June 20, 2026

The global hydrogen economy stands at a critical inflection point where multiple technological pathways, policy frameworks, and industrial applications are converging to reshape energy markets fundamentally. Unlike previous commodity cycles driven by supply-demand imbalances, the emerging hydrogen sector represents a structural transformation of industrial processes, creating new demand patterns for critical materials including platinum group metals (PGMs). This convergence creates unprecedented opportunities for strategic positioning across multiple sectors simultaneously, particularly as bullish hydrogen sentiment continues to drive investment flows and policy commitments worldwide.

Strategic Fundamentals Driving Hydrogen Market Evolution

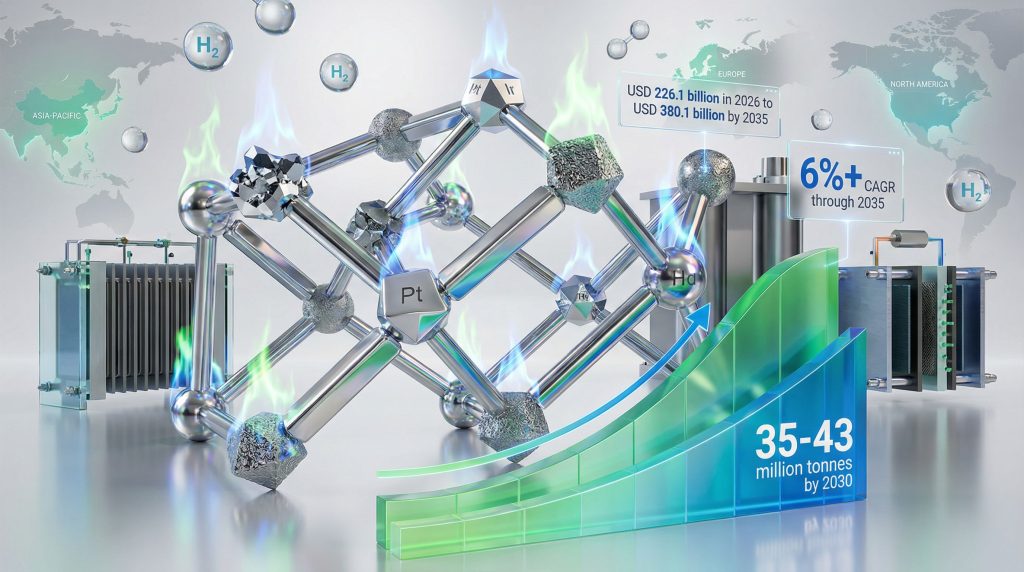

The hydrogen sector's momentum reflects deeper structural shifts beyond traditional energy transition security considerations. Market projections indicate expansion from approximately $226 billion in 2026 to potentially $380 billion by 2035, representing growth rates that suggest fundamental industrial transformation rather than cyclical commodity demand.

Policy Architecture Creating Long-Term Visibility:

- 58 national governments plus EU and ECOWAS implementing comprehensive hydrogen strategies

- Target production of 35-43 million tonnes low-emissions hydrogen by 2030

- Regional blending mandates establishing baseline demand floors

- Investment frameworks providing multi-decade planning horizons

China's Five-Year Plan integration demonstrates how coordinated government action can accelerate market development beyond traditional forecasting models. Furthermore, the strategic classification of hydrogen infrastructure within national industrial policy creates investment certainty that commodity markets typically lack.

European critical minerals policy frameworks establish carbon neutrality mandates by 2050, creating regulatory requirements for hydrogen adoption across multiple industrial sectors. These policy commitments create demand visibility extending decades beyond typical commodity planning horizons.

Technology Deployment Reaching Commercial Scale

Industrial hydrogen applications are transitioning from pilot projects to commercial deployment across multiple sectors simultaneously. Toyota's fuel cell technology utilisation demonstrates scalable commercial viability with 100 grams of platinum per cell in fully industrialised applications.

Northern China's industrial operations showcase immediate commercial hydrogen adoption. Single coking coal companies are deploying 20,000 hydrogen-powered trucks with expansion plans targeting 200,000 units, indicating mass market viability beyond experimental phases.

