July 23, 2026

When Regulatory Ambition Collides With Market Reality

The global automotive industry spent much of the past decade constructing elaborate roadmaps toward full electrification, driven by regulatory pressure, investor sentiment, and a collective assumption that consumer demand would follow policy leadership. That assumption has proven far more fragile than anticipated. The gap between government-mandated timelines and the actual purchasing behaviour of mainstream consumers has widened considerably, exposing a structural tension that is now reshaping corporate strategy at the highest levels of the industry.

When one of Japan's most storied automakers dismantles commitments that once defined its entire forward trajectory, it signals more than a single company's miscalculation. It reflects a broader reckoning with how quickly the EV transition was expected to move, and how different the reality has turned out to be. Honda pulls back from EVs due to consumer trends — and that decision is now made concrete.

When big ASX news breaks, our subscribers know first

Honda's Historic Financial Loss and the Collapse of an EV Roadmap

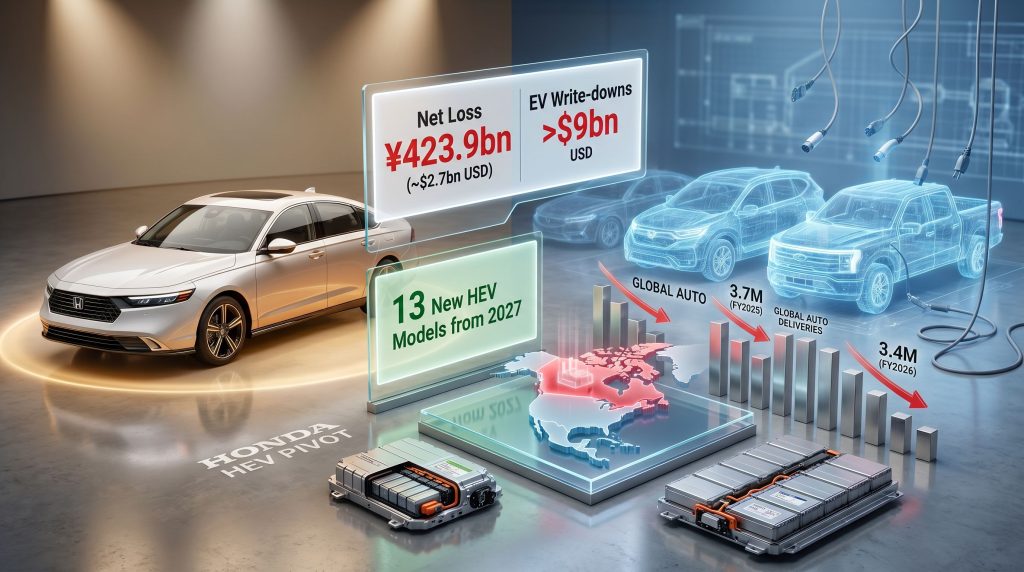

For any company to abandon targets it publicly championed is uncomfortable. For Honda to do so while simultaneously reporting its first annual net loss since the company listed on public markets in 1957 makes the reversal historically significant. The financial year ended March 2026 produced a net loss of ¥423.9 billion (approximately $2.7 billion USD), with more than $9 billion in EV-related write-downs and restructuring charges tied to cancelled or deferred electrification initiatives.

The scale of that write-down reveals just how deeply Honda had committed capital to a BEV future that the market was not yet ready to absorb. Global automobile deliveries fell to 3.4 million units in FY2026, down from 3.7 million units in FY2025, a year-on-year decline of roughly 8% driven by weakening EV demand and intensifying competition, particularly from Chinese manufacturers in Asia.

Against that backdrop, Honda's leadership took the decisive step of abandoning two cornerstone targets:

- The commitment for EVs to represent 20-30% of global vehicle sales by 2030

- The pledge to sell exclusively battery electric and fuel-cell vehicles by 2040

In place of these technology-specific commitments, Honda shifted toward a framework centred on total lifecycle CO₂ emission reductions across its entire fleet. This is not a semantic difference. By measuring emissions across a vehicle's full life rather than mandating a specific technology mix, Honda gains enormous flexibility. It can deploy hybrids, fuel-cell vehicles, and battery EVs in proportions that reflect actual consumer demand rather than predetermined quotas, and still demonstrate progress toward emissions reduction goals.

| Financial Metric | FY2026 Result |

|---|---|

| Net loss | ¥423.9bn (~$2.7bn USD) |

| EV write-downs and restructuring | >$9bn USD |

| Global vehicle deliveries | 3.4mn units |

| Prior year deliveries (FY2025) | 3.7mn units |

| Year-on-year volume decline | |

| Total investment cut (to FY2031) | From ~$69bn to ~$48bn USD |

The Consumer Demand Shortfall Nobody Wanted to Acknowledge

Understanding why Honda pulls back from EVs due to consumer trends requires looking honestly at the structural gap between policy-designed adoption curves and what buyers across North America and Europe have actually been willing to do. Several interconnected forces have suppressed mainstream EV uptake well below what earlier projections assumed.

