May 13, 2026

The Chokepoint Economy: How One Waterway Determines Whether the World Runs Out of Oil

Energy markets operate on a fundamental assumption that rarely gets tested in full: that the physical infrastructure connecting production to consumption will remain functional. Pipelines, terminals, tanker routes, and processing facilities are so deeply embedded in global trade architecture that their disruption is treated as a tail risk rather than a planning scenario. That assumption has now collapsed entirely.

The Iran war's impact on the Strait of Hormuz has transformed a theoretical vulnerability into an active, measurable catastrophe for global oil supply. The IEA Iran war oil supply deficit, as documented in the agency's May 2026 monthly oil market report, is already being described as the most severe supply shock in the history of modern energy markets, surpassing even the crises that previously defined the outer boundary of what analysts considered possible.

Understanding the full scope of this disruption requires examining not just the headline deficit figures, but the structural, geographic, and economic mechanisms that are simultaneously compressing supply and destroying demand in ways that compound each other.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: Geography as Destiny

The Strait of Hormuz is a narrow maritime passage connecting the Persian Gulf to the Gulf of Oman, flanked by Iran to the north and Oman and the UAE to the south. At its narrowest point, it spans approximately 33 kilometres, with navigable shipping lanes occupying only a fraction of that width.

Under normal operating conditions, this bottleneck carries more than 20% of globally traded oil and liquefied natural gas, according to the IEA's May 2026 assessment. That figure represents the combined export volumes of Saudi Arabia, the UAE, Kuwait, Iraq, Iran, and Oman, plus a substantial portion of Qatar's LNG output. Furthermore, LNG supply pressures from the region have compounded the overall energy crisis.

The geographic reality is stark: there is no fully functioning alternative. The East-West pipeline across Saudi Arabia and the Abu Dhabi Crude Oil Pipeline provide partial bypass capacity, but neither has the throughput to absorb anything close to full Hormuz-equivalent volumes at the speed required to offset a sudden blockade.

When tanker traffic through Hormuz became severely restricted as a result of the Iran war conflict, the consequences were not gradual. They were immediate, simultaneous, and cascading across multiple producer nations at once.

From 20 Million to 3.8 Million Barrels Per Day: The Blockade's Immediate Arithmetic

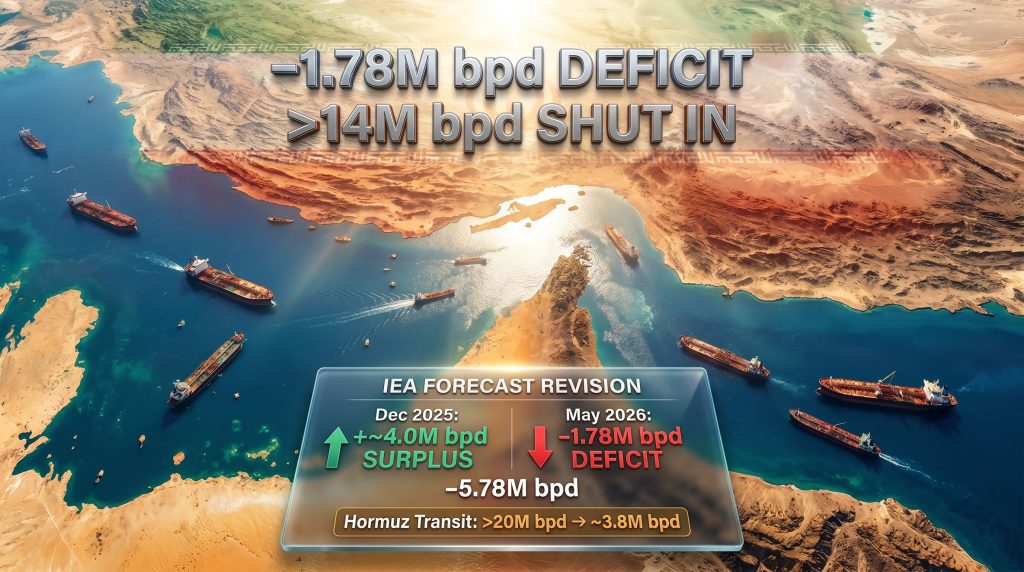

The reduction in Hormuz throughput from over 20 million barrels per day under normal conditions to approximately 3.8 million barrels per day following restrictions represents an 81% collapse in the world's most consequential energy corridor. This is not a partial disruption. It is a near-total functional closure of the passage that determines energy availability for a significant portion of the global economy.

