July 28, 2026

The Processing Bottleneck Nobody Talks About: Why Refining Graphite Is Harder Than Mining It

Battery supply chains have a hidden vulnerability that rarely makes headlines. While lithium, cobalt, and nickel dominate critical minerals conversations, graphite quietly underpins every lithium-ion battery cell in production today. A single electric vehicle battery pack requires roughly 70 to 100 kilograms of graphite — more by weight than any other battery mineral. Yet the vast majority of the world's capacity to convert raw graphite into the ultra-pure, precisely shaped particles that battery manufacturers actually need sits inside a single country's borders.

That concentration is now forcing a fundamental rethink of how Western nations approach battery materials. The answer, increasingly, is not to build entirely new facilities from the ground up, but to find smarter, faster, and more capital-efficient pathways to processing capacity. The International Graphite European JV with Alkeemia, formalised through a binding joint venture agreement in May 2026, represents precisely that kind of strategic thinking in action.

When big ASX news breaks, our subscribers know first

Understanding the Graphite Processing Gap: Why Purification Is the Real Prize

There is a common misconception that graphite is simply mined, concentrated, and shipped to battery factories. The reality involves a technically demanding transformation that most Western nations currently lack the industrial capacity to perform at scale. Furthermore, the global graphite shortage has amplified pressure on governments and investors alike to accelerate solutions beyond simple resource extraction.

Natural graphite deposits produce flake graphite after mining and flotation processing. However, battery manufacturers require spherical purified graphite (SPG), a product that demands micronisation (grinding flakes into precise particle sizes), spheroidisation (shaping particles into spheres to optimise packing density in anodes), and chemical purification to achieve carbon purity levels above 99.95%. Some processes push purity requirements even higher, to 99.99% or beyond, depending on the battery chemistry involved.

Each of these steps carries significant technical complexity:

- Purification typically involves either thermal treatment at temperatures exceeding 2,500°C, or chemical purification using hydrofluoric acid (HF) as the primary reagent.

- Particle sizing must be tightly controlled, as inconsistent particle distributions directly degrade battery capacity and cycle life.

- Coating with carbon materials (typically pitch-based) is often required to improve electrochemical performance and reduce first-cycle lithium loss.

China currently controls an estimated 70 to 80% of global graphite processing capacity, according to data widely cited across industry and government sources. This concentration is not accidental. It reflects decades of investment in integrated processing infrastructure, cheap energy, and accumulated technical expertise. Replicating that outside China is neither quick nor cheap — which is why the brownfield co-location model pioneered by the International Graphite and Alkeemia joint venture deserves close attention.

