June 14, 2026

The Execution Gap Threatening Southeast Asia's Most Ambitious Industrial Transformation

Across the global aluminium supply chain, the critical question for the coming decade is rarely about where raw materials exist — it is about whether the infrastructure, capital, and policy frameworks to convert those materials into finished products can be built fast enough. Indonesia sits at the centre of this question more acutely than almost any other nation. The country is engineering one of the most structurally complex industrial transitions in Southeast Asian history: a full vertical integration of its aluminium value chain, from ore in the ground to primary metal and beyond.

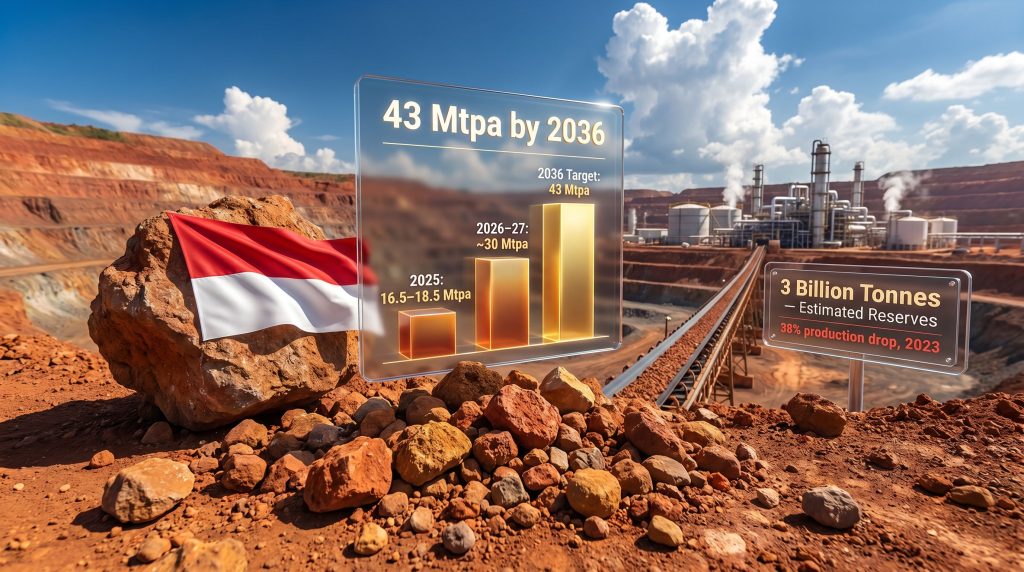

The Indonesia bauxite demand challenge embedded within this ambition is not a geological problem. With approximately 3 billion tonnes of bauxite reserves as of 2025, Indonesia's resource base is not in question. The challenge is operational, financial, and political simultaneously — and it is accelerating in urgency as refinery and smelter capacity outpaces the mine production needed to feed it.

When big ASX news breaks, our subscribers know first

Why Vertical Integration Creates Compounding Feedstock Pressure

Understanding the scale of the Indonesia bauxite demand challenge requires a clear picture of how aluminium is actually made. The production chain follows a strict sequential logic:

- Roughly 2.5 to 3 tonnes of bauxite are required to produce one tonne of alumina through the Bayer process

- Approximately 2 tonnes of alumina are then needed to produce one tonne of primary aluminium via the Hall-Héroult electrolytic reduction process

- This means that every tonne of final aluminium product effectively requires 5 to 6 tonnes of raw bauxite at the start of the chain

This conversion arithmetic means that downstream capacity additions do not create linear increases in bauxite demand — they create compounding ones. As Indonesia adds refinery and smelter capacity, the upstream feedstock requirement escalates disproportionately. The country's 2036 aluminium production targets, when translated back up the value chain, imply an annual bauxite requirement of approximately 43 million tonnes — a figure that dwarfs current operational throughput by a very substantial margin.

Technical note: The Bayer process, developed in 1887, remains the dominant method for refining bauxite into alumina globally. Its efficiency depends heavily on the quality of bauxite feed — specifically the ratio of available aluminium oxide (gibbsite, boehmite, or diaspore) to reactive silica content. Indonesian bauxite, predominantly gibbsite-type, is generally well-suited to the Bayer process but varies in quality across different mining regions, which has implications for refinery yield calculations and operating costs.