For Asia-Pacific importers, the impact is asymmetric and severe. Nations including Japan, South Korea, India, and China rely on Gulf crude for a substantial share of their refinery feedstock. With alternative supply sources unable to compensate at scale or at competitive cost, these economies face simultaneous refinery throughput reductions, energy price inflation, and industrial slowdowns.

Europe and other importing regions face parallel pressures, though their existing diversification toward Atlantic Basin, North Sea, and African supply sources provides marginally more buffer. However, the critical point is that no region is insulated from a disruption of this magnitude.

IEA Iran War Oil Supply Deficit: The Scale of the Forecast Reversal

The IEA Iran war oil supply deficit assessment is not merely an update to a standing forecast. It represents one of the most consequential single-period revisions the agency has made in its operational history, driven by the speed at which conflict conditions overrode all pre-existing supply-demand modelling assumptions.

From Comfortable Surplus to Historic Deficit: The Forecast Progression

Three data points trace the trajectory:

| Forecast Period | Supply-Demand Balance | Global Supply Change | Global Demand Change |

|---|---|---|---|

| December 2025 | +~4.0M bpd surplus | +1.1M bpd growth | +640K bpd growth |

| April 2026 | +410K bpd surplus | -1.5M bpd | -80K bpd |

| May 2026 | -1.78M bpd deficit | -3.9M bpd | -420K bpd |

| Net Swing | -5.78M bpd total | -5.0M bpd revision | -1.06M bpd revision |

Source: International Energy Agency Oil Market Reports, December 2025 through May 2026 (as reported by Reuters/Economic Times Energy, May 13, 2026)

The most striking element of this table is not any single figure, but the velocity of the revision. In five months, the global oil market went from an expected comfortable cushion of nearly 4 million barrels per day to a structural shortfall of 1.78 million barrels per day. That is a 5.78 million bpd swing in market balance, a number that dwarfs previous inter-year forecast adjustments.

Why the Magnitude of This Revision Is Without Modern Precedent

The IEA's assessment characterises the current supply shock as unprecedented in scale, with cumulative losses exceeding 1 billion barrels and more than 14 million barrels per day of Gulf production shut in simultaneously.

To contextualise this figure: the 1973 Arab oil embargo removed an estimated 4 to 5 million barrels per day from global markets over a period of several months, triggering the worst energy crisis of the 20th century. The current disruption involves more than 14 million barrels per day of shut-in production, representing a magnitude more than three times larger. The cumulative loss crossing 1 billion barrels marks a threshold that no previous energy disruption has reached in comparable timeframes.

This comparison matters not just for historical context, but because the 1973 crisis fundamentally restructured global energy policy, created the IEA itself, and permanently altered how governments think about energy security. Consequently, the current disruption is, by measurable production loss metrics, structurally larger.

The Base-Case Assumption and What It Requires to Be True

The IEA's May 2026 base-case forecast projects a gradual resumption of Hormuz tanker traffic beginning in Q3 2026. This assumption underpins the 1.78 million bpd deficit figure. If traffic resumes more slowly, or does not resume at all within the calendar year, the deficit deepens materially.

For the base case to materialise, the following conditions must emerge:

- Active hostilities in and around Hormuz must reduce sufficiently to allow commercial vessel navigation

- Insurance markets must re-designate tanker routes as insurable at workable premiums

- Gulf producer port infrastructure must be operational or repaired to loading capacity

- Diplomatic engagement between relevant parties must produce at minimum a de-escalation framework

None of these conditions currently exist simultaneously, which is why the IEA classifies this as a projection and not a certainty.

The Dual-Sided Shock: Why Demand Is Also Collapsing

Most major oil supply disruptions affect the supply side alone. Demand remains relatively inelastic in the short term, and price spikes, while painful, are absorbed by economies that have no immediate alternative to petroleum-based energy.

The Iran war disruption is structurally different because it operates on both sides of the ledger simultaneously. In addition, the broader context of oil market disruptions from earlier geopolitical shocks has left markets with fewer buffers to absorb this compounded pressure.

Price-Induced Demand Destruction: The Feedback Mechanism Explained

The IEA now forecasts a decline of 420,000 barrels per day in global oil consumption across 2026, revised sharply downward from a previous forecast of an 80,000 bpd decline. This marks the first year-on-year contraction in oil demand since the COVID-19 pandemic, according to the May 2026 report.

