June 21, 2026

The Geometry of Vulnerability: How Gulf Oil Infrastructure Was Built Around a Chokepoint

Energy infrastructure, by its nature, reflects the geopolitical assumptions of the era in which it was built. For decades, the Gulf's producing nations developed export systems oriented almost entirely toward a single maritime corridor. That corridor, the Strait of Hormuz, stretches just 21 nautical miles at its narrowest navigable point, yet it functions as the central artery of global petroleum trade. When regional conflict intensifies around that passage, the limits of that infrastructure design become impossible to ignore.

The question facing energy markets today is not simply whether Middle East oil producers bypassing the Strait of Hormuz is theoretically possible, but whether the existing bypass architecture is robust enough, geographically safe enough, and operationally reliable enough to absorb a serious disruption. The honest answer, based on current infrastructure data, is: partially, and at significant cost. Furthermore, understanding oil's global importance helps contextualise just how consequential any disruption to this corridor truly is.

When big ASX news breaks, our subscribers know first

How Much Oil Actually Moves Through Hormuz?

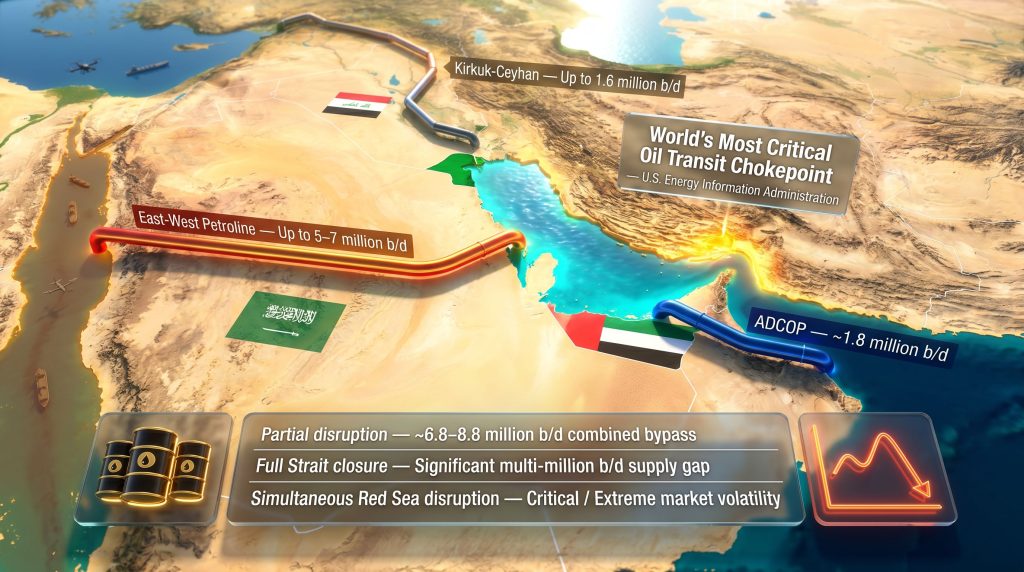

The U.S. Energy Information Administration has consistently identified the Strait of Hormuz as the world's most critical oil transit chokepoint. Approximately 20 to 21 million barrels per day of crude oil, condensate, refined products, and natural gas liquids typically transit the strait, representing roughly one-fifth of global petroleum consumption and close to one-third of all seaborne oil trade.

Six of the world's most significant hydrocarbon producers depend on Hormuz as their primary export channel: Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, Iran, and Qatar. Qatar's liquefied natural gas exports add another layer of strategic exposure, as the country routes nearly all of its LNG shipments through the passage. No other single waterway concentrates this volume or degree of continental energy dependency in such a narrow geographic space.

The asymmetry is stark. If Hormuz is disrupted, replacement supply cannot simply be rerouted at scale. The combined bypass infrastructure across the entire Gulf region covers, at best, roughly half of normal Hormuz throughput — and that estimate assumes every pipeline is operating at full design capacity simultaneously, which has never been the case in practice.

