June 25, 2026

The Structural Shift Reshaping Junior Gold Exploration in Scandinavia

There is a recognisable pattern playing out across the global gold sector right now. As Tier 1 producers refine their portfolios around near-term production assets, early-stage exploration projects with genuine geological merit are quietly being handed off to smaller, more focused operators. These juniors, unconstrained by the capital allocation pressures of a multi-asset major, are often better positioned to unlock value through concentrated drilling activity and regional specialisation. The Goldsky Agnico Barsele deal is one of the clearest recent examples of this dynamic in action, and it deserves a closer examination than a simple news announcement provides.

When big ASX news breaks, our subscribers know first

Why Full Ownership Changes Everything for a Junior Explorer

Joint venture structures in the mining industry can be operationally useful, but they introduce layers of complexity that often slow progress at the exploration stage. Shared decision-making, competing capital allocation priorities between partners, and the need for mutual approvals on drilling decisions can all compress the pace at which a project advances. For junior explorers operating on tight timelines and investor mandates, these frictions represent real costs.

When Goldsky Resources (TSXV: GSKR) closed its acquisition of Agnico Eagle's 55% interest in the Barsele gold project in Sweden, it eliminated all of those constraints at a stroke. Sole ownership means Goldsky can design, fund, and execute its drilling programs without requiring partner sign-off. It can respond faster to assay results, redirect resources toward higher-priority targets, and communicate a coherent, unambiguous strategy to its shareholders.

For Agnico Eagle, the logic is equally straightforward. The company has built one of the world's most admired gold mining portfolios through a disciplined focus on assets that can reach production at scale. Barsele, while geologically interesting, required years of additional exploration before any development decision could be made. Divesting that exposure while retaining both an equity stake and a royalty interest represents a textbook approach to managing optionality without operational drag. Furthermore, the mineral exploration importance of assets like Barsele becomes even clearer when viewed through this lens of strategic portfolio management.

Breaking Down the Goldsky Agnico Transaction Structure

The financial architecture of the Goldsky Agnico Barsele deal reflects careful thinking about balancing cash preservation with strategic alignment. Rather than a straightforward cash buyout, the transaction was structured to keep Agnico meaningfully invested in Goldsky's future success.

