June 11, 2026

The Silent Bottleneck Threatening America's Electric Vehicle Ambitions

Before a single battery cell rolls off a production line, before an electric vehicle charges at a highway stop, and before a grid-scale storage system absorbs a summer peak load, one material must be present in enormous quantity: graphite. Specifically, processed graphite shaped into anode material capable of storing and releasing lithium ions thousands of times over a battery's working life. It is the most voluminous material in a lithium-ion anode by weight, and yet the United States currently produces none of it domestically from natural sources. Every gram is imported. This is not a minor supply chain footnote. It is a foundational vulnerability sitting at the base of the entire American clean energy transition.

Understanding why the Graphite One Ohio anode plant matters requires grasping the full weight of that dependency, and the structural forces that have made it so difficult to dismantle.

When big ASX news breaks, our subscribers know first

Why Graphite Scarcity Is the Battery Industry's Most Underappreciated Problem

Public discourse around battery supply chains tends to fixate on lithium, cobalt, or nickel. These are important materials, but graphite operates at a different scale entirely. A typical lithium-ion battery cell contains roughly 10 times more graphite by weight than lithium. In a 100 kWh EV battery pack, this can translate to over 50 kilograms of anode-grade graphite per vehicle. At projected EV production volumes, the arithmetic becomes staggering.

The U.S. Geological Survey confirms that the United States is 100% import-dependent for natural graphite, a situation with no parallel among comparably critical battery materials. The global graphite shortage is further compounded by the fact that China controls approximately 80% of global graphite supply, encompassing not just mining but also the downstream processing, purification, and shaping of graphite into the specific particle geometries that battery manufacturers require.

"This is not merely a mining story. China's dominance extends to the finishing and coating stages of anode production, meaning that even companies with access to raw graphite ore outside China often still route their material through Chinese processing facilities before it becomes battery-ready."

This processing dependency is what makes anode material manufacturing so strategically significant. It is not enough to mine graphite. The material must be spheronized, purified to battery-grade carbon levels, and in many cases coated with carbon precursors to improve cycle life. Each step requires specialised equipment, chemistry, and process knowledge currently concentrated in China.

What the Graphite One Ohio Anode Plant Is Actually Building

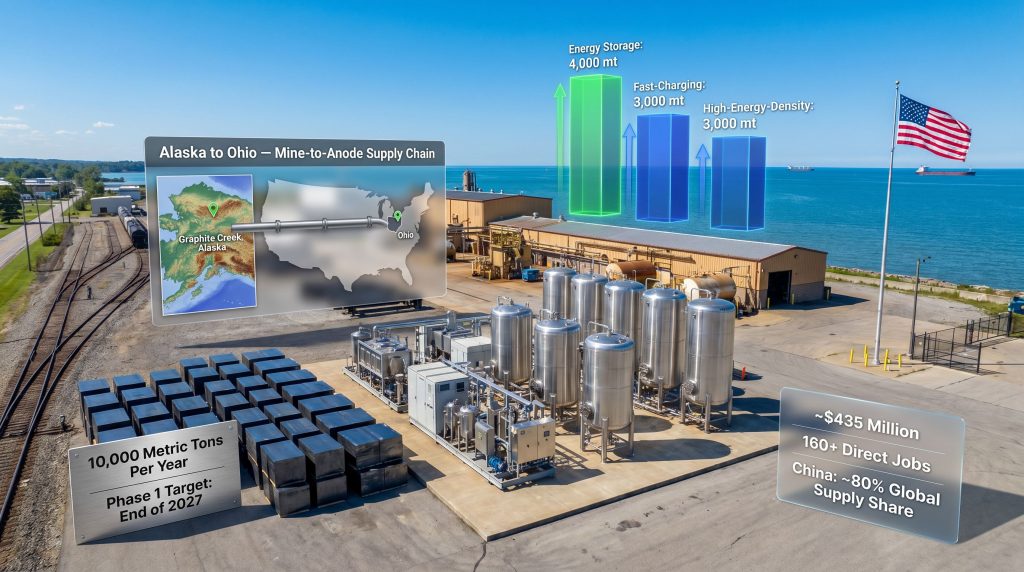

Graphite One Inc. has secured an industrial site in Conneaut, Ohio, a northeastern town situated on the southern shoreline of Lake Erie, approximately 65 miles northeast of Cleveland. The land will be leased from the Bessemer and Lake Erie Railroad Company, a subsidiary of Canadian National Railway, under a 50-year lease arrangement with a purchase option attached.