How the 2023 Export Ban Reshaped the Upstream Landscape

In mid-2023, Indonesia formalised a ban on raw bauxite exports, extending the resource nationalism logic it had previously applied to nickel. The policy intent was clear: redirect ore flows into domestic processing, accelerate refinery investment, and capture more value domestically rather than exporting unprocessed material.

The immediate market response, however, was the opposite of what policymakers had anticipated in terms of production volumes. Indonesian bauxite output fell by approximately 38% in 2023 compared to 2022 levels. The mechanics behind this contraction are instructive:

- Bauxite miners had historically oriented their entire business model around export revenue from international buyers, predominantly in China

- With export channels closed, the only available market became domestic refineries — but those refineries lacked sufficient operational capacity to absorb ore at pre-ban volumes

- Miners faced a choice between selling at distressed prices to limited domestic buyers or curtailing operations — many chose the latter

- Revenue compression created a secondary problem: reduced cash flows impaired miners' ability to invest in operational maintenance and expansion

This created what industry analysts describe as a feedstock paradox: a policy designed to increase domestic processing inadvertently suppressed the mining activity upon which that processing depends. Furthermore, the downstream was being built while the upstream was contracting, a tension that continues to define the sector today. Understanding global bauxite production trends helps contextualise just how significant Indonesia's self-imposed supply disruption has been on international markets.

Mapping the Demand-Supply Gap: 2025 to 2036

The trajectory of Indonesia's bauxite demand challenge becomes clearer when projected across distinct time horizons. Current operating alumina refinery capacity in Indonesia corresponds to approximately 16.5 million tonnes per annum (Mtpa) of bauxite feedstock demand. This figure is broadly manageable given existing mine output, but the forward curve steepens considerably:

| Timeframe | Projected Bauxite Demand | Notes |

|---|---|---|

| 2025 | 16.5 to 18.5 Mtpa | Near-balanced with current capacity |

| 2026 to 2027 | ~30 Mtpa | Assumes delayed refinery projects commission |

| 2032 to 2035 | ~35 to 40 Mtpa | Dependent on sustained investment pipeline |

| 2036 (target) | ~43 Mtpa | Full value chain realisation scenario |

Important disclaimer: All demand projections are derived from industry modelling based on announced project pipelines and conversion ratios. Actual outcomes will depend on project execution timelines, capital availability, regulatory conditions, and global aluminium market dynamics. These figures should not be treated as confirmed forecasts.

The jump from approximately 16.5 Mtpa today to 30 Mtpa within two to three years represents a near-doubling of bauxite consumption in a compressed timeframe. Achieving this requires not just mine expansion but simultaneous progress across refinery commissioning, logistics infrastructure, water and energy supply to processing zones, and the financing structures that underpin all of it.

The Quality Dimension: Why Not All Bauxite Is Equal

A dimension of the Indonesia bauxite demand challenge that receives insufficient attention is ore quality variability. Indonesian bauxite is predominantly gibbsite-type, which is among the more processable forms of bauxite under standard Bayer process conditions. However, not all Indonesian deposits are equivalent:

- Reactive silica content is a critical quality variable. High reactive silica increases caustic soda consumption in the Bayer process, raising operating costs and reducing refinery margins

- Deposits in West Kalimantan have historically been among the most commercially developed, but grade variability across the province is significant

- Stripping ratios — the volume of overlying material that must be removed to access ore — affect mining economics and can influence which deposits are commercially viable at any given alumina price

- Moisture content affects transport logistics: high-moisture bauxite is heavier and more expensive to move, with implications for port handling and slurry pipeline economics

These quality factors mean that Indonesia's 3 billion tonne reserve figure, while geologically accurate, cannot be uniformly converted into economically recoverable production at any single cost point. The commercially viable subset of that reserve base is smaller, and the cost structure varies meaningfully across different deposits. In addition, the leading bauxite mines globally demonstrate that quality consistency, not just volume, is what ultimately determines long-term refinery competitiveness.

Capital Constraints and the Foreign Investment Dependency

One of the least-discussed dimensions of the Indonesia bauxite demand challenge is the financing gap. Greenfield alumina refinery construction is among the most capital-intensive categories of industrial infrastructure — individual facilities can require investment ranging from several hundred million to over one billion US dollars depending on scale and configuration.

