June 7, 2026

When Oil Markets Collide With Geopolitics: Understanding India's April Crude Correction

Global crude oil markets rarely move in straight lines. Supply disruptions, sanctions regimes, and shipping logistics interact in ways that create sharp but often temporary volume swings — swings that can be misread as structural shifts when they are, in fact, the natural unwinding of compounded short-term pressures. Understanding what drives these corrections requires looking beneath headline import figures to the layered mechanics of international crude procurement, floating cargo dynamics, and the outsized influence of sanctions architecture on buyer behaviour. The crude market dynamics at play in 2025 and 2026 provide essential context for this analysis.

April 2026 delivered precisely this kind of moment for India's oil sector. After Russian crude arrivals surged to historically elevated levels in March, India Russian crude imports fall 20% in April — a sharp pullback that, on the surface, appeared to signal a strategic repositioning. The reality was considerably more technical — and considerably more instructive about how modern sanctioned-oil trade actually functions.

When big ASX news breaks, our subscribers know first

How India Became Russia's Most Strategically Important Crude Customer

Before February 2022, Russia played a relatively modest role in India's crude import mix, accounting for roughly 2–3% of total volumes. That figure was transformed almost overnight following Western sanctions on Russian energy exports, which displaced the European buyer base that had historically absorbed the majority of Russian crude production. Indian refiners, operating under a policy framework of energy sovereignty and non-alignment, stepped into the gap — and the economics were compelling.

Russian crude, particularly Urals grade and the ESPO blend exported from Russia's Far East, became available at discounts ranging from $8 to $15 per barrel relative to Brent crude benchmarks during the 2023–2024 period. For refinery procurement teams operating on thin crack spreads, that margin represented a meaningful competitive advantage — particularly for facilities already configured to process heavier, higher-sulphur feedstocks.

By mid-2022, Russia had overtaken Saudi Arabia and Iraq on certain monthly metrics to become India's largest crude supplier. By 2023–2024, Russian crude was estimated to represent 11–13% of India's total crude import basket, translating to approximately 1.2–1.4 million barrels per day across the refinery sector. The technical dimension of this shift mattered as much as the economic one.

Refinery Configuration and Grade Compatibility

Indian refineries adapted to Russian supply across two primary crude grades. Urals crude carries an API gravity of approximately 32–34 degrees with higher sulphur content, requiring robust hydrocracking and desulphurisation capacity. The lighter ESPO blend, exported through the Kozmino terminal on Russia's Pacific coast, offered a more flexible feedstock but involved longer, more complex shipping logistics for Indian west-coast refineries.

Nayara Energy's refinery at Vadinar presented the clearest structural case: with Rosneft holding a significant ownership stake following a 2017 restructuring, the facility maintained Russian crude at 35–38% of its crude slate during 2023–2024 — proportionally the highest among major Indian processors. Indian Oil Corporation, with its diverse refinery network and strong state-enterprise procurement capabilities, emerged as the dominant volume buyer across the broader market.

The Three Factors That Made March 2026 an Anomaly

India's Russian crude arrivals approached 2 million barrels per day in March 2026 — a figure that substantially exceeded the prevailing 2023–2024 baseline and reflected the simultaneous convergence of three distinct pressures, none of which were structural in character.

The Strait of Hormuz Disruption and Its Substitution Effect

The closure of the Strait of Hormuz in March 2026 created an acute shortage of Gulf-sourced crude for Indian refineries. The Strait serves as the transit corridor for approximately 21 million barrels per day of global seaborne crude — including the Iraqi, Saudi, Kuwaiti, and Emirati supplies that Indian refineries depend on as baseline feedstock. When transit through the Strait was interrupted, refinery procurement teams faced an immediate gap requiring rapid sourcing alternatives.

According to shipping analytics data from Kpler, Indian refiners responded by tapping readily available floating Russian cargoes positioned in the Indian Ocean and adjacent waters. These vessels, holding unsold or pre-positioned Russian crude, provided an accessible short-notice supply source that Middle Eastern alternatives — requiring renegotiation, reloading, and rerouting — could not match for speed. Furthermore, India and China's pivot to Russian oil during this period underscored how geopolitical disruptions accelerate supply diversification decisions among Asia's largest energy consumers.

