June 25, 2026

The Chokepoint That Controls a Fifth of the World's Energy

Every major energy importing nation carries a hidden vulnerability embedded in its supply chain architecture. For most of Asia's largest economies, that vulnerability has a name and a precise geographic location: a narrow strip of water roughly 33 kilometres wide at its most constrained point, sitting between the coastlines of Iran and Oman. The Strait of Hormuz is not simply a shipping lane. It is the single most consequential maritime passage on Earth when measured by the volume and strategic value of the cargo that moves through it daily.

Understanding why India-bound ships in the Strait of Hormuz have become a focal point of international concern in 2026 requires stepping back from the immediate crisis and examining the deeper structural dependencies that made this disruption not just possible, but arguably inevitable. The crude oil geopolitics shaping this standoff have been building for years, and the current episode represents their most acute expression to date.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Irreplaceable and Therefore Fragile

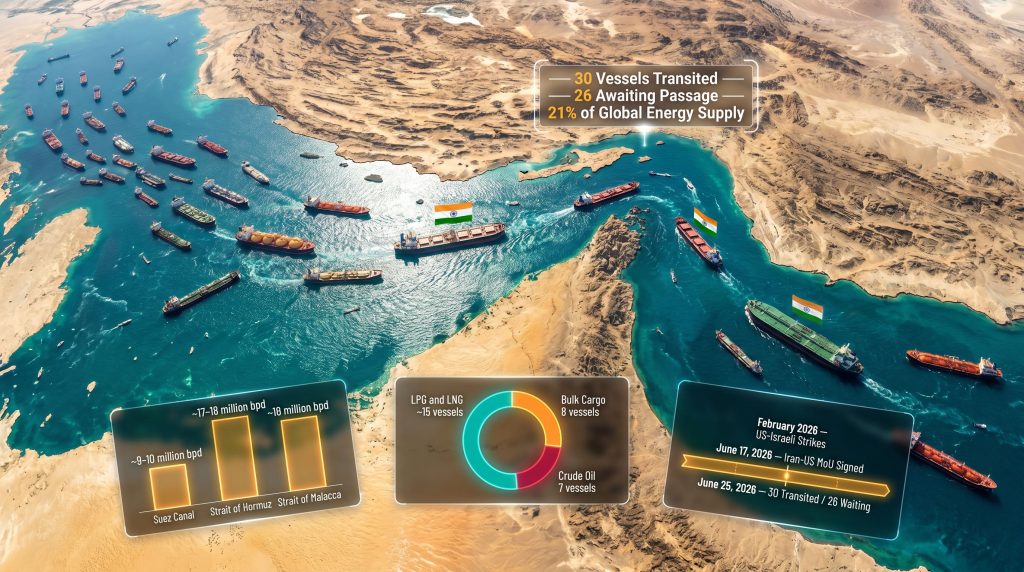

The Strait of Hormuz handles approximately 21% of global energy supply, translating into roughly 17 to 18 million barrels of oil equivalent per day transiting its waters. Unlike the Suez Canal, which has navigable alternatives through Cape of Good Hope routing, or the Strait of Malacca, where geopolitical risks are distributed across multiple state actors, Hormuz presents a unique problem: there is no practical bypass.

The two alternative pipeline routes that partially circumvent Hormuz — the Habshan-Fujairah pipeline in the UAE and the Iraq-Turkey pipeline — together carry only a fraction of the volume that moves by sea. No combination of overland infrastructure can replicate the throughput capacity of the strait itself.

A comparative view of the world's critical maritime chokepoints illustrates why Hormuz sits in a category of its own:

| Chokepoint | Share of Global Energy Flow | Daily Oil Equivalent (approx.) | Primary Risk Factor |

|---|---|---|---|

| Strait of Hormuz | ~21% | ~17-18 million bpd | Iran geopolitical leverage |

| Suez Canal | ~12% | ~9-10 million bpd | Regional conflict, blockade |

| Strait of Malacca | ~15% | ~16 million bpd | Piracy, China-Taiwan tension |

For India specifically, the exposure is amplified by the structure of its energy procurement model. The country sources the majority of its LPG and LNG from Gulf nations, with key supplier relationships concentrated in Qatar, the UAE, Saudi Arabia, and Kuwait. Every molecule of that gas must pass through Hormuz before it reaches an Indian regasification terminal or LPG import jetty.