What the International Graphite and Alkeemia JV Actually Involves

The Ownership Architecture: Equity Control vs. Economic Participation

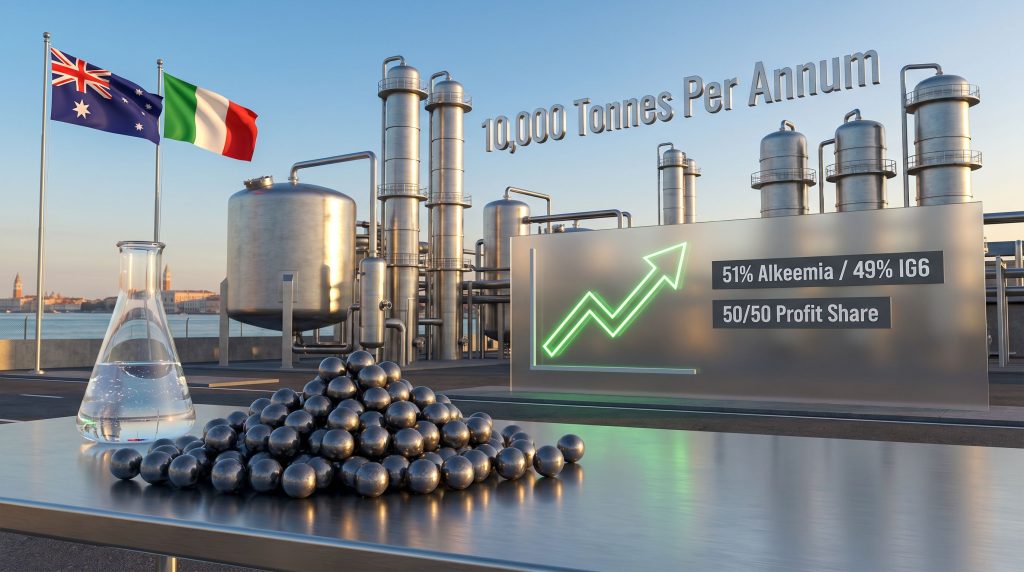

The binding joint venture, executed in May 2026, structures ownership with Italian chemical company Alkeemia S.p.A. holding 51% and ASX-listed International Graphite (IG6) holding 49%. Importantly, profit distribution is structured on a 50/50 basis, creating a deliberate separation between equity control and economic participation.

This asymmetric but economically balanced structure is increasingly favoured in cross-border critical minerals partnerships for several reasons:

- It gives the European partner operational and regulatory primacy, which can simplify workforce integration and permit approvals in EU jurisdictions.

- It reassures local stakeholders, including governments and communities, that the project is not simply a foreign-controlled extraction play.

- It preserves the upstream partner's full economic stake, ensuring International Graphite captures equal value from the facility's output despite holding the minority equity position.

"The 51/49 split with equal profit-sharing is a carefully engineered governance mechanism. Majority control sits with the party best positioned to navigate European regulatory and operational environments, while economic exposure remains perfectly balanced."

Porto Marghera: Why Location Is a Competitive Advantage, Not Just a Detail

The facility will be developed within Alkeemia's existing operational precinct at Porto Marghera, an industrial zone on the western edge of the Venice Lagoon in northern Italy. This is not a greenfield site selected for proximity to ore. It is an active chemical manufacturing hub with a history stretching back to the early twentieth century, originally developed as part of Italy's industrial expansion programme.

What Porto Marghera offers the JV is substantial:

- Existing laboratory facilities capable of supporting process development and quality assurance.

- Warehousing and logistics infrastructure already connected to European rail and road networks.

- An experienced chemical processing workforce familiar with regulated industrial operations.

- Construction equipment and services already mobilised on-site, reducing capital requirements.

- Established environmental compliance and permitting frameworks that apply to the existing facility.

The site's northern Italian location also positions the facility within relatively close reach of Europe's growing battery manufacturing cluster, which spans regions of Germany, Hungary, Poland, Sweden, and northern France. In addition, this positioning directly strengthens Europe's critical minerals supply chain, offering a credible non-Chinese processing alternative at the heart of the continent.

Alkeemia's Chemical Expertise: The Hidden Strategic Advantage

Alkeemia is recognised as one of Europe's significant producers of hydrofluoric acid, a highly corrosive and technically demanding chemical that happens to be one of the primary reagents in chemical graphite purification processes. This is not a coincidental alignment.

HF-based purification offers certain processing advantages over thermal purification, including lower energy consumption and the ability to operate at lower temperatures. However, it requires strict safety controls, specialist handling infrastructure, and robust environmental management systems — all of which Alkeemia has already established through its existing operations.

For International Graphite, this means the JV is not starting from zero on the chemical processing side. It is grafting a new graphite processing operation onto a partner that already understands the safety, regulatory, and operational demands of working with the exact reagents the process requires.

Greenfield vs. Brownfield: Why the Development Model Matters to Investors

The choice of development pathway has enormous implications for both timeline and capital efficiency. The table below illustrates how the Porto Marghera brownfield approach compares with alternative models.

| Development Approach | Capital Cost Profile | Estimated Lead Time | Infrastructure Risk | Regulatory Complexity |

|---|---|---|---|---|

| Greenfield standalone facility | High | 4 to 7 years | High | High |

| Brownfield co-location (JV model) | Significantly reduced | 2 to 4 years | Low to Medium | Reduced via existing permits |

| Toll processing arrangement | Low upfront | Near-term | Low | Minimal |

| Integrated mine-to-product model | Very high | 5 to 10 years | Very high | Very high |

The brownfield co-location model compresses both cost and timeline by leveraging infrastructure that would otherwise represent years of capital expenditure and permitting effort. For a junior ASX-listed developer, the ability to enter European graphite processing without bearing the full burden of greenfield construction is a meaningful structural advantage.