The channels through which elevated oil prices destroy demand include:

- Refinery feedstock shortages in Asia-Pacific, forcing processing facilities to reduce throughput or idle entirely when crude inputs become unavailable or prohibitively expensive

- Industrial and manufacturing slowdowns, where energy-intensive sectors curtail production as input costs exceed viable margins

- Fertiliser and agricultural supply chain disruptions, as natural gas price increases cascade into production cost increases for nitrogen-based fertilisers, threatening food supply chains in import-dependent nations

- Consumer transport demand compression, where retail fuel prices at structurally elevated levels suppress discretionary vehicle use and commercial transport activity

- Emerging market import cost crises, where nations without adequate foreign reserves or strategic stockpiles face acute shortages as import bills become unsustainable

| Demand Scenario | Previous IEA Forecast | May 2026 Revised Forecast | Magnitude of Shift |

|---|---|---|---|

| 2026 Demand Growth/Decline | -80K bpd decline | -420K bpd decline | -340K bpd additional contraction |

| Last Comparable Demand Decline | n/a | COVID-19 pandemic (2020) | Structural parallel |

| Primary Impact Regions | Global | Middle East, Asia-Pacific | Hormuz-dependent importers |

| Transmission to broader economy | Limited | Inflationary contagion | Global spread via energy costs |

The Economic Slowdown Feedback Loop

The interaction between supply loss and demand destruction creates a self-reinforcing cycle that standard economic modelling struggles to fully capture. When supply is constrained, prices rise. When prices rise above critical thresholds, economic activity contracts. When economic activity contracts, demand falls.

However, when demand falls under these conditions, it does not produce market stabilisation in the typical sense because the supply constraint remains physical, not price-responsive. This means the market cannot clear through normal mechanisms. The deficit persists not because producers are choosing to withhold supply, but because production infrastructure is physically unavailable.

Emergency Response: The 400 Million Barrel Strategic Reserve Release

The IEA coordinated the release of 400 million barrels from member nations' strategic petroleum reserves, representing the largest emergency drawdown in the agency's history, surpassing the coordinated releases that followed Russia's 2022 invasion of Ukraine.

How Strategic Petroleum Reserves Work and Where Their Limits Lie

Strategic petroleum reserves (SPRs) are government-held emergency stockpiles maintained specifically to buffer supply disruptions. Member nations of the IEA are required to maintain reserves equivalent to at least 90 days of net oil imports. These stockpiles are held in physical storage facilities including underground salt caverns, above-ground tankage, and distributed industry-held reserves that count toward national totals.

The critical structural limitation of SPR releases is that they address a stock problem with a flow solution. Releasing reserves temporarily supplements available supply, but reserves are finite and cannot be depleted indefinitely. Once strategic stockpiles fall below minimum threshold levels, the buffer disappears entirely.

A 400 million barrel reserve release, while historically unprecedented in coordination scale, offsets only a fraction of the cumulative supply losses that have already exceeded 1 billion barrels according to the IEA's May 2026 assessment. The arithmetic gap between intervention capacity and actual disruption magnitude reflects the unprecedented scale of the underlying shock.

The Gap Between Intervention and Disruption

To understand the adequacy of the SPR response, consider the following framing:

- Cumulative supply losses confirmed by IEA: exceeds 1 billion barrels

- Emergency reserve release deployed: 400 million barrels

- Coverage ratio: approximately 40% of confirmed cumulative loss

- Ongoing loss rate: more than 14 million barrels per day of shut-in production continuing

At 14 million barrels per day of shut-in production, the entire 400 million barrel release is equivalent to less than 29 days of what is not being produced. This does not make the reserve release ineffective — it provides critical market stabilisation, price signal management, and supply chain continuity for essential sectors. But it cannot resolve a structural deficit of this magnitude. Only the resumption of Hormuz traffic can do that.

Macro-Economic Consequences: How the Deficit Spreads Beyond Oil Markets

Energy Inflation as a Systemic Transmission Mechanism

Energy price inflation does not stay within the energy sector. It transmits across the entire economy through production costs, transportation costs, food costs, and consumer spending compression. Central banks face a structurally impossible scenario: inflation driven by supply-side energy shocks cannot be addressed through demand management tools like interest rate increases without deepening the economic contraction already underway.

This puts monetary policymakers in a position where every available tool either tolerates inflation or accelerates recession, with no neutral option available. Furthermore, the wider context of geopolitical trade tensions is amplifying these pressures across interconnected global supply chains.