What Is Keeping Mainstream Buyers Away From EVs?

Range anxiety and charging infrastructure remain binding constraints in suburban markets. In Honda's core North American geography, characterised by sprawling suburban communities with limited public transit and long commuting distances, access to reliable fast-charging infrastructure continues to fall short of what is needed to make BEV ownership a practical first-choice decision for average households.

Price sensitivity has not been adequately addressed. Entry-level battery electric vehicles continue to command a meaningful premium over comparable hybrid or internal combustion alternatives. For cost-sensitive buyers, particularly in the post-pandemic environment of elevated interest rates and compressed household budgets, that price gap remains a decisive deterrent.

Hybrids have emerged as the pragmatic middle ground. Rather than waiting for BEV economics to improve, a large segment of consumers in the US and other mature markets has gravitated toward hybrid vehicles, which offer genuine fuel efficiency gains without the infrastructure dependency that full EVs require. This is not consumer resistance to electrification per se; it is consumer preference for electrification on terms that work within existing infrastructure realities.

Energy cost differentials explain much of the geographic variation in EV adoption. At the FT Future of the Car Summit in May 2026, Benjamin Kreiger, Secretary-General of the European Association of Automotive Suppliers (Clepa), identified charging cost as perhaps the single most powerful driver of consumer vehicle choice. In China, electricity costs for EV charging run at approximately 3 cents per kWh. On European highways, drivers face costs of 70 to 80 cents per kWh. That differential does not merely affect total cost of ownership; it shapes the psychological calculus of whether an EV feels economically rational at the point of purchase.

"The energy cost asymmetry between markets is a critically underappreciated variable in EV demand forecasting. A technology that is genuinely cost-competitive in Shanghai may remain economically marginal in Stuttgart or suburban Ohio under entirely different energy pricing regimes."

Geopolitical Disruption and the Regulatory Instability Factor

Honda's head of government affairs, Patrick Keating, speaking at the FT Future of the Car Summit on 14 May 2026, identified the geopolitical environment as a compounding factor that made rigid technology-specific targets increasingly untenable. His assessment centred on the idea that the regulatory frameworks underpinning 2035 ICE phase-out timelines and ZEV mandates were constructed in a fundamentally different geopolitical moment.

Since those targets were established, the automotive industry has confronted:

- The economic and supply chain disruption associated with the Ukraine conflict

- A significant shift in US federal policy toward EV mandates and associated incentive structures following the post-2024 administration change

- Active reconsideration of EU CO₂ fleet targets under growing cost-competitiveness pressure from Asian manufacturers

- Uncertainty surrounding the UK's ZEV mandate trajectory as energy cost pressures reshape political priorities

This regulatory instability does not invalidate the long-term case for electrification, but it fundamentally undermines the ability of corporate planners to commit tens of billions of dollars to irreversible technology infrastructure on the basis of rules that may shift before the investment matures. Honda's own announcement made clear that this uncertainty played a central role in the company's decision to restructure its forward capital allocation.

The Hybrid Pivot: 13 New Models and a Redefined Competitive Position

Rather than retreating from electrification entirely, Honda is repositioning hybrid technology as the commercial centrepiece of its near-to-medium-term strategy. The company has confirmed plans to launch 13 new hybrid electric vehicle (HEV) models from 2027 onward, with North America as the primary target market given its demonstrated preference for hybrid powertrains over full BEVs.

Honda's ambition is to double its hybrid sales volume by 2030, leveraging a technology base the company has developed and refined over decades through platforms including the Civic Hybrid, Accord Hybrid, and CR-V Hybrid.

| Hybrid Strategy Element | Detail |

|---|---|

| New HEV models planned | 13 from 2027 onward |

| Primary target market | North America |

| Hybrid sales growth target | Double by 2030 |

| Cancelled BEV models | Honda 0 SUV, Honda 0 Saloon, Acura RSX |

| Long-term BEV re-entry | Conditional on demand recovery |

The commercial logic behind this pivot is grounded in several structural advantages Honda possesses in the HEV space that it does not yet command in full BEV production:

- Lower capital intensity relative to full BEV platform development and battery manufacturing build-out

- Compatibility with existing manufacturing infrastructure, reducing retooling costs and timeline risk

- Stronger consumer acceptance across price-sensitive segments in Honda's core markets

- Reduced exposure to battery raw material supply chain volatility, particularly lithium, cobalt, and nickel price fluctuations

- Proven technology reliability, critical for maintaining the brand trust Honda has built in markets like the US and Japan

Furthermore, Forbes coverage of Honda's strategy shift highlights how the company's hybrid pivot bucks the prevailing industry narrative in a manner that other western OEMs are watching closely.