| Component | Detail |

|---|---|

| Cash Consideration | US$20 million |

| Share Consideration | |

| Royalty Retained by Agnico | 2% NSR on Barsele production |

| NSR Buyback Option | US$50 million within two years of commercial production |

| Agnico's Resulting Goldsky Stake | |

| Finder's Fee (Nuvolari Capital) | 2.57 million shares at C$2.64 |

| CEO Share Allocation | 468,550 shares at C$3.20 deemed price |

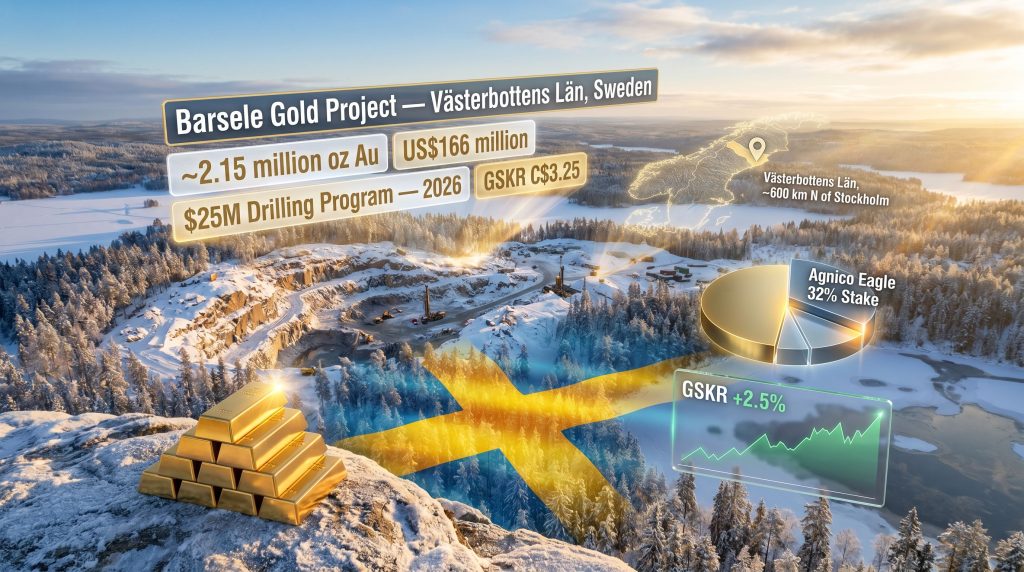

The total transaction value sits at approximately US$166 million, structured as a hybrid of cash and equity consideration. This approach is well-established in junior mining mergers and acquisitions: it conserves the acquirer's cash for exploration activity while giving the vendor direct participation in any re-rating of the asset they've sold. In addition, gold M&A activity of this nature is increasingly common as majors rationalise their portfolios in favour of near-term production assets.

Agnico's transition from a 4.1% minority holder to an approximately 32% strategic cornerstone investor is particularly significant. This is not a vendor walking away from a project they have lost faith in. The investor rights agreement, which includes top-up provisions, makes clear that Agnico intends to remain engaged with Goldsky's trajectory. Shareholders evidently agreed, with approval for Agnico's designation as a Control Person passing with 99.99% of votes in favour.

Understanding the Net Smelter Return Royalty

The 2% NSR royalty retained by Agnico deserves specific attention because it is often misunderstood by investors outside the mining sector. An NSR royalty entitles the holder to a percentage of gross revenue generated from ore sales, calculated after deducting smelting and refining charges, but with no requirement to contribute to any future capital expenditure or operating costs. In practical terms, it is a perpetual revenue stream that Agnico preserves at zero ongoing cost.

The inclusion of a US$50 million buyback clause, exercisable within two years of Barsele achieving commercial production, gives Goldsky a clearly defined pathway to full economic ownership of the project if it reaches that milestone. This clause is consequential: at production stage, a 2% NSR on a 2-million-ounce-plus project at prevailing gold prices could represent a very material annual royalty payment, so the option to extinguish that obligation for a fixed sum provides meaningful long-term financial flexibility.

It is also worth noting that Goldsky has assumed Agnico's existing royalty obligations to Orex Minerals (TSXV: REX) as part of the transaction. Stacked royalties can compress project economics at production stage, and investors in exploration-stage companies should factor the cumulative royalty burden into any long-term valuation work.

The Barsele Gold Project: Geological Context and Resource Profile

Barsele is located in Västerbottens Län in northern Sweden, roughly 600 kilometres north of Stockholm. The project sits within a Palaeoproterozoic-age geological province that has attracted sustained exploration interest for decades. Sweden's Fennoscandian Shield hosts some of Europe's most significant gold deposits, and the northern part of the country in particular has emerged as a genuine exploration destination with the geological credentials to support large-scale resource development.

The existing resource base at Barsele reflects approximately a decade of exploration work conducted by Agnico Eagle:

| Resource Category | Gold Ounces |

|---|---|

| Indicated Resource | 320,781 oz Au |

| Inferred Resource | ~1.83 million oz Au |

| Total Resource | ~2.15 million oz Au |

The heavy weighting toward the inferred category is the most important geological and commercial fact about Barsele. Under NI 43-101 reporting standards, inferred resources represent the lowest level of geological confidence. They cannot be included in economic assessments, pre-feasibility studies, or reserve calculations without first being upgraded through systematic drilling. The gap between Barsele's inferred base and its indicated inventory is, in effect, the core exploration mandate that Goldsky is now pursuing.

The resource structure also tells us something about the nature of the mineralisation at Barsele. Projects that remain predominantly inferred after a decade of work by a well-resourced major typically reflect either genuinely complex structural geology requiring dense drill patterns to resolve, or a deliberate decision by the previous operator to prioritise resource discovery over resource conversion. In Agnico's case, the latter seems more likely. The company's internal hurdle rates for continued investment probably favoured deploying capital elsewhere, leaving Barsele's conversion potential largely untapped.

The Gold Line Belt: A Geological Setting Worth Understanding

Two of Goldsky's other Swedish projects, Paubäcken and Storjuktan, sit within the Gold Line belt in northwestern Sweden. This structurally controlled, Palaeoproterozoic-age corridor is one of Scandinavia's most consistently mineralised gold trends, hosting multiple deposits and attracting sustained junior exploration activity over the past two decades.