Asia-Pacific's Asymmetric Exposure

Asia-Pacific economies face distinctly disproportionate exposure to the IEA Iran war oil supply deficit because their refinery infrastructure was built around Gulf crude grades, their import contracts are weighted heavily toward Middle Eastern supply, and their geographic distance from Atlantic Basin alternatives increases substitution costs.

Nations such as Japan and South Korea, which import the overwhelming majority of their crude oil requirements and have limited domestic production, face the combination of supply unavailability and prohibitive spot market premiums simultaneously. India's rapidly expanding refining sector, which has developed significant capacity around processing heavier Gulf crudes, faces similar feedstock constraints.

Emerging Market Debt Dynamics

For developing economies that lack both domestic production and substantial foreign currency reserves, the current price environment creates balance of payments stress that can escalate rapidly into sovereign debt crises. When energy import bills as a percentage of GDP rise sharply, fiscal space for other government functions contracts, currency reserves deplete, and borrowing costs rise as credit ratings reflect deteriorating external accounts. Al Jazeera's reporting has highlighted how meagre oil buffers in the developing world are intensifying these pressures.

The next major ASX story will hit our subscribers first

Scenario Modelling: Three Pathways for Global Oil Markets

Scenario 1: Gradual Hormuz Resumption (Base Case)

Under the IEA's base case, partial tanker traffic restoration begins during Q3 2026 following some form of de-escalation. Key market characteristics under this scenario:

- The 1.78 million bpd deficit narrows but does not fully close within the calendar year

- Oil prices remain structurally elevated above $100 per barrel through year-end

- Strategic reserve drawdowns continue at a reduced pace as emergency conditions persist

- Demand gradually recovers as price relief materialises in late 2026 or early 2027

- Global supply growth resumes from a significantly lower baseline in 2027

Scenario 2: Prolonged Blockade (Downside Case)

If Hormuz restrictions persist through Q4 2026 without meaningful de-escalation, the market faces a materially worse outcome:

- The deficit deepens beyond the current 1.78 million bpd projection

- Demand destruction accelerates as economic contraction spreads from energy-intensive sectors to broader economic activity

- Emergency reserve capacity approaches structural limits, removing the buffer function

- Oil price volatility increases as the market loses confidence in supply restoration timelines

- Secondary sovereign debt and financial market stress events become increasingly probable in emerging markets

Scenario 3: Diplomatic Breakthrough (Upside Case)

A negotiated framework between the United States and Iran that produces a credible Hormuz reopening commitment would trigger a rapid market repricing:

- Tanker traffic resumes within weeks of a credible agreement

- Surplus conditions could re-emerge by Q1 2027 as shut-in production returns

- A sharp price correction would follow, potentially in a disorderly fashion given the extent of current price elevation

- Energy-dependent fiscal budgets in producer nations would face sudden revenue contractions requiring rapid adjustment

- SPR drawdown programmes would cease and rebuild cycles would begin

The IEA has identified the restoration of normal tanker traffic through the Strait of Hormuz as the single most consequential variable determining which scenario materialises. Importantly, this means that diplomatic signalling, not OPEC market influence or non-OPEC supply additions, has become the primary driver of the 2026 oil price trajectory.

Who Bears the Cost: Differential Stakeholder Impacts

The Asymmetry Between Producers and Consumers

Not all participants in global energy markets suffer equally from the IEA Iran war oil supply deficit. The distributional impact depends heavily on position within the supply chain and geographic proximity to alternative supply sources.

| Stakeholder Category | Primary Impact | Secondary Impact |

|---|---|---|

| Gulf producers | Production revenue loss from shut-in volumes | Long-term market share risk as importers diversify |

| Non-Gulf oil producers (U.S., Canada, Brazil, Norway) | Revenue windfall from elevated prices | Capacity constraints limit full upside capture |

| Asia-Pacific importers | Feedstock shortages and import cost spikes | Industrial competitiveness and GDP growth erosion |

| European importers | Elevated energy costs, some supply diversification buffer | Inflationary pressure and central bank policy dilemmas |

| Emerging market importers | Balance of payments stress, potential sovereign debt pressure | Social stability risks from fuel and food price increases |

| Oil services and tanker companies (non-Gulf routes) | Elevated charter rates for alternative routing | War risk insurance premium increases |

Non-Gulf Producer Windfall Dynamics

For producers outside the Gulf region, the supply deficit represents a significant revenue opportunity. U.S. shale producers, Brazilian offshore operators, Norwegian North Sea fields, and Canadian oil sands operators all benefit from elevated Brent crude benchmarks. However, capacity constraints, production lead times, and infrastructure bottlenecks limit how quickly non-Gulf production can increase to partially compensate for Gulf losses.

