Analysis Framework:

Scenario 1: Continued Hawkish Stance Through 2026

- Expected gold price range: $4,200-$4,800

- Real rates remain elevated at 1.0%-2.0%

- Dollar strength persists amid rate differentials

- Alternative assets: Treasury bills, high-yield bonds, dividend stocks

Scenario 2: Gradual Easing Beginning Q3 2026

- Target gold price projections: $5,200-$5,600

- Rate cuts of 100-150 basis points over 12 months

- Reduced opportunity costs for non-yielding assets

- Duration risk considerations for existing bond positions

Scenario 3: Economic Downturn Forcing Aggressive Cuts

- Potential gold rally to $6,000+ levels

- Emergency rate reductions to near-zero levels

- Risk-off asset rotation patterns favour precious metals

- Credit market stress indicators signal recession probability

Each scenario requires distinct allocation approaches balancing precious metals exposure against interest rate sensitivity and credit risk considerations. Dynamic rebalancing based on Fed communication patterns becomes essential for optimising risk-adjusted returns.

The next major ASX story will hit our subscribers first

Regional Market Variations and Policy Transmission

Asia-Pacific Gold Demand Patterns

Chinese central bank accumulation strategies continue influencing global gold markets despite domestic economic headwinds. Chinese official reserves have expanded consistently, though monthly purchase volumes vary based on price levels and currency considerations.

Indian seasonal demand cycles remain important for global consumption patterns, particularly during wedding season and festival periods. Import policy adjustments by the Indian government can significantly impact global demand, especially when combined with currency fluctuations affecting local gold prices.

Australian mining sector production responses to current price levels affect supply-side dynamics. Production cost curves at $4,500 gold suggest most operations remain profitable, though reduced exploration and development activity may impact future supply availability.

European Monetary Policy Coordination Effects

European Central Bank policy divergence creates additional complexity for global gold markets. ECB monetary policy coordination with Fed decisions affects euro-dollar exchange rates and relative appeal of European versus US assets for international investors.

Brexit-related currency volatility continues impacting UK gold demand patterns, while European energy security considerations following Middle East tensions support some regional safe-haven demand despite broader market headwinds.

Forward-Looking Market Structure Analysis

Technology and Trading Evolution

Algorithmic trading systems increasingly dominate gold price discovery, with automated responses to Fed communications creating rapid price adjustments that may overshoot fundamental valuations. These systems often amplify volatility during policy uncertainty periods.

Cryptocurrency correlation patterns during Fed cycles reveal evolving relationships between digital assets and traditional safe havens. Bitcoin and gold correlations have varied significantly based on regulatory developments and institutional adoption patterns.

Technology Impact Factors:

- High-frequency trading: Millisecond responses to Fed statements

- Machine learning algorithms: Pattern recognition in policy cycles

- Digital asset competition: Alternative store-of-value narratives

- Settlement system evolution: T+0 settlement reducing counterparty risks

Supply-Side Constraints and Production Costs

Mining industry capital allocation decisions increasingly focus on high-grade, low-cost operations as companies prioritise cash generation over production growth. Current gold prices support most existing operations while reducing incentives for marginal project development.

Production cost curves indicate break-even levels for major producing regions range from $1,200-$1,800 per ounce for existing operations, suggesting substantial margins at current prices. However, new project development requires higher price assumptions given increased regulatory and environmental compliance costs.

Exploration and development pipeline analysis reveals reduced industry investment in new discoveries, potentially constraining future supply availability. This supply-side dynamic may support longer-term prices despite current monetary policy headwinds.

Risk Management Framework for Gold Investments

Volatility Measurement and Hedging Strategies

Historical volatility patterns during Fed rate cycles provide guidance for risk management approaches. Gold volatility typically increases during policy transition periods, requiring position sizing adjustments and enhanced hedging consideration.

Options market pricing reflects elevated uncertainty about future gold price direction. Put option premiums have increased relative to call options, indicating heightened downside protection demand among institutional investors.

Risk Metrics for Gold Exposure:

- Value-at-Risk (VaR): Potential losses over specific time horizons

- Correlation stability: Relationship consistency across market conditions

- Drawdown analysis: Maximum peak-to-trough decline patterns

- Sharpe ratio evolution: Risk-adjusted return optimisation

Liquidity Considerations Across Market Conditions

Bid-ask spread behaviour during stress periods reveals market depth and transaction cost implications. Physical gold markets typically experience wider spreads during volatility, while ETF trading maintains relatively tight spreads due to authorised participant arbitrage mechanisms.

According to Federal Reserve analysis, physical versus paper gold market dynamics can diverge during extreme conditions. Settlement and custody considerations become particularly relevant for large institutional positions requiring physical delivery capabilities.

Liquidity Risk Factors:

- Market depth: Order book thickness at various price levels

- Settlement timing: T+2 for ETFs versus longer physical delivery

- Custody costs: Storage and insurance expense considerations

- Counterparty risk: Exchange and clearing member exposures

Strategic Positioning for Gold Investment Success

Key Monitoring Indicators for Investors

Fed communication pattern analysis requires attention to both formal statements and individual Federal Open Market Committee member speeches. Changes in language regarding inflation outlook, labour market assessment, and international developments signal potential policy shifts before formal rate decisions.

Real yield threshold levels historically associated with gold support suggest monitoring 10-year Treasury Inflation-Protected Securities yields. When real yields exceed 1.5%, gold typically faces significant headwinds requiring exceptional circumstances to generate positive returns.

Critical Monitoring Framework:

- Fed Funds futures: Market-implied rate expectations 12-24 months forward

- Yield curve dynamics: 2-year/10-year spreads indicating recession probability

- Dollar index momentum: Currency strength trends affecting commodity pricing

- Geopolitical risk premium: Option volatility and safe-haven demand indicators

Dynamic Allocation Recommendations

Portfolio construction should incorporate scenario-based allocation models recognising the evolving relationship between gold prices and US Federal Reserve rate policy. Traditional static allocations may prove inadequate given current market structure changes.

Risk budget allocation for precious metals exposure requires balancing potential upside during crisis periods against opportunity costs during stable conditions. For comprehensive insights into future market dynamics, investors should consider reviewing the gold price forecast to understand the broader context of these allocation decisions.

Moreover, tactical allocation adjustments based on real yield levels and Fed communication patterns optimise risk-adjusted portfolio returns. Furthermore, understanding the relationship between record-high gold prices and current monetary policy provides essential context for these strategic decisions.

Timeline considerations vary significantly across investment horizons. Short-term tactical positions must account for Fed meeting schedules and economic data releases, while long-term strategic allocations focus on structural supply-demand dynamics and monetary policy regime changes.

The relationship between gold prices and US Federal Reserve rate policy continues evolving as central banking frameworks adapt to modern economic challenges. Investors navigating this environment benefit from understanding both traditional precious metals fundamentals and contemporary monetary policy transmission mechanisms. Success requires dynamic approaches recognising that historical relationships may not persist under current policy regimes, while maintaining awareness that fundamental economic principles continue governing long-term asset performance patterns.

Examining the historic gold surge explanation provides additional perspective on how market dynamics have evolved, while the comprehensive gold-stock market guide offers valuable insights into broader investment strategy implications during these unprecedented monetary policy conditions.

Ready to Capitalise on Market-Moving Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities whilst others react to yesterday's news. Explore how major mineral discoveries have historically generated substantial market returns, then begin your 14-day free trial today to position yourself ahead of the market.