June 21, 2026

The Chokepoint That Shapes a Nation's Energy Fate

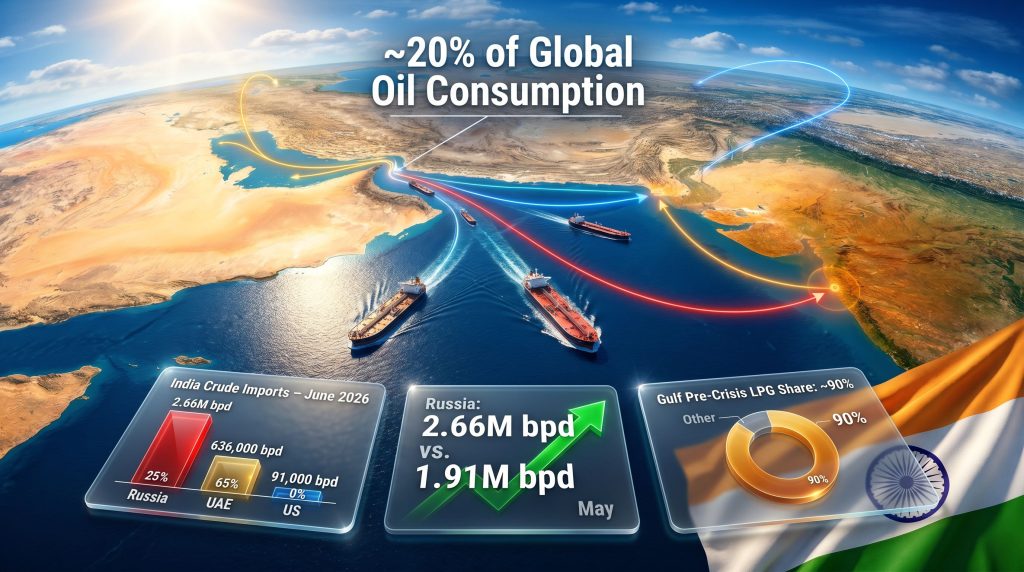

Few physical features on Earth carry as much economic consequence as a narrow stretch of water between the Omani and Iranian coastlines. At its most constricted point, the Strait of Hormuz measures roughly 33 kilometres across, yet through this slender corridor flows approximately 20% of global oil consumption. For energy-hungry economies, few geographic realities are more consequential. India boosts Russian and UAE oil purchases ahead of Strait of Hormuz recovery, and understanding why requires examining the structural vulnerabilities embedded into the nation's economic architecture.

Understanding how India navigated the recent Hormuz closure, and how it is now repositioning as the waterway partially reopens, requires examining not just the headline crude oil figures, but the layered, commodity-specific responses that played out across LPG, LNG, and crude markets simultaneously. The disruption did not affect all fuels equally, and consequently the recovery will not unfold uniformly either.

When big ASX news breaks, our subscribers know first

India's Structural Energy Exposure: The Numbers Behind the Dependency

India imports approximately 88% of its total crude oil requirements, a figure that immediately frames the scale of the strategic challenge. As the world's third-largest energy importer, India's economic trajectory is intimately connected to the reliability and cost of external energy supply. Furthermore, the oil and global economy relationship means that disruptions of this scale reverberate well beyond India's borders.

Before the Hormuz disruption, the Gulf region's share of India's energy imports was dominant across all three major hydrocarbon categories:

| Commodity | Pre-Crisis Gulf Share | Primary Gulf Suppliers |

|---|---|---|

| Crude Oil | ~50% of total imports | Saudi Arabia, Iraq, UAE, Kuwait |

| LNG | ~67% of total imports | Qatar, UAE, Oman |

| LPG | ~90% of total imports | Saudi Arabia, UAE, Kuwait |

This concentration meant that any disruption to Hormuz transit would ripple through India's energy system with force, though the severity would differ depending on how much alternative sourcing infrastructure already existed for each commodity.

The closure itself followed US and Israeli military strikes, which prompted Iran to shut the Strait, severing the principal export artery for all major Gulf producers. A subsequent US-Iran ceasefire facilitated the partial reopening of the waterway, though ongoing Israeli-Iranian tensions have kept confidence in the truce's durability fragile.

The partial nature of the recovery is itself significant: three Indian-flagged oil tankers carrying more than 860,000 tonnes of crude and an Indian LNG carrier have since resumed Hormuz transit, but the restoration of full normalised flows remains a process, not an event.