Green Hydrogen Infrastructure Scaling:

- Global electrolyser capacity expansion from 25 GW annually to 440-690 GW by 2036

- Multiple technology pathways (alkaline, PEM, solid oxide) creating diversified catalyst demand

- Industrial process integration across ammonia, methanol, and specialty chemical production

When big ASX news breaks, our subscribers know first

Regional Market Dynamics Reshaping Global Demand Patterns

Asia-Pacific Industrial Integration Accelerating

China's hydrogen strategy demonstrates how industrial policy coordination can create rapid market development. Northern China's coking coal operations generate grey hydrogen as industrial by-products, providing immediate commercial applications while green hydrogen infrastructure develops.

Asia-Pacific Growth Indicators:

- Regional market growth exceeding 6% compound annual rates through 2035

- China targeting 200,000-tonne production capacity by 2025

- Industrial transport applications achieving immediate commercial viability

- Heavy-duty trucking sector providing early adoption anchors

The integration of hydrogen applications within existing industrial processes creates demand patterns less dependent on standalone infrastructure development. This approach reduces deployment risks while establishing commercial viability across multiple applications.

European Green Transition Implementation

Europe's hydrogen market development reflects aggressive policy implementation rather than natural resource advantages. The EU's 15.3% global market share by 2026 demonstrates how regulatory frameworks can accelerate adoption timelines.

European support for transitional hydrogen technologies creates demand bridges while renewable capacity scales. However, this approach provides market development pathways that don't require simultaneous infrastructure completion across entire value chains, as hydrogen stocks analysis suggests.

North American Infrastructure Development

U.S. solar capacity expansion reaching 131 GW by end-2024 enables cost-competitive electrolysis in high-irradiance regions. This renewable capacity growth provides the foundation for large-scale green hydrogen production without relying on fossil fuel inputs.

North American Applications:

- City bus fleet conversions providing early commercial adoption

- Data centre backup power applications creating diversified demand streams

- Industrial process integration across existing chemical production facilities

Technology Pathways Creating PGM Demand Evolution

Fuel Cell Applications Achieving Market Penetration

Fuel cell vehicle deployment demonstrates scalable platinum utilisation across commercial applications. Chinese heavy transport adoption, with documented deployment of 20,000 hydrogen-powered trucks by single companies, indicates mass market viability beyond pilot programmes.

Toyota's commercialised fuel cell systems utilising 100 grams of platinum per cell represent fully industrialised technology ready for large-scale deployment. Consequently, this technology maturity reduces adoption risks while creating predictable catalyst demand patterns.

Electrolyser Technology Scaling Requirements

Green hydrogen production capacity expansion creates significant catalyst loading requirements across multiple technology pathways. Each electrolyser technology utilises different PGM combinations, creating diversified demand streams through renewable energy transformations.

| Technology Type | PGM Requirements | Scaling Timeline | Commercial Status |

|---|---|---|---|

| Alkaline Electrolysers | Ruthenium-based catalysts | Immediate deployment | Commercially available |

| PEM Electrolysers | Iridium anodes, platinum cathodes | Rapid expansion phase | Industrial scaling |

| Solid Oxide Systems | Platinum-based electrodes | Development to commercial | Emerging deployment |

Industrial Process Integration Expanding

Chemical process applications create diversified PGM demand streams less dependent on transportation sector adoption rates. Ammonia production, methanol synthesis, and specialty chemical manufacturing utilise hydrogen across established industrial processes.

This industrial integration provides market stability by distributing hydrogen demand across multiple sectors with different adoption timelines and risk profiles.

Investment Positioning Framework for PGM Market Evolution

Portfolio Diversification Strategy Analysis

Historical PGM demand concentration in autocatalyst applications created vulnerability to electric vehicle substitution. In addition, hydrogen applications offer portfolio rebalancing opportunities across multiple industrial sectors with different risk characteristics.