The site selection followed the abandonment of a previously planned location near Warren, Ohio. That decision was driven by a practical but consequential obstacle: the Warren site lacked the electrical infrastructure required to support three-phase anode material processing at commercial scale. Upgrading the grid connection would have introduced timeline risk that threatened the company's 2027 delivery targets. The Conneaut site resolved this immediately, with an existing on-site electrical substation already capable of supporting industrial-scale operations.

Why Infrastructure Logistics Define Competitive Position

The Conneaut site's advantages extend well beyond electricity. Furthermore, the combination of rail, water, and land assets creates a logistics platform that few alternative sites could replicate:

| Infrastructure Asset | Operational Significance |

|---|---|

| On-site electrical substation | Eliminates grid upgrade delays critical to 2027 timeline |

| Canadian National Railway multi-line access | Enables bulk inbound feedstock and outbound product movement |

| Lake Erie and Great Lakes shipping corridor | Opens water-based logistics for large volume material transport |

| Expandable land footprint | Supports multi-phase scaling without site relocation |

| Proximity to Midwest auto manufacturing | Roughly 65 miles from Cleveland's industrial corridor |

This kind of brownfield-adjacent industrial positioning is increasingly recognised as a key competitive differentiator. Greenfield sites with no existing power, rail, or water access can add years to permitting and commissioning timelines, costs that compound quickly at the capital intensity of battery materials processing.

A Three-Phase Production Architecture: From Synthetic Finishing to Full Vertical Integration

The Graphite One Ohio anode plant is designed to scale in three distinct phases, each building on the last while introducing new feedstock capabilities.

Phase 1: Synthetic Graphite Finishing — Is the 2027 Target Achievable?

The initial phase focuses on finishing and blending synthetic graphite sourced from external suppliers. The facility will process 10,000 metric tons per year of synthetic graphite input and convert it into three specialised anode product categories:

- 4,000 metric tons of energy storage material, targeting grid-scale and stationary battery applications

- 3,000 metric tons of fast-charging material, engineered for high-rate lithium intercalation demanded by performance EV platforms

- 3,000 metric tons of high-energy-density material, designed for data centre uninterruptible power systems and advanced EV applications

The distinction between these three product types is technically meaningful. Fast-charging graphite requires specific particle size distributions and surface structures that allow lithium ions to enter and exit the anode rapidly without causing structural degradation. High-energy-density material prioritises maximum lithium storage capacity per unit volume. Producing these as discrete, application-specific products rather than a generic anode blend reflects growing battery manufacturer sophistication in specifying their input materials.

Phase 2: Capacity Expansion (Target: End of 2028)

The second phase scales total processing throughput to 25,000 metric tons per year, representing a 2.5x increase from the Phase 1 baseline. This expansion is anticipated to be achieved through equipment additions at the Conneaut site, leveraging the scalability built into the land footprint from the outset. Consequently, the phased approach allows each stage of investment to be validated before committing capital to the next.

Phase 3: Natural Graphite Integration from Alaska (Target: 2030)

The third and most transformative phase ties the Ohio processing facility to the Graphite Creek mine in Alaska, currently described as the largest known graphite deposit in the United States. Upon completion, this integration would enable the Ohio plant to source its primary feedstock domestically, replacing or significantly supplementing imported synthetic graphite with mined and beneficiated natural graphite from American soil.

Long-term production capacity under this fully integrated model is targeted at up to 175,000 metric tons per year, establishing what would be the largest domestic graphite anode supply chain in U.S. history. Graphite One's bankable feasibility study underpins this long-range production vision with detailed technical and financial analysis.