Floating Cargo Mechanics: The Hidden Inventory Buffer

The floating cargo phenomenon is less widely understood than headline import statistics suggest. When Russian crude discounts are steep enough relative to prevailing benchmarks, traders find it economically rational to hold crude in floating storage aboard tankers — effectively creating a mobile, at-sea inventory buffer. Typical supramax tanker carrying costs for this purpose run approximately $25,000–$40,000 per day, meaning the economics only work when the expected discount narrowing justifies the holding cost.

By early 2026, a significant volume of Russian crude had accumulated in floating storage in the Indian Ocean, reflecting both uncertainty around Western sanctions enforcement and anticipation of demand recovery. The Hormuz disruption provided the demand catalyst that absorbed this inventory rapidly — inflating March arrival figures well beyond what Russian port loadings alone would have generated.

The Sanctions Waiver Window and Its Procurement Acceleration Effect

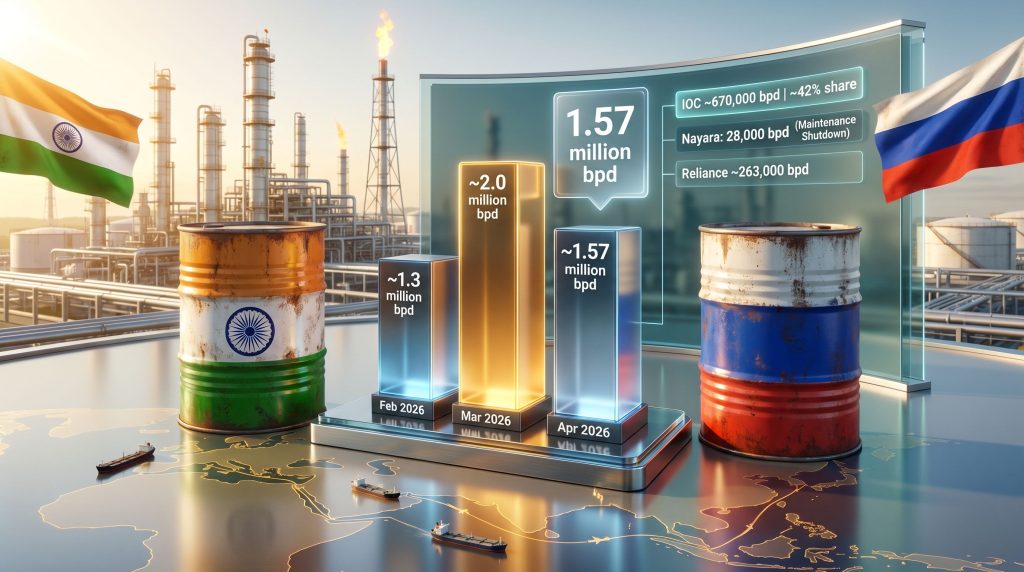

A temporary easing of US sanctions on key Russian crude exporters in the February–March 2026 window created a third accelerating factor. According to Kpler data cited in ET EnergyWorld's April 28, 2026 reporting, February loadings at Russian ports were constrained to approximately 1.3 million bpd — suppressed directly by sanctions that had deterred Indian buyer participation. As recently as January 2026, only three Indian refiners were actively sourcing Russian crude: Indian Oil Corporation, Nayara Energy, and BPCL.

The temporary easing of restrictions prompted a rapid re-engagement across the broader refinery sector, with loading activity accelerating in late February and through March. Given the approximately 30-day transit lag between Russian port loading and Indian port arrival, this procurement surge fed directly into elevated March arrival figures. The Russian oil sanctions impact on buyer behaviour, consequently, proved both profound and reversible within a relatively short timeframe.

The mechanics here mirror a pattern observed historically after sanctions-related demand suppression: when restrictions ease — even temporarily — buyers who deferred purchases accelerate procurement simultaneously, creating a demand spike that exceeds any single buyer's individual increase.

April 2026 by Refinery: Where the Numbers Actually Went

The April 2026 moderation — with India Russian crude imports fall 20% from March peaks — reflected a combination of normalising fundamentals and refinery-specific operational factors. The disaggregated picture is more informative than the aggregate decline.

Indian Oil Corporation: The One Counter-Trend Buyer

Indian Oil Corporation stood apart from the April correction, actually increasing its Russian crude intake month-on-month. IOC averaged approximately 670,000 bpd between April 1 and 26, up from 589,000 bpd in March — making it the sole major buyer to expand volumes during the broader market pullback.