A Data-Driven View of Bypass Capacity Across the Gulf

The table below maps the key bypass routes currently available across Middle East producing nations, including their design capacities, destination ports, and primary vulnerabilities.

| Bypass Route | Country | Estimated Capacity (b/d) | Destination Port | Key Vulnerability |

|---|---|---|---|---|

| East-West Petroline | Saudi Arabia | Up to 5–7 million | Yanbu (Red Sea) | Pumping stations, Houthi threat |

| ADCOP Pipeline | UAE | ~1.5–1.8 million | Fujairah (Gulf of Oman) | Within range of regional weapons systems |

| Kirkuk-Ceyhan Pipeline | Iraq | Up to 1.6 million (operating well below capacity) | Ceyhan, Turkiye | Political instability, chronic underutilisation |

| Kurdistan-Turkey Section | Iraq (Kurdistan) | Up to 250,000 | Ceyhan, Turkiye | Minimal recent volumes |

| Goreh-Jask Pipeline | Iran | Limited operational capacity | Gulf of Oman | Sanctions, infrastructure constraints |

| Trucking via Syria | Iraq | ~150,000 | Overland | Uneconomical at scale |

| Trucking via Turkey | Iraq | ~40,000 | Overland | Uneconomical at scale |

| Iraq-Jordan Agreement | Iraq | ~10,000 | Jordan | Suspended since February, recently renewed |

When combined, the theoretical maximum across all these routes sits somewhere between 6.8 and 8.8 million barrels per day — a figure that falls far short of the 20-plus million barrels that normally flow through the strait. This gap is the central strategic problem.

Saudi Arabia's East-West Pipeline: The Region's Largest But Most Exposed Bypass Asset

Saudi Arabia's East-West Petroline runs from the kingdom's oil-producing heartland in the Eastern Province westward to the Red Sea export terminal at Yanbu. The pipeline carries up to seven million barrels per day in transport capacity, with up to five million barrels per day available for actual export from Yanbu, according to analysis from the International Crisis Group.

On paper, this makes it the most significant bypass asset in the region by a considerable margin. In practice, however, its value is constrained by three intersecting problems.

Is the East-West Petroline Truly Secure?

First, the infrastructure itself is vulnerable. Whilst the pipeline is buried underground for much of its route, the facilities surrounding it are not. Production facilities that feed crude into the system, pumping stations distributed along the corridor, and the terminal infrastructure at Yanbu all represent targetable components. The strategic exposure of each is distinct:

- Production facilities feeding the pipeline are geographically dispersed but share proximity to established conflict zones

- Pumping stations are distributed along the pipeline route and represent discrete, identifiable targets

- Terminal facilities at Yanbu concentrate export operations into a single geographic point on the Red Sea coast

A pumping station strike attributed to Iranian forces in early April temporarily knocked out approximately 700,000 barrels per day of throughput, demonstrating that the vulnerability is not theoretical. Consequently, this has drawn significant attention to the oil price shock implications now rippling through energy markets.

Second, Saudi Arabia's customer base creates a routing problem. The majority of the kingdom's crude is sold to buyers in East Asia. Red Sea cargoes heading to those destinations must travel south, passing through the Bab al-Mandeb Strait, where Houthi forces in Yemen retain the capability to target commercial shipping. This means the Red Sea bypass route runs directly into a secondary threat environment, compounding rather than resolving the risk.

Third, the northern alternative is constrained. Cargoes can be rerouted north through the Suez Canal and the SUMED pipeline toward Mediterranean markets, but this corridor cannot accommodate the full volume the East-West Petroline is capable of delivering. It is a partial relief valve, not a full solution.

The UAE's Fujairah Terminal: Geographic Positioning and Its Limits

The Abu Dhabi Crude Oil Pipeline (ADCOP), often referred to as the Habshan-Fujairah pipeline, was specifically engineered to provide the UAE with a Hormuz-independent export capability. It connects onshore production facilities to the Fujairah terminal, which sits on the Gulf of Oman coastline east of the strait, allowing up to 1.5 to 1.8 million barrels per day to bypass Hormuz entirely.

Fujairah's geographic positioning is genuinely advantageous in a partial disruption scenario. Tankers loading at Fujairah never enter the strait at all, removing one layer of risk from the logistics chain. However, the terminal's location outside the strait does not place it outside the range of regional weapons systems.