Indonesia's domestic capital markets do not have the depth to finance this build-out independently. This has created a structural dependency on foreign direct investment, with Chinese industrial groups representing a primary source of project capital. This dynamic introduces several complications:

- Geopolitical exposure: Heavy concentration of Chinese investment in Indonesian aluminium infrastructure creates strategic dependencies that Indonesian policymakers are increasingly aware of

- Project risk pricing: International investors apply risk premiums to projects in markets with active export restrictions and evolving regulatory frameworks, raising the effective cost of capital

- Off-take linkages: Foreign investors typically require off-take agreements that direct alumina output back to their own smelting operations, which can limit Indonesia's ability to freely market its refinery output

- Technology transfer constraints: Joint venture structures that favour foreign partners can slow the development of domestic technical capability in refinery operations

For instance, the structure of an alumina refining joint venture can serve as a useful reference point for understanding how equity arrangements and off-take agreements shape domestic value capture in large-scale refinery projects.

A key insight often overlooked in mainstream coverage is that the financing structure of Indonesian alumina refineries directly shapes who captures the economic value of the processing margin. If foreign investors own controlling stakes and hold off-take rights, Indonesia's domestic value capture from the refinery segment may be more limited than headline investment figures suggest.

The next major ASX story will hit our subscribers first

Policy Architecture: The Export Ban Debate and Strategic Alternatives

The central policy tension in Indonesia's bauxite sector is whether the current export restriction framework serves long-term industrialisation goals or whether a strategic recalibration is warranted. The debate has meaningful precedents from other resource-rich jurisdictions:

| Country | Export Policy Approach | Downstream Integration Outcome |

|---|---|---|

| Indonesia | Full export ban since 2023 | Developing, with production contraction |

| Guinea | Volume caps under active discussion | Minimal domestic processing to date |

| Australia | Open export market maintained | Moderate integration, organic pace |

| Brazil | Open export, domestic processing incentives | High integration via major facilities |

| China | Import-dependent, processing mandates | Very high integration |

A conditional export allowance model — where limited ore export volumes are permitted to miners who can demonstrate that domestic refinery capacity is not yet sufficient to absorb their output — could provide a middle path. This approach would preserve miner economics during the refinery build-out phase without abandoning the downstream industrialisation agenda. No such policy adjustment has been formally announced as of mid-2026.

Beyond the export ban, permitting timelines for new mine development represent a separate bottleneck. Environmental impact assessment processes, community consultation requirements, and coordination between national and regional regulatory authorities can extend project development timelines by years. Streamlining these processes without compromising environmental or social standards is a governance challenge that directly affects how quickly additional supply can reach the market. Consequently, major aluminium mining companies operating in similarly complex regulatory environments offer instructive case studies in navigating these challenges efficiently.

The Four Structural Risks of an Unresolved Feedstock Gap

If the gap between bauxite supply and downstream demand is not addressed with sufficient speed, four interconnected risks materialise:

Risk 1: Refinery Underutilisation and Stranded Capital

Refineries operating below nameplate capacity due to ore shortfalls represent significant capital inefficiency. A refinery designed to process 6 Mtpa of bauxite but operating at 60% capacity due to feedstock constraints imposes fixed cost burdens on investors without generating proportional revenue. This dynamic weakens the investment case for subsequent smelter development.

Risk 2: Smelter Development Deferral

Primary aluminium smelters require reliable, competitively priced alumina supply. If Indonesian refineries cannot guarantee feedstock security at acceptable cost, smelter developers will reassess project viability. Deferred smelter investment directly undermines Indonesia's ambition to become a net exporter of primary aluminium.

Risk 3: Regional Socioeconomic Disruption

Bauxite mining is a primary employer in Kalimantan and other producing regions. Prolonged production suppression without compensating growth in downstream employment creates socioeconomic pressure in communities dependent on mining activity, which can translate into political resistance to the broader industrial programme.

Risk 4: Global Supply Chain Reverberations

Indonesia is a material contributor to global bauxite supply. A sustained domestic feedstock gap could simultaneously tighten international bauxite availability — as Indonesian ore is withheld from export — while failing to convert that ore into alumina at scale. The result would be a net negative for both Indonesian industrial ambitions and global aluminium supply chain stability. Indonesia's bauxite supply dynamics have already attracted significant international attention for precisely this reason.