IOC's April volume accounted for roughly 42% of India's total Russian crude purchases, approximately 2.5 times the intake recorded by Reliance Industries over the same period. This concentration reflects IOC's refinery network scale, its long-standing procurement relationships with Russian suppliers, and its status as a state-owned entity with strategic crude diversification mandates. IOC's counter-cyclical behaviour in April also suggests that its March volumes were less distorted by floating cargo absorption than other buyers — meaning the normalisation effect hit other participants harder.

Mid-Tier Refinery Participation: Stable but Reduced

The mid-tier segment showed relatively orderly April volumes, broadly consistent with operational throughput requirements rather than opportunistic buying patterns.

| Refiner | April 2026 Volume (bpd) | March Context |

|---|---|---|

| BPCL | 136,000 | Stable participation during normalisation |

| HPCL | 83,000 | Maintained despite logistics headwinds |

| MRPL | 68,000 | Mangalore refinery sustaining Russian slate |

| HMEL | 66,000 | Bathinda facility continuing discounted barrel intake |

These figures, sourced from Kpler shipping analytics data, suggest that mid-tier refiners absorbed floating cargo in March but reverted to conventional loading-cycle procurement in April — consistent with the thesis that the March surge was inventory-driven rather than demand-driven.

Nayara Energy: Maintenance Shutdown Creates a Statistical Distortion

The sharpest single-refinery move in April was Nayara Energy's collapse from 315,000 bpd in March to just 28,000 bpd in April — a reduction of nearly 91%. The cause was not strategic or sanctions-related: a planned 35-day maintenance shutdown commenced on April 9, 2026, taking the Rosneft-backed Vadinar refinery substantially offline.

This maintenance event is critical context for interpreting the aggregate 20% decline. Nayara's withdrawal alone removed approximately 287,000 bpd of Russian crude demand from the Indian market — accounting for roughly two-thirds of the total month-on-month volume reduction. Without this single operational factor, the April decline would have been considerably more modest.

Reliance Industries: A Cautious Return After Sanctions Abstention

Reliance Industries recorded approximately 263,000 bpd in April, having resumed Russian crude purchases in February 2026 following a period of abstention linked to sanctions-related compliance concerns. Reliance's return represented a strategically significant signal: the company's scale, global refinery partnerships, and export-oriented refined product sales create heightened sanctions exposure compared to domestic-focused peers, making its procurement decisions a bellwether for the broader regulatory risk environment.

Approximately 262,000 bpd of April Russian crude arrivals could not be attributed to named buyers in available Kpler shipping data — a figure reflecting the persistent opacity of spot-market procurement channels and the continued use of intermediary trading structures in sanctioned-oil supply chains.

Russian Export Infrastructure Under Pressure: The Baltic Terminal Factor

April's moderated arrivals were not solely a function of Indian demand dynamics. Supply-side disruptions at Russian loading infrastructure contributed independently to the volume correction.

Ukrainian military strikes targeted a key Russian Baltic Sea export terminal in March 2026, disrupting loading operations during a period when March loadings were already running at approximately 1.5 million bpd — itself a figure constrained relative to arrival volumes by the absorption of pre-positioned floating inventory. According to Kpler's senior research analyst Nikhil Dubey, as cited in ET EnergyWorld's April 28, 2026 report, the terminal attack added a further headwind to already moderating loading activity.

The 30-Day Lag and Its Analytical Implications

Russian crude shipments to India carry a transit lag of approximately 30 days, meaning April port arrival data directly mirrors March loading volumes rather than April loading activity. This structural lag creates significant analytical complexity: headline import figures reported for any given month actually reflect decisions made and loadings executed in the prior month.

This mechanism explains why February's suppressed loading volumes — constrained by sanctions to approximately 1.3 million bpd — translated into lower March arrivals on a loading-equivalent basis, even as floating cargo absorption pushed headline March arrival figures to approximately 2 million bpd. The two metrics were temporarily divergent, and April arrivals at roughly 1.57 million bpd represented a convergence back toward loading-equivalent volumes.