Demand Evolution Scenarios:

- 1990s Industrial Applications: 8-9 million ounce market across multiple sectors

- Peak Autocatalyst Period: 19 million ounce market with concentrated sector risk

- Projected Diversified Future: 12-13 million ounce baseline plus hydrogen growth opportunities

The return to diversified industrial applications reduces single-sector dependency while maintaining significant market scale. This diversification creates more stable long-term demand patterns, as evidenced by recent bullish hydrogen sentiment emerging in PGM industry discussions.

Technology Partnership Value Creation

Strategic alliances between PGM producers and technology companies accelerate application development timelines significantly. Research partnerships can reduce technology validation periods from traditional ten-year cycles to six-month development processes.

Partnership Benefits:

- Shared development risk across multiple technology pathways

- Accelerated testing and validation through combined resources

- Market access via established industrial relationships

- Portfolio approach reducing single-application dependencies

Strategic Scenario Planning Requirements

High Adoption Scenario: Rapid policy implementation, technology cost reduction, and coordinated infrastructure development create 15%+ annual market growth through 2035.

Moderate Growth Scenario: Steady industrial adoption with transport sector development following infrastructure availability, supporting consistent demand growth.

Delayed Implementation Scenario: Technology competition, infrastructure delays, and policy inconsistencies slow market development to sub-5% annual growth rates.

Market Development Challenges and Risk Assessment

Infrastructure Coordination Requirements

Hydrogen market success depends on simultaneous development across production, storage, transportation, and end-use applications. Unlike traditional commodity markets, hydrogen requires coordinated investment across entire value chains, reflecting broader geopolitical mining trends.

Critical Infrastructure Dependencies:

- High-pressure storage and transportation networks

- Industrial-scale electrolyser manufacturing capacity

- Fuel cell production scaling for commercial deployment

- Grid integration systems for renewable-powered electrolysis

Technology Competition and Market Substitution

Battery technology advancement creates competitive pressure in transportation applications while direct electrification may capture some industrial processes. Investment positioning must account for technology substitution risks across different time horizons.

Competitive Technology Factors:

- Battery energy density improvements affecting transport applications

- Direct electrification economics in industrial heating processes

- Alternative catalyst development reducing PGM requirements

- Process efficiency improvements changing demand calculations

Project Execution and Market Development Risks

Large-scale hydrogen project delays highlight execution challenges in coordinated infrastructure development. Middle East project cancellations and postponements demonstrate risks in ambitious development timelines.

Electrolyser overcapacity in some regions indicates supply-demand timing mismatches that create short-term market volatility despite long-term growth fundamentals.

The next major ASX story will hit our subscribers first

Long-Term Market Transformation Implications

Structural Demand Pattern Evolution

The hydrogen economy represents a fundamental shift from concentrated autocatalyst demand to diversified industrial applications. This transformation recreates the multiple-use market structure existing before automotive applications dominated PGM consumption, reflecting broader mining industry evolution.

Historical analysis indicates that diversified industrial demand provided more stable long-term growth patterns compared to single-sector concentration. The projected return to this market structure offers improved risk-adjusted returns.

Investment Timeline and Market Development

Hydrogen market development operates on extended timelines compared to traditional commodity cycles. Short-term volatility should be expected while medium-term fundamentals remain robust, with significant long-term optionality for strategically positioned market participants.

Timeline Considerations:

- Short-term (1-3 years): Policy implementation and infrastructure development creating market volatility

- Medium-term (3-10 years): Technology scaling and commercial deployment establishing demand patterns

- Long-term (10+ years): Structural market transformation creating sustained industrial demand

The convergence of policy support, technology maturation, and industrial adoption creates compelling investment positioning opportunities for hydrogen-exposed PGM demand, despite execution risks and competitive pressures across different application sectors.

For instance, the hydrogen economy's development represents more than cyclical commodity demand expansion. It creates fundamental restructuring of industrial processes, energy systems, and materials utilisation patterns that extend across multiple decades of market evolution, establishing a foundation for sustained bullish hydrogen sentiment among investors and industrial participants alike.

Ready to Capitalise on the Next Major PGM Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant platinum group metals and critical minerals discoveries across the ASX, empowering investors to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial at Discovery Alert today and position yourself strategically for the emerging hydrogen economy transformation.