At the same time, industry observers note a genuine long-term risk in this approach. Matias Giannini, Chief Executive of Horse Powertrain, observed at the FT Future of the Car Summit that the cost of developing proprietary EV technologies may no longer be viable for many western manufacturers, who could ultimately find themselves dependent on off-the-shelf technology from competitors. This raises an important strategic question: by prioritising hybrids now, Honda may be preserving near-term profitability while conceding ground on the EV technology learning curve that will define competitive positioning in the 2030s.

The Canada EV Value Chain: $11 Billion in Suspended Ambition

Perhaps the most concrete expression of Honda's original EV commitment was its planned C$15 billion (approximately $11 billion USD) integrated EV value chain project in Canada, announced in April 2024. This initiative was designed to establish a fully vertically integrated North American EV supply chain, encompassing:

- EV assembly facilities

- Battery cell manufacturing capacity

- Battery material processing operations

The strategic intent was to reduce Honda's dependence on Asian battery suppliers while anchoring a significant share of its North American EV production in Canada.

| Timeline Event | Date |

|---|---|

| Project announced | April 2024 |

| First delay (two years) due to weaker demand | May 2025 |

| Indefinite suspension confirmed | May 2026 |

The indefinite suspension of this project carries implications that extend well beyond Honda's own balance sheet. Battery material processing and cell manufacturing facilities of this scale represent anchor demand for critical mineral supply chains, including lithium, cobalt, nickel, and graphite. Their absence removes a significant forward demand signal from the North American battery materials ecosystem.

The next major ASX story will hit our subscribers first

How Critical Mineral Markets Are Affected

The shift from BEV to HEV as Honda's primary technology focus has measurable downstream consequences for battery material demand, and the mechanism is rooted in a stark difference in energy storage requirements between vehicle types.

A typical hybrid battery pack carries between 1 and 2 kWh of capacity. A typical full BEV battery pack carries between 60 and 100+ kWh. That means Honda's strategic pivot away from BEV production represents a per-vehicle reduction in battery material consumption of between 30 and 100 times, depending on the specific models compared.

Which Materials Face the Greatest Demand Impact?

The materials most directly affected include:

- Lithium (carbonate and hydroxide): Reduced BEV production volumes compress near-term demand, compounding existing lithium oversupply challenges that have already weighed heavily on the sector

- Cobalt and Nickel: Cancelled battery manufacturing commitments, particularly the Canada project, remove contracted forward demand, worsening the cobalt demand outlook for producers

- Graphite: Battery anode demand growth moderates in line with slower BEV ramp-up timelines, adding to existing graphite supply pressures across the supply chain

These developments sit within a broader context of slowing critical minerals demand tied to the energy transition, where OEM strategy reversals are creating genuine uncertainty for project developers and investors across the battery raw materials market.

Disclaimer: Battery material demand projections are inherently forward-looking and subject to revision based on evolving OEM strategies, technology developments, and macroeconomic conditions. The analysis above reflects directional trends rather than precise forecasts.

Adding a further layer of complexity, export restrictions on critical raw materials are tightening globally. According to OECD research published in April 2026, there has been a five-fold increase in export restrictions on critical materials since 2009. As of 2024, these restrictions cover up to 70% of global cobalt and manganese exports, 47% of graphite, and 45% of rare earth elements. Revenue generation drove nearly half of all new restrictions introduced in 2024, a notable shift from the earlier industrial policy rationale. This supply-side constraint compounds the demand-side uncertainty created by OEM strategy reversals like Honda's.

The Chinese Competitive Pressure: A Structural Asymmetry

While Honda recalibrates toward hybrids, Chinese automakers are accelerating in precisely the direction Honda is retreating from. China accounted for approximately 40% of global EV exports in 2024, shipping roughly 1.25 million electric vehicles to international markets. BYD alone delivered more than 4.5 million vehicles globally in 2025, combining battery electric and plug-in hybrid models at price points that western manufacturers have struggled to match.