Monthly Trend Comparison: Contextualising the April Correction

| Month | Estimated Russian Crude Arrivals (bpd) | Primary Driver |

|---|---|---|

| February 2026 | ~1.3 million | US sanctions suppressing export loading |

| March 2026 | ~2.0 million | Hormuz disruption + floating cargo surge + sanctions waiver |

| April 2026 | ~1.57 million | Normalisation + Nayara shutdown + terminal disruption |

The April figure of 1.57 million bpd sits meaningfully above the February suppression baseline but well below the March anomaly peak. Whether this represents a new structural floor or a transitional figure depends critically on which of April's headwinds persist. If Nayara resumes full operations within its projected post-maintenance timeline, that single factor alone would restore 250,000–300,000 bpd of Russian crude demand — pushing May arrivals back toward the 1.8 million bpd range, absent other offsetting factors.

The next major ASX story will hit our subscribers first

The Sanctions Architecture: How US Policy Continues to Shape Indian Procurement

The sanctions dimension of India's Russian crude purchasing is frequently oversimplified in market commentary. The relevant mechanism is not a blanket prohibition on Russian crude — India has consistently maintained that purchasing Russian oil does not violate Indian law or its international obligations. Rather, US sanctions operate through secondary market pressure: targeting specific Russian crude exporters rather than the crude commodity itself, and creating financial and reputational risk for Indian buyers who transact with designated entities.

This distinction explains the January 2026 market structure, when only three Indian refiners — Indian Oil Corporation, Nayara Energy, and BPCL — remained active Russian crude buyers. US sanctions on key Russian exporters had deterred other participants not through legal prohibition but through compliance risk management. The temporary easing that preceded the March surge effectively reduced that compliance risk sufficiently to re-activate broader market participation. Furthermore, the trade war oil impacts of this period added additional complexity for procurement teams navigating an already volatile geopolitical environment.

By April 2026, nearly all major Indian refiners had returned to Russian crude sourcing. Numaligarh Refinery remained the sole holdout among major buyers — a position reflecting either technical constraints on processing Russian crude grades or ongoing compliance caution at the management level.

Scenario Pathways: Four Possible Trajectories for India's Russian Crude Imports

The months following April 2026 present genuinely divergent scenarios, each with distinct implications for import volumes, refinery economics, and geopolitical signalling.

Scenario 1: Sanctions Tightening Returns

A reversal toward January 2026-level restrictions — whether through new OFAC designations or enforcement actions against intermediary trading structures — would recreate the compliance deterrence environment that reduced active buyers to three. Under this scenario, volumes could compress back toward 1.2–1.3 million bpd, with mid-tier refiners again exiting the market first.

Scenario 2: Hormuz Remains Contested

A second Gulf supply disruption would replicate the March floating cargo absorption dynamic. However, the available floating inventory buffer has already been substantially depleted — meaning a second disruption would not produce the same magnitude of surge unless fresh Russian crude had re-accumulated in floating storage.

Scenario 3: Russia-Ukraine Ceasefire and Baltic Terminal Restoration

A diplomatic resolution to the Ukraine conflict would potentially restore Baltic loading infrastructure and normalise export volumes from Primorsk and other key terminals. Paradoxically, this scenario might also reduce Russian crude discounts — as sanctions relief would restore Western buyer access, narrowing the price gap that makes Russian barrels economically attractive to Indian refiners.

Scenario 4: India Accelerates Middle East Diversification

India's refinery sector has strategic motivations to avoid over-dependence on any single crude source. If Russian discounts narrow substantially — whether through sanctions relief, geopolitical normalisation, or OPEC+ production adjustments — the economic rationale for maintaining Russian crude at 40%+ of the import basket weakens. Indian refiners have demonstrated flexible crude slate management before and could rotate back toward Middle Eastern grades if the economics shifted sufficiently.

The Price Discount Calculus: Why Complexity Remains Economically Justified

Indian refiners continue absorbing considerable logistical complexity to access Russian barrels — extended shipping distances, insurance complications linked to sanctions exposure, and payment settlement challenges through non-dollar intermediaries. The economics justify this complexity only as long as the per-barrel discount exceeds the per-barrel cost of that complexity.