This geographic dependency is not a policy failure; it reflects decades of rational procurement decisions based on proximity, volume availability, and cost. However, rational in peacetime becomes precarious under geopolitical stress, and the geopolitical risk landscape has shifted dramatically in 2026.

The 2026 Hormuz Crisis: How the Maritime Fallout Unfolded

What Triggered the Escalation?

The chain of events that produced the current disruption to India-bound ships in the Strait of Hormuz began with the US-Israeli strikes on Iranian territory in February 2026. Iran's response was measured initially, but within weeks the Islamic Revolutionary Guard Corps (IRGC) moved to impose direct consequences on commercial shipping transiting the strait.

Two high-profile seizures defined the opening phase of the crisis. The MSC Francesca, operating under a Panama flag, and the Epaminodes, a Liberia-flagged vessel, were intercepted by IRGC naval forces. Both carried cargo categories central to India's import pipeline. A third vessel, the Euphoria, found itself stranded in the ambiguous jurisdictional grey zone near Iranian waters, according to reports from DW, its status illustrating the difficulty of distinguishing enforcement from intimidation under Iran's emerging maritime framework.

What made this escalation structurally different from previous Iranian seizure incidents was the introduction of a formalised authorisation and toll payment system. Rather than ad hoc vessel detentions, Iran instituted what it described internally as a professional mechanism requiring vessels to obtain clearance and, in some cases, pay fees if they were associated with nations deemed cooperative with Iran's adversaries.

International maritime law experts have broadly criticised this approach as inconsistent with transit passage rights enshrined under the United Nations Convention on the Law of the Sea (UNCLOS), which classifies the Strait of Hormuz as an international waterway subject to freedom of navigation.

A formalised toll-and-authorisation system transforms maritime coercion from a tactical instrument into a structural one, creating recurring leverage rather than isolated incidents.

A partial easing came with the signing of an Iran-US Memorandum of Understanding on June 17, 2026, which altered transit conditions for certain vessel categories. However, the MoU's scope remained limited, and its protections did not extend uniformly to all commercial shipping.

Vessel Count, Cargo Breakdown, and What the Numbers Reveal

As of late June 2026, Indian shipping ministry sources confirmed the following status of vessels relevant to India's energy and cargo supply chain:

- 30 India-bound vessels had successfully transited the Strait of Hormuz

- 26 additional vessels remained in queue awaiting passage authorisation

- 22 Indian-registered vessels were still waiting for clearance to proceed

- 13 Indian-flagged vessels and one Indian-owned vessel remained stranded on the western (Persian Gulf) side of the strait

The composition of the 30 vessels that successfully crossed reveals the energy priorities at stake:

Cargo Breakdown: Transited Vessels

| Cargo Category | Number of Vessels |

|---|---|

| LPG and LNG carriers | ~15 (approximately half) |

| Bulk cargo vessels | 8 |

| Crude oil tankers | 7 |

The picture for vessels still waiting in the Persian Gulf is equally revealing, with fertiliser cargo representing a dimension of the crisis that has received less attention than the energy headline:

Cargo Breakdown: Vessels Awaiting Transit (West of Hormuz)

| Cargo Type | Vessels Waiting |

|---|---|

| Energy (LNG/LPG/crude) | 3 |

| Fertilisers | 10 |

| Other cargo | 13 |

Among the 30 vessels that have reached or are heading to Indian ports, 17 are foreign-flagged, with Marshall Islands-flagged ships representing the largest single national registry group at up to five vessels. This flag-state diversity matters from an insurance and liability standpoint, as protection and indemnity (P&I) club coverage terms vary significantly depending on whether a vessel operates under a flag whose government has been formally designated as cooperative or non-cooperative with Iranian authorities.