The geological architecture of the Gold Line belt is characterised by shear-zone hosted gold mineralisation, often associated with mafic to intermediate intrusive bodies. These structural settings can produce vertically extensive, high-grade ore shoots that are particularly valuable targets for underground mining scenarios. Understanding this geological context helps explain why a company like Goldsky is building a multi-project portfolio within a defined regional corridor: the exploration knowledge base and geological models developed at one project often directly inform targeting at adjacent licences.

Goldsky's fourth project, Rajapalot, is located in the Lapland region of Finland. This Finland gold project adds further regional diversification across the Fennoscandian Shield, and the broader portfolio gives the company exposure to what is increasingly recognised as one of the world's most geologically prospective and jurisdictionally stable gold exploration regions.

Goldsky's Multi-Asset Scandinavian Portfolio

| Project | Country | Region |

|---|---|---|

| Barsele (flagship) | Sweden | Västerbottens Län |

| Paubäcken | Sweden | Gold Line Belt (NW Sweden) |

| Storjuktan | Sweden | Gold Line Belt (NW Sweden) |

| Rajapalot | Finland | Lapland Region |

The deliberate concentration of assets across Sweden and Finland positions Goldsky as a regionally focused vehicle rather than a geographically diversified junior. This approach has both advantages and risks. On the positive side, regional concentration allows for genuine geological expertise to compound over time, with learnings from each project informing exploration across the portfolio. Infrastructure sharing, relationships with local communities, and familiarity with permitting requirements all become more efficient at scale within a defined geography.

The 2026 Drilling Program: Scale, Objectives, and Implications

With the Goldsky Agnico Barsele deal now closed, the immediate focus shifts to execution. Goldsky has committed $25 million toward its 2026 drilling program at Barsele, a campaign that management has described as one of the most extensive ever undertaken across the licence area.

A major drilling campaign at an exploration-stage gold project typically pursues several distinct but interconnected objectives:

-

Infill drilling tightens the spacing between existing drill holes across known mineralised zones, providing the geological data density required to upgrade inferred resources to the indicated category.

-

Step-out drilling extends known mineralisation along strike and at depth, testing whether the resource envelope can be expanded beyond its current boundaries.

-

Greenfield target testing involves drilling geophysical anomalies and structural targets that sit outside the current resource model, representing the highest-risk but potentially highest-reward component of the program.

-

Metallurgical sampling collects representative drill core for processing testwork, which is essential for understanding gold recoveries and informing future economic studies.

-

Resource model updating integrates all new assay data into a revised geological model that forms the basis of a public NI 43-101 compliant resource estimate.

For investors, the most commercially significant near-term catalyst is infill drilling success that converts inferred ounces to indicated status. This category upgrade does not change the total amount of gold in the ground, but it fundamentally changes what can be done with that gold from an economic evaluation perspective. Consequently, interpreting gold drill results correctly is essential for investors tracking Goldsky's progress. A project with two million indicated ounces is substantially more advanced, and more financeable, than one with two million inferred ounces.

The next major ASX story will hit our subscribers first

Market Response and Valuation Context

Goldsky's share price rose approximately 2.5% on the day the transaction closed, reaching C$3.25 per share and implying a market capitalisation of approximately C$598 million. Against a total resource base of roughly 2.15 million ounces, this translates to an implied in-situ valuation of approximately C$278 per resource ounce.

This per-ounce metric is a commonly used screening tool among junior gold investors, though it requires careful interpretation. Comparing this figure against peer companies in similar jurisdictions and at similar stages of development provides a useful relative value signal, but the absolute number is meaningless without considering resource confidence levels, jurisdiction risk, metallurgy, and the capital required to advance toward production.

Investor note: Given that the majority of Barsele's resource sits in the inferred category, any per-ounce valuation comparison should be made against peers with similarly weighted resource profiles, not against companies with predominantly indicated or measured resources. The risk-adjusted value of an inferred ounce is materially lower than that of an indicated ounce.

The C$598 million market capitalisation also provides context for the $25 million drilling budget. Goldsky is committing approximately 4.2% of its market cap to a single year's exploration activity at its flagship project. For a junior explorer, this represents a meaningful capital commitment that signals genuine intent to advance the resource quickly.

