May 23, 2026

The Structural Architecture of Commodity Control: Understanding Indonesia's Coal Export Overhaul

Global commodity markets have long operated on the assumption that large resource exporters function primarily through private-sector mechanisms, with state entities playing a secondary or regulatory role. That assumption is being tested in real time as Indonesia, the world's dominant seaborne thermal coal supplier, rolls out one of the most significant overhauls of its commodity export architecture in decades. The Indonesia coal export policy through DSI represents a fundamental shift in how the country's most strategically valuable resource flows to international markets, and the ripple effects are already being felt across Asia-Pacific energy supply chains.

When big ASX news breaks, our subscribers know first

Why Indonesia's Coal Market Position Makes This Policy Consequential

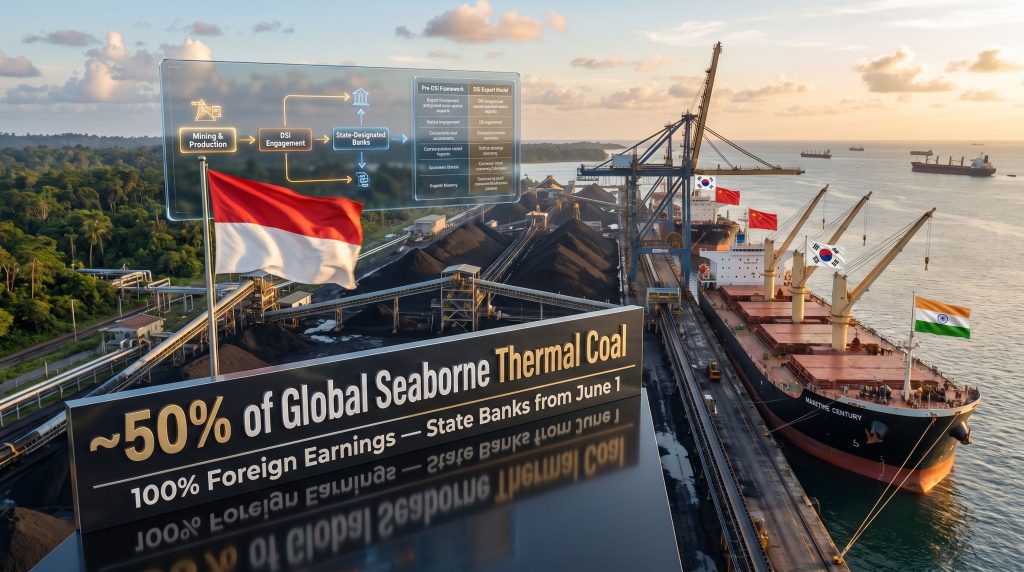

To understand the weight of this policy change, it helps to grasp just how central Indonesia is to the global electricity-grade coal trade. The country supplies approximately 50% of global seaborne thermal coal, a figure that situates it not as one supplier among many, but as the structural anchor of Asian power generation fuel supply. Roughly 80% of Indonesia's domestic coal production is directed toward export markets, meaning the country's policy decisions on export routing carry immediate consequences for power grids across China, India, Japan, South Korea, and Southeast Asia.

This concentration of market influence is further amplified by the current geopolitical backdrop. LNG supply disruptions linked to instability in the Middle East have driven power generators in Japan and South Korea to increase coal consumption as a baseload substitute. That surge in demand is colliding directly with Indonesia's administrative overhaul, creating a timing tension between supply reliability and the mechanics of state restructuring.

The combination of inelastic near-term demand and supply-side policy uncertainty is precisely the kind of market condition that generates price volatility and investor anxiety. Furthermore, these dynamics reflect broader global coal supply challenges that are reshaping how governments and markets approach energy security.

What DSI Is and How the New Export Routing System Functions

The Role of Danantara Sumberdaya Indonesia

Danantara Sumberdaya Indonesia, known as DSI, has been designated as the state intermediary through which exports of coal, palm oil, and ferroalloys must now be routed. The entity sits within Indonesia's broader sovereign wealth infrastructure under the Danantara framework, though its precise operational mandate distinguishes it from a conventional trading enterprise. DSI is not simply buying and reselling commodities in its own right; rather, it functions as an oversight and routing layer through which private export transactions must pass before shipment confirmation.

The initial tranche of commodities brought under DSI's mandate reflects a deliberate prioritisation of Indonesia's highest-value and highest-volume export categories. Whether additional commodity classes, including nickel, bauxite, and other strategic minerals, will be brought under similar oversight in future tranches remains an open question, but the precedent has been established.

The Transition Window and Its Unresolved Questions

Under the policy framework announced by President Prabowo Subianto, a transition period of up to three months has been established. During this window, business proceeds under existing arrangements, but all transactions are subject to DSI oversight. The intent is to provide operational continuity while the new architecture beds in.