Production Targets and Expansion Pathway

The initial facility is designed to produce approximately 10,000 tonnes per annum (tpa) of processed graphite. To contextualise this figure:

- A single large-scale European gigafactory producing cells for EV and stationary storage applications can consume tens of thousands of tonnes of battery-grade graphite annually.

- Europe's total battery manufacturing capacity is projected to scale dramatically through the late 2020s and into the 2030s, with multiple gigafactories either under construction or in advanced planning across the continent.

- At 10,000 tpa, the initial Porto Marghera facility represents a meaningful but clearly early-stage contribution to regional supply.

"A 10,000 tpa processing facility is not a solution to Europe's graphite deficit on its own. Its strategic value lies in what it enables next: a funded, operational platform from which capacity can be expanded using JV-generated cash flows, without requiring constant equity dilution from the parent companies."

The expansion model, funded through JV operating cash flows rather than external capital raises, is particularly notable. It suggests a self-compounding growth dynamic if the facility achieves commercial production and secures long-term offtake agreements, consequently allowing capacity to scale without proportionate increases in capital risk.

From LOI to Binding JV: The Staged Partnership Timeline

The International Graphite European JV with Alkeemia relationship did not materialise overnight. It followed a deliberate staged progression that is worth understanding as a template for how serious cross-border critical minerals JVs are constructed:

- Letter of Intent (December 2025): The initial framework agreement between the two parties, establishing mutual interest and broadly outlining the commercial structure.

- Memorandum of Understanding (March 2026): A deeper commitment that validated technical and commercial feasibility, including preliminary site assessments and processing pathway analysis.

- Binding Joint Venture Agreement (May 2026): The transition from exploratory framework to legally committed partnership, with defined ownership, profit-sharing, and governance structures.

Each stage required both parties to commit additional resources and demonstrate deeper alignment before proceeding. This staged approach reduces the risk of misaligned expectations and provides natural exit or renegotiation points if circumstances change.

The next major ASX story will hit our subscribers first

International Graphite's Broader Strategic Position

From Australian Miner to Integrated Producer

International Graphite (ASX: IG6) holds an advanced graphite project in Western Australia that has been described as one of Australia's largest graphite deposits by resource scale. The European JV transforms the company's strategic profile in a meaningful way. For context, the broader Australian graphite industry has been grappling with the challenge of moving beyond raw resource extraction, making this downstream integration particularly significant.

Prior to the JV, International Graphite's value proposition rested primarily on its upstream resource position: a large deposit of natural graphite in a Tier 1 mining jurisdiction. That is a solid foundation, but it is also one shared by multiple ASX-listed graphite developers. The addition of a binding European processing JV introduces a differentiated downstream capability that most peers cannot match.

The value chain progression this enables looks roughly as follows:

- Mining and concentration in Western Australia, producing flake graphite concentrate.

- Shipping of concentrate to Porto Marghera via existing European logistics networks.

- Processing and purification at the Alkeemia facility, producing battery-grade spherical purified graphite.

- Sale and delivery to European battery manufacturers seeking non-Chinese supply.

This end-to-end structure, if fully realised, repositions International Graphite from a single-jurisdiction miner into an integrated graphite business with a dual-geography revenue base.

The EU Policy Environment and Regulatory Backdrop

What the Critical Raw Materials Act Means for Graphite Developers

The European Union's Critical Raw Materials Act (CRMA), which came into force in 2024, established binding targets for the EU to produce, process, and recycle specified critical minerals domestically. Graphite is formally designated as a strategic material under the CRMA framework.

The regulation sets a target for the EU to process at least 40% of its annual consumption of strategic raw materials domestically by 2030. For graphite, this represents an enormous gap relative to current EU processing capacity, which is negligible compared to demand projections driven by battery manufacturing expansion.