India Boosts Russian and UAE Oil Purchases Ahead of Hormuz Recovery

The headline shift in India's import strategy during the disruption period has been the dramatic acceleration of purchases from Russia and the UAE. This trend now defines how India boosts Russian and UAE oil purchases ahead of Strait of Hormuz recovery as Gulf flows cautiously resume. The scale of this oil market disruption has forced rapid and decisive strategic adaptation.

Russia's Historic Surge: Cementing Dominance in India's Crude Basket

India imported an average of 2.66 million barrels per day (bpd) of Russian crude in June 2026 through June 19, sharply up from 1.91 million bpd in May, according to maritime and commodity intelligence data from Kpler. Full-month June volumes are projected to potentially set a new monthly record, with estimates pointing toward figures exceeding 2.35 million bpd across the complete period.

According to recent data on India's crude purchases, several interlocking factors explain Russia's ascendancy:

- Price discounts on Russian crude grades have remained persistent and commercially meaningful, providing Indian refiners with a margin advantage over equivalent grades sourced elsewhere.

- Refinery infrastructure adaptation: Indian refiners have progressively modified their processing configurations to handle Russian crude grades, creating operational switching costs that reinforce supply continuity beyond purely commercial considerations.

- Sanctions flexibility: The US temporarily relaxed restrictions to permit India to purchase Russian crude already at sea, enabling the redirection of stranded cargoes toward Indian ports during a period of acute supply tightness.

- Supply reliability: During a period when Gulf flows were constrained or uncertain, Russia provided a consistent, high-volume alternative that required no new logistics infrastructure.

The deeper strategic reality is that Russia's role in India's crude import basket has undergone a structural transformation since 2022, not merely a crisis-driven spike. The Hormuz disruption has amplified an existing trend rather than created an entirely new one.

UAE Crude Near Record Levels: The Strategic Proximity Advantage

UAE crude shipments to India reached 636,000 bpd in June through June 19, just marginally below the record 644,000 bpd recorded in May. The UAE's ability to maintain near-record export volumes to India during the Hormuz crisis reflects both geographic proximity, which reduces freight exposure, and the strategic depth of the bilateral energy relationship.

Beyond spot volumes, Abu Dhabi has formalised longer-term energy security arrangements with India. This includes a commitment to store up to 30 million barrels of crude within India's domestic strategic petroleum reserve infrastructure. This arrangement functions as a structural hedge against future short-duration supply shocks, providing India with a buffer that does not require permanent changes to its import sourcing mix.

US Crude Imports Collapse: Freight Economics and Competitive Pressures

The sharp reversal in US crude imports to India illustrates the price-sensitive and logistically driven nature of spot purchasing decisions. US crude volumes fell from 252,000 bpd in May to just 91,000 bpd in June, a decline of more than 60% within a single month.

The explanation lies in freight economics. As India redirected purchasing toward geographically closer, more commercially competitive suppliers, the cost disadvantage of Atlantic Basin crude from the US became more pronounced. Russian and Venezuelan grades offered Indian refiners processing heavier crude grades a more viable alternative, particularly when combined with sustained price discounts unavailable on US supply.

India's June 2026 Crude Import Rankings: Supplier Volumes at a Glance

| Supplier | June Volume (bpd, through June 19) | May Volume (bpd) | Rank |

|---|---|---|---|

| Russia | ~2,660,000 | 1,910,000 | #1 |

| UAE | ~636,000 | 644,000 | #2 |

| Saudi Arabia | ~384,000 | N/A | #3 |

| Venezuela | ~209,000 (recorded) | N/A | #4 |

| United States | ~91,000 | 252,000 | #5 |

Venezuela and the Atlantic Basin: Diversification's Emerging Frontier

Venezuela's emergence as India's fourth-largest crude supplier during the disruption period represents one of the more structurally interesting dimensions of India's crisis response. Venezuelan crude shipments to India are estimated at 300,000 to 400,000 bpd in June overall, with recorded flows of approximately 209,000 bpd through mid-month.

For Indian refiners configured to process heavier crude grades, Venezuelan supply offered a cost-effective substitute for Gulf heavy grades at a time when those flows were constrained. However, several risk factors temper the longer-term reliability of Venezuelan supply:

- Ongoing sanction risks introduce unpredictability into procurement planning and financing arrangements.

- Production capacity constraints within Venezuela's domestic oil industry limit the ceiling on sustainable export volumes.

- Logistical complexity associated with Venezuelan cargo arrangements adds operational risk compared to established Gulf supply chains.