Why Scandinavia Is Attracting Serious Junior Gold Capital

The jurisdictional context of the Goldsky Agnico Barsele deal matters as much as the geology. Sweden and Finland consistently rank among the world's most mining-friendly jurisdictions, offering political stability, transparent regulatory frameworks, and established permitting processes that reduce the sovereign risk premium that investors attach to projects in more volatile geographies.

Both countries are EU member states, giving companies listed on North American exchanges access to a European investor base that is increasingly focused on ESG-aligned commodity exposure. The ability to produce gold in a jurisdiction with high environmental standards, strong labour protections, and well-developed infrastructure is becoming a genuine differentiator as institutional capital flows increasingly incorporate non-financial risk factors.

Rising gold prices through 2025 and into 2026 have improved the economic case for advancing lower-grade or higher-cost projects. Furthermore, current gold exploration trends point firmly toward Fennoscandian assets as a preferred destination for junior exploration capital. Sweden's established mining infrastructure, including road access, power networks, and proximity to processing facilities, materially reduces the capital intensity of bringing a project like Barsele toward production compared with remote, infrastructure-poor jurisdictions.

Key Risks Every Investor Should Understand

The Goldsky Agnico Barsele deal is compelling on multiple fronts, but however, a balanced assessment requires clear-eyed acknowledgment of the risks involved.

-

Resource conversion is not guaranteed. Drilling programs frequently encounter geological complexity that prevents straightforward category upgrades. Discontinuous mineralisation, variable grade distribution, or structural complexity can all limit conversion success despite significant capital investment.

-

Capital requirements will grow substantially. A $25 million drilling program is a starting point, not an endpoint. Advancing Barsele through pre-feasibility and feasibility study stages would require investment measured in hundreds of millions of dollars, and future equity financings carry dilution risk for existing shareholders.

-

Stacked royalty obligations. The combination of the 2% NSR retained by Agnico and the existing obligations to Orex Minerals creates a royalty burden that will reduce net project economics at any future production stage. Investors should model these costs into any long-term scenario analysis.

-

Gold price sensitivity. The entire thesis depends, to varying degrees, on gold prices remaining supportive. A significant price correction would reduce the economic attractiveness of Barsele and potentially constrain Goldsky's ability to fund future exploration rounds.

-

Inferred resources are not a development inventory. The 2.15 million ounce figure, while impressive at first glance, should not be treated as a production-ready asset. It represents an exploration target that requires substantial additional work before any economic assessment can be conducted.

What This Deal Reveals About the Broader Junior Mining Landscape

The pattern established by the Goldsky Agnico Barsele deal is one that is likely to repeat across the sector. Major gold producers are operating in an environment where capital discipline and shareholder returns have become paramount, and maintaining a portfolio of non-core, pre-development assets consumes management bandwidth and balance sheet capacity without near-term payoff.

Junior operators with focused regional mandates, strong local geological expertise, and access to the TSXV capital markets are structurally well-suited to take on these assets. They can move faster, allocate capital more intensively to a single project, and tolerate the long timelines that exploration advancement requires without the earnings pressure that a major producer faces.

The deal structure itself, where a major retains a meaningful equity stake and a perpetual royalty, has become a template for managing this transition in a way that preserves optionality for both parties. Agnico Eagle's formal announcement confirms this structured approach: Agnico loses the operational overhead but gains leveraged exposure to Barsele's upside through its 32% Goldsky stake and a royalty that will generate cash flows if and when the project reaches production.

For investors watching the junior gold space, transactions of this type signal genuine geological endorsement from the vendor. Majors with deep exploration teams and rigorous internal review processes do not retain 32% stakes in projects they consider worthless. The question is not whether Barsele has merit, but whether Goldsky can execute the drilling campaign needed to demonstrate that merit at scale.

This article is for informational purposes only and does not constitute financial or investment advice. All exploration-stage resource figures, financial projections, and market data are subject to change. Investors should conduct their own due diligence and consult a qualified financial adviser before making investment decisions.

Want to Be First When the Next Major ASX Mineral Discovery Hits the Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex geological data into actionable investment insights — the same kind of structural shift driving deals like Goldsky's Barsele acquisition is precisely what creates early-mover opportunities for informed investors. Explore historic discoveries and their remarkable returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.