The timeline of transits also tells a nuanced story about the MoU's effectiveness:

| Period | Transit Completions |

|---|---|

| March 1 to June 17, 2026 | 19 vessel transits completed |

| Post-June 17, 2026 (MoU period) | 11 additional vessel transits |

| Total as of June 25, 2026 | 30 vessels transited; 26 awaiting |

The fact that 19 transits occurred before the MoU and only 11 after suggests the diplomatic agreement provided incremental rather than transformative relief. Furthermore, with 26 vessels still queued and the underlying geopolitical tension unresolved, the MoU appears to have been a partial palliative rather than a structural solution.

The Fertiliser Dimension: An Underreported Crisis Within the Crisis

Most coverage of the Hormuz disruption focuses on fuel. However, the 10 vessels carrying fertilisers stranded west of the strait represent a secondary supply chain rupture with significant downstream consequences for India's agricultural sector. India's broader fertiliser import reliance makes this dimension of the crisis particularly acute.

India's farming calendar is tightly coupled to input availability. Urea, DAP (diammonium phosphate), and MOP (muriate of potash) must reach inland distribution networks within specific seasonal windows to support planting cycles. A delay measured in weeks can translate into shortfalls in application rates, which then feed through into yield outcomes months later.

The simultaneous blockage of energy cargo and agricultural input supplies means this crisis operates across two distinct but equally critical domestic supply chains at the same time.

The Gulf region, particularly Qatar and Saudi Arabia, is a major source of nitrogen-based fertilisers for India. Consequently, any sustained disruption to fertiliser shipping through Hormuz adds an agricultural dimension to what is already a severe energy security event.

India's Diplomatic Response and Its Constraints

How Has New Delhi Responded?

India's Ministry of Shipping has been tracking both transited and queued vessels in real time, a surveillance capacity that reflects lessons learned from previous Gulf disruption episodes. However, real-time monitoring is not the same as real-time resolution.

India summoned Iran's ambassador to register formal concern about the safety of Indian-flagged vessels following two incidents involving gunfire. The Jag Arnav and Sanmar Herald, both Indian-flagged ships, came under fire despite Iran's stated policy of exempting friendly nations from coercive action. These incidents exposed the gap between official Iranian assurances and on-water enforcement reality, and hardened New Delhi's position considerably.

India's response strategy has included a notable precondition: new vessels will not be authorised to proceed to Gulf loading terminals until stranded ships have been released. This creates a diplomatic leverage point, but also risks deepening the supply shortage if the standoff extends over weeks rather than days.

The strategic constraint facing India is particularly acute. New Delhi has cultivated a purchasing relationship with Iran for discounted crude, making an overtly adversarial posture diplomatically and economically costly. At the same time, India's Gulf Cooperation Council partners, who supply the bulk of its LNG and LPG, expect India to push back against Iranian maritime coercion. Navigating between these two positions limits the directness of India's response.

The next major ASX story will hit our subscribers first

Three Scenarios for How the Hormuz Situation Resolves

The trajectory of the crisis from this point follows three broad pathways, each carrying different implications for Indian energy markets and global oil pricing:

Scenario 1: Sustained Partial Blockade

Iran maintains its authorisation system while selectively clearing vessels from nations it designates as cooperative. India continues diplomatic engagement, but LPG and fertiliser shortages deepen over a 60 to 90 day horizon. Brent crude sustains a geopolitical risk premium of $8 to $15 per barrel above pre-crisis baselines, compressing Indian refinery margins and feeding through into domestic fuel prices. Such a scenario would represent a significant oil price shock for energy markets globally.

Scenario 2: Full Normalisation via Diplomatic Resolution

A broader Iran-US framework agreement is reached, extending commercial shipping protections to third-party vessels. India's stranded fleet is released, the fertiliser pipeline resumes, and energy cargo flows normalise. The risk premium on crude retreats, and the immediate supply crisis is resolved, though the structural dependency that enabled it remains unchanged.

Scenario 3: Escalation and Extended Closure

Additional seizures or a military incident triggers coordinated international response from major oil importers including China, Japan, South Korea, and India. Emergency strategic petroleum reserve (SPR) releases are activated across importing nations. This scenario, while least likely in the near term, would represent the most severe price shock, with historical precedent from the 1980s Tanker War suggesting Brent crude could spike 30 to 50% above pre-crisis levels within weeks of a full closure.