However, the transition period has not resolved the most commercially sensitive questions facing miners and traders. As of the policy's announcement, the following remain formally unaddressed:

- Whether compensation to miners will be denominated in US dollars or Indonesian rupiah

- How pricing for export transactions will be determined or verified under state intermediation

- Which party bears logistical and shipping risk under the new routing framework

- The legal status of pre-existing long-term supply contracts between Indonesian exporters and international buyers

- Whether DSI will assume contractual obligations or act purely as a transactional clearinghouse

A parallel regulatory instrument adds further complexity. Effective June 1, all natural resource exporters in Indonesia are required to deposit 100% of their foreign currency earnings into state-designated banks. This foreign earnings retention requirement is the financial architecture underpinning DSI's commercial rationale, providing the government with direct visibility and control over export proceeds.

Structural Comparison: Pre-DSI vs. DSI Export Framework

| Feature | Pre-DSI Framework | DSI Export Model |

|---|---|---|

| Export routing | Direct private-to-buyer | Routed through state intermediary |

| Currency settlement | USD standard | USD vs. rupiah, currently unresolved |

| Foreign earnings retention | Partial domestic retention | 100% in state banks from June 1 |

| Oversight mechanism | Regulatory compliance-based | Active transaction oversight by DSI |

| Transition provisions | Not applicable | Up to 3-month transition period |

| Long-term contract status | Honoured by private parties | Uncertain under new framework |

The Macroeconomic Drivers Behind the Policy

Rupiah Stabilisation and Foreign Exchange Control

The rupiah has experienced significant volatility in recent periods, placing pressure on Indonesia's current account balance and import purchasing power. By centralising commodity export proceeds through state-designated banking infrastructure, the government is pursuing a dual objective: improving foreign exchange visibility and reducing the ability of private operators to hold export earnings offshore.

This strategy has historical precedent. Resource-dependent economies from Angola to Kazakhstan have deployed variants of export centralisation as a currency defence mechanism during periods of exchange rate pressure. The effectiveness of such measures typically depends on enforcement capacity and the extent to which private operators can route transactions through alternative channels.

The 100% foreign earnings retention requirement is not an isolated fiscal measure. It is the financial backbone of the entire DSI framework, designed to ensure that commodity export revenues materialise on Indonesian balance sheets rather than remaining in offshore accounts or correspondent banking arrangements.

Closing the Under-Invoicing Gap

Under-invoicing of commodity exports — where declared export values are artificially suppressed to reduce tax and royalty obligations — has been a documented and persistent source of revenue leakage in Indonesian commodity trade. The practice is particularly prevalent in bulk commodity sectors where physical shipment verification is complex and pricing benchmarks can be manipulated at the contract level.

DSI's oversight function is explicitly designed to address this gap. By inserting a state intermediary into the transaction chain, the government creates a verification layer that makes it structurally harder for exporters to declare prices below prevailing market benchmarks. Whether DSI has the institutional capacity, data infrastructure, and pricing expertise to enforce accurate declarations across the full volume of Indonesian coal exports — which runs into hundreds of millions of tonnes annually — remains a legitimate operational question.

How the DSI Export Process Is Expected to Work

The coal export supply chain under DSI involves a sequence of steps that introduces new administrative nodes into what was previously a more direct private-to-buyer transaction structure. The process is expected to function as follows:

- Mining and production proceed under existing licences held by private operators

- DSI engagement is required before export transactions can be confirmed or shipments authorised

- Pricing verification is applied by DSI to assess declared contract prices against market benchmarks, targeting under-invoicing

- Foreign currency proceeds from completed transactions are deposited into state-designated banks, fulfilling the 100% retention requirement from June 1

- Settlement to miners occurs after DSI processing, with the currency denomination of compensation currently unresolved

- Shipment execution proceeds under DSI's transactional oversight framework

The most commercially sensitive unresolved element sits between steps four and five. The currency in which miners receive compensation matters enormously given current rupiah volatility. USD-denominated settlement protects miners' real revenue, while rupiah settlement at an unfavourable exchange rate could represent a material reduction in effective returns, particularly for operators with USD-denominated operating costs or debt obligations.

Winners, Losers, and Operational Realities

How Different Stakeholders Are Affected

| Stakeholder | Likely Outcome | Key Risk or Benefit |

|---|---|---|

| Indonesian state and DSI | Revenue uplift, reduced under-invoicing | Execution complexity, market confidence |

| Large integrated miners | Manageable compliance burden | Currency settlement uncertainty |

| Small and mid-tier private miners | High administrative friction | Margin compression, cash flow risk |

| International coal traders | Short-term disruption, price volatility | Contract uncertainty, routing delays |

| Asian coal importers (Japan, South Korea) | Potential price increases | Supply continuity risk during transition |

| Indian coal buyers | Pricing uncertainty on long-term contracts | Exposure to spot market volatility |

The Long-Term Contract Problem

One of the most practically significant unresolved issues concerns the fate of existing long-term supply agreements. Coal trade, particularly in the Asian market, is heavily structured around multi-year contracts between Indonesian mining companies and state-owned utilities or large industrial consumers in China, India, Japan, and South Korea. These contracts specify pricing mechanisms, delivery schedules, quality specifications, and dispute resolution frameworks negotiated under the pre-DSI regulatory environment.