Alongside Venezuela, broader Atlantic Basin sourcing has expanded materially since March 2026, with Brazil contributing additional supply depth as Indian refiners built out a more geographically diversified procurement portfolio.

LPG: The Most Severely Disrupted Commodity in India's Energy System

While crude oil attracted the majority of market attention during the Hormuz closure, LPG experienced by far the most acute structural disruption. With approximately 90% of India's LPG imports sourced from Gulf producers prior to the crisis, there was virtually no pre-existing alternative supply infrastructure capable of absorbing the gap at scale.

The United States stepped in as a major LPG supplier following the disruption, supported by a long-term supply agreement signed in 2025. While this arrangement materially improved India's LPG supply diversification profile, it simultaneously introduced a significant freight cost burden.

LPG is expected to be the first commodity to benefit meaningfully from Hormuz reopening, precisely because the supply gap was most severe and the Gulf producers most motivated to restore export volumes quickly. Stranded LPG cargoes clearing the Strait represent the initial normalisation signal for India's entire hydrocarbon import recovery.

LNG: Relative Resilience Through Rapid Alternative Sourcing

Despite the Gulf accounting for roughly two-thirds of India's LNG imports pre-disruption, the LNG market demonstrated considerably more resilience than LPG during the Hormuz closure. Indian LNG buyers were able to source replacement cargoes from Oman, Nigeria, and the United States, partially but meaningfully offsetting the reduction in Gulf availability.

The LNG market's relative flexibility reflects several structural features:

- Spot market depth: Global LNG spot markets are considerably more liquid and geographically diverse than LPG supply chains, providing Indian buyers with more sourcing options under tight conditions.

- Longer contractual lead times: Indian LNG buyers had somewhat more operational runway to arrange alternative sourcing compared to LPG, where supply gaps emerge more abruptly.

- Existing supplier relationships: Established relationships with Omani, Nigerian, and US LNG exporters meant alternative sourcing could be activated without requiring entirely new commercial arrangements.

LNG normalisation is anticipated to follow LPG in a sequential recovery sequence, given the longer contractual and logistical timelines involved in restoring Gulf LNG flows to pre-crisis levels.

The next major ASX story will hit our subscribers first

The Sequential Recovery Framework: How Hormuz Normalisation Will Unfold

The reopening of the Strait of Hormuz will not produce an immediate return to pre-crisis trade patterns. Industry analysis, including assessments from commodity intelligence specialists with direct tracking of vessel movements and cargo flows, points to a phased recovery trajectory. The crude oil geopolitics underpinning this recovery are complex and deeply intertwined with regional security dynamics.

Phase 1: Clearing Stranded Cargoes and Rebuilding Shipping Confidence

The initial recovery phase centres on clearing vessels that were stranded or rerouted during the closure period. Shipping companies, cargo insurers, and commodity traders are expected to rebuild confidence in the Hormuz route gradually rather than immediately. War risk insurance premiums for Hormuz transit are a particularly important signal to watch, as these premiums directly affect the commercial economics of routing vessels through the Strait versus alternative paths.

A full return to pre-crisis trade patterns could take weeks to months as these market confidence metrics normalise.

Phase 2: LPG Flows Normalise First

Gulf LPG exporters have the strongest commercial incentive to rapidly restore shipments once transit confidence is re-established, given the scale of the supply gap created during the closure. India's LPG import mix is likely to rebalance toward Gulf suppliers in this phase, though the US will retain a meaningful and potentially growing share under the existing long-term supply agreement signed in 2025.

Phase 3: Gradual Crude and LNG Rebalancing

Crude and LNG import normalisation will follow a more cautious trajectory. Indian refiners and LNG buyers are expected to assess the durability of the ceasefire and the sustained reliability of Hormuz transit before unwinding the diversification positions they have built over the preceding months. Gulf producers including Saudi Arabia, Iraq, and Kuwait are anticipated to gradually reclaim market share in India's crude import basket, but this process will be measured rather than abrupt.

Will Russia's Position Survive the Hormuz Recovery?

One of the most consequential questions for global oil markets is whether Russia will retain its dominant position in India's crude import basket once Hormuz flows fully normalise and Gulf producers reassert supply capacity. The OPEC market influence on this rebalancing dynamic will also be a critical variable to monitor.

The evidence points toward structural persistence rather than reversal, for three interconnected reasons:

- Sustained commercial advantage: Russian crude's price discount structure reflects geopolitical and sanctions dynamics that are unlikely to resolve quickly, preserving the margin advantage for Indian refiners.