Analysis from conflict monitors indicates that Fujairah has sustained multiple strikes during the current conflict period, including one attack timed around an attempted U.S.-facilitated shipping corridor operation. Furthermore, the UAE has reportedly moved to accelerate pipeline investment in response to these vulnerabilities. Wood Mackenzie's analysis confirms that whilst the UAE can meaningfully bypass Hormuz, the volumes achievable through Fujairah represent a reduction from pre-conflict export baselines.

Iraq's Structural Bypass Underperformance

Iraq presents a different kind of problem. Its primary bypass infrastructure, the Kirkuk-Ceyhan pipeline running northward to the Turkish port of Ceyhan, has a design capacity of 1.6 million barrels per day but has chronically operated well below that ceiling. Political fragmentation between the federal government in Baghdad and the Kurdistan Regional Government, combined with periodic pipeline sabotage and unresolved revenue-sharing disputes, has kept actual throughput consistently depressed.

A March 2026 agreement opened the Kurdistan section of the Iraq-Turkey pipeline to a potential 250,000 barrels per day of federal Iraqi crude, but recent operational volumes have remained smaller than that figure. The overland trucking alternatives available to Iraq further illustrate the gap between theoretical and practical bypass options:

| Overland Route | Estimated Volume | Viability Assessment |

|---|---|---|

| Trucking via Syria | ~150,000 b/d | Limited by conflict exposure and infrastructure quality |

| Trucking via Turkey | ~40,000 b/d | Uneconomical at any meaningful scale |

| Iraq-Jordan Pipeline Agreement | ~10,000 b/d | Recently renewed after February suspension |

These figures confirm what energy analysts have long observed: overland trucking of crude oil is a last-resort mechanism, not a scalable bypass strategy. In addition, the trade war impact on oil market price impact has made these operational inefficiencies even more financially consequential for Iraq's export revenues.

The next major ASX story will hit our subscribers first

Kuwait and Iran: Two Opposite Ends of the Bypass Spectrum

Of the major Gulf producers, Kuwait has no meaningful pipeline bypass capability. All of its crude exports depend on Hormuz transit. This structural exposure makes Kuwait the most vulnerable major producer to any prolonged disruption of the strait, and analysis from the International Crisis Group confirms it has experienced the sharpest proportional export impact from the current conflict environment.

Iran occupies a different position — not because it has functional bypass infrastructure, but because it has been attempting to circumvent what is described as a U.S. naval blockade through vessel deception tactics rather than pipeline rerouting. According to reporting from the International Crisis Group, these efforts achieved limited success during the initial phase of the blockade but subsequently declined in effectiveness for crude oil.

Iran's Goreh-Jask pipeline, designed to route crude to the Gulf of Oman coast south of Hormuz, remains operationally constrained by sanctions and infrastructure limitations. Iran's rail export corridor to China remains active but faces challenges related to capacity and geopolitical utility versus commercial viability.

The Red Sea as an Export Corridor: Risk Stratification in Practice

The security picture in the Red Sea cannot be reduced to a simple safe or unsafe binary. According to analysis from the International Crisis Group, risk tolerance and actual transit behaviour vary significantly by vessel type, flag state, and the commercial or geopolitical affiliations of the shipping company involved.

Russian and Chinese-affiliated carriers have navigated the Red Sea with relatively few reported incidents, whilst many Western-linked operators continue to avoid the route. This divergence creates a two-tier shipping market with meaningful price implications for different grades and origins of crude.

Even during periods when Houthi forces have not been actively targeting commercial vessels, the residual probability of resumed attacks has been sufficient to keep overall Red Sea transit volumes suppressed relative to pre-October 2023 baselines. The market is pricing in tail risk, not just current operational conditions.

Bulk carriers have returned to the route more quickly than very large gas carriers (VLGCs), reflecting differences in cargo value, insurance availability, and replacement cost calculations. Wood Mackenzie analysts have noted that the Red Sea has so far remained a viable export route but stress that security risks persist, particularly at the Bab al-Mandeb Strait. Moreover, the LNG supply outlook for the region remains deeply uncertain given these compounding route vulnerabilities.