It is important to note that the CRMA creates a regulatory and policy environment that favours European graphite processing projects broadly. Whether any individual project qualifies for specific funding instruments, accelerated permitting, or financial support under EU mechanisms such as the European Investment Bank or Important Projects of Common European Interest (IPCEI) depends on project-specific criteria and application processes that have not been confirmed for this JV at this stage.

EU Battery Regulation: A Commercial Driver Beyond Policy

Beyond the CRMA, the EU Battery Regulation introduced mandatory carbon footprint declarations for EV and industrial batteries, phasing in from 2025 onwards. This regulation creates a commercial incentive for battery manufacturers to source graphite processed within Europe or in jurisdictions with lower carbon processing profiles.

Graphite processed using Chinese thermal purification methods carries a substantially higher carbon footprint than material processed using chemical methods or powered by lower-emission energy sources. European battery manufacturers seeking to comply with carbon footprint thresholds have a direct commercial reason to source locally processed graphite, independent of any geopolitical considerations. Furthermore, innovations such as the development of a recycled graphite product are also beginning to reshape how battery manufacturers think about sourcing diversification.

Risk Framework: What Investors Should Monitor

No early-stage JV is without execution risk. The following scenario framework captures the range of plausible outcomes.

Scenario A: Accelerated Execution

Offtake agreements secured within 12 months, final investment decision (FID) reached on schedule, construction commences. International Graphite establishes a first-mover position in European graphite processing among ASX-listed peers.

Scenario B: Delayed Commercial Agreements

Offtake negotiations extend beyond 18 months, pushing FID and construction timelines. Execution risk increases but the strategic rationale remains intact. Capital may need to be deployed to maintain momentum.

Scenario C: EU Policy Acceleration

New EU funding mechanisms or incentive frameworks specifically targeting graphite processing are confirmed and accessible to qualifying projects, improving project economics and potentially compressing the timeline to commercial production.

Key risk factors investors should track independently include:

- Progress on offtake negotiations and the identity and credit quality of potential customers.

- Capital cost estimation outcomes from the detailed engineering phase.

- Graphite price dynamics, particularly for battery-grade SPG in European spot and contract markets, as tracked in the broader battery raw materials market.

- Regulatory developments in the EU affecting battery material sourcing requirements.

- Execution by both JV parties on the agreed development roadmap.

This article is for informational purposes only and does not constitute financial or investment advice. Investors should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. Forward-looking statements and scenario projections involve inherent uncertainty and should not be relied upon as forecasts of actual outcomes.

Frequently Asked Questions: International Graphite European JV with Alkeemia

What is the International Graphite and Alkeemia JV?

A binding joint venture between ASX-listed International Graphite (ASX: IG6) and Italian chemical company Alkeemia S.p.A. to develop a graphite processing facility at Porto Marghera near Venice, Italy. Alkeemia holds 51% equity and International Graphite holds 49%, with profits distributed on a 50/50 basis. The full details of this agreement have been outlined by International Graphite's Managing Director Andrew Worland.

Why is Porto Marghera significant as a processing location?

Porto Marghera is an established industrial chemical precinct in northern Italy with existing laboratory facilities, workforce, warehousing, and logistics infrastructure. Co-locating within this active site substantially reduces the capital cost and development timeline compared to building a standalone greenfield facility.

Why is Alkeemia strategically important beyond providing the site?

Alkeemia is one of Europe's significant hydrofluoric acid producers. HF is a primary reagent in chemical graphite purification, meaning Alkeemia brings directly relevant technical capability, safety infrastructure, and regulatory compliance frameworks to the partnership.

What is the planned initial production capacity?

The initial facility targets approximately 10,000 tonnes per annum of processed graphite, with expansion intended to be funded through JV operating cash flows as the business scales.

What are the next milestones for the JV?

Current workstreams include detailed site infrastructure planning, capital cost estimation, and advancing commercial offtake discussions with potential European customers. These activities are expected to progress toward a final investment decision.

How does this JV fit into the broader graphite supply chain?

It connects International Graphite's Australian upstream resource with European chemical processing expertise, creating a pathway from raw flake graphite concentrate to battery-grade spherical purified graphite delivered to European battery manufacturers.

Want To Stay Ahead Of The Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex mineral data into actionable insights for both traders and long-term investors. Explore how major mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.