- Refinery configuration lock-in: The significant investments Indian refiners have made in adapting processing infrastructure to handle Russian crude grades create genuine switching costs that make a rapid reversal commercially unattractive.

- Supply security diversification value: Maintaining a large Russian supply position alongside Gulf supply diversifies India's source geography in a way that reduces concentration risk, a lesson the Hormuz crisis has powerfully reinforced.

Russian crude is expected to remain a cornerstone of India's import strategy even after Hormuz normalises, given the combination of favourable economics and supply security considerations, according to analysis from Kpler modelling specialists covering India's oil import flows.

India's Emerging Post-Crisis Import Architecture

The most enduring legacy of the Hormuz disruption for India's energy strategy is likely to be a permanently broader sourcing base. The diversification accelerated under crisis conditions, particularly toward Russia, Venezuela, Brazil, and Atlantic Basin suppliers, is expected to be deliberately retained as a structural supply security measure even as Gulf flows recover.

| Commodity | Pre-Crisis Gulf Share | Key Diversification Sources Established |

|---|---|---|

| Crude Oil | ~50% of imports | Russia, Venezuela, Brazil, Atlantic Basin |

| LNG | ~67% of imports | Oman, Nigeria, United States |

| LPG | ~90% of imports | United States (long-term 2025 agreement) |

The freight cost implications of this broader sourcing base deserve attention. Sourcing crude from Russia, Venezuela, Brazil, and the United States introduces higher average freight costs compared to Gulf supply. However, this premium is partially, and in many cases substantially, offset by the price discounts available on Russian and Venezuelan grades.

Furthermore, as reported by Reuters, India's May oil supply from the UAE had already topped pre-war levels, underscoring how aggressively India repositioned its import strategy even before the Hormuz partial reopening. The UAE's strategic petroleum storage commitment of up to 30 million barrels within India's domestic reserve infrastructure adds another layer of resilience architecture that did not exist at this scale before the crisis.

Frequently Asked Questions: India's Oil Strategy and the Hormuz Disruption

Why did India significantly increase Russian crude oil purchases during the Strait of Hormuz closure?

Russian crude offered a combination of persistent price discounts and reliable supply availability at precisely the moment Gulf flows were most constrained. June 2026 imports reached 2.66 million bpd, up from 1.91 million bpd in May, cementing Russia as India's dominant crude supplier by a significant margin. In addition, the oil price shock experienced globally reinforced the strategic logic of locking in discounted supply at scale.

Which Indian energy commodity was most severely disrupted by the Hormuz closure?

LPG was the most acutely affected commodity, given that approximately 90% of India's LPG imports originated from Gulf producers. Crude oil and LNG proved more resilient due to India's ability to activate alternative sourcing arrangements relatively quickly.

What is the expected timeline for India's energy import flows to return to pre-crisis conditions?

LPG flows are expected to normalise first as stranded cargoes clear and Gulf exporters prioritise restoring this supply. LNG and crude rebalancing will follow on a more gradual timeline, with a full return to pre-crisis trade patterns potentially taking weeks to months as shipping confidence, insurance markets, and trader risk appetite rebuild.

Will India reduce its Russian crude oil purchases once Hormuz fully reopens?

Analysts expect Russian crude to remain structurally embedded in India's import strategy even after normalisation, given sustained commercial discounts, refinery adaptation investments, and the supply diversification value that maintaining a large Russian supply position provides. India boosts Russian and UAE oil purchases ahead of Strait of Hormuz recovery in a manner that reflects long-term strategic intent, not merely crisis opportunism.

How has the UAE strengthened its energy relationship with India during and after the crisis?

Beyond near-record spot crude volumes in both May and June 2026, Abu Dhabi has formalised longer-term energy security arrangements including a commitment to store up to 30 million barrels of crude within India's domestic strategic petroleum reserve infrastructure.

Disclaimer: This article contains forward-looking assessments and projections derived from industry analysis and commodity intelligence data current as of June 2026. Energy market conditions, geopolitical developments, and trade flow patterns are subject to rapid change. This content is for informational purposes only and does not constitute financial or investment advice. Readers should conduct independent research before making any investment or commercial decisions.

Want To Stay Ahead of the Next Major Market-Moving Discovery?

While India's energy strategy reshapes global commodity flows, Discovery Alert's proprietary Discovery IQ model is scanning the ASX daily for significant mineral discoveries with the potential to deliver exceptional returns — explore historic examples of major discoveries and their outcomes on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial at Discovery Alert to ensure you're positioned ahead of the market.