Scenario Analysis: What the Numbers Look Like Under Different Disruption Conditions

| Scenario | Available Bypass Capacity | Estimated Supply Gap | Market Price Impact |

|---|---|---|---|

| Partial disruption (reduced tanker traffic) | ~6.8–8.8 million b/d combined | Moderate | Elevated freight premiums |

| Full Strait closure (no tanker transit) | ~6.8–8.8 million b/d combined | Significant multi-million b/d shortfall | Severe price spike potential |

| Simultaneous Red Sea disruption | Severely constrained | Critical | Extreme market volatility |

Strategic petroleum reserves held by IEA member countries provide a short-term buffer in disruption scenarios, but their duration is finite. The IEA's coordinated reserve release mechanism is designed for weeks, not months. A prolonged closure that persisted beyond the buffer window would require structural market adjustment, contributing further to crude oil volatility across global markets.

Frequently Asked Questions: Hormuz Bypass Infrastructure

Can Saudi Arabia Fully Bypass the Strait of Hormuz?

No. Whilst the East-West Petroline can transport up to seven million barrels per day to Yanbu, the Red Sea route those cargoes must take faces its own security threats, and the pipeline's supporting infrastructure remains targetable. The bypass reduces but does not eliminate exposure.

How Much Oil Does the UAE Export Through Fujairah Instead of the Strait?

The ADCOP pipeline enables up to 1.5 to 1.8 million barrels per day to be exported via Fujairah. This represents a meaningful but partial bypass, and export volumes via this route are lower than the UAE's pre-conflict export baselines.

Which Gulf Country Is Most Vulnerable to a Strait of Hormuz Closure?

Kuwait, which has no pipeline bypass infrastructure and routes all crude exports through the strait, faces the greatest structural exposure of any major Gulf producer.

What Is the Total Bypass Capacity Available Across All Middle East Producers?

Across all routes — including Saudi Arabia's Petroline, the UAE's ADCOP, Iraq's northern pipelines, and minor trucking and overland options — the theoretical combined capacity is approximately 6.8 to 8.8 million barrels per day, well below normal Hormuz throughput of 20 to 21 million barrels per day.

Is the Red Sea a Safe Alternative Export Route for Middle East Oil in 2026?

Safety varies by carrier nationality, vessel type, and cargo. Whilst the route has remained partially operational, the Bab al-Mandeb presents ongoing risk, and overall transit volumes remain below pre-October 2023 levels even during ceasefire periods.

The Structural Conclusion: Bypass Routes Reduce Risk, They Do Not Replace the Strait

The fundamental insight emerging from a full assessment of Gulf bypass infrastructure is that the region's pipeline architecture was never designed to substitute for Hormuz at scale. It was designed to provide optionality — to give producers a partial alternative during brief disruptions rather than a complete replacement corridor during prolonged conflict.

The gap between available bypass capacity and actual Hormuz throughput spans more than 12 million barrels per day under optimistic assumptions. That gap represents the structural ceiling on how much of the world's oil supply can be rerouted if the strait is seriously compromised. Consequently, Middle East oil producers bypassing the Strait of Hormuz at anything approaching full Hormuz volumes remains, for now, an engineering and geopolitical impossibility.

Geopolitical escalation creates a further compounding problem that infrastructure investment alone cannot resolve: the same conflict environment that increases demand for bypass routes simultaneously degrades the safety of those routes. Red Sea threats grow more acute as Gulf tensions rise. Pipeline targets become more attractive as adversaries seek leverage.

For energy markets, this means that the risk premium associated with Hormuz-region disruptions should not be modelled as a simple rerouting problem. It is a systemic exposure question — one in which the backup architecture and the primary corridor share overlapping threat environments rather than being genuinely independent. Understanding that interdependence is the starting point for any serious analysis of Gulf energy security.

This article reflects publicly available analysis and reported data as of May 2026. It does not constitute investment or financial advice. Forward-looking assessments of supply disruption scenarios involve significant uncertainty and should not be relied upon as precise forecasts.

Want to Stay Ahead of the Market Moves Driven by Global Energy Disruptions?

When geopolitical shocks like a Hormuz disruption send commodity prices surging, the investors who act first on significant ASX mineral discoveries stand to gain the most — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those opportunities emerge on the ASX, transforming complex commodity data into clear, actionable insights across more than 30 resources. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.