The insertion of a state intermediary into this chain raises genuine legal and commercial questions. Does DSI assume the contractual obligations of the Indonesian exporting party? If a shipment is delayed due to DSI processing backlogs, which party bears the demurrage cost? India-based trading firms with long-term contractual exposure to Indonesian coal have flagged these uncertainties as material concerns requiring urgent clarification. In addition, proposals such as an India coal trading exchange could further reshape how Indian buyers navigate these evolving supply arrangements.

Vietnam-based coal trading participants have similarly indicated that export controls of this design typically produce upward price pressure for importers in the short term, driven by administrative friction, increased transaction uncertainty, and potential shipment disruptions during the transition window. This is not merely speculative; it reflects a well-documented pattern from comparable commodity export centralisation episodes in other markets.

The next major ASX story will hit our subscribers first

Indonesia's DMO Framework as a Policy Precedent

Indonesia has previously used the Domestic Market Obligation (DMO) framework to reserve a portion of coal production for domestic power needs, typically requiring miners to sell a set percentage of output to domestic buyers at regulated prices. The DMO experience provides relevant context for understanding how DSI may evolve.

When the DMO was first implemented, private miners faced a period of pricing uncertainty and administrative adjustment before compliance mechanisms were standardised. Some smaller operators experienced cash flow pressure during the transition. Over time, the framework became a predictable cost of doing business, but the initial period of implementation generated friction that parallels the concerns now being raised about DSI.

The key distinction is scale. The DMO regulated domestic sales volumes, a subset of total production. DSI targets the entirety of export transactions, which represents approximately 80% of Indonesian coal output. The administrative and operational complexity is correspondingly larger. Consequently, the Indonesia coal export policy through DSI carries structural implications that extend well beyond any previous domestic market intervention.

Scenario Analysis: Three Possible Outcomes for DSI Implementation

| Scenario | Description | Market Impact |

|---|---|---|

| Smooth Implementation | DSI establishes clear protocols within the transition period; miners and traders adapt efficiently | Minimal long-term disruption; modest short-term price premium subsides |

| Prolonged Uncertainty | Key operational details remain unresolved; contract disputes emerge; buyer confidence weakens | Sustained price volatility; some buyers accelerate diversification to Australian or South African supply |

| Policy Revision | Industry pressure or market disruption forces government to modify DSI scope or mechanics | Short-term relief; longer-term uncertainty about policy direction deters foreign investment |

The Sovereign Risk Premium and Investment Implications

For investors with exposure to Indonesian coal equities, the DSI announcement has introduced a new category of risk into the valuation framework. Sovereign policy risk — the possibility that government intervention materially alters the commercial terms under which private operators function — is now an active variable rather than a background consideration. The relationship between commodity prices and miners is already complex, and this layer of policy uncertainty adds further pressure to earnings forecasts.

The unresolved questions around currency settlement, contract continuity, and logistical liability are not merely operational concerns. They directly affect the earnings visibility of Indonesian coal producers, and earnings visibility is a foundational input into equity valuation. A less predictable operating environment typically commands a higher discount rate, compressing valuations even when underlying commodity fundamentals remain constructive.

Longer-term, if DSI implementation succeeds in improving fiscal capture and supporting rupiah stability, the macro environment for Indonesian investment could improve. A more stable currency reduces the cost of imported capital goods and strengthens Indonesia's external balance. However, that positive scenario is contingent on execution quality that has yet to be demonstrated. For context, Australia's resource export challenges illustrate how policy-driven uncertainty can create market openings for competing suppliers when major exporters introduce structural friction.

Furthermore, the broader context of trade war supply chains is reshaping global commodity flows in ways that intersect directly with Indonesia's policy ambitions. The Indonesia coal export policy through DSI does not exist in isolation; it is being introduced into a market already navigating tariff volatility, geopolitical realignment, and energy transition pressures.

Finally, independent analysis from Indonesian coal export policy researchers suggests that the long-run effectiveness of state intermediation depends critically on the transparency and speed of administrative processes — factors that remain untested at DSI's anticipated transaction volumes.

Key Takeaways: Indonesia Coal Export Policy Through DSI

- Indonesia has mandated that coal, palm oil, and ferroalloy exports be routed through state entity DSI, with a transition period of up to three months

- The policy is designed to reduce under-invoicing, increase fiscal capture, and support rupiah stabilisation amid currency volatility

- A parallel measure requires 100% of foreign export earnings to be held in state-designated banks from June 1

- Critical operational details including currency settlement, contract continuity, and logistical risk allocation remain formally unresolved

- Indonesia supplies approximately 50% of global seaborne thermal coal, making this policy shift a material event for Asian energy markets

- Short-term price increases and shipment disruption are considered probable by market participants during the transition window

- The policy introduces a new sovereign risk premium into Indonesian coal sector investment analysis, with longer-term outcomes dependent on execution quality

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario analyses, and market projections discussed herein involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions related to Indonesian coal sector equities or commodity markets.

Want To Stay Ahead of Major Commodity Shifts Affecting ASX-Listed Miners?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity market shifts — like those reshaping Indonesian coal supply chains — into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.