During peak discount periods in 2023–2024, the $8–$15 per barrel gap comfortably covered these additional costs. However, if geopolitical conditions shift the discount toward $4–$5 per barrel — the approximate threshold at which logistical premiums consume the price advantage — Indian refiners would have direct economic incentive to rotate sourcing toward less complex Middle Eastern supply chains, even without any policy direction to do so. Broader oil price movements during 2025 have already begun testing those thresholds in certain market conditions.

This price sensitivity creates a natural self-correcting mechanism in India's Russian crude dependency: the lower the discount, the weaker the demand, which in turn tends to preserve the discount at equilibrium levels. Understanding this dynamic is essential context for interpreting whether Indian buyers are strategic partners in Russia's oil export system or purely opportunistic price-sensitive participants. For a broader perspective, the crude oil market overview provides useful benchmarking against these evolving discount thresholds.

Frequently Asked Questions: India's Russian Crude Imports in 2026

Why did India Russian crude imports fall 20% in April 2026?

Three factors converged: the natural unwinding of a floating cargo surge that temporarily amplified March arrivals, a planned 35-day maintenance shutdown at Nayara Energy's Vadinar refinery that removed approximately 287,000 bpd of demand, and loading disruptions at Russian Baltic Sea terminals following Ukrainian military strikes in March.

Which Indian refiner purchases the largest volume of Russian crude?

Indian Oil Corporation dominated April 2026 procurement, averaging approximately 670,000 bpd and accounting for roughly 42% of India's total Russian crude intake — approximately 2.5 times the volume imported by Reliance Industries during the same period.

Is the April decline a sign that India is reducing its dependence on Russian oil?

Available data does not support this interpretation. The April correction reflects specific short-term operational and supply-chain factors rather than any strategic policy shift. With Nayara Energy expected to resume full operations after its maintenance window and floating cargo inventory likely rebuilding, May volumes may recover meaningfully from April levels. According to India's crude import trends, the data broadly supports this assessment.

How do US sanctions affect Indian refinery purchasing decisions?

US sanctions target specific Russian crude exporters rather than prohibiting Russian crude as a commodity category. This creates compliance risk for Indian buyers transacting with designated entities, deterring participation without creating an outright legal prohibition under Indian law.

What is the transit lag for Russian crude shipments to India?

Approximately 30 days from loading at Russian export terminals to port arrival in India, meaning any given month's arrival data reflects the prior month's loading activity — not current procurement decisions.

Why did Nayara Energy's volumes fall so sharply in April?

A planned 35-day refinery maintenance shutdown commenced on April 9, 2026, temporarily reducing the Rosneft-backed facility's crude intake from 315,000 bpd in March to just 28,000 bpd in April. This is an operational, not strategic, development.

What the April Correction Reveals About the Broader India-Russia Energy Relationship

The April 2026 data carries implications that extend well beyond a single month's import statistics. Several less widely appreciated dynamics are worth emphasis.

First, the opacity of spot-market procurement channels remains structurally significant. With approximately 262,000 bpd of April arrivals unattributed to named buyers in Kpler shipping data, a meaningful portion of India's Russian crude trade continues to flow through non-transparent intermediary structures — a feature of sanctioned-oil markets that complicates both enforcement and analysis.

Second, the speed of market re-entry following sanctions easing is striking. Moving from three active buyers in January to nearly all major refiners by April demonstrates that the compliance deterrence effect of US sanctions is powerful but reversible on relatively short timescales. This has implications for how policymakers and market analysts should interpret periods of apparent demand suppression. Hormuz disruption effects on Indian and Chinese buyers further illustrate how rapidly import strategies can shift in response to supply shocks.

Third, the single-refinery concentration risk illustrated by Nayara Energy's maintenance impact deserves attention. A single planned shutdown at one refinery was responsible for roughly two-thirds of the total month-on-month volume decline — a reminder that aggregate import statistics can be heavily influenced by idiosyncratic operational factors at individual facilities.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or energy policy advice. Import volume figures are sourced from Kpler shipping analytics data as reported by ET EnergyWorld and may be subject to revision as additional vessel discharge data becomes available. Forward-looking scenarios represent analytical possibilities, not predictions, and actual market outcomes will depend on geopolitical, regulatory, and operational factors that remain subject to change.

Want to Capitalise on the Next Major Commodity Discovery Before the Broader Market?

While geopolitical forces reshape global oil flows and create volatility across commodity markets, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time — instantly identifying significant mineral discoveries and turning complex data into actionable opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.