"The shift from synthetic to natural graphite feedstock in Phase 3 is commercially significant beyond supply security. Natural graphite, when produced at scale, typically carries lower energy costs than synthetic graphite, which requires high-temperature furnacing of petroleum coke or coal tar pitch. This could improve the facility's cost position relative to Chinese competitors over time."

The Synthetic vs. Natural Graphite Distinction: Why It Matters to Battery Makers

Many observers treat graphite as a monolithic commodity. In practice, battery manufacturers distinguish sharply between synthetic and natural graphite anodes, and increasingly between different particle morphologies within each category. This nuance is increasingly reflected in how the battery raw materials market is evolving, with buyers specifying anode inputs with far greater precision than in previous years.

| Characteristic | Synthetic Graphite | Natural Graphite |

|---|---|---|

| Primary feedstock | Petroleum coke or coal tar pitch | Mined graphite ore |

| Production energy intensity | Very high (Acheson furnace process) | Moderate (beneficiation and purification) |

| Purity consistency | Highly controlled | Deposit-dependent, requires sorting |

| Performance profile | Excellent rate capability, high purity | Cost-competitive, good energy density |

| Current U.S. availability | Importable but costly | 100% import-dependent |

| Graphite One strategy | Phases 1 and 2 primary input | Phase 3 integration from Graphite Creek |

Synthetic graphite currently dominates premium EV battery applications because of its consistency and high purity, often exceeding 99.95% carbon. However, it is energy-intensive to produce, which inflates both cost and carbon footprint. Natural graphite, once properly spheronized and purified, offers a lower-cost alternative with an improving sustainability profile, particularly when the mining and processing occur within a single domestic supply chain.

Customer Engagement: Six Major Players in Specification Testing

Perhaps the most commercially significant detail in the current project status is the engagement of six major industry participants in active specification testing of commercial-grade anode material samples. This group spans three major EV manufacturers and three leading lithium battery companies.

It is worth understanding what specification testing actually involves in this context. Battery manufacturers do not simply accept anode material that meets a generic purity threshold. They conduct rigorous electrochemical characterisation, including:

- Half-cell and full-cell cycle testing to assess capacity retention over hundreds of charge-discharge cycles

- Rate capability testing to evaluate performance at different charge speeds

- First-cycle efficiency measurement, a critical metric that determines how much lithium is permanently consumed on initial charge

- Particle morphology analysis to ensure consistency with existing electrode manufacturing processes

- Tap density and BET surface area measurement for electrode coating compatibility

Passing this gauntlet across six companies simultaneously is a significant undertaking. No binding offtake agreements have been publicly confirmed, and investors should treat customer engagement as a commercial validation signal rather than a revenue guarantee. However, simultaneous multi-party specification testing of this scale is not routine, and it reflects meaningful interest from the demand side of the market.

The next major ASX story will hit our subscribers first

The Capital Commitment and Economic Footprint

Phase 1 capital investment is estimated at approximately $435 million, with direct job creation of more than 160 positions at the Conneaut facility. Construction commencement remains contingent on financing completion, making capital raise milestones a key leading indicator for project advancement. Graphite One's $435 million Ohio investment has drawn considerable attention given the scale of the domestic manufacturing commitment it represents.

| Project Metric | Current Status or Target |

|---|---|

| Site location | Conneaut, Ohio (Lake Erie shoreline) |

| Lease counterparty | Bessemer and Lake Erie Railroad Co. |

| Phase 1 output | 10,000 mt/y synthetic graphite processing |

| Phase 2 output | 25,000 mt/y |

| Phase 3 output | Up to 175,000 mt/y with Alaskan natural graphite |

| Phase 1 capital estimate | ~$435 million |

| Direct employment | 160+ positions |

| Phase 1 target date | End of 2027 |

| Customer engagement | 6 major EV and battery companies in specification testing |

Risk Factors Investors and Industry Observers Should Monitor

The Graphite One Ohio anode plant carries a layered risk profile that reflects the complexity of building a novel industrial supply chain from scratch. However, understanding these risks in the context of broader critical minerals demand helps frame the strategic imperative that underpins the project despite its challenges.