China's approach to EV adoption offers a striking contrast to Europe's regulatory-driven model. Rather than restricting ICE vehicles through mandates, China combined industrial subsidies, state-backed supply chain investment, domestic competition, and export strategy to build globally competitive EV manufacturers. The result is an industry that produces cheaper, higher-specification vehicles at scale, supported by charging infrastructure with electricity costs that make EV operation genuinely compelling for consumers.

This asymmetry creates a compounding strategic dilemma. Honda's hybrid pivot is rational within the context of its current cost structure and market positioning. However, each year that passes without meaningful BEV volume production widens the technology and manufacturing experience gap relative to Chinese competitors who are scaling BEV and PHEV production simultaneously.

Markets Where EV Momentum Remains Intact

Honda's experience should not be read as evidence that the EV transition is fundamentally broken. The most instructive counterpoint comes from Australia, where EV market penetration reached 14.6% of new vehicle sales in March 2026 and 16.4% in April 2026, compared with just 7.5% and 5.9% respectively in the same months a year earlier, according to the Federal Chamber of Automotive Industries.

Australia's federal government extended its fringe benefits tax exemption for EVs through March 2027, a policy decision that combined with rising fuel costs to accelerate adoption. The Australian data illustrates a critical nuance: EV demand is not uniformly weak. It is highly sensitive to the combination of energy pricing, infrastructure availability, fiscal incentives, and fuel cost volatility.

Markets where these variables align favourably continue to show strong adoption momentum. Markets where they do not, particularly suburban North America, have stalled. Europe's 2035 ICE phase-out remains the baseline regulatory trajectory, preserving long-term EV demand pull across the region's major automotive markets despite near-term uncertainty.

In the UK, moreover, moves to de-link electricity pricing from international gas markets — including reforms to fixed-price contracts for low-carbon generators — are aimed at making EV ownership more economically predictable for consumers, though the effectiveness of these measures remains to be demonstrated.

What Would Bring Honda Back to Battery EVs?

Honda has not described its retreat as permanent. The company has framed BEV re-entry as conditional on changed market circumstances rather than foreclosed entirely. Based on the reasoning articulated through its leadership, the conditions most likely to trigger renewed BEV investment include:

- Recovery of EV demand growth rates in the US market to levels that justify platform investment

- Battery cell cost reductions sufficient to enable profitable EV pricing at volume without subsidy dependence

- Regulatory clarity across the EU, UK, and North America that allows long-horizon capital allocation decisions

- Charging infrastructure density improvements in Honda's suburban North American core markets

- Stabilisation of the competitive cost gap relative to Chinese OEM production economics

Whether those conditions converge within a timeframe that allows Honda to re-enter the BEV market with proprietary technology, rather than relying on externally sourced platforms, is the central strategic question facing the company over the next five years.

Key Takeaways for Investors and Industry Observers

Honda pulls back from EVs due to consumer trends in a way that represents a confluence of financial, consumer, regulatory, and competitive forces that no single factor can adequately explain. Several implications deserve particular attention:

- The shift from technology-specific sales targets to lifecycle CO₂ frameworks gives OEMs greater compliance flexibility but reduces the clarity of forward EV demand signals for battery material markets

- The indefinite suspension of the Canadian EV value chain project removes a significant source of forward investment in North American battery manufacturing and material processing

- Per-vehicle battery material consumption drops dramatically when production shifts from BEV to HEV, with hybrids using 30 to 100 times less battery capacity than full electric vehicles

- Export restrictions on critical minerals are tightening globally just as OEM demand signals are becoming less certain, creating a period of elevated uncertainty for battery supply chain participants

- Markets with aligned policy, infrastructure, and energy pricing continue to demonstrate strong EV adoption, suggesting the technology is viable but the enabling conditions are unevenly distributed

Consequently, Honda's experience serves as a broader warning to the industry: the path to electrification is not linear, and the assumption that regulatory ambition automatically translates into consumer behaviour has proven, in this instance, to be deeply flawed.

This article is intended for informational purposes only and does not constitute financial advice. Figures, statistics, and company announcements referenced herein are drawn from Argus Media reporting dated May 2026 and associated source materials. Forward-looking statements involve inherent uncertainty and should not be relied upon as predictions of future outcomes.

Want To Catch The Next Major Mineral Discovery Before The Market Does?

While Honda's retreat from EVs reshapes battery material demand across lithium, cobalt, nickel, and graphite, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — explore historic examples of major discovery returns or begin your 14-day free trial today to position yourself ahead of the market.