A Credible Three-Phase Roadmap to 43 Mtpa

Closing the Indonesia bauxite demand challenge by 2036 requires sequenced progress across three distinct phases, each with its own priorities and constraints:

Phase 1: Stabilisation and Capacity Recovery (2025 to 2027)

- Restore bauxite mine production to pre-ban levels through targeted investment incentives and potential conditional export adjustments

- Prioritise commissioning of near-complete refinery projects to absorb available ore at existing mine throughput levels

- Establish a national bauxite feedstock registry to improve supply-demand transparency and reduce information asymmetry between miners and refiners

Phase 2: Scaling and Integration (2028 to 2031)

- Commission new mine developments in proven reserve areas, prioritising projects with existing road and port infrastructure access to minimise capital requirements

- Develop integrated industrial zones co-locating mining, refining, and smelting operations to reduce logistics costs and improve feedstock security

- Attract specialised project finance through structured off-take agreements that balance investor return requirements with Indonesia's domestic value capture objectives. A carefully considered downstream processing strategy from other resource-rich nations demonstrates how integrated zone development can accelerate this phase

Phase 3: Full Value Chain Realisation (2032 to 2036)

- Achieve 43 Mtpa bauxite production capacity through a combination of expanded existing operations and newly commissioned projects

- Establish Indonesia as a net exporter of alumina and primary aluminium rather than raw ore

- Develop downstream aluminium product manufacturing capacity to capture further margin across the value chain

Frequently Asked Questions: Indonesia Bauxite Demand Challenge

How much bauxite does Indonesia need to achieve its 2036 aluminium production targets?

Indonesia's 2036 aluminium production ambitions imply an annual bauxite consumption requirement of approximately 43 million tonnes, derived by applying standard conversion ratios across the full bauxite-to-alumina-to-aluminium processing chain.

Is Indonesia's reserve base sufficient to support long-term production at this scale?

Yes. Indonesia holds approximately 3 billion tonnes of bauxite reserves as of 2025, which is more than sufficient in aggregate terms. The challenge lies in the pace at which economically viable subsets of that reserve base can be permitted, financed, and brought into production.

Why did bauxite output fall after the export ban was introduced?

The 2023 export ban closed the primary revenue channel for Indonesian miners before sufficient domestic refinery capacity existed to replace it as a demand source. Miners facing reduced ore sales either curtailed output or operated at a loss. Production fell by approximately 38% in 2023 compared to 2022.

What is the current bauxite feedstock demand from Indonesia's operating refineries?

Active alumina refinery capacity in Indonesia currently generates approximately 16.5 million tonnes per annum of bauxite feedstock demand, projected to reach 16.5 to 18.5 Mtpa in 2025 and potentially 30 Mtpa by 2026 to 2027 as delayed projects reach commissioning.

Reserves Are Not the Constraint — Execution Is

The Indonesia bauxite demand challenge distils to a single insight: geological wealth and industrial ambition are insufficient conditions for success when the execution infrastructure connecting them is under-developed. Indonesia has the reserves, the policy intent, and the industrial vision. What remains is the harder work of synchronising mine production ramp-up, refinery commissioning, project finance, infrastructure development, and regulatory efficiency within a compressed timeframe.

The policy decisions made between 2025 and 2028 carry disproportionate weight. How Indonesia navigates the tension between export restriction and miner viability, how quickly stalled refinery projects are brought to commissioning, and how effectively foreign capital is structured to maximise domestic value capture will collectively determine whether the 2036 target becomes a transformative industrial achievement or a cautionary study in the gap between policy ambition and operational reality.

Strategic perspective for industry observers: When assessing Indonesia's long-term aluminium supply potential, the relevant variable is not the country's reserve base — that question is effectively settled. The operative variable is the rate at which operational bauxite production capacity can be synchronised with the refinery and smelter infrastructure being built around it. That synchronisation challenge, more than any geological or policy factor, defines the credibility of Indonesia's 2036 vision.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly translating complex commodity data across more than 30 resources into clear, actionable investment insights — so subscribers can identify high-potential opportunities before the broader market reacts. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself at the forefront of the next major find.