This asymmetry explains why price remains elevated even as non-Gulf producers attempt to maximise output. Supply elasticity outside the Gulf is real but insufficient to address a 14 million barrel per day shortfall within any near-term timeframe. The dynamics of oil trade geopolitics continue to play a defining role in how these windfall gains are distributed and reinvested.

Frequently Asked Questions: IEA Iran War Oil Supply Deficit

What is the IEA's current forecast for the global oil supply deficit in 2026?

The IEA's May 2026 monthly oil market report projects that global oil supply will fall approximately 1.78 million barrels per day short of total demand across 2026. This represents a dramatic reversal from a surplus of close to 4 million barrels per day forecast as recently as December 2025, and from a 410,000 bpd surplus projected in the April 2026 report.

How much oil has been shut in as a result of the Iran war?

According to the IEA's May 2026 assessment, more than 14 million barrels per day of Gulf production has been shut in, with cumulative supply losses from the conflict already exceeding 1 billion barrels, a scale the agency characterises as historically unprecedented.

Why is the Strait of Hormuz so critical to global oil supply?

The Strait of Hormuz is the world's most strategically significant maritime energy corridor. Under normal conditions, more than 20% of globally traded oil and liquefied natural gas passes through this passage, representing the combined export volumes of multiple major Gulf producers. The strait's narrow navigable width and lack of equivalent alternative routes means that any sustained restriction creates an immediate, large-scale global supply deficit.

How has the Iran war affected oil demand?

Beyond direct supply losses, the conflict has simultaneously suppressed demand. The IEA now forecasts a contraction of 420,000 barrels per day in 2026 global oil consumption, the first year-on-year decline since the COVID-19 pandemic, driven by price-induced demand destruction, refinery idling across Asia-Pacific, and broader economic slowdown propagating through energy-intensive industries.

What emergency actions has the IEA taken in response?

IEA member nations have collectively released 400 million barrels from strategic petroleum reserves, the largest coordinated emergency drawdown in the organisation's history. While this intervention provides critical short-term market support, it offsets only a portion of cumulative supply losses that have already exceeded 1 billion barrels, and cannot resolve the underlying physical supply constraint without Hormuz traffic restoration.

What would need to happen for oil markets to stabilise?

The IEA has identified the restoration of normal tanker traffic through the Strait of Hormuz as the primary condition required for market stabilisation. Achieving this outcome depends on diplomatic progress between relevant parties, most directly between the United States and Iran. Without tangible de-escalation, the structural supply deficit and its downstream economic consequences will persist and potentially deepen.

Key Takeaways

- The Iran war has produced a 5.78 million bpd swing in global oil market balance, from a nearly 4 million bpd surplus forecast in December 2025 to a 1.78 million bpd deficit now projected for 2026

- More than 14 million barrels per day of Gulf production is shut in, with cumulative losses exceeding 1 billion barrels, a scale without historical precedent in recorded energy market history

- Demand is simultaneously contracting by 420,000 bpd, the first decline since COVID-19, as price destruction and economic slowdown compound the supply-side shock

- The IEA's emergency release of 400 million barrels from strategic petroleum reserves, while the largest in the agency's history, covers less than 40% of confirmed cumulative supply losses

- The Strait of Hormuz remains the singular physical constraint determining market outcomes, and the IEA's base-case forecast of gradual Q3 2026 resumption is conditional on de-escalation that has not yet materialised

- Diplomatic outcomes, not production decisions, now represent the dominant variable in the 2026 oil price outlook

Disclaimer: This article is based on information reported by Reuters and published via Economic Times Energy on May 13, 2026, citing the IEA's monthly oil market report. Forward-looking forecasts, scenario projections, and market balance estimates involve significant uncertainty and should not be construed as financial or investment advice. Readers are encouraged to consult the IEA's official Oil Market Reports at iea.org and independent energy analysis from established research institutions for primary source verification.

Want to Stay Ahead of the Commodity Shifts Driving the Next Wave of ASX Mineral Discoveries?

As energy market disruptions reshape global commodity demand and capital flows, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries before the broader market reacts — explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself at the forefront of the next major find.