- Financing risk remains the most immediate variable. Without completed funding, construction cannot begin, and the 2027 timeline compresses quickly once groundbreaking is delayed.

- Feedstock sourcing risk in Phases 1 and 2 depends on reliable access to synthetic graphite from non-Chinese suppliers, a market that is itself constrained.

- Technology execution risk around the finishing and coating processes must be managed as the facility scales from pilot to commercial volumes.

- Market timing risk is real. EV demand trajectories have proven difficult to forecast accurately, and battery chemistry is evolving, with some next-generation chemistries potentially altering the graphite anode's role.

- Geopolitical risk cuts both ways: US critical minerals tariffs could accelerate domestic procurement mandates, or could shift in ways that alter competitive dynamics for imported alternatives.

"The project's phased structure creates strategic optionality, allowing each stage to be validated before full capital commitment to the next. However, it also means that delays compound across phases. A slip in Phase 1 financing pushes Phase 2 expansion, which delays Phase 3 integration with Graphite Creek, extending the timeline to full vertical integration."

In addition, the emergence of competing domestic anode projects and the ongoing evolution of battery recycling expansion as a secondary source of battery-grade graphite could reshape the long-term supply landscape in ways that are difficult to predict at this stage.

Frequently Asked Questions: Graphite One Ohio Anode Plant

Where is the Graphite One Ohio anode plant located?

The facility is planned for Conneaut, Ohio, on the southern shore of Lake Erie, approximately 65 miles northeast of Cleveland. The site will be leased from the Bessemer and Lake Erie Railroad Company, a subsidiary of Canadian National Railway.

What products will the plant manufacture?

The Conneaut plant will produce three categories of battery anode material: energy storage graphite for grid applications, fast-charging graphite for high-performance EV batteries, and high-energy-density graphite for data centre and advanced EV uses.

When is Phase 1 expected to begin operations?

Phase 1 operations are targeted for the end of 2027, subject to financing completion and related construction milestones.

How does this project reduce U.S. dependence on Chinese graphite?

By establishing domestic finishing and blending capacity in Phase 1, then integrating Alaskan natural graphite in Phase 3, the project aims to create a fully domestic supply chain from mine to finished anode material, eliminating the need for Chinese processing intermediaries.

Has Graphite One secured customers?

Six major industry participants, including three EV manufacturers and three battery companies, are conducting specification testing on commercial-grade samples. No binding offtake agreements have been publicly disclosed at this stage.

What a Domestic Graphite Anode Industry Means for U.S. Energy Security

The absence of a domestic graphite anode industry is not simply an economic inefficiency. It represents a structural dependency that touches national defence readiness, grid resilience, and the credibility of the entire domestic EV manufacturing buildout. Battery factories without secure anode supply are assembly operations dependent on foreign goodwill.

Ohio's position within the Great Lakes industrial corridor adds geographic logic to the project's location. The region's existing heavy industrial infrastructure, rail networks, and proximity to Midwest automotive manufacturing clusters creates a natural gravitational centre for battery materials processing. The Rust Belt reinvention narrative has real industrial substance in this context, not just political symbolism.

Whether the Graphite One Ohio anode plant achieves its full potential will ultimately depend on execution across financing, construction, customer conversion, and the successful development of the Graphite Creek mine in Alaska. Each of those milestones carries uncertainty. What is not uncertain is the scale of the gap the project is attempting to fill, and the strategic importance of filling it.

This article contains forward-looking statements and projections based on publicly available information. Construction timelines, production capacities, and capital estimates are subject to change based on financing outcomes, regulatory approvals, and market conditions. This content does not constitute financial advice. Readers should conduct independent due diligence before making investment decisions.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial today to position yourself ahead of the broader market.