Alternative Supply Routes: Options and Their Limitations

India's medium-term resilience depends on diversifying away from exclusive Gulf dependency, but the infrastructure constraints are substantial. In addition, the challenges of the global LNG supply landscape further complicate any rapid pivot to alternative sources:

- US LNG can reach Indian import terminals via Atlantic routing, but vessel transit times run 25 to 30 days versus 7 to 10 days from Gulf sources, adding significant cost

- Australian LNG offers Pacific routing advantages for India's east coast terminals, but contract volumes and regasification capacity constraints limit how quickly this source can be scaled

- Cape of Good Hope routing for Gulf cargo avoids Hormuz entirely but adds approximately 3,500 to 4,000 nautical miles per voyage, increasing freight costs and extending delivery timelines by 10 to 14 days

- India's strategic petroleum reserves currently hold approximately 5.33 million tonnes across Visakhapatnam, Mangalore, and Padur, providing a buffer measured in weeks rather than months for a disruption of this scale

The regasification infrastructure bottleneck is particularly binding. India's LNG import capacity is concentrated in facilities designed around Gulf cargo specifications and delivery schedules. Rapidly pivoting to non-Gulf LNG sources at scale would require both available terminal capacity and renegotiated contractual terms with alternative suppliers, neither of which can be arranged quickly.

The Legal Architecture of Hormuz and Why It Matters

Under UNCLOS, the Strait of Hormuz qualifies as a strait used for international navigation, granting commercial vessels transit passage rights that are stronger than the innocent passage rights applicable in standard territorial waters. Specifically, transit passage cannot be suspended by the coastal state, a provision designed precisely to prevent nations like Iran from using geographic position as a commercial toll mechanism.

Iran has historically maintained a dissenting position on this legal framework, asserting a degree of territorial authority over the strait that most international maritime law scholars consider inconsistent with UNCLOS provisions. Iran is also not a party to UNCLOS in the same ratification status as other nations, which complicates the enforcement of international legal norms against its maritime actions.

The practical consequence is a legal grey zone where Iran's enforcement actions carry political cost but face limited immediate legal accountability, particularly given the absence of a rapid international adjudication mechanism for maritime disputes of this kind.

Key Takeaways for India's Energy Security Calculus

The 2026 Hormuz crisis has surfaced a set of structural truths about India's energy security posture that policy discussions have long acknowledged but rarely been forced to confront at operational speed. India-bound ships in the Strait of Hormuz have become the clearest expression of these systemic vulnerabilities:

- India's Gulf-centric procurement model offers cost and proximity advantages that are difficult to replicate through diversification alone

- Diplomatic tools have produced only partial and fragile relief, with the Iran-US MoU enabling 11 additional transits while leaving 22 Indian-registered vessels still awaiting clearance

- The simultaneous disruption of energy and fertiliser cargo creates compounding downstream risks extending well beyond fuel pricing

- The legal framework governing Hormuz transit is real but practically unenforceable in the short term without broader multilateral pressure

- Medium-term resilience requires investment in regasification capacity, expanded SPR holdings, and contractual diversification toward non-Gulf LNG sources, none of which can be activated quickly enough to address the immediate crisis

The Strait of Hormuz will remain a systemic risk factor in India's energy security architecture for as long as the country's import dependency on Gulf hydrocarbons persists. The 2026 episode is a stress test that the system has partially absorbed, but the underlying fragility has not been resolved. It has simply been deferred.

This article contains forward-looking scenario analysis and projections regarding geopolitical developments, energy market pricing, and supply chain outcomes. Such scenarios involve inherent uncertainty and should not be interpreted as predictions of specific outcomes. Readers should conduct independent analysis before making any decisions based on the information contained herein.

Want to Know Which ASX Resources Companies Are Positioned for Energy and Commodity Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they hit the exchange, transforming complex data across more than 30 commodities into clear, actionable insights — precisely the kind of market intelligence that matters when geopolitical shocks reshape global supply chains. Explore historic discoveries and their returns to understand the potential upside, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major market-moving announcement.